Over the weekend, Donald Trump, in an interview with the Washington Post, stated that economic conditions are so perilous that the country is headed for a “very massive recession” and that “it’s a terrible time right now” to invest in the stock market.

Of course, such a distinctly gloomy view of the economy runs counter to the more mainstream consensus of economic outlooks as witnessed by some of the immediate rebuttals:

Here is the problem.

Ben is correct. There is CURRENTLY no evidence of a recession now, or even in the few months ahead. There never is.

A Funny Thing Happened On The Way To The Recession

The majority of the analysis of economic data is short-term focused with prognostications based on single data points. For example, let’s take a look at the data below of real economic growth rates:

- January, 1980: 1.43%

- July, 1981: 4.39%

- July, 1990: 1.73%

- March, 2001: 2.30%

- December, 2007: 1.87%

Each of the dates above show the growth rate of the economy immediately prior to the onset of a recession.

You will remember that during the entirety of 2007, the majority of the media, analyst and economic community were proclaiming continued economic growth into the foreseeable future as there was “no sign of recession.”

I myself was rather brutally chastised in December of 2007 when I wrote that:

“We are now either in, or about to be in, the worst recession since the ‘Great Depression.'”

Of course, a full-year later, after the annual data revisions had been released by the Bureau of Economic Analysis was the recession officially revealed. Unfortunately, by then it was far too late to matter.

However, it is here the mainstream media should have learned their lesson.

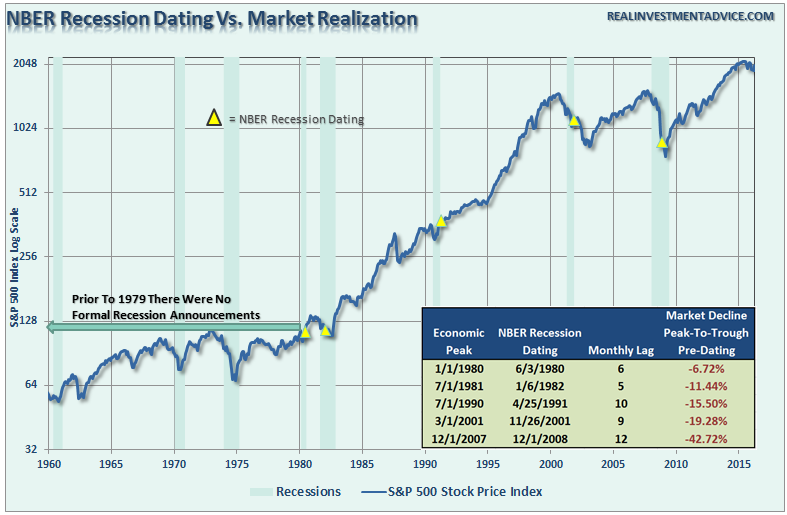

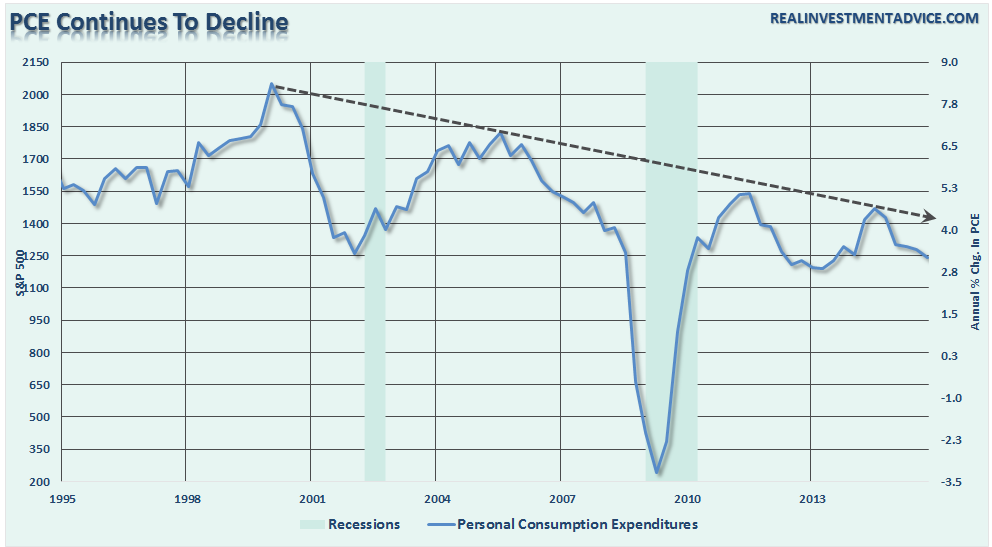

The chart below shows the S&P 500 index with recessions and when the National Bureau of Economic Research dated the start of the recession.

There are three lessons that should be learned from this:

- The economic “number” reported today will not be the same when it is revised in the future.

- The trend and deviation of the data are far more important than the number itself.

- “Record” highs and lows are records for a reason as they denote historical turning points in the data.

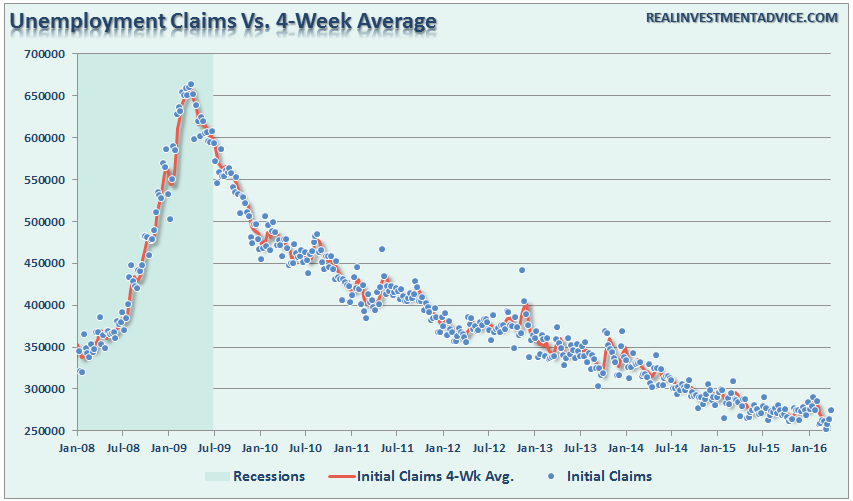

For example, the level of jobless claims is one data series currently being touted as a clear example of why there is “no recession” in sight. As shown below, there is little argument that the data currently appears extremely “bullish” for the economy.

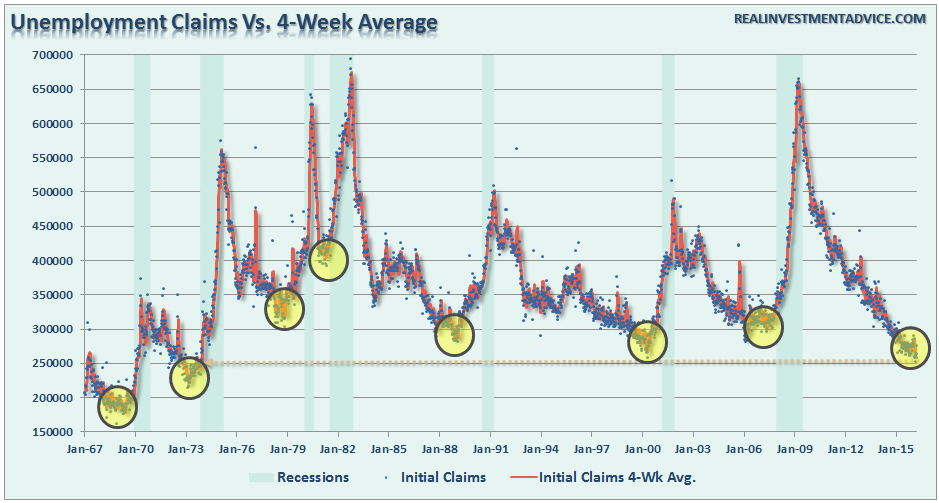

However, if we step back to a longer picture we find that such levels of jobless claims have historically noted the peak of economic growth and warned of a pending recession.

This makes complete sense as “jobless claims” fall to low levels when companies “hoard existing labor” to meet current levels of demand. In other words, companies reach a point of efficiency where they are no longer terminating individuals to align production to aggregate demand. Therefore, jobless claims naturally fall.

But there is more to this story.

Less Than Meets The Eye

The last two-quarters of economic growth have been less than exciting, to say the least. However, these rather dismal quarters of growth come at a time when oil prices and gasoline prices have plummeted AND amidst one of the warmest winters in 65-plus years.

Why is that important? Because falling oil and gas prices and warm weather are effective “tax credits” to consumers as they spend less on gasoline, heating oil and electricity. Combined, these “savings” account for more than $200 billion in additional spending power for the consumer. So, personal consumption expenditures should be rising, right?

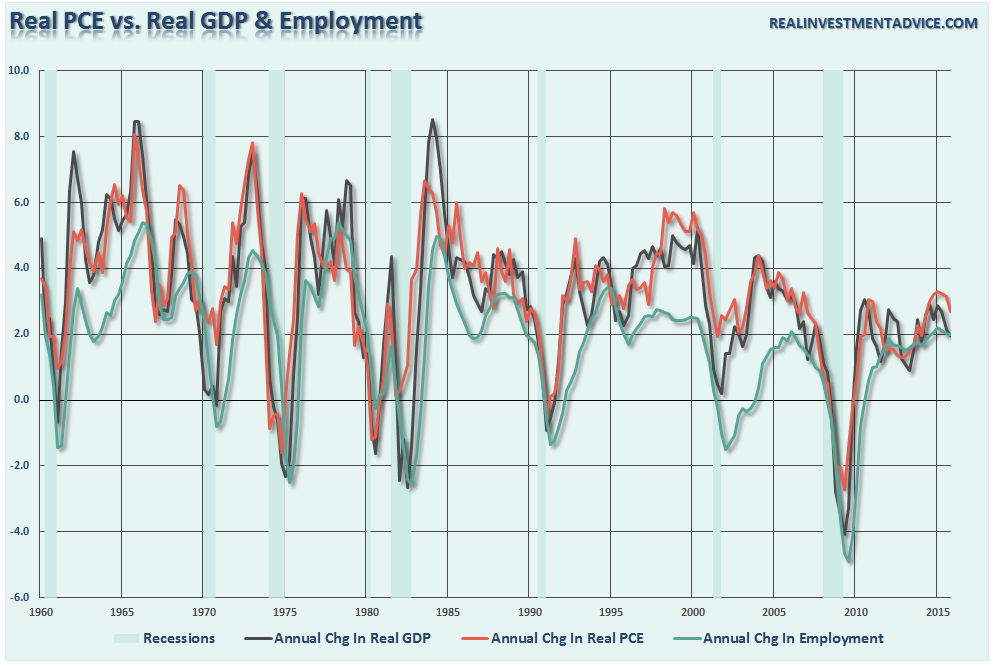

What’s going on here? The chart below shows the relationship between real, inflation-adjusted, PCE, GDP, Wages and Employment. The correlation is no accident.

Economic cycles are only sustainable for as long as excesses are being built. The natural law of reversions, while they can be suspended by artificial interventions, can not be repealed.

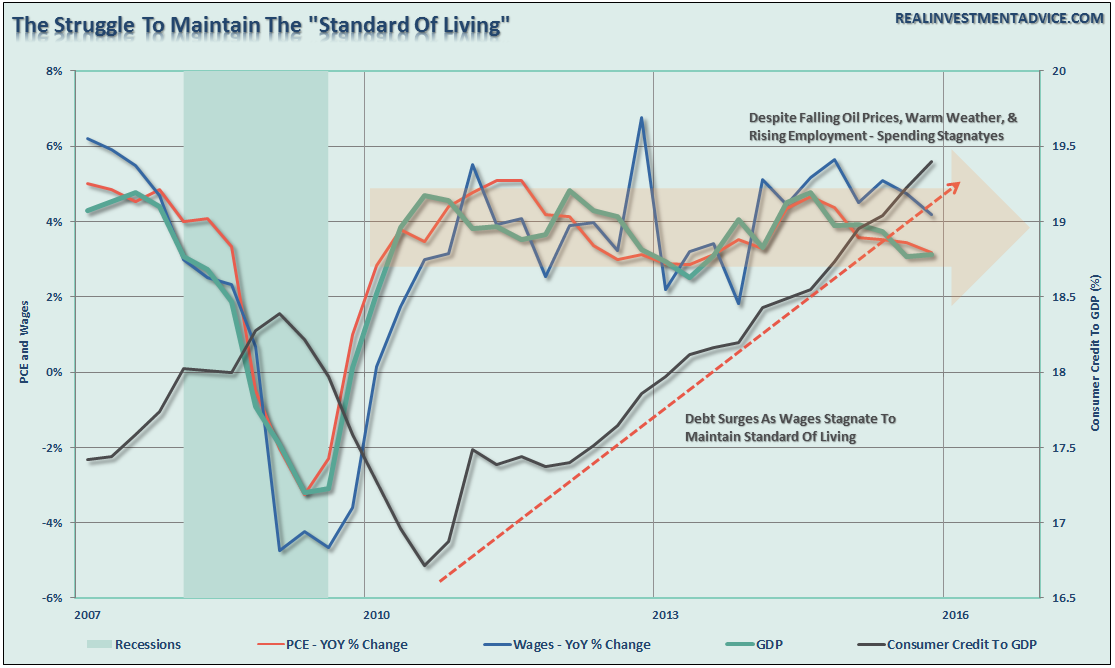

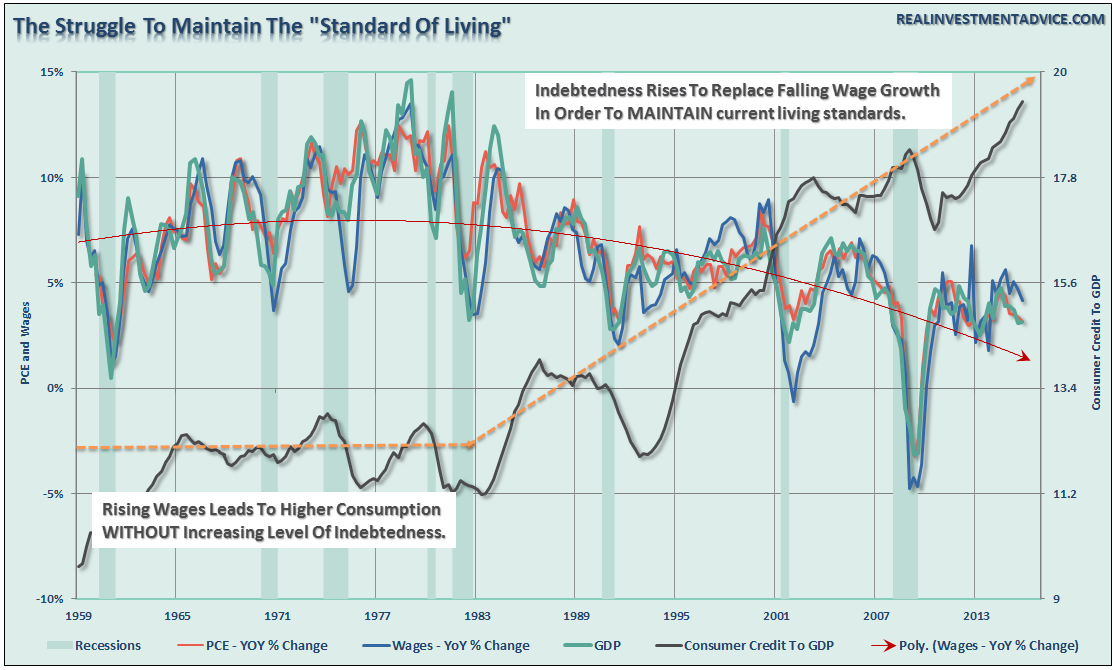

More importantly, while there is currently “no sign of recession,” what is going on with the main driver of economic growth – the consumer?

The chart below shows the real problem. Since the financial crisis, the average American has not seen much of a recovery. Wages have remained stagnant, real employment has been subdued and the actual cost of living (when accounting for insurance, college, and taxes) has risen rather sharply. The net effect has been a struggle to maintain the current standard of living which can be seen by the surge in credit as a percentage of the economy.

To put this into perspective, we can look back throughout history and see that substantial increases in consumer debt to GDP have occurred coincident with recessionary drags in the economy. No sign of recession? Are you sure about that?

Importantly, the extremely warm winter weather is currently wrecking havoc with the seasonal adjustments being applied to the economic data. This makes every report from employment, retail sales, and manufacturing appear more robust than they would be otherwise. However, as the seasonal trends turn more normal we are likely going to see fairly negative adjustments in future revisions. This is a problem that the mainstream analysis continues to overlook currently, but will be used as an excuse when it reverses.

Here is my point. While Trump’s call of a “massive recession” may seem far-fetched based on today’s economic data points, no one was calling for a recession in early 2000 or 2007 either. By the time the data is adjusted, and the eventual recession is revealed, it won’t matter as the damage will have already been done.

As Howard Marks once quipped:

“Being right, but early in the call, is the same as being wrong.”

While being optimistic about the economy and the markets currently is far more entertaining than doom and gloom, it is the honest assessment of the data and the underlying trends that is useful in protecting one’s wealth longer term.

Is there a recession currently? No.

Will there be a recession in the not so distant future? Absolutely.

Trump’s call for a “massive recession” may very well turn out not to be true. However, whether it is a mild, or“massive,” recession will make little difference as the net destruction to personal wealth will be just as disastrous. That is the nature of recessions on the financial markets.

Of course, I am sure to be chastised for penning such thoughts just as I was in 2000 and again in 2007. That is the cost of heresy against the financial establishment, but well worth paying to keep my clients from being burned at the stake, not if, but when the next recession begins.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“.