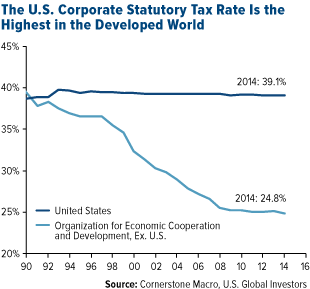

During this month’s Republican presidential primary debate in New Hampshire, businessman Donald Trump took high taxes to task for stunting job growth in the U.S., claiming that “we’re the highest taxed country in the world.”

Several critics and pundits were quick to find fault with The Donald’s comment, pointing out that many other countries have a higher tax rate than the U.S. If you look at tax revenue as a percentage of GDP, the U.S. actually ranks 27 among 34 developed countries, according to the Organization for Economic Cooperation and Development (OECD). (Denmark tops the list, followed by France, Belgium, Finland and Italy.)

|

It’s not the first time Trump has made a wild claim, but in this case he’s right, by one very important measure—the corporate statutory tax rate. Since 1990, this rate has hovered around 39 percent, making it the highest among OECD nations, and for the largest GDP in the world.

Even when compared to 162 other countries, the U.S. still has the third highest corporate tax rate, following the United Arab Emirates (55 percent) and Chad (40 percent), where collecting taxes formally is very difficult.

To his larger point, Trump is right again. High taxes—both in the U.S. and abroad—stand in the way of global growth and create economic friction. But these taxes aren’t the only hurdle, and lowering them would be just the first step in a series of steps to lighten the burden placed on businesses.

The other hurdle is what the Competitive Enterprise Institute (CEI) calls the “hidden” tax—regulation. Complaining about income taxes is an American pastime in its own right, but regulatory costs run much higher, eating up 11 percent of the country’s $17.4 billion GDP.

The $2 Trillion Hidden Pathogen, with No End in Sight

The CEI calculates that in 2014, the annual cost of federal regulation and intervention amounted to a jaw-dropping $1.8 trillion, a figure that exceeds the $1.3 trillion collected in federal income taxes that year. Nearly $400 billion had to be spent on economic regulation alone, $316 billion on tax compliance.

Because these numbers are so large, they can be hard to conceptualize. It isn’t until you look at cost per employee that you realize just how burdensome these hidden taxes really are. In 2012, the last year such data is available, companies in every industry paid an average $9,991 per employee per year. That means if you run a business with 100 employees, you pay close to $1 million every year just to comply with federal laws and regulations. That’s $1 million you could be putting instead toward salaries and benefits and new business growth.

This has helped fuel runaway legal and compliance costs. The Wall Street Journal reported this week that fees at some of the nation’s largest corporate law firms have climbed to an unbelievable $1,500 per hour. That’s 200 times the minimum wage of $7.25, and includes only salaries, not benefits or options.

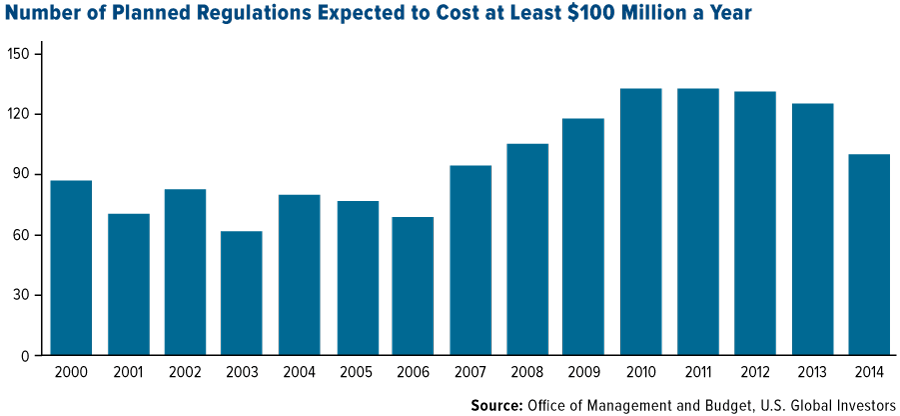

And the rules keep piling up. The chart below shows the number of proposed regulations that cost more than $100 million per year. In 2000, for instance, there were 87 new regulations costing upwards of $100 million, to say nothing of those costing less.

Following the 2008-2009 financial crisis, regulations in the banking sector spiked exponentially, as you can see in the Deutsche Bank chart below. The increase in regulations, not to mention legal costs associated with them, has caused fiscal drag and prevented the formation of capital.

In a 2014 survey conducted by the Centre for the Study of Financial Innovation, global financial leaders cited regulatory pressure as the number one impediment to financial growth right now. We have excessive anti-money laundering laws mandating that every transaction be scrutinized and accompanied by supporting documentation. It’s currently easier to buy marijuana in Colorado than it is to open an investment account. If government can streamline the purchase of weed, why can’t it do the same for investing? The regulators seem to be saying there’s more risk in investing than in smoking dope.

But this is a global phenomenon, a contagion that knows no borders. The countries that place the heaviest burden of regulation on businesses, according to the World Economic Forum, include many in Europe (Serbia, Croatia, Italy) and South America (Argentina, Brazil, Venezuela). As money managers, we see fiscal drag all over the globe as a direct result of taxation through regulation, which tends to favor government work and compliance, not innovation. Private businesses end up paying the price.

The U.S. should be a leader in this area and commit itself to reducing the blockades that impede growth and innovation. A good model for such a task is Canada’s “One-for-One Rule,” introduced in April 2012 during former Prime Minister Stephen Harper’s administration. The rule requires that when a new or amended regulation is introduced, another must be removed.

However it’s accomplished, the time has come to reverse this economy-dragging trend. We also remain encouraged by the Trans-Pacific Partnership (TPP), which promises to eliminate 18,000 tariffs around the globe and unleash trade.

Gold Fear Trade Crackles as Recessionary Worries Hit Market

In times of economic uncertainty and market turmoil, investors have tended to reposition into so-called “safe haven” assets, including gold and municipal bonds. Today is no exception. With talk of a global recession rattling markets around the world, gold had its best start to the year since 1980, putting to rest last year’s speculation that the yellow metal has lost its haven appeal.

Gold is currently up 20 percent year-to-date, compared to a loss of 10 percent for the S&P 500 Index, which adds weight to the belief that the metal works well as a diversification instrument.

Fears of negative interest rates have also spurred record gold investing and retail buying, as the metal acts as a better store of value in an environment where it costs interest to have the government hold your money. Negative rates seem to be the new favorite trick of central banks, from Sweden to Switzerland to Japan, and during her Congressional testimony on Thursday, Federal Reserve Chair Janet Yellen commented that negative rates in the U.S. “aren’t off the table.” Gold shot up $50 by the end of the day.

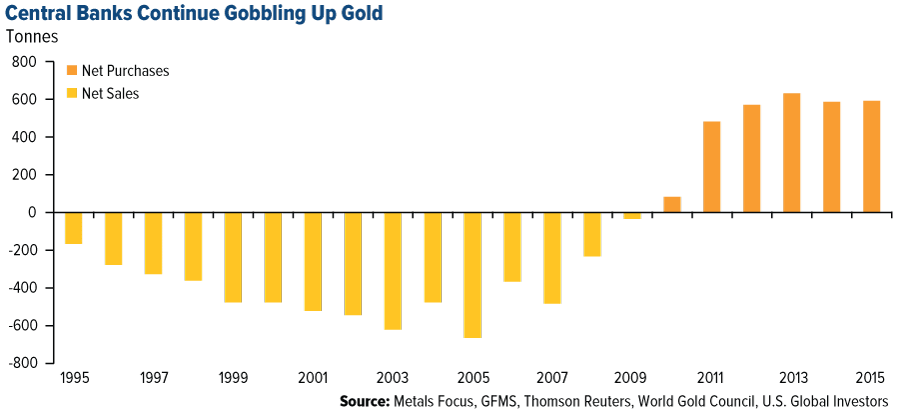

Demand was robust in 2015, with investment up 8 percent from the previous year, according to the World Gold Council (WGC). Central banks continued to add to their reserves, resulting in the second highest annual demand in the WGC’s records. In the fourth quarter, central bank purchases, led by China and Russia, were up an impressive 25 percent over the same quarter in 2014.

|

The smart money seems to think this gold rally isn’t over. As of February 2, money managers’ net long positions surged to a three-month high while short bets declined dramatically, according to data from the Commodity Futures Trading Commission (CFTC). And this week billionaire Mark Cuban, owner of the Dallas Mavericks and “Shark Tank” investor, told CNBC that he had just bought “a lot” of call options in gold, saying: “When traders don’t know what to do, they go where everybody is. And I thought that would be gold.”

Many investors, sensing additional risk in stocks, are likewise seeking shelter and tax-free income in muni bonds. Munis also come equipped with attractive tax advantages, shielding investors from taxes at the federal level and often at the state and local levels too. That means they can help “Obamacare-proof” your interest from the 3.8 percent Affordable Care Act (ACA) tax on investment income (applicable to those who make more than $200,000 in taxable income per year).

In 2015, munis, as represented by the Barclays Municipal Bond Index, were actually the top fixed-income asset class, beating both Treasuries and corporate debt. But they also outperformed S&P 500 stocks, gaining more than double what equities delivered.

Billions of dollars fled domestic equity funds on a near-weekly basis in 2015 as investors anticipated a rate hike, which the Fed finally implemented in December. Meanwhile, muni fund inflows have been positive since October, according to Morningstar, with no signs of slowing in the near-term.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.43 percent. The S&P 500 Stock Index fell 0.81 percent, while the Nasdaq Composite fell 0.59 percent. The Russell 2000 small capitalization index lost 1.38 percent this week.

- The Hang Seng Composite Index lost 5.10 percent this week; while Taiwan finished flat and the KOSPI fell 4.30 percent.

- The 10-year Treasury bond yield rose 8 basis points to 1.75 percent.

Domestic Equity Market

Strengths

- Consumer staples was the best performing sector this week, increasing by 0.80 percent versus an overall decline of -0.91 percent for the S&P 500.

- Akamai Technologies was the best performing stock for the week, increasing 17.50 percent. The company’s shares surged after it reported better-than-expected quarterly revenue (helped by higher demand for its security services), and announced a $1 billion share buyback program.

- Third time was the charm for generic drug maker Mylan NV, which finally came to terms with Sweden’s Meda AB. The company will pay $7.2 billion for the takeover. The cash and stock deal is expected to close in the third quarter.

Weaknesses

- Utilities was the worst performing sector for the week, falling -2.53 percent versus an overall decline of -0.91 percent for the S&P 500.

- Chesapeake Energy was the worst performing stock for the week, falling -48.04 percent. The stock plunged following a report about the company hiring restructuring attorneys.

- According to Thomson Reuters, as of February 9, 2016, 67 percent of S&P 500 companies have reported earnings for the fourth quarter of 2015. The blended earnings growth estimate is -4.1 percent overall, but increases to 2.2 percent when the energy sector is excluded. The blended revenue growth estimate is -3.5 percent, or 0.9 percent excluding the energy sector.

Opportunities

- The defensive consumer staples sector in general, and the soft drinks sub-group in particular, have outperformed smartly of late. Widespread improvement in key soft drink earnings drivers signals additional upside potential.

- Broad global stock indices will not stabilize while global bank stocks are getting crushed. As such, monitoring bank credit default swaps (CDS) for signs of stress is important. Nonetheless, a systemic breakdown in banking in developed markets is unlikely.

- One variable that will likely show improvement before a major bottom in share prices transpires is equity market breadth. The U.S. equal-weighted equity index was underperforming the S&P 500, signifying deteriorating market breadth, well before the S&P 500's recent plunge. Importantly, the equal-weighted stock index is not yet outperforming the market cap weighted index, suggesting breadth is not yet improving and a market bottom is not imminent.

Threats

- U.S. stocks have bounced from highly oversold levels as a result of deeply bearish sentiment; however, this bounce is unlikely to prove sustainable unless accompanied by improving profitability.

- U.S. bank stocks might be cheap, but the deteriorating credit backdrop will be an impediment to an early reversal in fortunes.

- Equities are particularly vulnerable this cycle, as risk premiums have become divorced from fundamentals while the Fed’s balance sheet expanded.

![[thumb]](/images/content_image/data/5b/5b13fa7c428334d4ab251da0c56a463c.jpg)

February 11, 2016Gold is Skyrocketing, Here’s Why |

![[thumb]](/images/content_image/data/af/af209c0e5e7aa480e08d191feee2321d.jpg)

February 10, 2016Frank Tells BNN: Gold Is an Opportunity |

![[thumb]](/images/content_image/data/63/634a571372e20a9d214135bb91fb501e.jpg)

February 9, 2016Frank Holmes Talks Gold with Bloomberg TV |

The Economy and Bond Market

Strengths

- U.S. January retail sales rose a better-than-expected 0.2 percent, and December sales were revised up to 0.2 percent from the previously reported -0.1 percent. Core retail sales, excluding automobiles, gasoline, building materials and food services, jumped to 0.6 percent in January, up from -0.3 percent in December.

- Despite chaotic financial markets and growing recession fears, U.S. weekly jobless claims, a closely watched high-frequency data series, show no signs of trouble for the labor market. Initial claims for unemployment benefits fell 16,000 to 269,000, not far from the post-recession low of 256,000.

- The eurozone economy expanded at a 1.5 percent annualized rate in the fourth quarter of 2015, meeting market expectations.

Weaknesses

- During her semi-annual monetary policy testimony to Congress, Federal Reserve Chair Janet Yellen said that the Fed was quite surprised by the movements in oil prices and the extent of the dollar’s strength. While not ruling out the potential use of negative interest rates should further accommodation become necessary, she did note that the legality of such a move would be unclear. Yellen said it is premature to say a recession is looming, though global financial and economic developments impact the U.S. economic outlook.

- China’s total foreign exchange reserves dropped to $3.23 trillion, the lowest in three years. The country has been forced to sell down reserves in order to slow the yuan’s depreciation.

- Sweden’s Riksbank, the central bank of Sweden, lowered its key interest rate by 0.15 percent to -0.50 percent, despite deepening concerns in the financial markets that negative rates could be counterproductive. Banks have come under severe pressure as profit margins have been squeezed amid flattening yield curves.

Opportunities

- According to BCA Research, the developed market economic and policy divergence has peaked. As a result, the U.S. dollar will remain flat, and perhaps depreciate somewhat, relative to the yen and the euro. This would be positive for U.S. exporters and multinationals.

- The one-month trend of housing starts remains above the three-month trend. This bodes well for next week’s release of January data.

- U.S industrial production is expected to turn in a positive 0.3 percent growth in January from December’s -0.4 percent reading. This would be a welcome development for the economy.

Threats

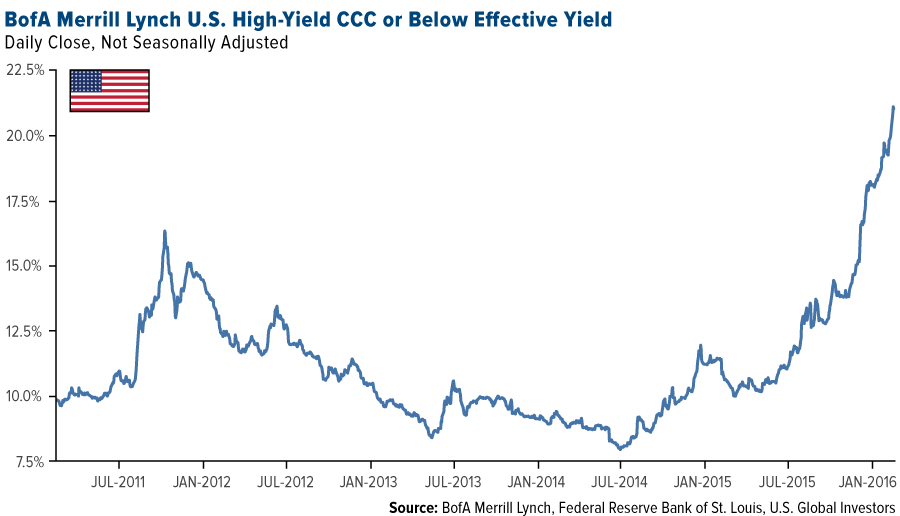

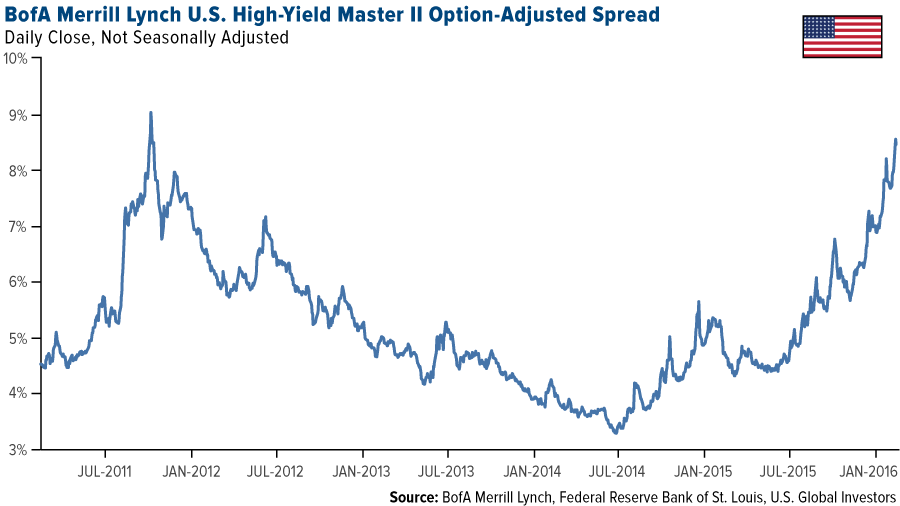

- The pressure on U.S. high-yield bonds has been relentless. Spreads continue to rise and lower quality names (CCC rated or below) are now pushing yields over 21 percent. This tightening of financial conditions poses very negative repercussions for the credit markets and ultimately, the economy.

- A Wall Street Journal survey of economists and CEOs showed that the odds of a U.S. recession in the next 12 months have risen to 21 percent from around 10 percent at the end of 2015. Headwinds from abroad are largely blamed for the higher recession risk.

- Next week European finance ministers, along with representatives of the European Council, ECB and ESM, hope to conclude a review of Greek's adherence to the conditions of the third bailout package agreed upon last summer. A Greek failure to pass the review will trigger a new episode in the crisis and feed into global bearishness.

Gold Market

This week spot gold closed at $1,237.92, up $64.10 per ounce, or 5.46 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, climbed 10.35 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index traded up just 0.59 percent. The U.S. Trade-Weighted Dollar Index slid 1.10 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Feb-11 | U.S. Initial Jobless Claim | 280k | 269k | 285k |

| Feb-12 | Germany CPY YoY | 0.5% | 0.5% | 0.5% |

| Feb-16 | Germany ZEW Survey Curent Situation | 55.0 | -- | 59.7 |

| Feb-16 | Germany ZEW Survey Expectations | 0.0 | -- | 10.2 |

| Feb-17 | U.S. Housing Starts | 1175k | -- | 1149k |

| Feb-17 | U.S. PPI Final Demand YoY | -0.6% | -- | -1.0% |

| Feb-18 | U.S. Initial Jobless Claims | 275K | -- | 269k |

| Feb-18 | U.S. CPI YoY | 1.3% | -- | 0.7% |

Strengths

- The best performing precious metal for the week was gold, up 5.46 percent. This follows 54 tonnes of gold ETF purchases in January. Central banks in the fourth quarter increased their demand for gold by 25 percent, according to the World Gold Council, as a haven from oil’s slump and concerns about a stumbling economy, as seen in the chart below.

- The Economist calls gold’s surge past $1,200 an ounce this week a “hedge against ignorance,” pointing to question marks hanging over the global economy, some of which include China’s economy, falling oil prices and the fragility of global banks. Even as gold prices fell on Friday, the metal headed for its biggest weekly jump since 2011, reports Bloomberg.

- Tahoe Resources announced its definitive agreement this week to acquire Lake Shore Gold. TD Securities reports that the offer represents a 14.8 percent premium to the closing price of Lake Shore shares on Friday and a 25.7 percent premium to the 20-day volume weighted average price (VWAP) for the period ending Friday.

Weaknesses

- The worst performing precious metal was palladium, still up 4.26 percent for the week. Palladium is likely being pulled up with spreading interest in precious metals to hedge general market risk.

- It seems that even gold bulls failed to imagine just how much the precious metal could soar this year, reports Bloomberg, adding that gold prices have surged past three-quarters of the peak forecasts in a mid-January survey by the London Bullion Market Association. In another article entitled “Gold’s Monkey Magic Seen Fading after Biggest Advance Since 1980,” Bloomberg reports that 12 analysts surveyed believe gold will drop this month as Chinese consumers slow purchases that surged before the start of the Lunar New Year. Prices could drop to $1,100 an ounce from Monday’s $1,200 high, say seven additional analysts providing forecasts.

- After the market close on Wednesday Franco-Nevada announced a $500 million “bought deal” to fund the acquisition of future production from a mine owned by Glencore and the book was filled that evening with prospective investors wearing the overnight risks until allocations were to be announced at 7:30 a.m. before market open. Unfortunately, gold prices jumped $50 on Thursday and demand surged for the offering since all the late comers to the party wanted a crack at getting some free money since the price of the offering had been fixed the prior day.

Opportunities

- Gold climbed to the highest in a year as investors reacted to Janet Yellen’s suggestion that the central bank may delay raising interest rates, reports Bloomberg. Investors poured money into the precious metals markets this week, with $1.6 billion of total money tracked by Bank of America Merrill Lynch buying up gold and other precious metals including silver and platinum. To emphasize the fears wracking markets, Business Insider reports that the biggest outflows last week were seen from three risky asset areas: $6.8 billion from equities, $2.5 billion from high-yield bonds and $1.1 billion from emerging-market government debt. This could just be the first wave of money beginning to buy gold.

- There seems to be a correlation between the UK’s net gold export and China’s wholesale gold demand, implying gold imports by China are supplied by London, reports Goldseek. In December 2015, the UK gross exported 213 tonnes of gold, the second-highest number on record. In addition, Raymond James reports this week that gold valuations have room to run. The group says that prior to gold’s recent bear run they often looked at the gold price to gold stock ratio, with the ratio touching an all-time high of 28X this past January. They continue by noting that a more normal paradigm could range from 16X to 13X, still far below today’s valuations. Circling back to the news of Tahoe Resources’ bid to buy Lake Shore Gold, we expect there to be more acquisitions of Canadian and Nevada based assets as it is still likely cheaper to still buy assets in or near production in these prime locations.

- The CIO of JPMorgan, Robert Michele, believes that this week’s precious metals flight shows retail investors have more confidence in gold than in paper money. Jeffrey Gundlach, founder of DoubleLine Capital, added to this belief by Tweeting that investors are losing faith in central banks and gold could hit $1,400 an ounce.

Threats

- Sweden’s central bank shook markets this week with a rate cut of 0.15 percent, now at -0.50 percent. Bank shares plunged in reaction to the cut, with Societe Generale down 13 percent, Deutsche Bank down 7 percent and Santander down 6 percent.

- There are “no limits” to how far central banks can ease monetary policy, reports Bloomberg, stating that this is a recent declaration of both the ECB President Mario Draghi as well as Bank of Japan Governor Haruhiko Juroda. These leaders have joined their counterparts in Denmark, Sweden and Switzerland to embrace interest rates of less than zero. JP Morgan’s economist reported in a recent study that the ECB could cut rates to -4.5 percent and the Fed to -1.3 percent. They strongly cautioned investors that there appears to be a lot of room for central banks to probe how low rates can go stating, “We believe it would be a mistake to underestimate their capacity to act and innovate.”

- Goldman Sachs predicts losses over the coming year for gold, despite the precious metal’s rally this week, citing the Fed’s interest rate increases over no fewer than three times. The group forecasts that bullion will be at $1,100 in three months, reports Bloomberg. Supporting Goldman’s view, gold’s relative-strength index, an indicator that tracks momentum, has climbed over 70, reports Bloomberg. This indicates to some analysts that prices will fall.

Energy and Natural Resources Market

Strengths

- Midland crack spreads rose three-fold this week, rising to the highest level this year, as numerous key events coincided. For starters, crude inventory builds at key storage locations in the U.S. increased availability of inputs, while a booming gasoline price boosted revenues for refiners. In addition, refiners are beginning their heavy spring turnaround processes which normally result in significant capacity cuts, thus limiting the availability of refined product.

- The best performing sector for the week was gold mining. Gold miners rallied 10 percent for the week as gold prices rose to their highest level in a year, capping the best weekly performance for the yellow metal since 2008.

- The best performing stock for the week in the broader natural resource space was Goldcorp. The Canadian miner rose 14 percent for the week, catching up with some of its senior gold peers, which it had lagged year-to-date.

Weaknesses

- Crude prices dropped more than 5 percent for the week after Iran began offering crude cargoes at a discount to Saudi Arabian benchmark prices. This move is not surprising as it is the only way Iran can re-establish higher export volumes in the current heavily oversupplied market.

- The worst performing sector for the week was MLPs. The Alerian MLP Index declined over 10 percent for the week as Credit Suisse moved to downgrade a number of its largest holdings, arguing their valuations are too rich given the current oil price environment. The Swiss bank also expects distribution growth to decline, which should result in multiple-compression.

- The worst performing stock for the week in the S&P Global Natural Resources Index was ArcelorMittal. The Luxembourg-based steel marker declined 17 percent for the week after missing earnings expectations, and announcing it may seek to raise $3 billion through a rights issue.

Opportunities

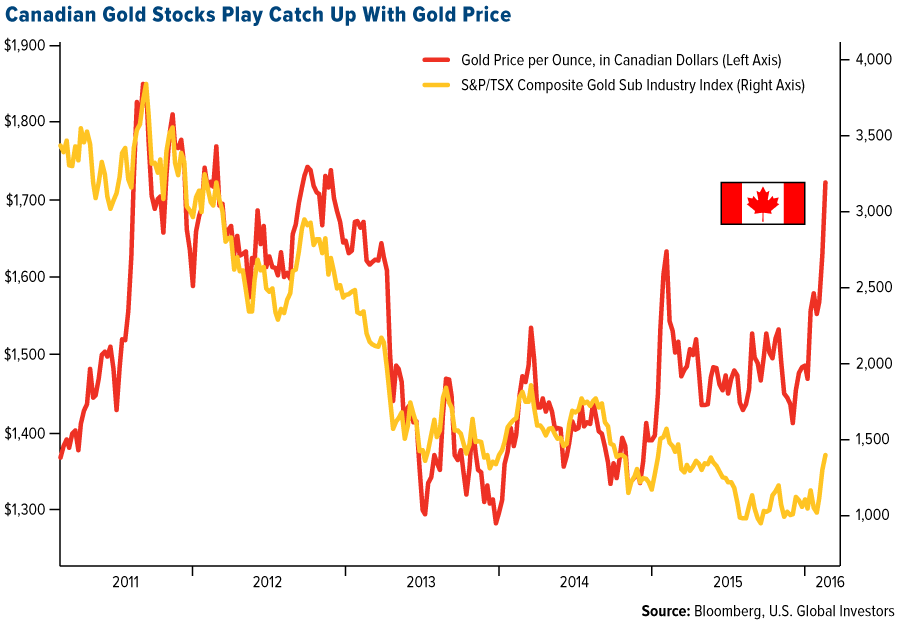

- Canadian gold miners have a lot of catching up to do. Despite a spectacular start to this year, with Canadian gold miners rallying 36 percent year-to-date, the miners have yet to price in the advance of gold in Canadian dollars. Since their respective peaks in 2011, the Canadian-dollar gold price has recovered, and is now only 9 percent below its all-time high. The same is not true for the miners, which are 63 percent below their peak, thus lagging the recent performance of the metal, and setting up a significant re-valuation opportunity.

- Mining M&A is set to rebound in 2016 as financial distress and forced divestitures incentivize deal making. After five years of M&A volumes and values declining, Ernst & Young, the global consultancy company, suggests the mix of available private capital and distressed mining balance sheets may lead to a rebound in the volume of deals this year.

- Base metals prices may be set for a rebound as London Metals Exchange (LME) inventories have remained on a sustained downward trend. Over the last five months, copper inventories are down 33 percent, zinc stocks are down 25 percent and aluminum stocks are 16 percent lower according to VTB Capital report.

Threats

- Oil prices may be depressed for longer as the International Energy Agency (EIA) suggests the global oil surplus will be bigger than previously estimated. Supply may exceed consumption by an average of 1.75 million barrels a day in the first half of 2016, compared with an estimate of 1.5 million published just last month, according to the IEA.

- Crude inventories in the U.S. may continue to rise, adding to a supply glut as refiners reduce production runs. Cuts in refinery runs mean more crude oil goes into storage. Cushing, Oklahoma, the major delivery point for U.S. crude, already has a record amount of inventories.

- Fertilizers and agricultural chemicals will continue to see price pressure as the U.S. Department of Agriculture forecasts that farmers will face a drop in farm economics for the third straight year as persistent surpluses depress crop and livestock prices.

China Region

Strengths

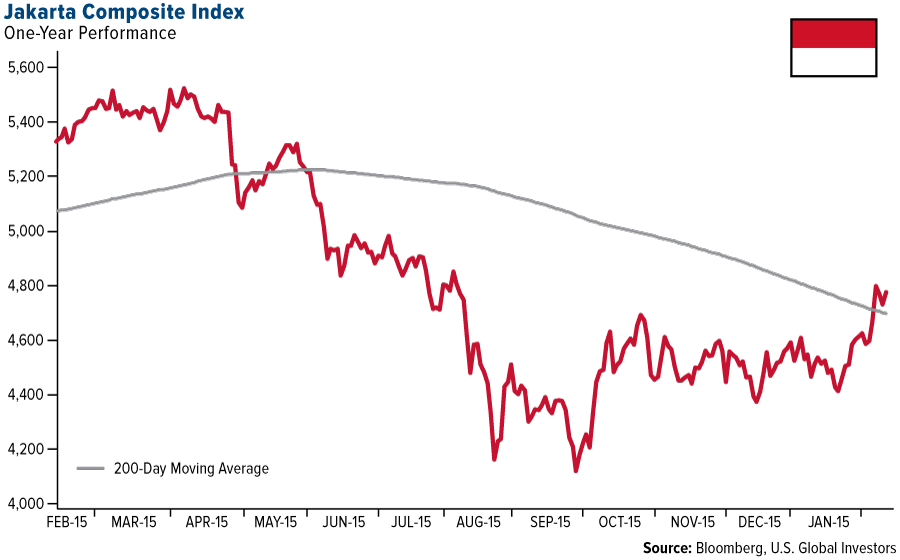

- Following Indonesia’s stronger-than-expected fourth quarter GDP print last week, which came in year-over-year at just above 5 percent, the Jakarta Composite Index remained among the strongest performers in the region throughout this holiday-shortened week. The island nation’s currency, the rupiah, strengthened by about 1 percent on the week.

- Hong Kong’s Secretary for Financial Services and the Treasury, K. C. Chan, reassured investors this week that the city can withstand attacks on its currency, thanks to large FX reserves and assets. Reuters reports Chan saying that, “The foreign reserves and assets we have today far exceed the last time the peg was attacked.”

- The number of visitors to Macau during the early part of the Lunar New Year holiday weekend came in higher this year, with overall tourist arrivals up by 5.2 percent year-over-year. Mainland tourists rose by some 6.7 percent in the same time frame, perhaps a positive sign for beleaguered Macao casinos.

Weaknesses

- A violent riot broke out in the Mong Kok district of Kowloon in Hong Kong during the Lunar New Year celebrations earlier this week, resulting in scores of injuries and arrests and marked by warning shots fired from police. The violence of the riots—allegedly sparked by a police shutdown of illegal hawker stalls—drew media attention for the seemingly stark difference to the relatively peaceful pro-democracy “Occupy Central” movement of 2014.

- The Hang Seng Composite Index fell to new 52-week lows after Hong Kong’s Lunar New Year holiday.

- South Korea’s KOSPI Index fell to new 2016 lows.

Opportunities

- As mainland China, Taiwan and Vietnam reopen following Lunar New Year celebrations, markets will assess whether the lengthy holiday period brought any respite to the negative sentiment and uncertainty marking global and regional markets of late. This weekend, China will also release its import and export data for January.

- Ahead of a U.S.-ASEAN summit in California next week, reports suggest that more countries from the Association of Southeast Asian Nations (ASEAN) have expressed interest in joining the Tran-Pacific Partnership, or TPP, including Indonesia, the Philippines and Thailand.

- China plans to expand yuan convertibility in free trade zones, according to Reuters.

Threats

- As mainland China returns to work next week, investor attention may once again be drawn to heightened scrutiny of Chinese policymaking and the country’s slowing growth, capital outflows and currency stability.

- Tension rose again this week between North and South Korea, with South Korea shutting off water and electricity supplies to an inter-Korean industrial area after North Korea seized equipment and products in the South Korean portions of the complex. Tension around the demilitarized zone between the estranged countries has been higher since North Korea’s latest missile tests, and comes as the U.S. Congress sends President Obama a bill to escalate sanctions against North Korea.

- Recent and ongoing volatility may continue to weigh upon the region and sentiment.

Emerging Europe

Strengths

- Ukraine was the best performing market this week, gaining 1.05 percent. The country has agreed on a restructuring deal with Russia's Sberbank on $367.4 million of state-guaranteed debt.

- The Romanian leu was the best performing currency this week, gaining 1.24 percent against the U.S. dollar. Gross domestic product expanded by 3.7 percent from 3.6 percent a year ago.

- The information technology sector was the best performing sector among Eastern European markets this week.

Weaknesses

- Greece was the worst performing market this week, losing 9.4 percent. Once again the Athens Stock Exchange Index was pulled down by banks as Greek creditors are discussing the status of its first bailout review.

- The ruble was the worst relative performing currency this week, losing 1.19 percent against the U.S. dollar. Crude oil retreated toward $30 a barrel and the Bank of Russia said it sees no reason to intervene in order to prevent the currency weakness.

- The consumer staples sector was the worst performing sector among Eastern European markets this week.

Opportunities

- The diminishing prospect of a rate rise in the U.S. strengthened the euro against the dollar and at the same time made the European Central Bank’s (ECB’s) task to bring inflation closer to its target of 2 percent more difficult. An economist at JPMorgan Chase said that they expect the ECB to reduce the deposit rate, the rate ECB charges to park funds overnight, in March to -0.5 percent from the current -0.3 percent. A later policy shift could cut the rate to -0.7 percent. Quantitative easing and deposit rates are some of the most important tools of eurozone monetary policy.

- Hungary’s central bank will start buying non-performing commercial loans after the European Union (EU) approved a plan intended to clean up the bank’s balance sheets and boost corporate lending. According to the central bank’s estimates, the non-performing loan ratio should decline from the current 15 percent to just over 5 percent by 2017.

- Eastern European countries are growing at a much faster pace than the eurozone area. Poland’s GDP rose 3.9 percent year-over-year, followed by Romania at 3.7 percent and Hungary at 3.2 percent. Eurozone aggregate GDP was reported at 1.5 percent. Rising domestic demand, low rates and weak oil price support growth in Emerging European countries.

Threats

- German industrial production suffered a sharp decline in December, raising fears over economic growth in the eurozone's biggest economy. Industrial production declined 1.2 percent month-over-month and a 2.2 percent decline was reported for the year-over-year period. Germany is considered a locomotive to the eurozone area and a slowdown in Germany could have implications for the economic growth of this 19-members bloc.

- According to JPMorgan, investors are demanding more than 500 basis points to hold developing nation debt over U.S. Treasuries for the first time since 2009, pointing to declining appetite for risk. The premium, which rose 12 basis points to 506 on Thursday, has widened 43 basis points this month.

- Recent comments in a Polish newspaper suggest that Finance Minister Pawel Szalmacha may leave the office. Szalamacha’s departure could prove unsettling to the Polish market as he has been firm on keeping the country’s deficit under 3 percent of GDP and opposes scrapping the private pension scheme. If he were to go, bond yields could go higher.

(c) US Global Investors