Editor’s Note: This week’s commentary is a collage of brief observations about an eventful first quarter. Even though this is April Fools’ Day, we are quite serious about all of these topics.

Terror, Encore

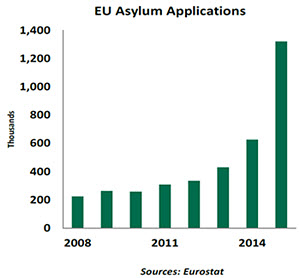

Four months after terrorist attacks struck the streets of Paris, Europe was hit again, at its heart – Brussels. The sophistication of the attacks amid tightened security has once again raised questions around intelligence-sharing across Europe’s borders, and added fuel to the migration debate.

After weathering, to varying degrees of success, the Global Financial Crisis, the sovereign debt crisis and the Greek crisis, it is now the migration crisis that threatens European unity the most. If the link between terrorism and migration (implied by populist politicians) begins to stick with the public, fears over security may begin limiting the openness that Europe has sought to maintain. Borders may close and calls for power repatriation from Brussels may increase.  This is why a united, coordinated response from European leaders is so desperately needed. The recent deal with Turkey to stem the flow of migrants may help in the short term, but it is unlikely to hold in the longer term for a host of reasons.

This is why a united, coordinated response from European leaders is so desperately needed. The recent deal with Turkey to stem the flow of migrants may help in the short term, but it is unlikely to hold in the longer term for a host of reasons.

The Brussels attacks also increase the risk of Brexit. With the polls neck-and-neck, an exogenous negative event such as this will not help those would like the United Kingdom to retain membership in the European Union.

Economically, the effect of the attacks will probably be minimal. Markets have a habit of recovering quickly after such events, and there was no interruption to financial services. But this could change in the long term if Europe becomes divided.

Go Your Own Way

Central bank divergence has been a key theme for the past several months. U.S. economic data may exaggerate this in the months ahead.

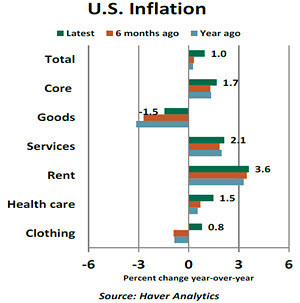

The “first stirrings” of inflation are visible in the United States. Overall inflation (as measured by the deflator on personal consumption expenditures), at 1.0%, is about 65 basis points higher than it was six months ago. It will continue to rise as the months of declining energy prices recede into the past.

Core inflation, which excludes food and energy, at 1.7%, has increased by about 40 basis points in the same period. Inflation data present widespread gains in prices ranging from higher housing costs to health care expenses and clothing prices. Inflation expectations have turned around after the decline seen in the past six months.  Despite these developments, Federal Reserve Chair Janet Yellen is not confident that these inflation readings are durable. The weak global economic environment is still seen as a risk to achieving the Fed’s objectives. But other major central banks have an extremely accommodative policy stance, which suggests that global growth is unlikely to weaken further and unleash disinflationary forces.

Despite these developments, Federal Reserve Chair Janet Yellen is not confident that these inflation readings are durable. The weak global economic environment is still seen as a risk to achieving the Fed’s objectives. But other major central banks have an extremely accommodative policy stance, which suggests that global growth is unlikely to weaken further and unleash disinflationary forces.  The March employment data suggest that the Fed is not far from achieving its other mandate. Although the March unemployment rate moved up one notch to 5.0%, it reflects an increase in the participation rate. Roughly 2.2 million people have entered the labor force in the past five months. Payroll employment rose 215,000 in March, putting the three-month moving average at 209,000. Nearly all of the U.S. labor market indicators send a positive signal.

The March employment data suggest that the Fed is not far from achieving its other mandate. Although the March unemployment rate moved up one notch to 5.0%, it reflects an increase in the participation rate. Roughly 2.2 million people have entered the labor force in the past five months. Payroll employment rose 215,000 in March, putting the three-month moving average at 209,000. Nearly all of the U.S. labor market indicators send a positive signal.

Progress on both of the Fed’s mandates makes a strong case for further actions to normalize interest rates.

Oil’s Still Not Well

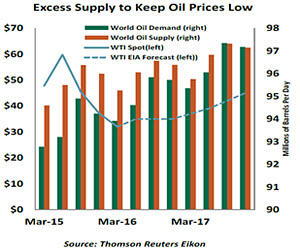

Oil prices gained more than 50% during the first quarter in what was essentially a supply story. Some analysts were quick to declare a bottom to the long decline in this market, but this conclusion may be premature.  The battle for market share means that any agreement to prop up prices will be unstable. While there have been rumors of cooperation to contain supply, nothing concrete has been agreed to. We will know more on April 17 when major producers meet to discuss a production freeze.

The battle for market share means that any agreement to prop up prices will be unstable. While there have been rumors of cooperation to contain supply, nothing concrete has been agreed to. We will know more on April 17 when major producers meet to discuss a production freeze.

Inventories suggest that the supply glut will be with us for a long while. Furthermore, the massive recent buildup in long positions in the energy futures market represents a potential for price correction when profit-taking commences.

These circumstances will not be reassuring for producers. The rig count has been falling alarmingly in the United States —currently at a low last seen at the turn of the century. The fiscal pain felt by leading international producers has contributed to recessions in Brazil and Russia, and has made Arab nations much less comfortable financially.

In the longer term, lack of capacity, demand growth and depletion of known reserves will certainly place upward pressure on prices. But these factors may take some time to gain the upper hand. It appears that cheap oil will be with us for some time.

Japan Searches for the Right Stimulus

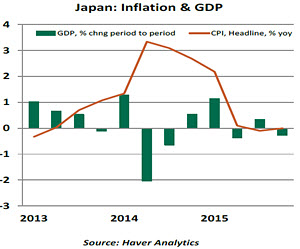

The year started with a monetary policy surprise from the Bank of Japan (BoJ) – negative interest rates. Indeed, most of the bold policy moves of the past two years have been on the monetary side, including the launch of a Quantitative and Qualitative Easing (QQE) program in April 2013 that was expanded in October 2014. Last month, BoJ Governor Haruhiko Kuroda reiterated that the Bank is willing to do more of the same, in its bid to boost inflation.

But it is increasingly obvious that fiscal policy must complement monetary stimulus if the BoJ is to stand any chance of meeting its 2% inflation target. Kuroda and Prime Minister Shinzo Abe have repeatedly called for substantial wage increases to spur demand-pull inflation, but so far, the country’s employers have not obliged. February’s target inflation measure (CPI ex-fresh food) was flat on the year thanks to low energy costs and feeble consumption, and household inflation expectations are still very weak.

But it is increasingly obvious that fiscal policy must complement monetary stimulus if the BoJ is to stand any chance of meeting its 2% inflation target. Kuroda and Prime Minister Shinzo Abe have repeatedly called for substantial wage increases to spur demand-pull inflation, but so far, the country’s employers have not obliged. February’s target inflation measure (CPI ex-fresh food) was flat on the year thanks to low energy costs and feeble consumption, and household inflation expectations are still very weak.

For Japan, a fiscal counterpart to monetary stimulus is critical as the government is by far the country’s biggest debtor. In simple terms, if the government doesn’t spend, negative rates – which have proven deeply unpopular with the public – are pointless.

The administration is working on a new fiscal stimulus package worth at least ¥5 trillion, and Abe has urged the finance ministry to front-load spending in the fiscal year 2016 budget as much as possible. But he also stated this week that the sales tax hike scheduled for April 2017 will go ahead unless the economy is hit by a severe shock. The last two sales tax hikes, in 1997 and again in April 2014, are widely assumed to have contributed to subsequent economic contractions. Will a return to recession be enough of a threat to delay the tax hike and trigger a significant fiscal stimulus package? Japan’s future may rest on the answer to that question.

Trade’s Shifting Tide

A little over four years ago, Barack Obama promised a “pivot toward Asia.” The President hoped to expand America’s trade relationships and political influence in a region that was growing very quickly. Unfortunately, the early promise of this effort has trailed off.

The economic centerpiece of this effort was the Trans Pacific Partnership (TPP), an agreement among 12 Pacific Rim countries that was signed last month. It calls for lowering trade barriers, protections for intellectual property and expedited customs procedures, among other things. Prospective benefits to American firms were counted in the billions of dollars.

But the TPP will need to be ratified locally by each of its signatories. The odds it faces in the U.S. Congress are long: voices at the edges of both political parties are questioning the benefits of free trade, especially when compared to the loss of jobs and industry that often ensue. Similar opposition is being seen in other countries which are parties to the treaty.

The Administration continues to press for passage of the TPP, but hopes are not high. As a hedge, the President visited several Latin American capitals this month to rekindle discussions of economic cooperation within the Western Hemisphere. Another pivot may be at hand.

Brazil’s Ills

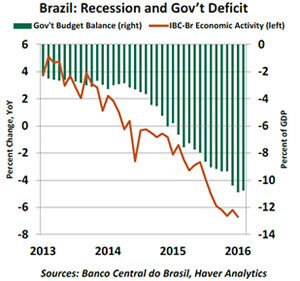

Between corruption investigations and impeachment proceedings against President Dilma Rousseff, politics have dominated the headlines in Brazil as of late. Potentially next in line to the Planalto Palace, Vice President Michel Temer has outlined an ambitious economic reform agenda that has markets upbeat.  Reforms are badly needed, as the economy suffers what is expected to be the nation’s deepest recession in a century. Real GDP fell 3.8% in 2015, with a 5.7% annualized decrease in the fourth quarter and no end in sight. Investment has contracted for 10 consecutive quarters. The national unemployment rate rose to 9.5% in January, up from 6.8% over the previous 12 months. A weak labor market combined with double-digit inflation has real wages down 2.3% over the past year.

Reforms are badly needed, as the economy suffers what is expected to be the nation’s deepest recession in a century. Real GDP fell 3.8% in 2015, with a 5.7% annualized decrease in the fourth quarter and no end in sight. Investment has contracted for 10 consecutive quarters. The national unemployment rate rose to 9.5% in January, up from 6.8% over the previous 12 months. A weak labor market combined with double-digit inflation has real wages down 2.3% over the past year.  Government finances are in the deepest hole. The gross government budget deficit has ballooned from 3.3% of GDP in mid-2014 to 10.7% in February 2016; gross government debt has risen more than 10 percentage points to 67.6% of GDP over the same period. Credit ratings are now firmly in junk territory.

Government finances are in the deepest hole. The gross government budget deficit has ballooned from 3.3% of GDP in mid-2014 to 10.7% in February 2016; gross government debt has risen more than 10 percentage points to 67.6% of GDP over the same period. Credit ratings are now firmly in junk territory.

With plans for reduced government spending, pension reform and a more independent central bank, a Temer Presidency could be just what Brazil needs. However, Temer risks being ensnared in the same corruption investigation that will likely topple Rousseff in the coming months, narrowing the scope for deep reforms. Thus, Brazil’s struggle to separate economics from politics looks set to continue.

The beginning of the summer Olympics is only four months away. One wonders which leader will open the Games, and what kind of Brazil will be on display.

Age Before Bounty

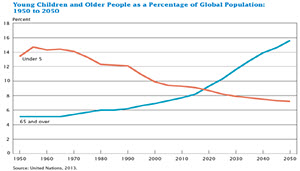

The subject of demographics is getting a lot of attention, but it probably deserves more. The composition of populations influences everything from potential economic growth to fiscal sustainability.  This week, the Census Bureau released a report entitled “An Aging World,” which is filled with interesting facts and displays. They all illustrate some inconvenient truths: many of the world’s leading economies are getting very old very fast. Absent more childbirth or increased levels of immigration, these countries can expect diminishing labor forces and stress on their social safety nets.

This week, the Census Bureau released a report entitled “An Aging World,” which is filled with interesting facts and displays. They all illustrate some inconvenient truths: many of the world’s leading economies are getting very old very fast. Absent more childbirth or increased levels of immigration, these countries can expect diminishing labor forces and stress on their social safety nets.  Unfortunately, immigration has become a four letter word in today’s populist political realm. The terrorist attacks in Belgium earlier this month will certainly not lead to more open borders for Europe. The American campaign sentiment on this issue has not been encouraging. A facet of this issue which has been little discussed is the rapid aging of some U.S. states, several of which have very challenging situations with their public pension systems. The low interest rate environment and adverse demographics will make it extremely challenging for states like Illinois to find their way back to budgetary health.

Unfortunately, immigration has become a four letter word in today’s populist political realm. The terrorist attacks in Belgium earlier this month will certainly not lead to more open borders for Europe. The American campaign sentiment on this issue has not been encouraging. A facet of this issue which has been little discussed is the rapid aging of some U.S. states, several of which have very challenging situations with their public pension systems. The low interest rate environment and adverse demographics will make it extremely challenging for states like Illinois to find their way back to budgetary health.

Fox Hunt

At the start of the Premier League soccer season in Britain, a bettor could have received 5000-1 odds for tipping Leicester City to win the title. Those chances are comparable to the average golfer getting a hole in one, or being dealt a straight flush in five-card draw poker.  Those odds are now down to 7-4 for the Foxes, who have risen from the precipice of relegation last year to brink of a championship. With a payroll that is about a fifth of what the richest clubs in the competition spend, Leicester City have a five point margin over second place Tottenham and 11 points over third place Arsenal with but seven matches left.

Those odds are now down to 7-4 for the Foxes, who have risen from the precipice of relegation last year to brink of a championship. With a payroll that is about a fifth of what the richest clubs in the competition spend, Leicester City have a five point margin over second place Tottenham and 11 points over third place Arsenal with but seven matches left.

Leicester is best-known as the final resting place of King Richard III, whose remains were found beneath a local parking lot in 2012. (Interestingly, the soccer club began its unexpected run of success just after the former monarch was given a proper burial in the Leicester Cathedral.) A premiership might not be quite so historic, but it would be a very happy event for the East Midlands. And it would offer hope for other groups facing long odds of reaching the top. Maybe a World Cup win for the United States? Now that would be a shocker.

(c) Northern Trust