This Chart Shows Earnings, Not Valuations or the Fed, Might Spoil the Party

For many years I have believed that three things were largely responsible for significant movements in the equity markets: the policy of the Federal Reserve (Fed), the level of valuation, and the path of earnings expectations. I still believe this and feel reasonably comfortable with two of these factors. However, the path of earnings expectations is worrying me more as the year progresses.

The Fed will likely continue to be a generally benign force for stocks for a while, focusing mainly on encouraging (not discouraging) economic growth. If that is true, then any interest-rate hike would occur only in the face of more vigorous and robust economic data than is currently being presented. A rate hike would not be a tightening but merely an adjustment to reflect those stronger data. The Fed should continue to push money toward the economy and that (all else being equal) should be a plus for the capital markets.

I don’t think stock market valuation will be a negative (although it probably won’t be a positive, either). By my count, the current S&P 500 Index price to forward bottom-up consensus earnings expectations is between 15.5 times and 16.5 times. That is also between the 30-year and 20-year trailing average of that number. The good news is that valuations are probably not high enough to offset an improvement in the fundamentals. The bad news is that they are not low enough to support us if those fundamentals turn sour. I suspect that, as usually is the case, valuations will be a result of market conditions, not a cause of them.

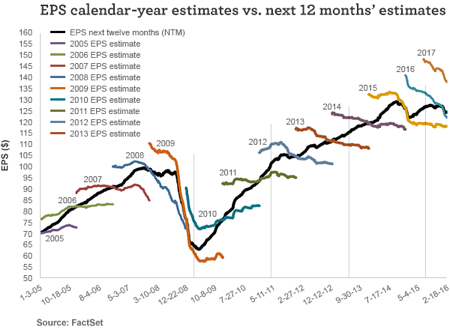

No, more and more, I worry that the risk is in a potential decline of earnings expectations. To give some context, I have included a graph showing forward earnings-per-share (EPS) expectations since 2005. Super-imposed on that line are the lines representing consensus expectations for the calendar years in that period. The reader will note that the forward line tends to rise (but not always) while the annual lines tend to diminish as time progresses. The latter fact should come as no surprise to those who realize that analysts’ first stabs at a company’s earnings in the somewhat distant future is no more than an approximation of potential earnings that will evolve into more realistic (and lower) numbers as time progresses. Its decline usually is natural and not the result of some business contraction.

However, a decline in the forward number is not natural and possibly quite dangerous. If the decline is short and shallow, it can be overlooked and, possibly, overpowered by strongly positive monetary pressure from the Fed. But, if the break is sharp and steep, it is usually the result of bad news on the economy and financial system and bad tidings for the equity market.

Earnings expectations have been flat for well over a year and bear an ominous if unfair and arbitrary comparison to 2007. Back then, it took a massive financial panic to bring the earnings expectations and the equity market significantly lower. I think the first problem is unlikely to be repeated and, therefore, a deep market decline should not be viewed as the most likely scenario.

Still, like most people, I worry. The negative stars don’t seem to have aligned as they did eight years ago. Leverage is lower, banks are stronger, and investor pessimism—not faith—seems to be the order of the day.

Yet, I always worry that I am wrong and, this time, believe that if I am making a mistake, it will be brought on by a failure in earnings growth.

However, a decline in the forward number is not natural and possibly quite dangerous. If the decline is short and shallow, it can be overlooked and, possibly, overpowered by strongly positive monetary pressure from the Fed. But, if the break is sharp and steep, it is usually the result of bad news on the economy and financial system and bad tidings for the equity market.

Earnings expectations have been flat for well over a year and bear an ominous if unfair and arbitrary comparison to 2007. Back then, it took a massive financial panic to bring the earnings expectations and the equity market significantly lower. I think the first problem is unlikely to be repeated and, therefore, a deep market decline should not be viewed as the most likely scenario.

Still, like most people, I worry. The negative stars don’t seem to have aligned as they did eight years ago. Leverage is lower, banks are stronger, and investor pessimism—not faith—seems to be the order of the day.

Yet, I always worry that I am wrong and, this time, believe that if I am making a mistake, it will be brought on by a failure in earnings growth.

Original blog post

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 2-29-16 and are those of John Manley, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management