Four Emerging Markets Topics Investors Should Watch

When it comes to investing in emerging markets companies, selectivity is key.

Indeed, international markets posed several challenges for investors in early 2016. This includes official confirmation that China’s economy registered its slowest growth in years and the ongoing political scandal and economic depression in Brazil. At the same time, you’ll see pockets of opportunity if you look past the headlines. China is continuing its long transition from investment-led growth to a more balanced economy. As we mentioned in our last blog post, in absolute terms, China’s household consumption grew by approximately 188% between 2006 and 2014, driven primarily by urban consumption. India, meanwhile, has one of the fastest-growing economies in the world.

Here are four international developments that we think investors should focus on:

1. China’s continuing transition from investment-led growth

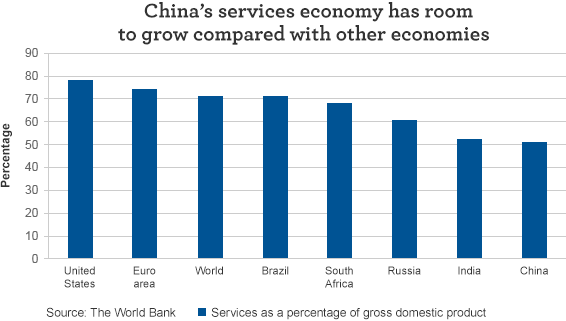

The headlines are focusing on China’s headline number for growth in gross domestic product (GDP), which dipped below 7% in 2015 for the first time since 1990. However, we are more interested in the growth of the service side of the economy. China’s tertiary industry, the services sector, surpassed construction and manufacturing for the first time in 2012 and now represents more than 50% of the economy.

The new China names tied to domestic consumption should provide more secular growth rather than the cyclical names of the old China economy. New China would include industries such as environmental protection or renewable energy as well as services such as education, tourism, health care, travel, and wealth management. As an example, while some sectors of the Chinese economy are in a dire situation, the consumer is still alive and well. The travel and tourism sector is strong, including airports and some online travel-booking companies. Consider these statistics from China Outbound Tourism Research Institute on consumer trends tied to the New Year holiday:

- Chinese consumers are spending money on outbound travel. Two of China’s travel agencies reported that 60% of all Chinese travelers that booked with them were going overseas for the holiday.

- Chinese consumers are choosing to pay for higher-quality hotels. For the New Year holiday Golden Week, more than 60% of travelers booked hotels with 4 or 5 stars, exceeding expectations.

2. Dividends become more important in a slower-growth world

China is the second-largest economy on the planet. Just by the law of large numbers, it is inevitable the country’s economy will continue to slow. However, that does not mean its stock market is going to collapse. The flip side of low growth is that companies tend to become more efficient, more productive, and more shareholder-friendly. Companies also become more likely to consider stock buybacks and dividends in a slower-growth environment.

Investors should pay attention to the dividend approach not just in China but in all emerging markets. If we are in a somewhat lower-growth world, then the dividend component of dividend income and growth becomes even more important. We also believe that a dual focus on dividends and growth can help dampen portfolio volatility because it typically favors better-quality companies with strong cash flows, strong balance sheets, and responsible management teams that allow companies to more consistently pay higher dividends. That is a risk/reward approach worth considering.

3. India’s economy shows growth and resilience

We are structurally bullish on India over the long term. Its 7.5% growth in GDP made it one of the fastest-growing economies in the world in 2015. One distinguishing characteristic of India is that it’s much less dependent on the world economy than other emerging countries, which is an advantage in times of slowing global growth.

India does have some structural challenges, and we have yet to see robust private-sector capital expenditures. Public infrastructure spending still remains an important part of the equation in India. We do see long-term catalysts for growth. For example, the Reserve Bank of India is requiring the country’s banks to recognize nonperforming loans at a faster rate, which is putting near-term pressure on bank stocks but should aid the long-term health of the banking industry. Another catalyst is a potential reform of the country’s indirect tax system to further a common internal market.

In India, we would say the main divide is between urban and rural. The rural economy remains weak, in part because the country suffered two years of poor monsoons that badly affected the rice harvest. However, this year is expected to be a good year for the monsoon. If this happens, the rural sector and companies that play in the rural sector should be able to recover.

4. Brazil’s political and economic situations remain challenged

Brazil is experiencing what we call the perfect storm of lower oil prices, a prolonged recession, widescale political corruption involving the state-owned oil company Petrobras, and a possible impeachment of President Dilma Rousseff.

The markets recently rallied on a bounce in the price of crude and on the hope that President Rousseff would be removed from power, but the oil-price bounce may not be sustained and Rousseff’s impeachment may still be averted. While the president’s recent attempt to bring former minister Luiz Inacio Lula da Silva into the cabinet backfired, having been thwarted by the Judiciary, Lula retains a lot of political influence.

Also, while one of Brazil’s major coalition parties, the PMDB, just decided to make a clean break from President Rousseff, her government may still have enough votes in the lower house for her to avoid impeachment. We think there is still asymmetric risk that the political situation could unravel. As if that were not enough, the country is suffering from the second consecutive year of severe GDP contraction.

As we’ve said before, emerging markets are volatile, but investors don’t have to invest in all of them. The key is being selective in researching companies.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 4-6-16 and are those of Dr. Brian Jacobsen, CFA, CFP® and Jo Lee, CFA, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management