China's Economy Is Transforming; It Just Needs Time

Today we have a joint blog post by Anthony Cragg and Stephen Kinney, CFA, of the Wells Fargo Emerging Markets Equity Income Fund.

The slowdown in China’s economy has been widely publicized and often takes the blame for developed market volatility. However, the decline in the growth rate of gross domestic product (GDP) is a natural and unavoidable outcome for what is now the second-largest economy in the world. We expect China to remain the fastest-growing major economy globally over the next five years.

However, in order to sustain a relatively high level of growth, the structure of China’s economy needs to change from one that is heavily dependent on fixed asset investment to one that can be supported by domestic consumption. This transition will take time.

It’s important to look below the surface of China’s economy

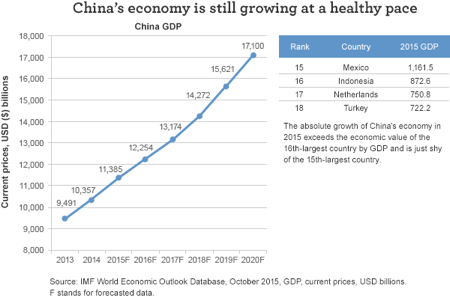

Let’s take a closer look at the current state of China’s GDP and its perceived lack of growth using World Bank data. In absolute terms, the country’s GDP is forecast to have grown $1,028.3 billion in 2015 to $11.4 trillion. The absolute growth of the Chinese economy in 2015 exceeds the economic value of the 16th-largest country by GDP (Indonesia) and is just shy of the 15th-largest country (Mexico). Moreover, the absolute year-over-year growth in China was greater than that of any other country in the world by a substantial margin. For example, the U.S. grew its economy by $620 billion in 2015. Clearly, the Chinese economy is still growing at a healthy pace.

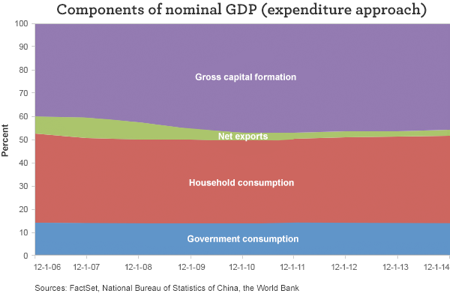

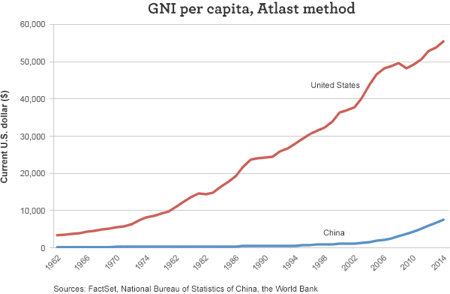

Turning to consumption, some might argue that the transition to a consumption-led economy is not happening. After all, household consumption currently accounts for 38% of nominal GDP, roughly the same level as in 2006. In absolute terms, though, China’s household consumption grew by approximately 188% between 2006 and 2014, driven primarily by urban consumption. Going forward, urban consumption should continue to grow at a steady pace, in part because of reforms to the household registration system (hukou system) that will provide basic services to cities’ migrant populations, as well as a target of reaching 60% urbanization in 2020 versus 55% today. Increased urbanization combined with a goal to bring rural residents out of poverty should spur income growth, the key driver behind consumption growth, but it will take time. According to World Bank data, at the end of 2014 China ranked 83rd in terms of gross national income (GNI) per capita at $7,400, a level reached by the U.S. in 1973. On a more positive note, income has grown roughly 600% since the turn of the century.

Growth in the services sector points toward the future

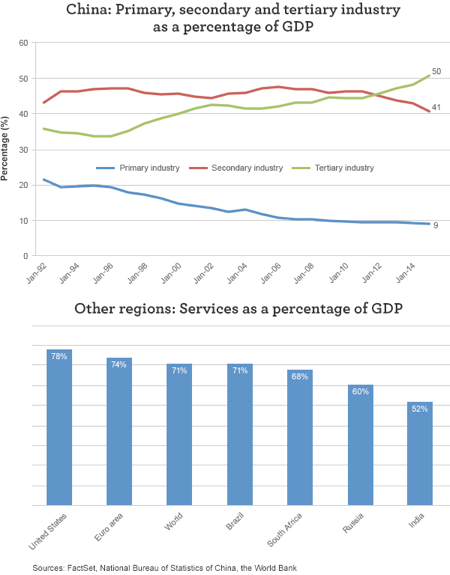

While consumption has made only modest gains as a percent of GDP, one can see China’s potential in the growth of its tertiary industry (or services sector) over the past 20 years. The services sector surpassed the secondary industry (construction and manufacturing) for the first time in 2012 and now represents more than 50% of the economy, achieving the government’s goal. However, China still trails the developed world and a number of emerging markets countries on this metric. The services sector represents more than 70% of developed market economies, and emerging economies Brazil, South Africa, Russia, and India lead China in terms of services as a percent of GDP. As China continues its transformation, the services sector could provide the potential for significant growth. In our view, all the country needs is time.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 3-30-16 and are those of Anthony Cragg and Stephen Kinney, CFA, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management