- The ECB’s Race Against Time

- Making the Case for Fed Delay

- U.S. Bank Energy Exposure Is Modest and Manageable

Our son is on a path toward the Army medical corps. We’re really proud of him and of his prospective service. But we’re also hoping that his services are never required during battle. War is very serious business.

So I don’t really like it when bellicose terms are used to describe civilian situations. For example, this week’s actions from the European Central Bank (ECB) were depicted by various observers as a “bazooka,” which used “the full arsenal,” in the “war against deflation.” The metaphor is a little unfortunate. But the ECB’s steps were substantial, and they come at a critical juncture.

Buffeted first by the Global Financial Crisis (GFC) and then by the sovereign debt crisis two years later, the eurozone has struggled to restore prosperity. Real gross domestic product (GDP) has still not recovered to the level recorded eight years ago, and growth has been uneven. Unemployment remains elevated, especially among young people.

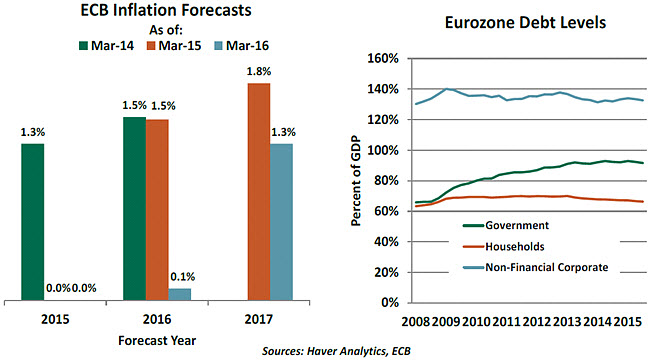

As a result of all this, eurozone inflation has persistently run far below the ECB’s 2% target. A good bit of the blame can be assigned to falling oil prices, but sub-par levels of economic activity have also contributed. On a year-over-year basis, the eurozone price level has fallen by 0.2% overall and “core” prices (which exclude energy) have risen only 0.8%. The forecasts released by the ECB this week once again marked down inflation expectations.

There has been a lot of discussion about whether some of the current disinflation is “good,” since falling prices for some things are beneficial to consumers. But low inflation is unambiguously bad for debtors, since it raises the real value of their obligations. Said differently, inflation allows debtors to pay back fixed amounts with income that grows as the price level rises.

Among the legacies of the eurozone’s near-decade of disappointment is a sizeable accumulation of leverage. Private debt in the United States and the United Kingdom has trended down (as a percentage of GDP) since 2008, and the rise in government debt has moderated. But debtors in the eurozone have not made much of a dent in their liabilities.

This makes the endeavor to restore normal inflation even more important. But the policy options for doing so are limited. Fiscal matters are handled at the national level, and the potential for stimulus is limited in many places by the need for austerity. Structural changes to speed economic transition (such as labor market reform) can only be implemented locally, and those are moving very, very slowly.  So monetary policy has been the only game in town since the GFC, and the ECB has pressed on even though its tools may not be best suited to deal with the myriad limitations on eurozone growth. The measures announced this week covered a broad range of tactics: interest rates were pushed more deeply into negative territory, quantitative easing (QE) was expanded, and low-cost funding was offered to banks in exchange for making more loans.

So monetary policy has been the only game in town since the GFC, and the ECB has pressed on even though its tools may not be best suited to deal with the myriad limitations on eurozone growth. The measures announced this week covered a broad range of tactics: interest rates were pushed more deeply into negative territory, quantitative easing (QE) was expanded, and low-cost funding was offered to banks in exchange for making more loans.

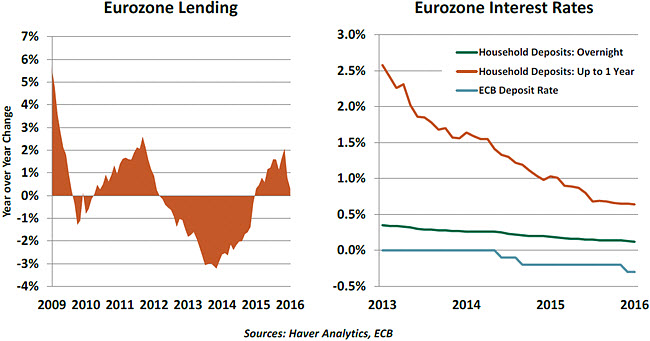

Getting the credit channel reopened to support consumption and new business formation is essential to the eurozone. But many eurozone households and businesses may be seeking to reduce, not increase, their leverage. And many banks are still burdened by crisis-era bad loans and exposure to emerging markets. Loan growth moved back into positive territory last year but has been falling back over the past two months.

In taking rates negative, the ECB’s intent was to make it expensive for financial institutions to leave money on deposit with the central bank instead of lending it. But banks have been reluctant to reduce the rates they offer to retail depositors, for fear of an adverse reaction. So the ECB’s policies have produced a bit of an earnings squeeze, which has been counterproductive to the goal of fostering expanded lending.

The measures announced this week are intelligently designed. By offering very low-cost funding to banks through the Targeted Long Term Refinancing Operations (TLTROs), the ECB is hoping to foster new lending that is profitable. The decision to raise monthly asset purchases to €80 billion and include corporate bonds in the program will make the ECB a direct provider of capital for large firms. It all sounds good in theory, but the program will be judged on tangible results.

The ECB’s efforts over the past 14 months have also been beneficial on two other fronts. Easier monetary policy has weakened the euro, and low interest rates have prompted investors to move into shares. Gains in the equity markets can produce wealth effects that benefit consumption.  But the potency of ECB stimulus seems to be wearing off in these arenas. The euro rallied, and European equity markets fell after Thursday’s announcement. This led some questioners to challenge ECB President Mario Draghi about the wisdom of pressing on.

But the potency of ECB stimulus seems to be wearing off in these arenas. The euro rallied, and European equity markets fell after Thursday’s announcement. This led some questioners to challenge ECB President Mario Draghi about the wisdom of pressing on.

Draghi responded elegantly, by pointing out that policy can only be judged by comparing what actually happens to what would have happened in the absence of intervention. This “counterfactual” can never be observed, but many think that the eurozone would have been much worse off if the ECB had not stepped up its efforts.

To those who think that the only true antidote for Europe is time to heal (tellingly, Draghi referred to this policy with the German phrase “nein zu allem,” or no to everything) that time may be running out. The patience of the plebiscite has been wearing thin, and regime change is becoming a more-significant risk. Draghi’s policy and his passion may be the best hope for preserving European integrity.

Better Late Than Early?

The ECB cedes the stage this coming week to the Bank of England and the Federal Reserve. The Fed will be gathering Tuesday and Wednesday to deliberate, and the meeting could be much more interesting than previously thought.

Three months ago, the consensus within the Federal Open Market Committee (FOMC) was that four interest rate increases would be appropriate in 2016. Three weeks ago, analysts were debating whether any interest rate increases would be appropriate. Global financial markets had faltered, and the resulting tightening in financial conditions threatened to constrain economic growth. Some were predicting that the Fed’s next move would be one of retreat.

But the tone has changed significantly since mid-February. As we discussed two weeks ago, financial conditions have improved. The latest sign of recovery is in the high-yield debt market, which has enjoyed renewed investor interest. China reduced its reserve requirements in an effort to stimulate its economy and confirmed its growth expectations at last week’s Party Congress. Oil has increased by almost $12 per barrel since hitting bottom.

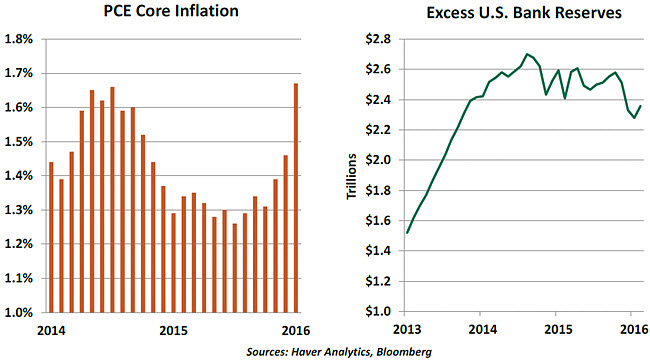

More importantly, readings covering the Fed’s dual mandate have taken a sharp turn for the better. The January job report was modest but February’s more than made up for it. And the Fed’s favored inflation reading jumped in January to a gain of 1.7% over the past year. This is not far from the 2% inflation target.

The FOMC should also take note of what has been going on in bank balance sheets. A significant majority of the reserves the Fed put into the banking system through its QE program have sat idle on bank balance sheets. Recently, though, the level of excess reserves declined as lending accelerated.

Taken together, all of this makes a pretty good case for an interest rate increase. Fed Chair Janet Yellen has said that monetary policy is data-dependent, and the data over the past month has been very positive. There will certainly be hawkish voices on the FOMC pressing that case.

We don’t think that the hawks will win the day, however. Fed officials haven’t had sufficient time to preview a move; as recently as four weeks ago, officials were making a case for caution. So any tightening next week would challenge financial markets.  In addition, there is a school of thought within some corners of the Fed system that it is better to err by tightening too late than too early. The case for such an asymmetric stance is detailed in a recent paper from Charles Evans and economists from the Federal Reserve Bank of Chicago. Quoting the authors:

In addition, there is a school of thought within some corners of the Fed system that it is better to err by tightening too late than too early. The case for such an asymmetric stance is detailed in a recent paper from Charles Evans and economists from the Federal Reserve Bank of Chicago. Quoting the authors:

“If the FOMC misjudges the impediments to growth and inflation and reduces monetary accommodation too soon, it could find itself in the uncomfortable position of having to reverse course and being constrained by the zero lower bound (ZLB) again…In contrast, if the Fed keeps rates too low and inflation rises too quickly, it most likely could be brought back into check with modest increases in interest rates. Since the unconventional tools available to counter the first scenario may be less effective than the traditional tools to counter the second scenario, the costs of premature liftoff may exceed those of delay.”

There are certainly those who would debate the idea that it would be easy to check inflation that rises too quickly. And the lower bound of interest rates might be less than zero, affording the Fed a little more dry powder. But for now, expect the Fed to err on the side of caution and buy itself another three months to consider its next move.

Oil Will Not Drown U.S. Banks

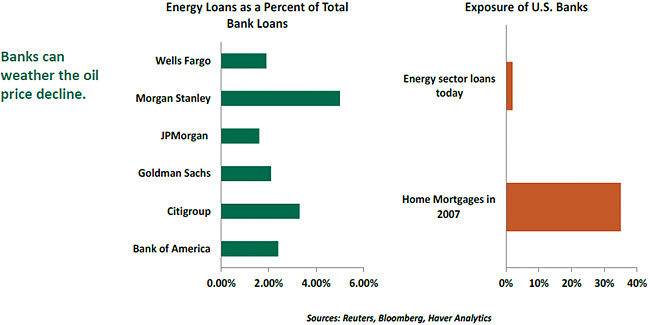

There are winners and losers when oil prices plunge. Oil exporters and producers suffer, along with banks and other lenders to this industry. We have been asked on several occasions if exposure of banks to energy-related loans has the potential to become a replay of the mortgage crisis or even a replay of the energy lending debacle of a generation ago. But those concerns are very much misplaced.

Bloomberg noted that there are $123 billion of bank loans outstanding to the energy industry. If this is accurate, energy industry loans accounted for less than 2% of outstanding bank loans in 2015. By contrast, mortgage loans in 2007 were close to 35% of the loan book, and some firms had mortgage-related exposure in their trading and investment portfolios.

The energy industry has raised a great deal of the funds it needs from the bond market. In fact, investment-grade ($409 billion, 9% of market) and high-yield ($154 billion, 12% of market) bonds account for a larger share of the energy industry’s outstanding debt.

Although the volume of energy industry loans is not monumental, they have to be serviced. Failure of borrowers to meet their obligations leads to an increase in loan losses and a reduction in earnings. This aspect received attention when fourth-quarter earnings were published recently, and banks noted that a further reduction in energy prices would be problematic.

Offsetting this is the fact that bank portfolios include loans obligors who benefit from low oil prices. The reduction in oil prices would serve to augment the profitability and creditworthiness of this latter group.

To be sure, some banks have more energy exposure than others. But the loss-absorbing capacity of bank balance sheets today is vastly different from 2008.

Finally, the recent firming in oil prices has improved prospects of energy loans being serviced. There may certainly be another banking crisis someday, but today is not that day.

© Northern Trust