Look Beyond the Headlines: China's Services Sectors Continue to Grow

Three emerging markets portfolio managers — Dale Winner, Anthony Cragg, and Jerry Zhang—offer their views on investing in China.

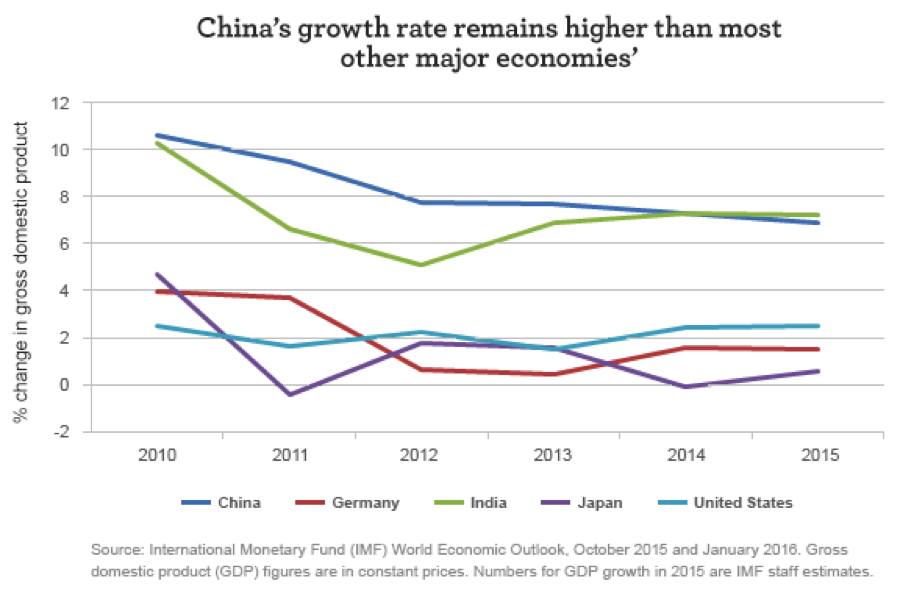

The health of China’s economy is one of the key questions facing investors. Although stock markets face challenges across the globe—which range from the low price of oil pressuring energy producers to the rise of nonperforming loans in major economies such as Italy—the prospect of a deflationary collapse in China seemed to weigh heaviest on stock prices. China’s economic growth rate has indeed slowed, edging beneath 7% in 2015 for the first time since the first quarter of 2009. Yet, when we spoke with three professional money managers that have long experience investing in China, they all believed that the concerns were overdone.

“The idea that there is no further growth in China is clearly ridiculous,” says Anthony Cragg, co-portfolio manager of the Wells Fargo Emerging Markets Equity Income Fund and the Wells Fargo Asia Pacific Fund. Citing the 2015 IMF World Economic Outlook, Mr. Cragg notes: “On an absolute basis, the amount that the Chinese economy grows each year is equivalent to the entire economy of the Netherlands.”

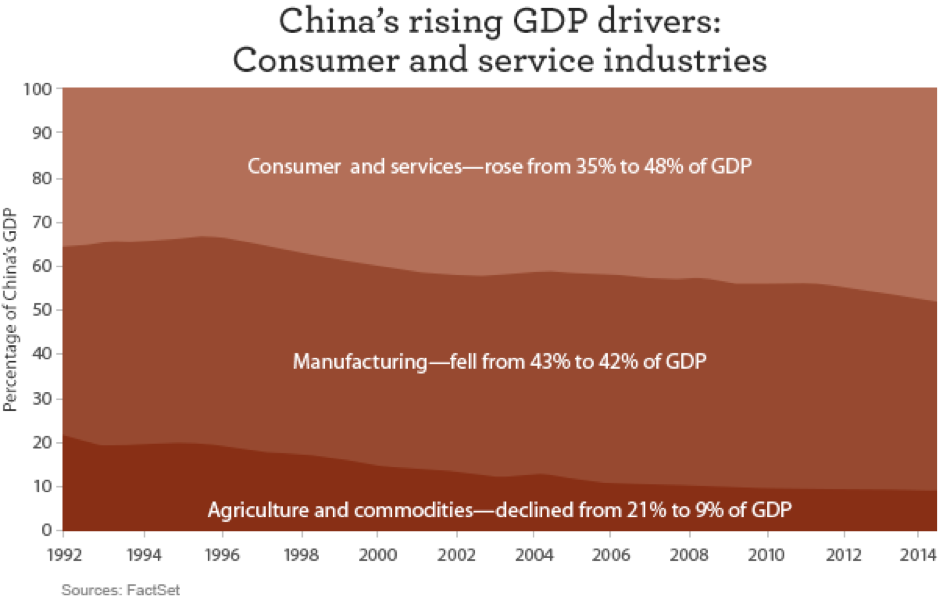

“We believe that China represents value, not a value trap,” says Dale Winner, portfolio manager of the Wells Fargo International Equity Fund. “That is because China controls its destiny. One, through monetary stimulus. China cut rates six times last year and we expect another one or two cuts in 2016. Second, by possibly unleashing another round of fiscal stimulus. And third, by implementing structural reforms, such as opening up its capital markets to foreigners, restructuring state-owned companies, and very importantly, making the transition from manufacturing to services.”

Opportunities in China’s new economy

“Right now, we have a discrepancy between China’s old economy—the infrastructure and export-related sectors—and its new economy, which includes the online and travel sectors,” says Cragg. “While the former part of the economy is struggling, the latter is booming. In November 2015, China’s online shopping day, Singles Day, rang up sales that made it five times larger than Cyber Monday in the U.S. Likewise, the number of tourists to Japan from mainland China doubled in 2015. Certain sectors in China continue to offer investors tremendous growth.”

“Everyone is focusing on the slowdown in China’s manufacturing,” says Mr. Winner, “but that’s part of the plan to move from a situation where capital investment represents approximately half of the economy—an unsustainable level—to a greater focus on consumption in services. China’s services sector is still growing.”

Jerry Zhang, co-portfolio manager of the Wells Fargo Emerging Markets Equity Fund, likewise highlights the opportunities in China’s services sectors. “The infrastructure and export-oriented parts of China’s economy are under stress,” says Mr. Zhang, “but some of the consumption-oriented sectors are performing well, particularly high-end services such as tutoring and tourism. China’s information technology companies have also benefited from trends such as increased adoption of social media and cloud computing.”

A good time to invest

Mr. Cragg points to major events in late 2015 that made China’s stocks more attractive. In November, the IMF announced that it would add the renminbi to its currency basket. The other currencies in the basket are the U.S. dollar, the euro, the Japanese yen, and the British pound. The renminbi’s inclusion highlights the global importance of the Chinese economy and encourages the currency’s use as a store of value. The second major event was that index provider MSCI added U.S.-listed stocks of Chinese companies to its MSCI Emerging Markets Index. The move will increase the overall weighting of Chinese companies in the index and cause passive investors to increase their weighting to the country. Both moves together should encourage institutional investors to treat China with the respect it deserves as a major economy.

“We’ve seen a long period of outperformance for the U.S. market relative to international stocks, resulting in relative inexpensive valuations for most international markets,” notes Mr. Winner. “As value investors, we get excited about cheap valuations, but not when there’s too much downside risk. In China, we believe the identifiable risks are justified by the potential rewards.”

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 2-25-16 and are those of John Natale, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management