Five Reasons Emerging Markets Assets Have Rebounded

Summary:

- Emerging markets assets have seen a rebound—in many cases, a sizable rebound—so far in 2016, as yields have fallen, dramatically in some cases, and emerging markets currencies have mirrored this strong performance to a lesser extent.

- Many investors are asking if these improvements are temporary or if they instead represent a more stable turn for the better.

- We argue that the policy mix now in place is responsible for reversing the destructive confluence of events in 2015, which helped produce sizable declines across emerging markets equity indexes and significant intermediate-term bond yield increases in popular investment destinations.

Five reasons emerging markets assets have rebounded

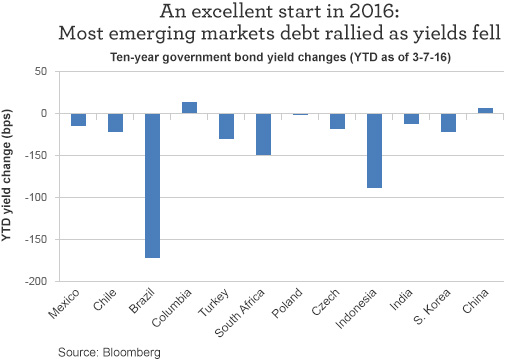

Emerging markets assets have seen a rebound—in many cases, a sizable rebound—so far in 2016. Emerging markets yields have fallen, dramatically in some cases, and emerging markets currencies have mirrored this strong performance to a lesser extent. Many investors are asking if these improvements are temporary or if they instead represent a more stable turn for the better. We argue that the policy mix now in place is responsible for reversing the destructive confluence of events in 2015, which helped produce sizable declines across emerging markets equity indexes and significant intermediate-term bond yield increases in popular investment destinations like Brazil, South Africa, and Indonesia. As a result of better fiscal policies being put in place, investors are now anticipating that restrictive monetary policies will be relaxed somewhat, which is helping drive a reassessment of emerging markets assets.

Why are emerging markets, apparently suddenly, doing better? It helps to go back to 2015. Last year, emerging markets countries faced a negative combination: Growth was slowing due to China and commodity price declines, causing some capital flight. This capital flight resulted in weakening currencies, which led to higher inflation rates. Faced by declining growth, weakening currencies, and high inflation rates, most emerging markets central banks opted to increase target rates or maintain already high rate levels—in effect, attempting to bring inflation down and force currency stability, even at the cost of slower growth.

Why the policy mix of 2015 is showing signs of success

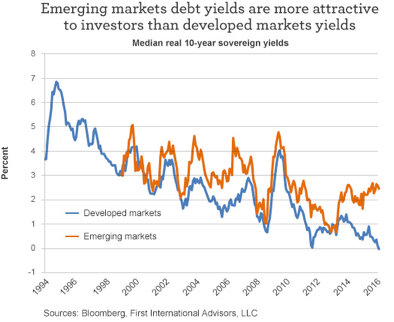

- Real (inflation-adjusted) yields are higher in emerging markets compared with developed markets. The chart below shows that valuations support emerging markets fixed income because the yield difference is at one of its widest spreads on a historical basis.

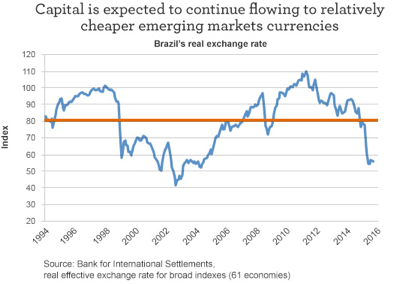

2. Most emerging markets currencies appear cheap based on common valuation metrics. This supportive valuation is a key reason capital flows into emerging markets are expected to continue over time. The chart below highlights the real effective exchange rate for Brazil’s currency, as calculated by the Bank for International Settlements. It highlights that Brazil’s currency is approximately 40% below its average real valuation since 1994.

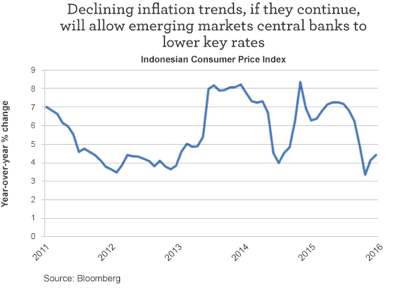

3. Inflation rates in some emerging markets countries are beginning to decline. We see this as a critical issue for fixed income to continue to do well. If inflation in emerging markets countries has peaked and shows signs of declining, central banks will be able to reverse their 2015 policies and perhaps begin reducing target rates to support growth. The best evidence for stable-to-declining inflation is in countries like Indonesia, Turkey, and Mexico. Indonesia, for example, has recently reduced interest rates twice, feeling confident enough that inflation has peaked and is trending lower.

4. The fiscal policy mix in some countries is improving. To highlight this point, earlier this month, Mexico announced an improved fiscal package, coupled with policies aimed at strengthening its currency. Emerging markets are challenged by the slow global growth outlook, but investors should be aware that even slight policy improvements can likely drive large returns given the starting valuations for many emerging markets assets.

5. China’s near-term outlook has become more stable. After currency devaluations in August and again in the fourth quarter of 2015, it appears that China has changed course slightly. Its leaders are emphasizing capital controls and similar mechanisms to control capital flight rather than further currency depreciations. While China has an overvalued currency and will face future challenges on the currency front, our view is that, over the near term, China is unlikely to devalue its currency further. That stability should be a positive for the emerging markets asset class. In addition, two of the key challenges economically for emerging markets—declining Chinese growth rates and declining Chinese domestic liquidity—are starting to show signs of abating. Overall, we assess the developments in China as slightly positive for emerging markets near term.

Where do emerging markets go from here?

Despite the significant rallies in emerging markets fixed income and, to a lesser extent, their currencies so far in 2016, emerging markets fixed income and currencies could continue their positive trend. Both emerging markets debt and currencies are cheap on a historical basis and therefore offer relative value to investors. Better fiscal policymaking in emerging markets countries, which will allow for easier monetary policies, as well as modest improvements in the near-term outlook for China also could support this asset class going forward. Investors might consider Indonesia, Mexico, Poland, Colombia, and, to a lesser extent, Brazil, where the above factors have combined to create attractive risk/return opportunities.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 3-22-16 and are those of Ashok Bhatia, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management