Advice for Riding This Market's Rocky Rebound

Posted by

Posted by

Dr. Brian Jacobsen, CFA, CFP®

Summary:

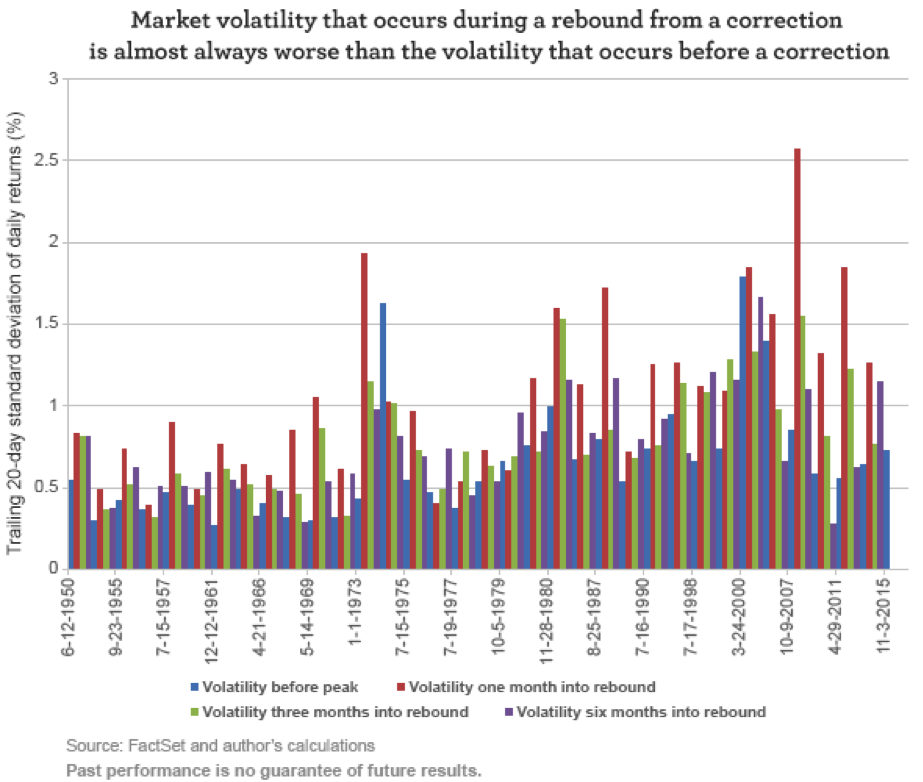

- Where should you be positioned in a rocky market rebound? History shows that volatility that occurred during rebounds from corrections was almost always worse than volatility that occurred before.

- Investors need to consider the fact that—while waiting in cash positions can be comfortable—it can also be costly if you miss out on buying opportunities.

- Wells Fargo Asset Management’s Dr. Brian Jacobsen offers insights on portfolio positioning, looking at factors such as market capitalization and sector.

The S&P 500 Index dropped to an intraday low of 1,812 on January 20. Will that be the lowest of the market’s lows? It’s possible, but there are still risks and plenty of unknowns yet to be resolved. Will China keep successfully propping up its economic growth? Will oil prices stabilize? Will the dollar keep strengthening? Will U.S. manufacturing weakness contaminate service sector strength?

Weak first-quarter earnings could be a threat, although maybe the price declines we’ve seen since S&P’s last peak in November have factored in an anticipation of the weak data rather than a reaction to it. Markets will likely move well before things get resolved. So, investors need to consider the fact that—while waiting in cash positions can be comfortable—it can also be costly if you miss out on buying opportunities.

The market volatility that occurred during a rebound from a correction historically was almost always worse than the volatility that occurred before a correction.

Coming out of the 26 corrections and 9 bear markets we’ve had in the U.S. since 1950, volatility that occurs one month into a rebound (measured by the trailing 20-day standard deviation of S&P 500 Index daily returns) has been approximately 1.8 times the volatility that prevailed before the correction began. For example, the standard deviation of daily returns in the 20 days before the November peak was 0.73%. My calculations suggest we should expect volatility of around 1.3% in the month coming out of the correction. It’s been about 1.27%, so that’s pretty close.

Knowing that market volatility is an expected variable doesn’t necessarily make it easier to stomach. That’s why cash management, maintaining precautionary balances, and keeping your long-term portfolio diversified are so important. However, knowing what causes a correction might help soothe the stomach and the heartburn that volatility brings.

The narrative around what caused the most recent correction may never be settled, but I think it was triggered by the same factors as the correction that ended in August: fears over China’s economy slowing, fears over what deflation actually means, and anticipation over what the knock-on effects will be for global growth. In a way, this is just a variant of the three primary causes of corrections: growth fears, inflation (or deflation) fears, or geopolitical issues. Considering the similarities to the summer market swoon, perhaps the current rebound will look similar with large-cap growth stocks and energy shares leading the way.

Where should you be positioned in the rebound?

On that note, let’s think about the future. Where should you be positioned in the rebound? As you consider how to approach portfolio construction, it’s important to keep in mind that not every correction plays out the same way. So for the 35 episodes I studied, I looked at the performance of the stock market from two different perspectives.

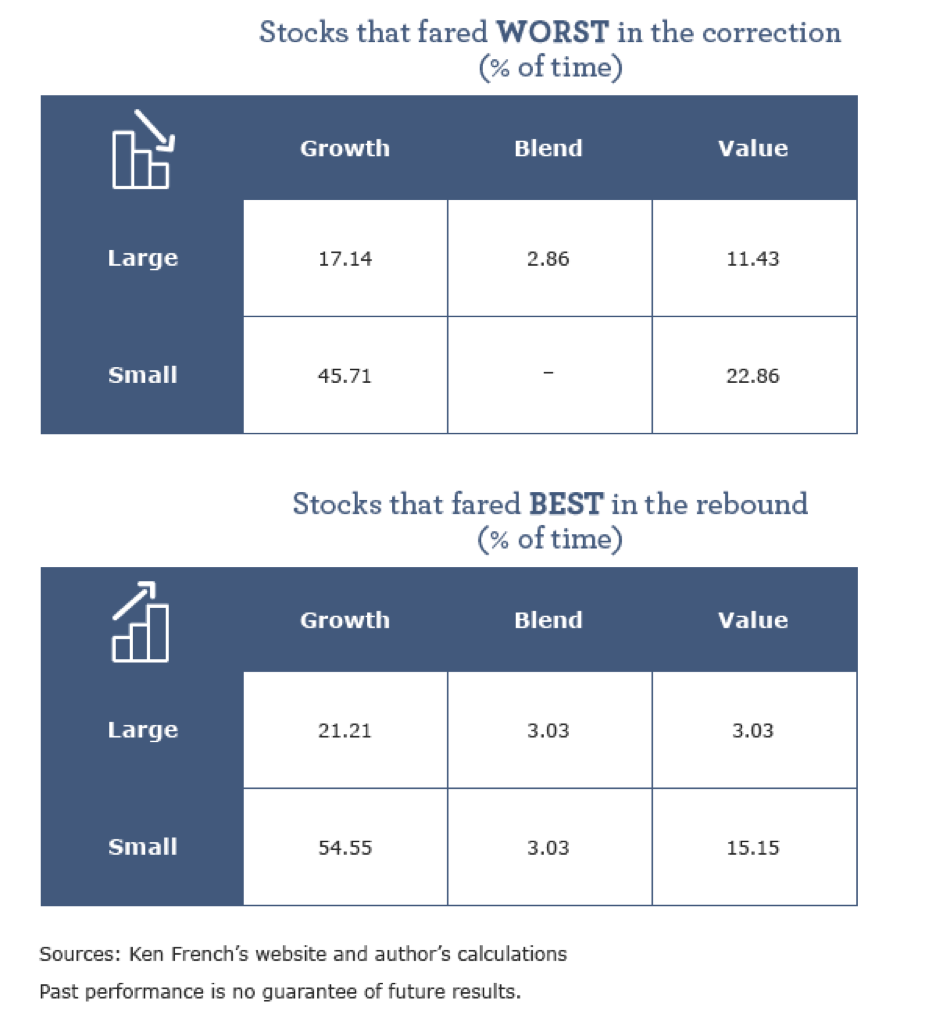

- Slice and dice the U.S. stock market by capitalization (large versus small) and then by style (value, growth, or a blend).

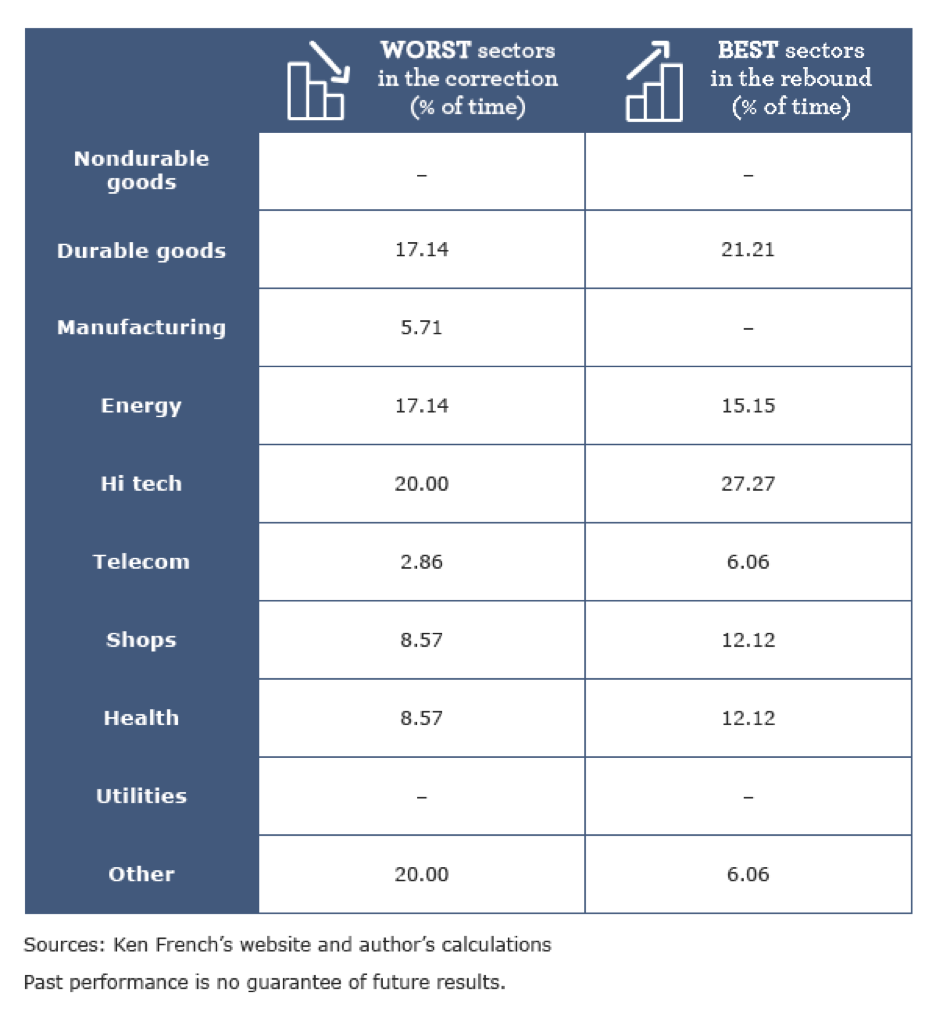

- Or, instead of size and style, you can look at the performance by sector. To do this, I used the data available from Ken French’s website. He’s been providing daily return data on U.S. markets going back to 1926.

Corrections are usually small-cap phenomena, with small-cap stocks doing worse than large-cap stocks. The recent correction is no different, with small-cap value performing the worst in the downturn. That’s the same category that fared the worst in the 1971, 1975, 1979, 1989, 2010, 2011, and 2015 corrections.

However, what goes down typically goes back up. Coming out of the summer 2015 correction, large-cap growth led the way up, but in 2011—after small-cap value led the way down—small-cap growth charged ahead. That was after just one month. Looking out six months into the rebound, small-cap growth typically did best coming out of all previous corrections and bear markets. In a way, it paid to “get your beta on.”

By broad sector, it’s widely known that energy performed the worst in recent months. However, after the summer 2015 correction, energy was the best-performing sector. The last time energy was the worst-performing sector in a correction was in 1982 after the oil price boom was followed by a bust. In the 1982 market rebound, consumer discretionary (especially shops, referring to retail) did the best. That could have been because lower oil prices fueled higher consumer spending (eventually), as the economy emerged from the double-dip recession of the early 1980s. I’d say all of this sounds quite familiar to what we’re experiencing now.

It’s hard to think one month out—or better yet, a few years out—when you’re living in the midst of the volatility. But those hard times are also when it’s most important to keep a long-term perspective.

*A note to readers on Ken French’s research. These indexes are sometimes known as the “Fama-French Indexes” because French worked with a co-author (Eugene Fama) in developing some of the theory and empirical support for modern notions of investing by various factors, such as size and style. Most popular indexes only go back a couple decades, so while it’s easy to argue with whether the Fama-French Indexes are the best way to classify stocks according to size, style, or sector, it’s perhaps the best available to look for long-term regularities.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 2-9-16 and are those of Dr. Brian Jacobsen, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management