Is Your Asset Allocation in Line with Your Goals?

A financial plan can help you line up your resources with your goals; every investor should have one. However, one problem that many people face is their asset allocations are way off from what their plans require. Like many things in life, it’s easy to know you need to address something but hard to actually do it. Let’s walk through a plan to get your asset allocations back in line with your long-term financial goals.

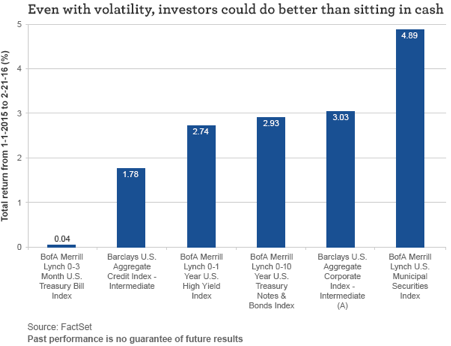

The first step is recognizing that, if you hold too much cash, your current asset allocation isn’t going to help you achieve your long-term goals. Some people may have enough financial resources to sit in cash forever, but those people are few and far between. Most investors sitting in cash are seeing the real purchasing power of their assets declining; when inflation exceeds your rate of return, the purchasing power of your wealth erodes.

For planned expenditures, keep cash in hand

So what role should cash play in your financial plan? I think cash balances should cover anywhere from a few months’ to a year’s worth of planned expenditures that aren’t met by steady and reliable sources of income, such as Social Security or work income. It’s prudent to have a few extra months’ worth of spending covered, even with a source of stable income. These expenditures include mortgage payments, utilities, transportation costs, food, gifting, charitable contributions, and other expenses. If you want to maintain your lifestyle, these expenses are pretty much set in stone—so you don’t want to rely on risky assets to fund them. So every month, topping off your cash account to keep a rolling six months’ to one year’s worth of expenses covered can help you sleep better at night.

For life’s unexpected costs, think low volatility

Precautionary balances are also an important part of a financial plan. You many need to fund unexpected life events, such as a spontaneous trip, a medical expense, or a car that needs repairs. Sure, a line of credit can help, but if you have the financial means, keeping an extra six months’ to a year’s worth of spending in low-volatility investments can add some cushion to your asset allocation. Granted, with low volatility often comes low returns, but the returns can be better than what cash offers. This is where short-term fixed-income investing can fit nicely within a financial plan. Opportunistically, or quarterly, topping off your precautionary balances can help you shift your focus from thinking that every market swing will affect your daily life to recognizing that risk is simply an inherent part of trying to earn a higher rate of return than you’d find in risk-free securities.

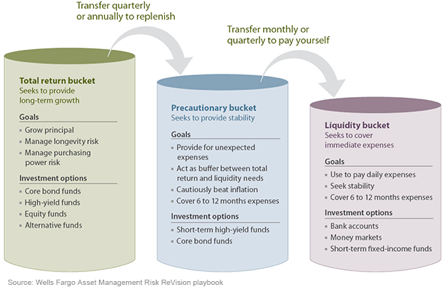

For long-term goals, a three-bucket approach

With your planned expenditure and precautionary balances taken care of, the rest of your asset allocation can be devoted to a third category: longer-term goals. Sometimes people refer to this three-category method of portfolio-building as an envelope or bucket approach, in which you have three containers to fill. The following chart shows the interconnected relationship between these three components.

What if your liquidity or precautionary bucket is currently overflowing? This could be because you’re just not sure when, or how, to get back to your planned allocation. It’s frustrating to try to buy on the dips only to find that there are more dips than you have cash for. Similarly, it can be frustrating when you’re trying to get out of a position in which you would love to pick the top but find that things keep running higher after you sell. In both of these scenarios, a method called dollar cost averaging (DCA) can cover a multitude of market-timing sins.

To return to proper allocation, use DCA

DCA is an investing strategy that overlooks the market’s daily ups and downs and acknowledges how difficult it can be to pinpoint the ideal time to invest. Instead, you invest a fixed dollar amount on a regular and recurring basis over a period of time. While DCA doesn’t guarantee a profit or protect from losses, it does help investors focus on asset accumulation and is a smart alternative to guessing when and how much to buy.

So how does DCA work as part of your long-term plan? Considering that stocks—as measured by the S&P 500 Index’s inflation-adjusted total return from 1800 to 2016—have been up over a one-year horizon 68% of the time, I believe it pays to take a tear-the-bandage-off approach and just get your allocation strategy back to what your long-term plan requires. However, this approach might not be so comfortable for investors.

Let’s say you have a five-year holding period for stocks in your portfolio. The average annual real internal rate of return of simply going all-in on stocks for five years is 6.73% with a standard deviation of 7.48%, according to Global Financial Data’s (GFD) current and historical tracking of the S&P 500. Now, instead of going all-in, consider DCA into stocks over the span of one year. During this period, you’d invest one-twelfth of your target allocation into stocks every month. Imagine putting $10,000 a month into the S&P 500 and then holding until the end of year five. Doing so would increase the average annual real internal rate of return to 6.78%, with a slightly higher standard deviation than the all-in approach (7.74%).

This is because while you may miss out on the trend growth rate of stocks, you take advantage of the stock market’s ups and downs, effectively getting a lower cost basis for your stocks. Volatile markets can be your friend when you DCA in.

Most people have probably heard of DCA into stocks, but you can also DCA out of stocks if you are too heavily allocated in equities. Consider a strategy in which you take the first year to ease into stocks and the last year to ease out. In year one, you’re putting in a fixed amount every month. You then hold this for three years. In the last year, you take out a fixed amount every month. For easing out, the strategy that I modeled takes one-twelfth of a portfolio’s balance (from the end of year four) out every month until the end of year five. This model allowed all 12 payments to be taken 97.8% of the time. Among the other results:

- In a small fraction of instances (2.2% of the time), the model’s total return bucket ran dry before all 12 payments could be taken.

- In the majority of cases, not only could all 12 equal payments be taken but there was a lump sum left at the end.

- The real internal rate of return of this DCA in—and then DCA out—averaged 5.18% with a standard deviation of 7.84%. Remember: these are inflation adjusted numbers.

Final words of advice

Caution can be costly, although that cost might be worth it if it’s more comfortable. In my view, this approach is certainly better than doing nothing. Your plan to get back to plan can be a simple three-step approach:

Step 1: Recognize that you need to get your allocation back in line with your long-term goals.

Step 2: Recognize that you won’t be able to pick the top or the bottom, so stop trying. DCA might not be optimal, but it can be a comfortable option.

Step 3: Don’t get yourself in this situation again. Focusing on cash management and building a precautionary balance can help you not freak out about the longer-term growth portion of your portfolio.

Original blog post

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 3-1-16 and are those of Dr. Brian Jacobsen, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management