- China Faces Capital Punishment

- Should We Be Concerned About Financial Conditions?

The Great Wall of China is one of the seven wonders of the modern world. Its origins date back more than 2,000 years; it runs for more than 5,000 miles, through mountainous terrain that made construction very difficult. It is a singular feat of engineering.

Almost from the very first, though, the Wall has required a good deal of maintenance. The earliest sections were fashioned from earth and gravel; the use of brick and mortar came later, but even the best masonry is vulnerable to the ravages of weather (not to mention invading hordes). As a result, the Wall presently has a number of gaps.

The Chinese are presently giving a lot of consideration to gaps in a different kind of barrier, one that restricts the flow of money instead of people. Despite a system of controls, capital has left the country in significant amounts, pressuring Chinese markets and the Chinese currency.

This has challenged Chinese officials, who aspire to have a more open economy but are committed to preserving financial stability. The choices Chinese investors and policymakers make in the months ahead will significantly influence international markets.

Globalization has been a persistent theme over the last generation. The flow of goods and capital across borders has grown geometrically since the early 1980s. In theory, removing barriers allows greater choice for consumers and investors and lets countries specialize in what they do best.

Modern portfolio theory suggests that diversification increases expected return and reduces variance. This is very much true in an international context; owning a global basket of assets is better than concentration in any single country or currency over the long term. Free capital markets also allow movement from weaker markets to stronger ones when opportunities arise.

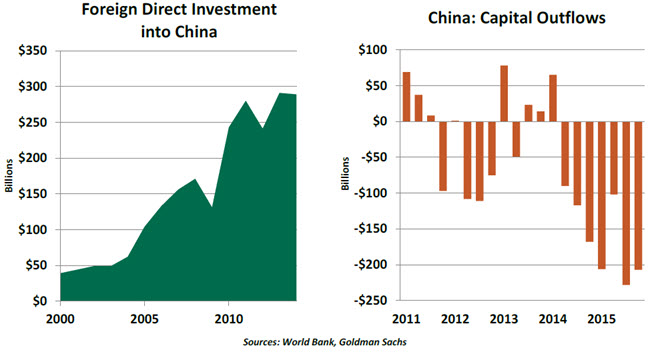

Few countries benefitted more from inbound investment than China has over the last 30 years. The market opportunities attracted corporate and individual interest, which generally has been well-rewarded by China’s exceptional expansion.

But China’s economic growth has diminished, its currency weakened, and many see a range of its assets as overvalued. This has prompted a very natural reaction: portfolios are moving in other directions. An estimated $650 billion departed the country last year.

And it’s not just foreigners who are reallocating assets; Chinese investors are also moving their money away from home. China’s recent prosperity created immense wealth, an estimated 30% of which is owned by the top 1% of the population. Apart from seeking portfolio diversity, some fear that anti-corruption forces will reach them and confiscate assets.

Some analysts are less troubled by the recent outflows. They observe that some of the capital was forwarded to China’s “One Belt, One Road” effort, which seeks to invest in infrastructure throughout Eurasia. Some of it was used to pay down foreign debt, in advance of the RMB weakening against the U.S. dollar. A fraction also represents foreign companies performing routine repatriation of profits.

Still, it does appear that capital is fleeing because the risk/reward dynamic in China is less favorable than it once was. This places downward pressure on Chinese markets and increases pressure on ventures that relied on a stable pool of capital. Together, these developments place pressure on Chinese banks and the Chinese economy.

China has been very cautious about managing capital flows, having observed what happened to several of its neighbors in 1997-98. Emerging Asian “tigers” accepted a lot of inbound investment and used it for long-term development. But they left the door open for capital to depart when times turned. The mismatch of time horizons proved very damaging.

China consequently controlled capital outflows in various ways. For a long time, the Chinese currency was not convertible, which made it exceptionally difficult to take capital out of the country. While that policy was eventually relaxed, official rules allow citizens to “export” only US$50,000 annually, and foreign enterprises have to apply to withdraw equity.

But these rules are routinely flouted in overt and covert ways. This is clear from the scale and extent of Chinese property ownership in major world cities. Chinese officials could certainly stop the outflow by tightening controls on capital. But this might be seen as a panicked reaction. If not done comprehensively, some of the Chinese nouveau riche might intensify their evasive efforts.

Further, tighter capital controls would run counter to the country’s stated aspiration to allow freer movement of capital across its borders. It would be viewed as a significant backward step and potentially hinder the willingness of foreigners to invest as much in China.

Chinese policymakers will also be challenged to mediate between investors and exporters. As investors leave, they exchange their RMBs for other world currencies. This reduces the value of the RMB, which in turn reduces the value of RMB-denominated assets. To prevent this negative spiral from progressing, Chinese officials used their official reserves to support their currency. This is an expensive effort, one which hinders Chinese companies that want to sell their wares more cheaply overseas.

Chinese reserves are still formidable, but they are needed on a variety of fronts: foreign exchange management, bank recapitalization and economic stimulus, among them. To preserve them, China allowed the RMB to depreciate modestly since last summer. This reduced the scale of intervention required in the currency markets, and the downward move has been small enough not to alarm investors. But the current equilibrium is very tenuous.

Free capital markets can be a scary thing. But trying to control them can be equally frightening. The Great Wall was constructed to keep out marauders; Chinese officials must now decide whether to tighten their financial defenses against unwelcome departures.

Changing Signals on the Fed’s Radar Screen?

Following the Great Recession, financial conditions became an important ingredient in monetary policy discussions, as it was recognized that they bear significantly on real economic developments. This subject has featured prominently of late in remarks by Federal Reserve officials. Chair Janet Yellen testified before Congress earlier this month that “financial conditions in the United States have recently become less supportive of growth.”

It is dangerous to ignore the potential impact that capital markets can have on economic growth. But recent concern over financial conditions may be overdone. Private observers and policymakers should be careful not to overreact to what may be a fleeting signal.

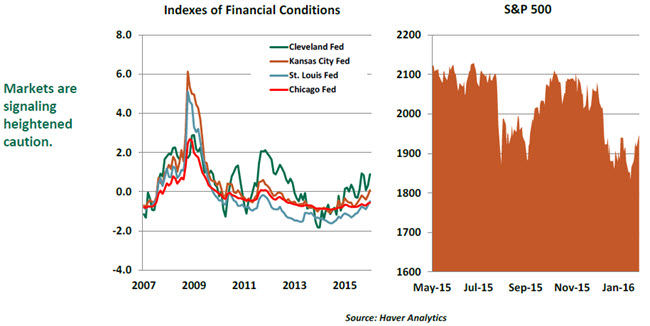

Financial conditions define the current state of financial variables that affect economic behavior and consequently the future state of the economy. Researches have put together financial conditions indexes (FCI) to assess whether there is stress in the financial system. The peaks of the FCIs correspond closely with peak phases of financial crises. Turning points closely match known U.S. economic and financial turning points.

The variables included in specific FCIs vary, but they share similarities. Most FCIs include measures of short-term interest rates, long-term interest rates, credit spreads, market volatility, exchange rates and equity market performance. The chart below plots four FCIs from the different Federal Reserve Banks.

Despite the variance in coverage and methodology, the four Federal Reserve Bank FCIs are showing similar trends at the present time. Positive values indicate financial conditions are tighter than average, and negative values suggest below-average financial stress. Each of the four FCIs is higher relative to the situation a few months ago. But, more importantly, they are still well below regions that might be suggestive of economic contraction.

The January 2016 Federal Open Market Committee meeting included an extended discussion about financial conditions. At that time, the Fed concluded that domestic financial conditions had tightened, consistent with the message of the FCIs. It also held that if these developments persist, it will be “roughly equivalent of a firming of monetary policy.” Some analysts have calculated that impact to be about 75 basis points of tightening.

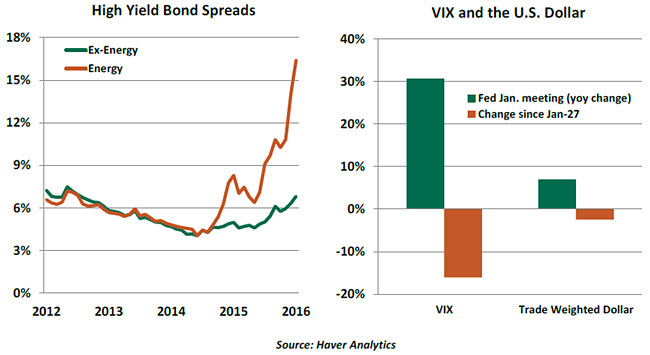

The Fed narrowed the focus of financial conditions to four indicators – equity prices, credit spreads, market volatility and the dollar’s foreign exchange rate. The message from each of these indicators featured in the FCIs suggests that pressure on credit conditions has diminished importantly in the last month.

Equity prices had dropped almost continuously since the beginning of 2016. The Fed was concerned that a further decline would translate into an unfavorable wealth effect and lower consumer spending. But equity prices have recovered a portion of the losses seen at the January meeting. The Standard & Poor’s 500 stock index stands about 7% higher than the bottom it touched earlier this month.

The recent widening of credit spreads should be also viewed with caution. Investment-grade and high-yield bond spreads have widened. But within the universe of high-yield bonds, a differentiation between energy and non-energy high-yield bonds is critical. Energy-related industries are in the doldrums following the sharp plunge in oil prices. It is not surprising that credit spreads on energy-sector issues show a markedly different path than issues related to other economic sectors.

Yields on investment-grade bonds have risen more modestly. Companies with solid ratings are not being constrained from issuing debt.

Market volatility as measured by the Volatility Index (VIX) shot up in mid-January as equity prices fell and global risks were perceived to be higher than previously estimated. Higher VIX readings encourage investors to reduce risk and raise the returns premium required of risk assets. In the last month, however, the VIX has settled at a much lower level.

The dollar strengthened significantly in 2015 and continued to advance, albeit at a slower pace, in the early part of 2016. The Fed was concerned about the repercussions if the greenback advanced further, as a strong dollar reduces exports. The knock-on effects have been a reallocation of resources away from export industries and reduce foreign profits of firms.

The good news is that the trade-weighted dollar has slipped since the Fed’s last meeting. It has remained well below its mid-January peak, in spite of the strength it gained on speculation surrounding the “Brexit” referendum.

Tightening of financial conditions also includes availability of credit. In this context, the Fed also noted that loan underwriting standards for commercial and industrial loans and for commercial real estate (CRE) loans had tightened in recent months. But many measures of business credit availability remain very positive, and many observers (including the Fed) have viewed moderation in CRE lending as healthy.

When the Fed met in January, the threat from tight financial conditions was pertinent, and there was ample reason for caution. Looking ahead, though, the Fed may find reason to be more sanguine about this facet of the outlook. We certainly are.