Headwinds from China, market turbulence and soft economic reports cast doubt about the strength of U.S. economic fundamentals as 2016 began. But the most recent data provide evidence to the contrary.

A string of economic reports – industrial production, consumer spending, durable goods orders and the Institute of Supply Management’s (ISM) factory survey – look considerably better. And financial conditions do not indicate a weakening economic situation.

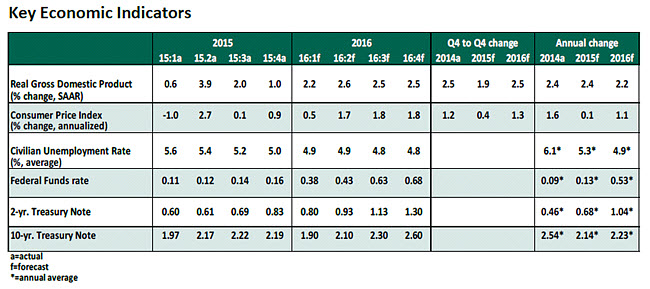

First-quarter real gross domestic product (GDP) is predicted to show an improvement after only a 1.0% increase in the final three months of 2015. The outlook for 2016 is positive, with economic growth expected to be close to the economy’s potential capacity.

Key Elements of Forecast

- Consumer spending slowed in the final three months of 2015 to 2.0%. January data brought comfort when consumer spending shot up 0.4%, reflecting gains in all three major components – durables, non-durables and services. Auto sales were nearly flat in February, putting the two-month average at 17.6 million, which is an elevated reading but slightly below the 17.9 million average of the fourth quarter. Bearing in mind these factors, a 3.0% increase in consumer spending during the first quarter should not be surprising.

- Business capital expenditures fell in the fourth quarter, and factory surveys until recently pointed to slowing conditions. The good news is that the February manufacturing ISM survey shows a pickup in production and a steady reading for new orders. Shipments of non-defense capital goods rose in January. Although these are modest improvements, they reduce concern about capital spending declining sharply in the months ahead.

- Sales of existing homes moved up 0.4% in January after a strong 12.1% increase in the prior month. The level of existing home sales is close to the post-crisis high established in July 2015. Purchases of new homes slipped a little over 9.0% in January. Housing starts fell in December and January, a bit disappointing. But residential construction outlays for new homes advanced 0.4%. All in, housing market data have been mixed. The strong labor market performance and growth in personal income suggest that the recent slowing could be temporary.

- The pace of job creation slowed in January, which raised uncertainty about employment conditions. The February labor market report eased these anxieties with a 242,000 increase in payrolls. The unemployment rate held steady at 4.9% despite an increase in the participation rate. This is an important development, as it reflects the return of some discouraged workers. The quit rate in the U.S. economy at 2.1% is close to readings at the peak of the last expansion. Full employment is not too far away.

- In January, overall inflation increased 1.3% on a year-to-year basis. The core personal expenditure price index is up 1.7%, which is close to the Fed’s 2.0% inflation target. This is not a one-off event, as it reflects widespread increases in prices. Also, the benefit of the decline in oil prices and the appreciation of the dollar will be smaller going forward. Moreover, oil prices appear to have established a bottom. Putting these factors together, the Fed may have its wish of sustained higher inflation delivered soon.

- Bullish economic data helped to lift the 10-year Treasury note yield from a low of 1.63% in February to 1.86% as of this writing. Credit spreads, both investment-grade and high-yield, have narrowed. The Volatility Index is trading around 17.5, a far cry from the worrisome 25-plus reading of February. Equity prices have recovered, and the trade-weighted dollar is down from the highs seen in January. In sum, financial conditions are not as oppressive now versus a few weeks ago.

- Central banks of China and Japan announced monetary policy easing to support economic growth, while markets are eagerly awaiting the European Central Bank’s announcement on March 10. The key is that central banks are acting to lift business activity, which reduces fear of sustained global economic weakness.

- The Federal Open Market Committee meeting next week is nearly certain to conclude without any change in policy. The Fed is mostly likely to note that risks are nearly balanced, a change from the prior meeting when the Fed’s risk assessment was missing. Of course, markets will focus on the forecast dot chart for clues about the extent of policy hikes. We retain our call for tightening action in June and December 2016.