How Much Risk Are You Taking in Your Fixed-Income Portfolio?

Summary:

- Low interest rates have left many investors stretching for additional yield. That means they may have taken on more risks in their portfolio than they intended.

- Now is a good time to check in on fixed-income portfolio allocations to make sure the level of risk is what the investor expected and doesn’t conflict with or over-amplify other risks in the portfolio.

- One way to do so is to make sure core fixed-income investments aren’t carrying more high-yield exposure or bigger macro bets than the investor intended. We believe these types of exposure are better served by more targeted and intentional allocations, not as a key part of core portfolios.

How much risk are you taking in your fixed-income portfolio?

The recovery from the 2008 financial crisis has seen the Federal Reserve keep interest rates near zero for the better part of a decade. Unprecedented monetary policy, both in the U.S. and increasingly overseas, has had plenty of unintended consequences across the financial markets. One of the effects was driving investors away from their traditional allocations toward core fixed income. Starved for yield, many investors turned to dividend-paying stocks or to lower-rated/quality bonds. Others turned the core bond portion of their portfolios over to core-plus funds seeking to get additional returns. Still others shortened duration, betting that a sharp rise in rates was just around the corner. As the volatility of the past several quarters showed, however, these investors also ended up taking on additional risk. After this long period of reaching for yield, now is a good time for investors to reassess where they stand and ask themselves, “Do I know how much risk I’ve added to my portfolio?”

Know the role bonds play in your portfolio

While each investor and investor type has their own unique angles and objectives, in general, fixed income plays an important role in the overall portfolio construction—that is, fixed-income allocations are used to provide a specific type of risk and return behavior that complements and diversifies other asset classes in a portfolio. A common theme for investors is that they look to fixed income to provide stability, consistency, and diversification when riskier parts of the portfolio may stumble.

Taking risk in fixed income? How much, and what kind?

In this market, there have been plenty of stumbles. The recent market volatility has shined a bright light on fixed-income managers and has highlighted two important questions for investors:

1. How much risk is my fixed-income manager taking?

An investment-grade benchmark can provide a reference point for investors who use bonds to form the core of their portfolio. In that case, investors should examine whether the core portion of their portfolio still has the quality and liquidity characteristics of the benchmark as a whole. For example, if they substituted a core-plus fund for a traditional core bond fund, are they still confident that the quality and liquidity characteristics of their core-plus fund are performing the volatility-minimizing role they’d originally intended? Or has the new fund added additional volatility where they weren’t expecting it?Some characteristics to look for are whether a fund:

- Employs leverage (and how much)

- Uses derivatives

- Invests in non-dollar securities

- Doesn’t have an adequate upper limit on holdings of below-investment-grade (high-yield) bonds; we believe a core bond portfolio, for example, should limit high-yield bonds to a maximum of around 5%

None of these characteristics are worrisome on their own; they’re only problematic when they’re not being put to the use the investor intended in the overall context of their portfolio. Keep your high-yield exposure, for example, out in the open where you know how it’s working for you, not obscured in the core of your portfolio where you didn’t expect it.

2. What kind of risks is my fixed-income manager taking?

There is obviously a place for market and sector-level bets in a portfolio, but we’d argue that the core position of a portfolio is a place where these bets should be treated with extra caution. Investors should instead make sure the risks they’re exposed to are intentional and targeted and aren’t overly represented in other areas of their portfolio. Pay special attention to:

- Duration risk (is there a bet that rates are going to rise or fall?)

- Yield-curve risk (is there a stance on the shape of the interest-rate curve?)

- Sector risk (over/underweighting certain segments—like mortgages or credit—of the larger bond market)

These macro-level risks can be usefully added in a targeted fashion via overall portfolio construction, so make sure that, if you are reflecting these exposures elsewhere, you’re not taking on more exposure than you intended. Investors can successfully target these risks, but it’s hard to get them consistently right over a long period of time, and it can be challenging for these types of risks to be a replicable generator of alpha, especially in the kind of violently flat volatile environment we’re navigating. That’s why we believe that, for many investors, the core bond portion of a portfolio could benefit from bottom-up, bond-by-bond security selection-driven alpha that seeks neutral duration and yield-curve exposure and avoids sector bets.

Fixed income can perform a specific role in volatile markets

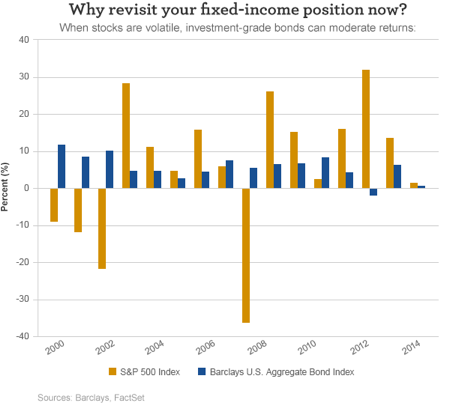

A few selected data points can help illustrate the important role that a risk-aware fixed-income allocation can play in a portfolio. From 2000 to present, the worst years for the S&P 500 Index saw annual returns of -37% (2008), -22% (2002), and -12% (2001). By comparison, across the same time frame, the Barclays U.S. Aggregate Bond Index—a widely used investment-grade bond benchmark—saw only one negative year, with an annual return of -2% (2013). The second worst year in that period was 2005, with a positive return of almost 2.5%. In 2008, when the S&P 500 Index was down 37%, the Barclays U.S. Aggregate Bond Index had positive returns.

Correlations matter: Make sure your bonds act like bonds, not stocks

Investors who want their fixed-income managers to provide stability, consistency, and diversification should look carefully at:

- Performance in volatile markets. How did your fixed-income allocation perform in 2008? What about in 2015?

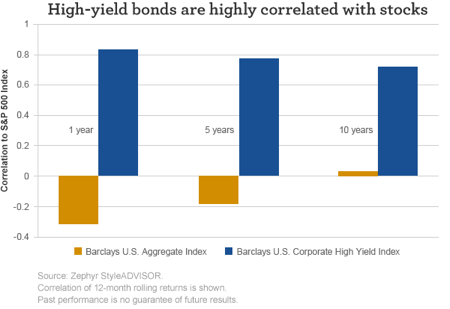

- Quality. Do you own more high-yield bonds than you expected? Over time, the Barclays High Yield Index has a correlation to the S&P 500 Index around 0.75, which means that high-yield bonds can behave a lot like equities. It’s worth keeping in mind that in 2008, when the S&P 500 Index was down 37%, the Barclays High Yield index was down 26% (the Barclays U.S. Aggregate Bond Index was up over 5%).

- Correlation. How correlated are your fixed-income allocation’s returns to equities? The Barclays U.S. Aggregate Bond Index has a roughly flat/zero correlation to equities.

Know what you own and why

Knowing what you own in fixed income is important. There can be big differences between core and core-plus funds within the Morningstar intermediate-term bond category. Within this category, around 60% of funds had allocations or allowable allocations to high-yield bonds of 10% or above. Some funds in the category had more than 50% allocated to high yield. This can provide a meaningful difference in performance behavior relative to investment-grade strategies.

In volatile markets, these differences can be important. 2015 was a year of differentiation in fixed income. For the Morningstar intermediate-term bond category, in 2015 the gap between the performance of the top and bottom deciles was 270 basis points (100 basis points equals 1.00%). That’s about 40% higher than three- or five-year averages. Only 28% of funds beat the Barclays U.S. Aggregate Bond Index in 2015.

Looking specifically at core versus core plus, in a time of market volatility these two types of fixed-income managers performed quite differently: In 2015, Lipper’s core composite returned +0.3% while its core-plus composite returned -0.5%. Did both of these styles perform the fixed-income role in a portfolio that investors were looking for? Did your bonds act like bonds in 2015? 2015 was a year of differentiation. 2016 could be as well.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 3-16-16 and are those of David Klug, CFA, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management