Chinese President Xi Jinping is about to tell millions of government workers: “You’re fired.”

Reuters reported this week that China plans to lay off between five and six million state workers over the next two to three years, in an effort to curb overcapacity in what’s being described as “zombie companies”: those that are being kept alive on bank loans despite bleeding revenue. Close to two million of these layoffs will come from the coal industry alone.

The layoffs are part of a series of sweeping reforms announced ahead of the National People’s Congress (NPC) meeting this weekend. Every year, close to 3,000 Chinese officials and executives from all over the country convene in Beijing to develop and assess the status of the country’s Five-Year Plan. In response to worldwide demands that China manage its slowing economy better, President Xi Jinping this year has proposed what he calls “supply-side structural reform.”

And if that sounds a little like Chinese Reaganomics, that’s kind of the point.

Besides layoffs, Xi’s plan includes tax cuts, deregulation and reductions in state spending—economic policies you might expect to come from the desk of Reagan or Thatcher. We might also expect the results of these policies to be the same in China as in the U.S. and United Kingdom in the 1980s: a boom in entrepreneurship and innovation.

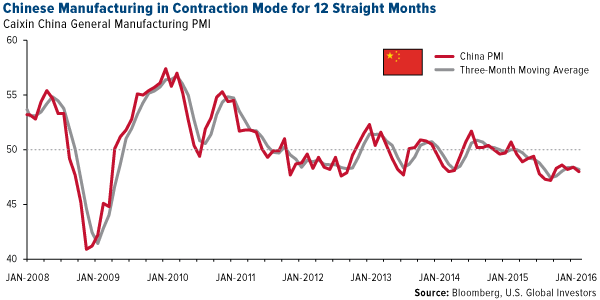

These reforms come at a crucial time for China, whose manufacturing sector has been in contraction mode for a year now as the country’s economy shifts toward domestic consumption. In February, China’s purchasing manager’s index (PMI) fell to 48.0 from 48.4 in January.

We closely follow government policy changes in China for a number of reasons. For one, its economy is the second largest in the world, and when based on purchasing power parity (PPP), its GDP is actually the largest, followed by the U.S., India and Japan. China’s economy, then, has a huge effect on the rest of the world, touching everything from commodities demand to consumption.

In 2015, total retail sales in China touched a record, surpassing 30 trillion renminbi, or about $4.2 trillion. By 2020, sales are expected to climb to $6.4 trillion, representing 50 percent growth in as little as five years. This growth will “roughly equal a market 1.3 times the size of Germany or the United Kingdom,” according to the World Economic Forum (WEF).

One of the main reasons for this surge in consumption is the staggering expansion of the country’s middle class. In October, Credit Suisse reported that, for the first time, the size of China’s middle class had exceeded that of America’s middle class, 109 million to 92 million. As incomes rise, so too does demand for durable and luxury goods, vehicles, air travel, energy and more.

But middle-income families aren’t the only ones growing in number. The WEF estimates that by 2020, upper-middle-income and affluent households will account for 30 percent of China’s urban households, up from only 7 percent in 2010.

Gold’s Back in a Bull Market at the BMO 25th Metals and Mining Conference

This week I returned from sunny Florida, where I had been attending the BMO Metals and Mining Conference, widely regarded as the best in the business. Sentiment toward gold was very optimistic, as I told Kitco News’ Daniela Cambone in this week’s edition of Gold Game Film. As always, Daniela did a fabulous job covering the events, interviewing all of the CEOs and other mining executives.

The yellow metal is 2016’s best-performing asset class so far, having climbed more than 19 percent. It just had its strongest February since 1975.

What’s more, gold appears as though it’s back in a bull market, often defined as a 20 percent gain from a recent trough. Short-term, though, it’s way overbought, so a correction at this point would be healthy.

Follow the Money, Follow the Gold Flows

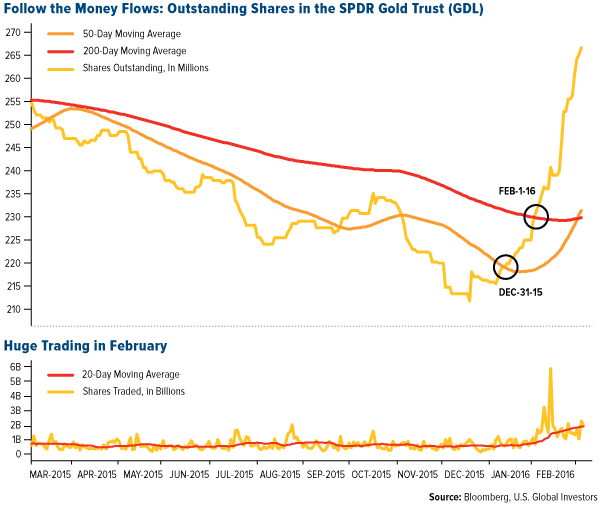

At the BMO Conference, I had the pleasure of meeting and speaking with my friend Pierre Lassonde, cofounder of Franco-Nevada, and company CEO David Harquail. Pierre told me that for every $1 billion that flows into the SPDR Gold Trust (GLD), the price of gold rises approximately $30 per ounce. Since the beginning of the year, we’ve seen about $9.3 billion flow into the GLD. During the same period, gold has risen 20 percent from its six-year low of $1,049.60 per ounce on December 17 to end Friday trading at $1,259.25.

The first breakout signal occurred on December 31, 2015, when money started to flow into gold, and the second important signal was when gold flows surpassed the 200-day, or 10-month, average, on February 1, 2016. Since the beginning of the year, gold has surged.

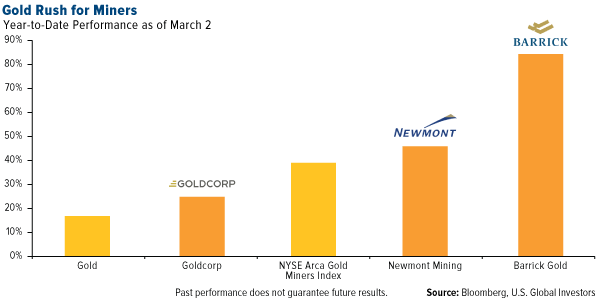

Like bullion, gold miners had a particularly gainful February, its best since 1998. The NYSE Arca Gold Miners Index rose an impressive 38.7 percent, compared to the 0.4 percent the S&P 500 Index lost in February. Year-to-date, production leaders Goldcorp, Newmont Mining and Barrick—which has recently lowered its debt-to-equity ratio—are thriving with prices pushing higher.

Gold is surging right now for a number of reasons, many of which I’ve covered in the last few weeks, including stronger inflation, negative interest rates and other components of the Fear Trade.

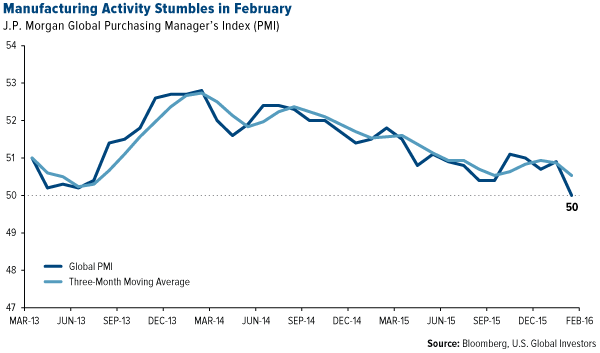

Global growth concerns have also spooked many investors, driving them into gold’s arms. This week we learned that the global PMI fell pretty dramatically to a neutral 50.0 reading in February, down from 50.9 in January. Anything below 50.0 indicates manufacturing deterioration, and while I hope we don’t cross into that territory, the PMI has been trending downward over the last two years. We haven’t seen sub-50 readings since 2012.

As I’ve discussed many times before, we use PMIs to help forecast global manufacturing conditions three to six months out. (I’ve likened the economic indicator to the high beams on your car, with GDP serving as your rearview mirror.) That the PMI remains below its three-month moving average doesn’t bode well for commodities or energy in the short-term. The weakness underscores the need for global economies to reform their tax systems and relax regulations, as China is attempting to do.

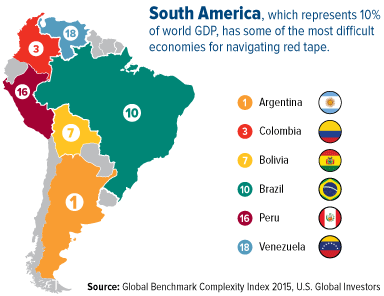

Comparing Countries’ Compliance Complexity

The TMF Group, a professional services firm, just released its annual Global Benchmark Complexity Index, which ranks countries according to the complexity of their business compliance standards. As you might expect, dominating the top 10 most complex governments are those found in South America, including Brazil, Bolivia, Colombia and, at number one, Argentina.

Colombia climbed—or fell, depending on your perspective—18 spots, from 21 to three, mainly due to the tax changes its government rolled out last year courtesy of its socialist finance minister, Mauricio Cárdenas Santa Maria. The South American country is now in the process of raising its income tax incrementally, from 40 percent this year to 43 percent in 2018, and with the agreement of other countries, it may now also tax the wealth its citizens hold in other jurisdictions (very similar to FATCA, or the Foreign Account Tax Compliance Act, here in the U.S.).

For the third consecutive year, Argentina ranks as the world’s most complex country in terms of business compliance. Back in November I wrote about the election of free-market advocate Mauricio Macri, expressing my hopes that the new president can bring significant reforms to the country’s business infrastructure and eliminate corruption. I’m still encouraged, but as we all know, political change is fraught with challenges and can take some time.

It’s a shame that Argentina, Colombia, Brazil and many other resource-rich countries in South America can’t move more quickly to eliminate the roadblocks that stand in the way of growth and prosperity. Brazil, which is on course for its worst recession in over a century, shrank 3.8 percent in 2015, the largest decline since 1990, and its central bank expects it to shrink a further 3.45 percent this year.

Reform would benefit not just their own capital markets but the world economy as a whole. South America represents about 10 percent of the global economy, meaning a 1 or 2 percent rise or fall in GDP could have a significant effect on world GDP.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.20 percent. The S&P 500 Stock Index rose 2.67 percent, while the Nasdaq Composite climbed 2.76 percent. The Russell 2000 small capitalization index gained 4.31 percent this week.

- The Hang Seng Composite gained 4.58 percent this week; while Taiwan was up 2.76 percent and the KOSPI rose 1.85 percent.

- The 10-year Treasury bond yield rose 11 basis points to 1.88 percent.

Domestic Equity Market

Strengths

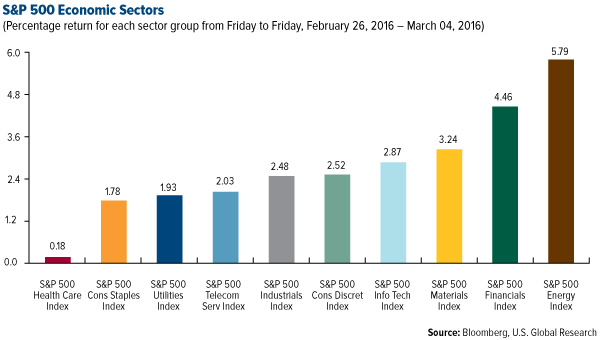

- Energy was the best performing sector, increasing by 5.79 percent vs an overall increase of 2.67 percent for the S&P 500.

- Chesapeake Energy was the best performing stock for the week, increasing 88.15 percent. The run-up in crude oil prices helped trigger a massive short squeeze on the stock. Shares also surged after the company received immunity from prosecution in the bid-rigging case against its former CEO Aubrey McLendon.

- U.S. exchange operators Intercontinental Exchange Group and CME Group are considering separate bids to combine with the London Stock Exchange (LSE). The LSE announced talks with Germany's Deutsche Boerse last week.

Weaknesses

- Health care was the worst performing sector for the week, increasing by 0.18 percent vs an overall increase of 2.67 percent for the S&P 500.

- Endo International was the worst performing stock for the week, falling -19.83 percent. The shares plunged after the company announced it will close its Astora Women’s Health division by the end of March after failing to find a buyer.

- According to BCA, the combination of high leverage and weak earnings is leading to a substantial rise in corporate defaults.

Opportunities

- While global manufacturing and business investment still lacks robustness, an easing in the U.S. dollar has the potential to cause a meaningful re-rating in overly depressed industrials profit expectations and relative valuations.

- Following years of global government austerity, rising global fiscal thrust should boost demand for defense capital goods.

- With the S&P 500 crossing the major technical 2000 level, stocks could be poised for a continued surge upward.

Threats

- According to BCA, return on equity has peaked for the cycle.

- In a deflatiotnary world rife with excess capacity, pricing power is deteriorating for the majority of U.S. companies, at a time when wages continue to rise, albeit slowly.

- Defaults in high-yield energy companies remain a looming threat.

The Economy and Bond Market

Strengths

- Friday's unemployment report showed solid job gains in February with a surge of 242,000. The report should help dispel lingering slowdown fears.

- The ISM manufacturing index rose to 49.5 in February from 48.2, suggesting that the contraction in the sector may be starting to turn around.

- Construction spending surged 1.5 percent month-over-month in January with upward revisions to December and November.

Weaknesses

- Wage growth took a hit, dipping to 2.2 percent year-over-year from 2.5 percent in January.

- According to the Wall Street Journal, a number of the largest shale oil producers in the United States have announced production cuts of approximately 5 percent to 10 percent this year. Crude oil prices, which have steadied in recent weeks, experienced modest gains this week in the wake of the announced cuts.

- The trade deficit widened in January to $45.7 billion from $44.7 billion in December.

Opportunities

- Activity picked up in most regions, according to the Beige Book, which is prepared in advance of each meeting of the U.S. Federal Reserve's rate-setting committee. Investors do not expect a hike at the March meeting. The market is currently pricing in just one rate hike over the next 12 months, as implied by futures contracts on the federal funds rate.

- Consumer prices fell 0.2 percent year-over-year in February, setting the stage for a more accommodative policy from the European Central Bank (ECB) when the Governing Council meets on March 10. The ECB targets an inflation rate of just below 2 percent.

- In the U.S., we continue to monitor business sentiment. The NFIB small business survey will be released on Tuesday; the ratio of expectations about selling price hikes and wage gains is an excellent leading indicator of profit margins.

Threats

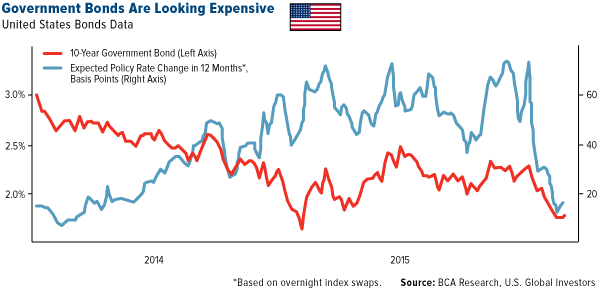

- Government bonds are at risk from a number of factors. Oil is in a bottoming process and is expected to be stronger in the second half of the year. While inflation is far from threatening, inflation could ramp up with rising energy prices. Moreover, the term premium in 10-year government bonds is near the lows observed when yields bottomed last April. Lastly, the market has almost priced out all rate hikes over the next 12 months in the U.S., even though Yellen, Dudley and Fischer have signaled that the Fed has not completely taken rate hikes off the table for later this year. This leaves the Treasury market vulnerable to any rebound in financial market sentiment, U.S. economic growth or positive inflation surprises.

- Moody's cut the outlook on China's credit rating to negative from stable. The credit rating agency warned that without credible and efficient reforms, China's GDP growth will slow markedly as a high debt burden dampens business investment and demographics turn increasingly unfavorable.

- There has been no conclusive signs yet of improving growth trends in China. Next week, several data points should help shed light, but of particular note for global investors, is the extent to which Chinese deflation risks are spreading. Chinese producer and consumer price updates will be released Wednesday. Similarly, U.S. import/export prices will be released Friday.

Gold Market

This week spot gold closed at $1,259.25, up $36.60 per ounce, or 2.99 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, climbed 5.00 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index traded up 4.52 percent. The U.S. Trade-Weighted Dollar Index slipped 0.94 percent for the week.

|

Date |

Event |

Survey |

Actual |

Prior |

|

Feb-29 |

Eurozone CPI Core YoY |

0.9% |

0.7% |

1.0% |

|

Feb-29 |

Caixin China PMI Mfg |

48.4 |

48.0 |

48.4 |

|

Mar-1 |

U.S. ISM Manufacturing |

48.5 |

49.5 |

48.2 |

|

Mar-2 |

U.S. ADP Employment Change |

190k |

214k |

193k |

|

Mar-3 |

U.S. Initial Jobless Claims |

270k |

278k |

272k |

|

Mar-3 |

U.S. Durable Goods Orders |

-- |

4.7% |

4.9% |

|

Mar-4 |

U.S. Change in Nonfarm payrolls |

195k |

242k |

172k |

|

Mar-10 |

ECB Main Refinancing Rate |

0.050% |

-- |

0.050% |

|

Mar-10 |

U.S. Initial Jobless Claims |

275k |

-- |

278k |

|

Mar-11 |

Germany CPI YoY |

0.0% |

-- |

0.0% |

Strengths

- Despite all the recent focus on gold, the best performing precious metal for the week was palladium, up 14.78 percent. Platinum should also get special mention with a gain of 7.10 percent. The World Platinum Investment Council made a strong investment case for the platinum group metals going forward as over 2 million ounces of vaulted stocks have been liquidated over the past four years, depressing the price of the metals.

- Following poor Chinese manufacturing data (which contracted for a record seventh month), gold held near a two-week high this week, reports Bloomberg News. Traders are pricing in only a 10-percent chance of an interest rate increase this month as well, and 50-percend odds of it happening by year end, adding to gold’s appeal.

- Gold headed for its biggest monthly gain in four years, reports Bloomberg, as falling equities bolstered demand for a haven asset during February. Central banks like the precious metal too, extending the longest gold-buying spree since 1965. According to Bloomberg, countries purchased almost 590 metric tons last year, accounting for 14 percent of annual global bullion demand.

Weaknesses

- The worst performing precious metal for the week was gold. Silver climbed 5.48 percent. Perhaps we are seeing some of the money flows rotate down to the other precious metals as year to date, gold has had all the glory.

- A dispute erupted this week between India’s Prime Minister Narendra Modi and thousands of the nation’s jewelers. Modi wants to impose a 1 percent excise duty on jewelry produced and sold within the country, reports Bloomberg. This caused a three-day stoppage on Wednesday by members of the All India Gems & Jewellery Federation. A similar shut down in 2012 was successful in getting the then Manmohan Singh government to drop plans for an excise duty.

- Bad news is on a roll, reports HSBC Global Research, citing that most PMIs fell in the month of February. The group says volatility in financial markets might be affecting corporate sentiment. The most “worrying development” was the sharp fall in Markit U.S. service sector index; the Markit measure of business activity fell below 50 for the first time since 2013.

Opportunities

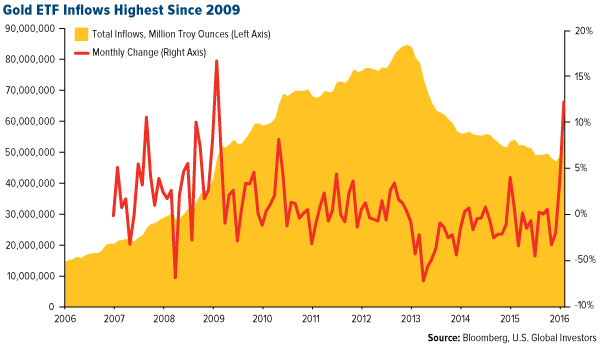

- As seen in the chart below, gold ETF inflows surged to the highest since 2009. The last time inflows were high, the S&P 500 had fallen more than 18 percent for the year and the Federal Reserve was only three months into its first QE program, reports Bloomberg. Lawrie Williams writes that the gold price is resilient and set for an interesting year. He points out, “The markets ignored the fact that all these ETF liquidations were being eagerly soaked up by the Chinese, Indians and others yet the gold price was being marked down on the COMEX futures markets where the price is largely set.”

- According to Taurus Wealth advisors, bullion could prove to be this year’s best performing asset class as central banks exhaust their firepower. The group says there is a high probability gold could reach $1,350 to $1,400 an ounce at year end, says Rainer Michael Preiss at Taurus. Deutsche Bank also raised its outlook on gold, citing slowing global growth and the possibility of a large yuan devaluation. Deutsche sees gold at $1,195 an ounce in 2016. This week on CNBC, a top economist for Moody’s stated that there are absolutely zero signs of recession. A Sovereign Man article mockingly writes of Moody’s statement, “When the agency that consistently fails to predict recession predicts that there will be no recession, you can pretty much guess what’s going to happen next.” The article continues by stating, “This is what virtually assures negative interest rates in America.”

- And of particular interest to investors were the announcements of two acquisitions this week. In one case, Endeavour Mining pulled the trigger to buy True Gold Mining for a 43.4 percent premium to the prior day’s close. In a second transaction, Lundin Mining agreed to take over Freeport McMoRan’s stake in a copper-gold project in Serbia. Reservoir Minerals was a partner with Freeport in the project and its share price jumped 17.62 percent on the news.

Threats

- William Dudley, president of the Federal Reserve Bank of New York, says he’s lost some confidence on his prediction that inflation will reach the U.S. central bank’s 2-percent target over time, citing recent turbulence in financial markets. “Partly, this reflects my assessment that uncertainty to the outlook has increased and that downside risks have crept up,” said Dudley.

- In a recent report from Cornerstone Macro, the group considers a few of the unintended consequences of negative rates. One consequence Cornerstone noted is that negative rates around the world are acting as a drag on U.S. interest rates, making the Fed’s job a bit tougher.

- In a video interview with SchiffGold this week, John Rubino of Dollar Collapse joins the discussion to talk about the printing of money. The description of the interview reads, “The ability to essentially create money out of thin air has allowed the world’s governments to take on unprecedented debt.” It continues by calling attention to the fact that 20 years ago economists never would have imagined a world with $7 trillion of bonds trading at negative interest rates, along with global debt at 300 percent of global GDP. However, that is the exact situation we are in today. Even the Wall Street Journal ran a story this week on the woes of negative interest rates. The writer found it somewhat interesting that the major insurers in Europe, who are big bond holders, never mentioned negative interest rates in their recent earnings calls.

Energy and Natural Resources Market

Strengths

- Gold is officially in a bull market. The metal is up more than 20 percent since a December low, the common definition of a bull market, outpacing all major assets. The yellow metal rose $36 per ounce this week, heedless of rebounding stock markets, as markets continue to expect central banks to curb yields in an effort to spur economic growth.

- The best performing sector for the week was the S&P/TSX Diversified Metals & Mining Index. The index rose 30 percent for the week following strong moves in copper up 7 percent, and nickel up 6 percent this week. Base metals have reached four- to six- month highs, on new speculative buying ahead of the Chinese National People’s Congress this Sunday.

- The best performing stock for the week in the broader natural resource space was Vale SA. The Brazilian iron ore producer rallied 61 percent for the week on three fronts: 1) strong speculation that China’s woes will ease; 2) expectations that iron ore prices will continue to see support from strong steel prices, and; 3) the signing of an agreement with authorities to cover the damages for the Samarco social and environmental disaster of 2015.

Weaknesses

- Iran’s crude exports rose to 1.4 million barrels per day in February. Overall the level may disappoint those who expected Iran to rapidly grow exports to pre-sanction levels. However, production is tracking 350 thousand barrels per day ahead of 2015 levels, a volume that has the ability to continue to distort the supply/demand rebalancing in the global crude markets.

- The worst performing sector for the week was the S&P 500 Fertilizers and Agricultural Chemicals Index. Monsanto Co., the index’s largest weighting, said it may have to push back its long-term earnings guidance as weak agricultural markets continue to pressure its forecasts. The decline in corn and soybean prices continues to hurt farmer economics globally, adding headwinds to fertilizer volumes and prices.

- The worst performing stock for the week in the S&P Global Natural Resources Index was Fibria Celulose. The Brazilian paper manufacturer dropped 8 percent as a surge in the Brazilian real against the U.S. dollar dimmed the prospects for exporter revenues. Fibria has 90 percent of its sales in North America, Europe, and Asia.

Opportunities

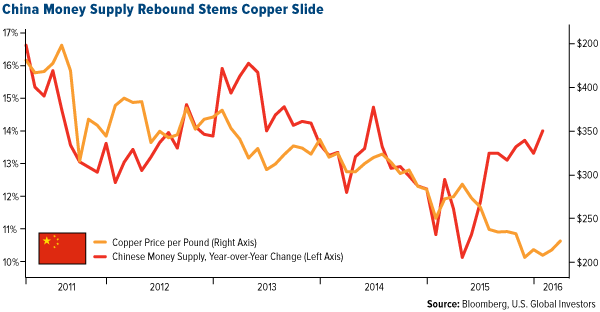

- Copper climbed to the highest in almost four months on speculation China will announce more measures to bolster growth. China is expected to announce plans to revive growth during its National People’s Congress this Saturday. However, monetary policy growth in China has already rebounded to 10-month highs and has stemmed the decline in copper prices.

- Citi is pounding the table on oil prices. Ed Morse, Citi’s global head of commodities research, argued Friday that crude oil prices may have already reached their lowest levels. In his opinion, the relatively weak seasonal period of March and April when refiners take capacity offline, and crude inventories rally to the detriment or prices, may not play out this year as U.S. shale produces have responded to oversupply in a more aggressive manner than the street expects.

- Physical gold appears to be running scarce as BlackRock Inc. suspended issuing shares in its physically backed gold ETF after a historic surge in buying. The move illustrates the voracious demand for bullion at a time when physical availability has shrunk owing to multi-year strong accumulation in China and India.

Threats

- February’s aggregate manufacturing PMI index for the leading industrial powers was just 49.7, denoting contraction. Macquarie Research notes this is the lowest level since December 2012. Declines were recorded across a number of the world’s industrial power houses, including China, Japan, Europe and Brazil. In fact, the only meaningful offset came from the US, were the ISM manufacturing index rose to 49.5, although it remained in sub-50 territory for the fifth consecutive month.

- Chinese steel mills are set to restart in March, likely capping strong advances in steel prices globally. Chinese agencies revealed plans to restart about 19 million tons of capacity after margins bounced back to levels last seen since the second quarter of 2015.

- March is coming in like a lamb for gas producers, at least according to Desjardins analysts. The Energy Information Administration (EIA) reported a weekly 48 billion cubic feet (bcf) withdrawal, well below the seasonal average of 137 bcf. Storage surplus expanded to over 650 bcf and there appears to be little relief in sight with extremely mild temperatures expected to persist through mid-March.

China Region

Strengths

- Early this week and to some surprise, the Peoples’ Bank of China (PBOC) lowered the reserve ratio requirement (RRR) for major banks to 17 percent from 17.5 percent, a form of traditional stimulus unexpected by markets after the PBOC had explicitly guided away from RRR cuts. The surprise move, made almost in tandem with the G20 meetings in Shanghai and the PBOC’s statement about “prudent” policy with an “easing bias,” aided sentiment this week as China heads into National People’s Congress.

- Singapore’s Straits Times Index rose more than 7 percent in the last 5 trading days , now only down about 1.5 percent year-to-date.

- Once again, the Malaysian ringgit had a strong week, rising to multi-month highs and aided by strength in oil and energy. Malaysia is the region’s only net energy-exporting country.

Weaknesses

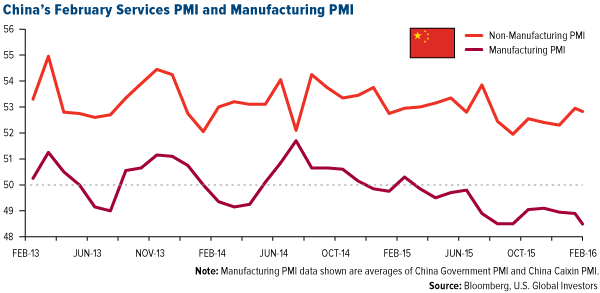

- Chinese PMIs continue to trend lower. Both manufacturing and services PMIs missed for February, in both the official and Caixin measurements. Official Chinese manufacturing PMIs were at 49.0, missing expectations of 49.4, while Caixin manufacturing PMIs came in at 48.0, missing expectations of 48.4. Services PMIs both came in well above 50, still signaling expansion. Official non-manufacturing came in at 52.7, while the more export-oriented Caixin services PMI reading came in at 51.2.

- The Nikkei Indonesia Manufacturing PMI ticked lower for February, falling to 48.7 from 48.9, and still in contraction territory.

Opportunities

- The release of China’s thirteenth “5 Year Plan” at the National People’s Congress and CPPCC will offer more and important clarity on Chinese policy direction, and China will also provide an official 2016 GDP estimate.

- The PBOC’s announced RRR cut and about-face on its use of this policy tool have sparked market expectations for further RRR cuts and stimulus. While the RRR cut does act indirectly to place some pressure on the yuan, China also reassured G20 members that no large devaluation is forthcoming. Any change in sentiment that helps reverse recent capital outflows can help bolster the yuan.

- Many markets are still recovering from the year’s early selloffs, and it may not take much to continue the recent rallies in equities markets across Asia.

Threats

- China releases its foreign exchange reserve levels for February this weekend. A miss may weigh heavily on sentiment given the recent capital outflow concerns.

- This week China put a halt to two outbound investment programs to aid in cracking down on capital outflows. One program allowed foreign investment managers in the Shanghai free trade zone to sell overseas investment products to wealthy Chinese citizens and the other allowed Chinese investment in foreign equities.

- Recent volatility and potential poor sentiment left over the early weeks of this year may continue to weigh upon markets if headlines disappoint.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 9 percent. Greek stocks have been among the worst performers for the past two years, and this week had the biggest surge among 93 national equites tracked by Bloomberg. Eurobank Ergasias Bank led the rebound, gaining more than 40 percent.

- The Russian ruble was the best performing currency this week, gaining 5.9 percent against the dollar. Brent crude oil gained 10.8 percent in the past five days. February services PMI was reported at 50.9 and composite PMI reached 50.6, crossing above the 50 level that separates growth from contraction. Inflation declined to 8.1 percent from 9.8 a year ago.

- The consumer staples sector was the best performing sector among Eastern European markets this week.

Weaknesses

- Ukraine was the worst relative performing market this week, gaining 63 basis points. Ukrainian’s central bank left its benchmark rate unchanged for a fourth meeting over concerns on inflation. The central bank targets 12 percent inflation at the end of 2016 as gross domestic product recovers, way below current inflation of 40 percent.

- The Czech koruna was the worst relative performing currency this week, gaining 60 basis points against the dollar. The PMI in February declined from 56.9 to 55.5. The budget balance was reported at 27.7 billion versus prior 45.9 billion. On the positive side, the country’s economy grew at 4 percent in 2015, at a faster pace than the prior year.

- The health care sector was the worst performing sector among Eastern European markets this week.

Opportunities

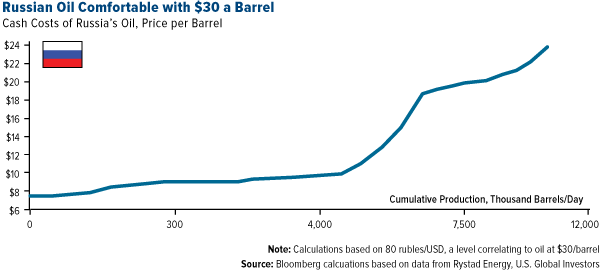

- According to Bloomberg calculation, Russian oil companies can live with oil prices as low as $30 per barrel as the cost of production of Russia’s most expensive barrels doesn’t exceed $24. A weak ruble, which has dropped more than 50 percent against the U.S. currency in the past two years, has helped keep cost low.

- Economists predict that the European Central Bank (ECB) will expand its quantitative easing program next week. There is now a 60 percent chance that ECB’s monthly bond buying program will be increased by 10 billion, which is currently at 60 billion euros. There is a near certain view among economists that the central bank will cut its negative deposit rate further to negative 0.4 from a negative 0.3, meaning that it will cost more to park money overnight at the bank.

- Hard currency reserves are increasing in Russia. The central bank of Russia held $379 billion in foreign exchange and gold as of February 19, up $29 billion from last’s year low in April, making Russia the only major emerging country with a gain. Russia announced a plan to further boost its reserves to $500 billion, a level last seen in 2014.

Threats

- The eurozone slid back into deflation in February as cheaper oil and anemic growth weighed on prices. Consumer prices fell 0.2 percent from a year earlier in February, a sharper drop than economists had expected. It was the first decline since September of last year.

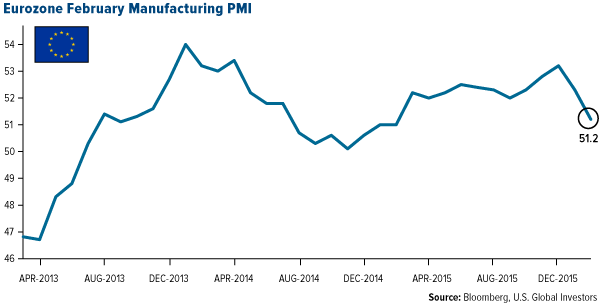

- Eurozone February manufacturing PMI is at a 12-month low of 51.2, down sharply from 52.3 in January. Production, new orders, exports and employment are losing momentum due to decreasing domestic demand and a slowdown in global markets. However, the service PMI for February was reported at 53.3 versus prior 53 and the composite PMI climbed to 53 from 52.7.

- The Venice Commission, an advisory group to human rights body the Council of Europe, visited Warsaw last month to see whether democratic standards are being upheld by Poland. In a preliminary opinion, obtained by the Gazeta Wyborcza newspaper and made public over the weekend, the Venice Commission said an ongoing constitutional crisis in Poland poses a danger to the rule of law, democracy and human rights. Full report will be reported March 11.

Leaders and Laggards

Weekly Performance

|

Index |

Close |

Weekly Change($) |

Weekly Change(%) |

|

DJIA |

17,006.77 |

+366.80 |

+2.20% |

|

S&P 500 |

1,999.99 |

+51.94 |

+2.67% |

|

S&P Energy |

453.31 |

+24.82 |

+5.79% |

|

S&P Basic Materials |

272.64 |

+8.55 |

+3.24% |

|

Nasdaq |

4,717.02 |

+126.55 |

+2.76% |

|

Russell 2000 |

1,081.94 |

+44.75 |

+4.31% |

|

Hang Seng Composite Index |

2,750.40 |

+120.38 |

+4.58% |

|

Korean KOSPI Index |

1,955.63 |

+35.47 |

+1.85% |

|

S&P/TSX Canadian Gold Index |

181.37 |

+4.42 |

+2.50% |

|

XAU |

66.75 |

+4.85 |

+7.84% |

|

Gold Futures |

1,261.60 |

+41.20 |

+3.38% |

|

Oil Futures |

36.22 |

+3.44 |

+10.49% |

|

Natural Gas Futures |

1.67 |

-0.12 |

-6.70% |

|

10-Yr Treasury Bond |

1.88 |

+0.11 |

+6.35% |

Monthly Performance

|

Index |

Close |

Monthly Change($) |

Monthly Change(%) |

|

DJIA |

17,006.77 |

+670.11 |

+4.10% |

|

S&P 500 |

1,999.99 |

+87.46 |

+4.57% |

|

S&P Energy |

453.31 |

+24.32 |

+5.67% |

|

S&P Basic Materials |

272.64 |

+20.64 |

+8.19% |

|

Nasdaq |

4,717.02 |

+212.78 |

+4.72% |

|

Russell 2000 |

1,081.94 |

+71.64 |

+7.09% |

|

Hang Seng Composite Index |

2,750.40 |

+171.34 |

+6.64% |

|

Korean KOSPI Index |

1,955.63 |

+64.96 |

+3.44% |

|

S&P/TSX Canadian Gold Index |

181.37 |

+31.23 |

+20.80% |

|

XAU |

66.75 |

+16.73 |

+33.45% |

|

Gold Futures |

1,261.60 |

+120.30 |

+10.54% |

|

Oil Futures |

36.22 |

+3.94 |

+12.21% |

|

Natural Gas Futures |

1.67 |

-0.37 |

-18.01% |

|

10-Yr Treasury Bond |

1.88 |

-0.01 |

-0.64% |

Quarterly Performance

|

Index |

Close |

Quarterly Change($) |

Quarterly Change(%) |

|

DJIA |

17,006.77 |

-840.86 |

-4.71% |

|

S&P 500 |

1,999.99 |

-91.70 |

-4.38% |

|

S&P Energy |

453.31 |

-20.63 |

-4.35% |

|

S&P Basic Materials |

272.64 |

-14.41 |

-5.02% |

|

Nasdaq |

4,717.02 |

-425.25 |

-8.27% |

|

Russell 2000 |

1,081.94 |

-101.46 |

-8.57% |

|

Hang Seng Composite Index |

2,750.40 |

-309.26 |

-10.11% |

|

Korean KOSPI Index |

1,955.63 |

-18.77 |

-0.95% |

|

S&P/TSX Canadian Gold Index |

181.37 |

+44.96 |

+32.96% |

|

XAU |

66.75 |

+16.80 |

+33.63% |

|

Gold Futures |

1,261.60 |

+176.80 |

+16.30% |

|

Oil Futures |

36.22 |

-3.75 |

-9.38% |

|

Natural Gas Futures |

1.67 |

-0.52 |

-23.56% |

|

10-Yr Treasury Bond |

1.88 |

-0.40 |

-17.40% |

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission ("SEC"). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of 12/31/2015:

Freeport McMoRan

Lundin Mining

Newmont Mining Corp.

Reservoir Minerals

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The J.P. Morgan Global Purchasing Managers’ Index is an indicator of the economic health of the global manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The Caixin China Services PM, released by Markit Economics, is based on data compiled from monthly replies to questionnaires sent to purchasing executives in over 400 private service sector companies.

A basis point, or bp, is a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01% (0.0001).

The COMEX is a commodity exchange in New York City formed by the merger of four past exchanges. The exchange trades futures in sugar, coffee, petroleum, metals and financial instruments.

S&P/TSX Capped Diversified Metals and Mining Index is an index of companies engaged in diversified production or extraction of metals and minerals.

The S&P 500 Fertilizers and Agricultural Chemicals Index is a capitalization-weighted index.

The S&P Global Natural Resources Index includes 90 of the largest publicly-traded companies in natural resources and commodities businesses that meet specific investability requirements, offering investors diversified, liquid and investable equity exposure across 3 primary commodity-related sectors: Agribusiness, Energy, and Metals & Mining.

The Straits Times Index is a modified market capitalization-weighted index comprised of the most heavily weighted and active stocks traded on the Stock Exchange of Singapore.

The ISM manufacturing composite index is a diffusion index calculated from five of the eight sub-components of a monthly survey of purchasing managers at roughly 300 manufacturing firms from 21 industries in all 50 states.