Rising Global Taxes and Regulations (Indirect Taxation) Are Chipping Away at the Benefits of Low Int

During a trip to New York this week I was able to talk gold and commodities on Bloomberg TV, and also had the pleasure of hearing Canadian Prime Minister Justin Trudeau address Wall Street investors in the Bloomberg studios the same day. Trudeau discussed his plan for new infrastructure spending of C$60 billion over the next 10 years, as a means to lift the country’s highly oil-dependent economy. Trudeau answered questions on his country’s federal fiscal deficit and I was able to ask him about the amount of Ontario’s debt in particular. Ontario has twice the debt as the state of California and only half of its population.

|

In the U.S., states are held to a strict balanced budget standard when it comes to fiscal taxation and spending, while the federal government can let the budget go into deficit spending. In Canada however, it’s the opposite, and the provinces seem to have abused their debt levels, but Trudeau is ready to help.

The former Prime Minister of Canada, Stephen Harper, never smiled like Justin Trudeau. But he was a great defensive leader, and his conservative leadership allowed the country to successfully weather the financial crash of 2008. Now the current government can leverage that strong balance sheet to stimulate economic activity.

During the Bloomberg conference Trudeau sought to reassure his audience that he will remain cautious on spending.

Creeping Taxation and Negative Interest Rates Ignite Global Caution

Compliance and regulation measures have intensified from the financial sector to the food industry, from the U.S. all the way to Brazil. Many CEOs of banks, as well as brokers that I have spoken with recently, have lamented on the financial burden of excessive regulation and the indirect taxation that comes along with this rise in rules on steroids. Regulations are fueled with good intentions; however, the unexpected consequences like slow global growth need to be adjusted.

In Brazil, the government promotes short-term government bonds to fund its bloated government workforce. The anti-capitalist nature of Brazil’s government extends to extreme limitations on public markets, where new companies can only go public by offering shares at $1,000. And I’ve shared with you before how Colombia’s citizens are taxed at every turn.

Meanwhile, central bankers around the world captured headlines this week, and it looks as if easy money is here to stay for the time being, as well as high taxes and regulations. The prevailing message was that global economic conditions have not improved well enough to support any significant changes to monetary policy, which now has interest rates around the globe at near-zero or, in some cases, subzero levels.

|

Last Thursday, the European Central Bank (ECB) came out with deeper cuts to already-negative rates and steeper purchases of bonds, from 60 billion euros to 80 billion euros. This was followed on Tuesday by the Bank of Japan’s (BoJ) decision to leave negative rates unchanged as it assesses the impact of its controversial policy, which shocked global markets when it was unveiled in January. Likewise, the Bank of England decided on Thursday to keep interest rates at the historic low of 0.5 percent.

As I (and many others) expected, the Federal Reserve also put rates on hold, even as the U.S. economy is showing signs of improvement in employment, housing and inflation. According to Fed Chair Janet Yellen, a soft global economy made a rate hike too risky.

Be that as it may, our emphasis on central bank actions is way overdone and in many ways a distraction from what’s really important: balanced fiscal policy. Today, many investors expect central banks to jumpstart the global economy, and indeed their decisions can have huge consequences. But they can’t do it alone. What we need is a commitment to streamline regulation and relax taxes, with prudent spending on economy-boosting infrastructure, manufacturing and construction. Until that happens, it doesn’t matter how low policymakers drop rates or how much debt they purchase.

Tailwinds to Global Growth

I’ve written before about how we use the purchasing managers’ index (PMI) as a forward-looking indicator. It’s like using the high beams on your car, to see where the economy is headed three or six months from now. In the latest PMI update from February, the reading trended downward to 50.

Industrial production data came out this week down 0.5 percent in February. As I’ve discussed numerous times, industrial production is a subset of GDP, both of which indicate where the markets have been.

Regulations and high taxes are headwinds to global growth. Whether we are looking ahead or looking back, the data are showing slowdown in the global economy. We need a fiscal policy intervention to be the tailwind that pushes the economy in the right direction. We hope that the Trans Pacific Partnership (TPP) will be signed soon, eliminating many tariffs and restrictions to trade, but it is currently held up by protests from unions. Once passed, we are optimistic the TPP will facilitate and accelerate global trade.

Gold is Smiling This Week

The most welcome news was that the core consumer price index (CPI)—which excludes food and energy—rose 2.3 percent year-over-year in February, representing the fourth straight month of inflation and the highest rate since October 2008.

As I’ve pointed out many times before, gold has tended to respond well when inflationary pressure pushes real interest rates below zero. To get the real rate, you subtract the headline CPI from the U.S. Treasury yield. When it’s negative, as it is now, gold becomes more attractive to investors seeking preservation of their capital. The yellow metal has risen more than 18 percent so far this year.

Other precious metals have also been strong performers in 2016, with silver up 13 percent, platinum 11 percent, and palladium 8 percent.

Good Old American Ingenuity from Silicon Valley to U.S. Energy Fields

The U.S. Energy Information Administration (EIA) reported this week that hydraulic fracturing, or fracking, now accounts for a little more than half of current U.S. crude oil production. In 2000, fracking wells produced only 2 percent of the national total. Today, they make up over 50 percent of oil output—a figure that will likely continue to climb as technology improves.

But since the end of 2015, overall oil production in the U.S. has begun to taper down. Earlier in the week I shared with you the fact that December’s year-over-year change in output turned negative for the first time in five years, a sign that U.S. producers are finally responding to low prices.

This decline in production is reflected in the chart below, which also shows that Iraq’s share of the global oil market has grown comparatively more than Saudi Arabia and Russia’s.

The anticipated production freeze between those two countries, therefore, probably won’t have as significant an impact on oil prices as markets are hoping for. It will only ensure that the two-million-barrels-per-day global surplus won’t get any worse.

Plus, there’s no guarantee such a freeze would stick, let alone could be agreed upon. Iran has already called the proposal “ridiculous” and plans not to reign in production until it reaches pre-sanction output levels, and Saudi Arabia is unlikely to let its chief political adversary in the region gain the upper hand.

As I’ve said before, short of geopolitics, the likeliest path to oil recovery is to coordinate a production cap on a global scale. The chances of that happening, however, are slim to none.

Tax-Free, Stress-Free Income with Calm Investing

No matter what happens with the Fed’s interest rate decisions, be sure to register for our webcast on March 30. Learn about the power of municipal bonds in uncertain rate environments.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.26 percent. The S&P 500 Stock Index rose 1.35 percent, while the Nasdaq Composite climbed 0.99 percent. The Russell 2000 small capitalization index gained 1.30 percent this week.

- The Hang Seng Composite gained 2.50 percent this week; while Taiwan was up 1.20 percent and the KOSPI rose 1.05 percent.

- The 10-year Treasury bond yield fell 10 basis points to 1.88 percent.

Domestic Equity Market

Strengths

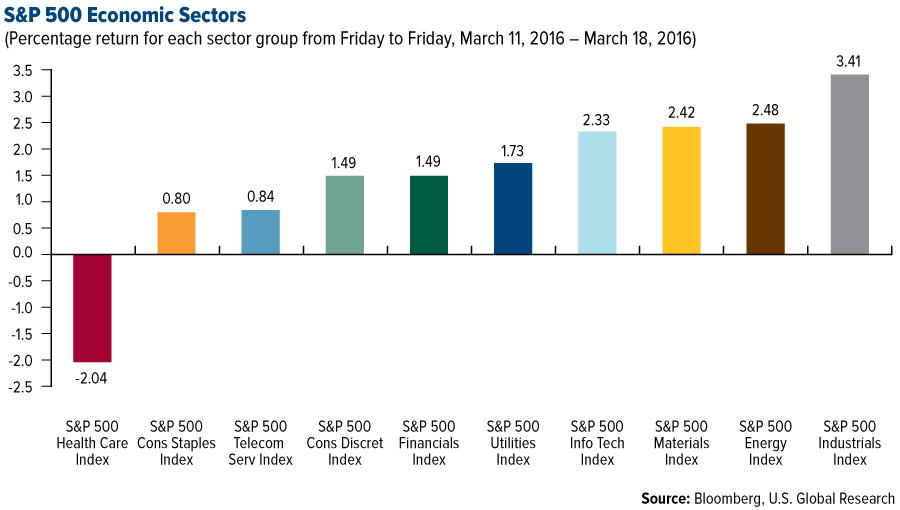

- The best performing sector for the week was industrials, increasing by 3.41 percent versus an overall increase of 1.35 percent for the S&P 500.

- Starwood Hotels & Resorts was the best performing stock for the week, increasing 14.41 percent. The company received a $12.8 billion cash offer from China’s Angbang Insurance Group, which was better than the previous offer from Marriott International.

- The operator of the London Stock Exchange agreed to merge with Germany's largest exchange operator Deutsche Boerse in an all-stock transaction.

Weaknesses

- Health care was the worst performing sector for the week, falling by -2.04 percent versus an overall increase of 1.35 percent for the S&P 500.

- Endo International was the worst performing stock for the week, falling -29.62 percent. The company revealed weaker-than-expected first-quarter 2016 guidance at the Barclays Global Healthcare Conference.

- The rout in pharmaceutical stocks continues as Valeant’s massive plunge this week leads to more investor concern.

Opportunities

- TransCanada will buy Columbia Pipeline, which will create one of the largest regulated natural gas businesses in North America. The transaction is valued at $13 billion including debt.

- China's Anbang Insurance went on a U.S. acquisition spree, announcing two high-profile deals this week. It offered $12.8 billion for U.S. hotel operator Starwood, and agreed to a $6.5 billion purchase of Strategic Hotels and Resorts, owner of the Waldorf Astoria, from the Blackstone Group.

- The allure of gold equities has risen another notch following this week’s dovish shift at the FOMC meeting. Combined with the unknown consequences and efficacy of negative deposit rates abroad, the allure of owning gold as a portfolio and currency hedge is climbing.

Threats

- A broad-based EPS contraction has already caused havoc in the overall market in recent months, but a more painful downturn has been averted because nominal GDP growth has managed to stay above long-term Treasury yields. However, leading economic indicators remain bearish, and the slide in the monetary base warns that the path of least resistance for GDP growth is lower. History shows that once GDP growth dips below the level of 10-year Treasury yields, a prolonged slump in stocks typically ensues.

- Areas hit the hardest in the sell-off have bounced the most in recent weeks, namely cyclical and interest rate sensitive sectors. In the background, however, defensive equities have stayed in favor and are the only sectors making new highs. That suggests that a fundamentally driven capital rotation into higher beta equities is not occurring. Instead, overall equity market relief reflects short covering and the resolution of oversold conditions. With no visible catalysts to push the major indices sustainably higher, the equities outlook remains bearish.

- The outlook for the S&P consumer discretionary sector looks bearish. We now face the opposite as full employment has already been reached and the Fed is poised to continue lifting interest rates this year. Historically, interest rates have been inversely correlated with relative performance.

The Economy and Bond Market

Strengths

- This week's dovish outlook from the Federal Reserve sent the U.S. dollar lower and oil higher. Both WTI and Brent pushed through the $40-per-barrel barrier. Hopes for production cuts and dwindling fears of a global recession contributed to the continued recovery in crude and other commodities.

- The Empire Manufacturing Index was reported at a positive 0.62 in March, up from -16.64 in February. The ISM-adjusted index echoed the positive jump in the headline and popped up to 51.1, above the 50 breakeven level and thereby showing expansionary conditions in the manufacturing sector in the New York area. The Philadelphia Fed Business Outlook Index jumped to 12.4 in March from -2.8 in February. The ISM-adjusted index increased to 51.7 in March from 44.7 in February, representing expansion in activity.

- The Fed's dovish commentary on inflation is getting stale fast. The evidence for a pick-up in wage and core price inflation is not just a few data points, but is broad based. Markets are only beginning to come to terms with the reality of a steady upward move in inflation.

Weaknesses

- The FOMC surprised investors with a more dovish-than-expected policy statement, a downgrade to the growth and inflation outlook, and a slower pace of planned rate hikes. The revised dot projection trimmed the number of quarter-point rate hikes this year to two, bringing it roughly in line with current market expectations. Beyond 2016, the "dots" and market expectations again diverge. The message is that an April rate hike is off the table, leaving the June meeting as the earliest we should expect the next rate adjustment.

- The Japanese central bank left policy unchanged but downgraded its economic outlook at its meeting on Tuesday. The BOJ primarily blamed a slowdown in emerging markets for the downgrade. Despite adopting negative rates at its January meeting, the BOJ must now contend with a strengthening yen, a further headwind to growth and inflation.

- Retail sales fell 0.1 percent month-over-month in February, retail sales (ex-autos) declined 0.1 percent month-over-month, and core control was flat.

Opportunities

- The recession in U.S. corporate profits is leading to weaker capex. The February durable goods orders, a key barometer for capex, will be released on Thursday. A positive surprise, given the Fed's dovish comments this week, would sustain the U.S. equity bounce.

- The March eurozone purchasing managers’ index (PMI) data released Tuesday will provide a timely update on eurozone growth. Firm readings would indicate that the recovery is continuing and that the European Central Bank (ECB) can remain on the sidelines.

- Government bond yields were pricing in an overly pessimistic scenario, having overshot to the downside in the aftermath of the global financial market turbulence that began the year. Policy rate cuts are now priced into all major markets, except the U.S. where the Treasury market has been too quick to price out Fed rate hikes for 2016. BCA recommends overweighting higher-yielding markets with slowing economic growth momentum and central banks that appear too hawkish, like the U.S. and the U.K. while underweighting markets with low-to-negative yields where the risk/reward for yields has become highly unfavorable, like Germany and Japan.

Threats

- Stocks with high operating leverage have bounced smartly in recent weeks. The materials sector in particular is fraught with companies with heavy debt loads and highly cyclical operating drivers. According to BCA, materials stocks have traditionally been late cycle plays, as earnings outperform when the economy is heating up and global resource utilization is burgeoning. Chinese money growth has perked up, but this may not lead to increased manufacturing activity and/or import demand, given high existing debt-loads, weak export growth and soft domestic activity measures such as real estate and fixed asset investment. Meanwhile, global trade remains poor. Furthermore, emerging market leading economic indicators still warn of downside economic risks. The implication is that the outlook remains bearish.

- Last week, the Federal Reserve updated its Labor Market Conditions Index (LMCI), which is a summary indicator of 19 data releases, and it came in below zero in February for the second consecutive month. The decline in the LMCI is due to weakness in the number of online job openings. If this trend persists it could eventually signal a slowdown in the pace of wage growth.

- In the U.S., the backdrop for investment grade corporate spreads remains problematic. Corporate profits are contracting, monetary conditions (both the Fed funds rate and the dollar) are far less accommodative, bank lending standards are tightening and layoff announcements are increasing. As a consequence, investors should stay cautious on investment grade corporates in the U.S.

Gold Market

This week spot gold closed at $1,255.57, up $4.87 per ounce, or 0.39 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, edged higher by 2.67 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index traded up 0.78 percent. The U.S. Trade-Weighted Dollar Index sank 1.15 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Mar-15 | U.S. PPI Final Demand YoY | 0.1% | 0.0% | -0.2% |

| Mar-16 | U.S. Housing Starts | 1150k | 1178k | 1120k |

| Mar-16 | U.S. CPI YoY | 0.9% | 1.0% | 1.4% |

| Mar-16 | U.S. FOMC Rate Decision | 0.50% | 0.50% | 0.50% |

| Mar-17 | Eurozone CPI Core YoY | 0.7% | 0.8% | 0.7% |

| Mar-17 | U.S. Initial Jobless Claims | 266k | 265k | 258k |

| Mar-22 | Germany ZEW Survey Current Situation | 53.0 | -- | 52.3 |

| Mar-22 | Germany ZEW Survey Expectations | 5.4 | -- | 1.0 |

| Mar-23 | U.S. New Home Sales | 510k | -- | 494k |

| Mar-24 | U.S. Initial Jobless Claims | 268k | -- | 265k |

| Mar-24 | U.S. Durable Goods Orders | -3.0% | -- | 4.7% |

| Mar-25 | U.S. GDP Annualized QoQ | 1.0% | -- | 1.0% |

Strengths

- The best performing precious metal for the week was silver, up 2.87 percent. Investors own the most silver in exchange-traded products in seven months, boosting holdings from a three-year low, according to ZeroHedge. This rebound comes as hedge funds and other money managers hold a near-record bet on further price gains.

- Physical gold ETF holdings have increased by over 270 tonnes since reaching their cycle-low in early January, reports TD Securities, coinciding with an 18 percent rally in the gold price. In contrast, only three tons of gold have been collected so far in India’s newly announced deposit plan. Macquarie raised its 2016 gold forecast for the precious metal by 4.8 percent, while Morgan Stanley announced its gold price outlook for the year up 8 percent to $1,173 per ounce.

- Calico Resources Corp. and Paramount Gold Nevada Corp. announced this week that Paramount has agreed to acquire all of the issued and outstanding common shares of Calico. Particulars of the transaction show that holders of Calico Shares will be entitled to 0.07 of a share of common stock of Paramount, in exchange for each Calico Share held. This represents an implied offer premium of 49.2 percent per share.

Weaknesses

- The worst performing precious metal for the week was gold, still up 0.34 percent. Gold consolidation is underway says UBS, adding that this should be healthy for the market. In its Global Precious Metals Comment this week, the group points out that pullbacks in gold so far this year have been relatively shallow and short-lived, not really offering investors many opportunities to enter at better levels.

- While the Indian jewelry trade continues its stir for withdrawal of the 1 percent excise duty announced in the Union Budget, the finance ministry does not indicate a compromise, reports the Business Standard. The strike entered its seventeenth day on Thursday. One ministry official said, “There is no question of a rollback.”

- B2Gold Corp. announced this week its approval for Gold Prepaid Sales Financing Arrangement, or prepaid sales, of up to $120 million. As stated in the company’s release, the prepaid sales (in the form of metal sales forward contracts) allow B2Gold to deliver pre-determined volumes of gold on agreed future delivery dates in exchange for upfront cash pre-payment. These financing arrangements will help fully fund the Fekola Mine Construction.

Opportunities

- CLSA’s Christopher Wood believes that the European Central Bank’s meeting last week reinforces the fact that central banks globally are addicted to unconventional monetary policies, reports Barron’s. Prior to the Bank of Japan meeting this week, Wood said that pension funds should have 70 percent exposure to the precious metal. Wood’s logic says that as we adjust for rising income, gold could peak again at $4,212 an ounce in an ultimate bull market.

- Bloomberg reports that in Japan, negative interest rates are boosting gold demand (according to the nation’s biggest bullion retailer). The same is true in Germany, where reinsurer Munich Re has boosted its gold and cash reserves in the face of the negative interest rates imposed by the ECB, reports Reuters. Last week the ECB cut its main interest rate to zero and dropped the rate on its deposit facility to -0.4 percent from -0.3 percent.

- Roxgold Inc. announced results from its latest drilling project this week from the QV1 structure at the Bagassi South regional exploration target, 1.8 kilometers to the south of the 55 zone. “Results from this program further confirm the potential at QV1,” stated John Dorward, President and CEO of Roxgold. These results make a stronger case for owning Roxgold and likely increased the prospect of Roxgold as a significant take out candidate.

Threats

- The CSFB “Fear Indicator” (specifically designed to measure investor sentiment, and represented by the index prices zero-premium collars that expire in three months) has never been higher, writes ZeroHedge. This could indicate that institutional investors are not believers in the equity rally and that there is more demand for put protection, continues the article, a sign of fear in the marketplace.

- Total business inventories have ballooned to crisis levels, according to a report from Macro Strategy Partnership. This can be seen in the chart below which shows the inventory-to-sales ratio. Inventories are up another 1.8 percent year-over-year to $1.81 trillion, and are up 18.5 percent from the prior peak in August 2008 while sales are only up 5.8 percent over the period.

- Barclays thinks that the rally in commodities is overdone, and although economic data has improved, it is not enough to support current prices. With a fragile global economy still in place, the group believes that a turning point for commodities is still some way away.

Energy and Natural Resources Market

Strengths

- Oil rose to its highest level in 2016 this week, topping $40 per barrel as OPEC and non-OPEC producers agreed to meet in Qatar mid-April to discuss an output freeze. Crude has now rallied for five consecutive weeks, its longest stretch since May last year.

- The best performing sector for the week was the S&P/TSX Diversified Metals and Mining Index. The index rallied 10.6 percent for the week following a strong 2.1 percent rebound in copper prices, mainly attributable to a weaker U.S. dollar benchmark.

- The best performing stock for the week in the broader natural resource space was First Quantum Minerals. The Canadian copper miner rose 15.5 percent for the week aided by strong copper prices and speculation that a successful asset sale the previous week will be sufficient to shore its levered balance sheet.

Weaknesses

- Iran will not take part in the OPEC and non-OPEC April meeting designed to freeze oil output and tackle the global surplus. Bloomberg reports Iran plans to boost crude output to 4 million barrels a day, the highest level since 2008, before it will consider joining other suppliers in seeking ways to rebalance the global oil market.

- The worst performing sector for the week was the Philadelphia Oil Service Sector Index. The index priced down 1.0 percent for the week after Citi analysts warned that a number of companies in the sector will have no choice but to raise equity to repair balance sheets and survive the downturn.

- The worst performing stock for the week in the S&P Global Natural Resources Index was Smurfit Kappa Group. The Irish container and packaging company posted a 3.9 percent weekly decline as the sector continues to struggle with overcapacity amid falling demand for paper products.

Opportunities

- Electric vehicle (EV) demand for copper is expected to grow five-fold over next 5 years. Although growing from a low base, the EV sector is going to have strong growth in coming years, fueled by China and its government pollution-reduction requirements and their energy-saving targets.

- Gold’s appeal is getting support from multi-year record negative real interest rates. On Wednesday, U.S. core CPI rose 2.3 percent in the 12 months through February, the highest reading since 2012. With five-year U.S. bond rates sitting at 1.34 percent, investors are locking in a near 1 percent negative real interest rate, the worst negative capture in at least three years.

- China’s Premier Li Keqiang is confident the country can achieve its growth targets. The Premier added that Beijing is ready to use “innovative” tools to strengthen the recovery, vowing to reduce taxes and bureaucracy to unleash China's entrepreneurial potential.

Threats

- The U.S. dollar is setting up for one “final leg higher,” a move normally associated with lower commodity prices, according to Morgan Stanley analysts. The bank believes the trade-weighted dollar will hit 135 by the end of 2017, a 10 percent rally from current levels, as emerging market currencies will continue to weaken until these economies eliminate their output gap.

- Copper prices have “run ahead of fundamental reality,” according to a recent Citi report, following a 14 percent rally in the metal. After all, demand for the metal is falling outside of Asia, while Chinese demand in 2015 grew at the slowest pace since 2006. In addition, Goldman Sachs forecasts that Chinese demand is unlikely to rebound this year.

- Peabody Energy, the world’s largest private coal mining company, may file for bankruptcy. The miner announced that tough market conditions in its key markets made it unable for the company to make a $71 million interest payment on Tuesday, concluding that there was a “substantial doubt” that it could continue as a going concern. Arch Coal and Alpha Natural Resources, both major U.S. coal miners, filed for bankruptcy in recent months.

China Region

Strengths

- Several equity indices throughout the region continued their recent rallies this week, with Shanghai, Singapore, Korea and the Philippines all returning better than 3 percent over the last five trading days.

- The Malaysian ringgit strengthened this week, rising about 1.3 percent to multi-month highs (falling, if one is looking at the customary spot quote). Malaysia is the region’s only net energy-exporting country.

- Fixed asset investment (FAI) in China beat expectations this week, coming in at 10.2 percent for February’s measurement, ahead of expectations for 9.3 percent and higher than January’s reading of 10.0 percent.

Weaknesses

- Industrial production (IP) and retail sales for the February period in China both came in weaker than expected last weekend, with IP at a 5.4 percent versus 5.6 percent expected, and retail sales at a 10.2 percent, shy of analysts’ expectations for 11.0 percent.

- The Indonesian rupiah was the weakest currency in the region this week, finishing slightly down despite U.S. dollar weakness.

- Indonesia and Thailand finished the week down 16 and 4 basis points respectively, underperforming the rest of the region.

Opportunities

- The Chinese yuan continues to stabilize, and the head of the People’s Bank of China (PBOC) announced last weekend that the currency will enter a period of “normalcy and rationality,” continuing a theme that government officials have reiterated from the start of the G20 Shanghai meeting and all throughout the National People’s Congress.

- Premier Li Keqiang announced plans to initiate a stock-connect program between Hong Kong and Shenzhen later this year.

- New home prices gained in 47 cities across China for the February period, up from only 38 in January.

Threats

- Bloomberg News reported this week that the PBOC drafted rules for a tax on foreign-exchange transactions, aimed at disrupting speculation against the Chinese currency.

- Labor protests—and their dispersal—in China received increased media attention this week.

- North Korea fired at least one ballistic missile more than 500 miles into the waters of the Sea of Japan, defying tightening international sanctions. Earlier this week North Korea also sentenced a U.S. student to 15 years of hard labor.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 4.5 percent. Turkey funds its debt in dollars and Turkish equites appreciated after the U.S. Federal Reserve announced more gradual rate hikes.

- The Polish zloty was the best performing currency this week, gaining 1.9 percent against the dollar. The Central Bank of Poland left its main interest unchanged at 1.5 percent. The current account balance improved and retail sales picked up according to latest data reported this week.

- The utilities sector was the best performing sector among Eastern European markets this week.

Weaknesses

- Greece was the worst performing market this week, losing 3.1 percent. Greece is working with its creditors on the 1st bailout review. European Stability Mechanism chief Klaus Regling says Greece could finish its review by May 1. The ongoing issue with refugees has made the situation more difficult as it requires a lot of time from the Greek government.

- The Ukrainian hryvnia was the worst performing currency this week, losing 4.1 percent against the dollar and erasing gains from the prior week. Fitch affirmed the Ukrainian City of Kyiv’s long term foreign and local currency Issuer Default Rating at CCC and its national long term rating at BBB with stable outlook. Fitch expects Kyiv’s finances to remain fragile over the medium term due to overall weakness of sovereign public finances.

- The health care sector was the worst performing sector among Eastern European markets this week.

Opportunities

- The U.S. Fed left interest rates unchanged and signaled fewer rate hikes in coming months, increasing investors’ appetite for more risky assets.

- Unexpectedly Russia ordered its warplanes back to Russian territory beginning Tuesday. It is unclear how long the withdrawal of Russian forces will continue, or how many Russian troops and aircrafts may remain in Syria. Peace talks began in Geneva to bring a negotiated end to Syria’s five year conflict.

- According to Olga Tanas from Bloomberg, Russian banks are sitting on the most cash in five years, allowing them to lend to each other at a lower rate than they borrow from the central bank. Banks have high level of cash after the Finance Minister transferred 2.6 trillion rubles ($37 billion) from the $50 billion rainy-day sovereign wealth fund into the economy last year to cover the fiscal gap.

Threats

- Lending in Poland fell for the first time in almost a year in February, the first month banks had to pay a tax on their assets. The government imposed a new tax of .44 percent of lenders’ assets, including loans. The tax is expected to bring a total of 4.4 billion zloty ($1.1 billion) to the state budget this year.

- The current account deficit in Turkey has been improving, but it may deteriorate in the second half of 2016. According to Finansinvest Research Team, geopolitical risk, conflict with Russia, lower tourism revenue, devalued regional currencies as well as normalized gold trade (Turkey will become net importer in 2016) will cause the current account deficit to widen. A worse than expected current account outlook will put pressure on lira.

- According to a survey conducted by Romir, 71 percent of Russians define the economic situation in the country as crisis versus 53 percent at the beginning of 2015. To cope with the crisis, 25 percent of Russians respondents are trying to find new sources of income, 22 percent are delaying expensive purchases, 11 have cancelled expensive services and 12 percent have returned to grow their own fruit and vegetables. 2016 may be difficult with further pressure on consumption and cost savings.

© U.S. Global Investors