Delta Force

ΔGDP = ΔPopulation + ΔProductivity

So Whom Can You Depend On?

Can We Have a Little Economic Participation, Please?

Dallas, Houston, Abu Dhabi, Raleigh, and SIC

Last week we looked at the world’s demographic destiny for the coming decades. I imagine most readers perused the information and said, “Yes, we already know the world’s population is getting older. Everybody keeps saying demographics are important, but I’d like to know how slowly changing demographics actually affect the economy here and now.

Today we are going to explore how demographic change impacts growth. (We will use lots of charts and graphs, but the text of the letter is actually shorter than usual. The whole picture is worth 1000 words thing.)

Every politician and economist wants to see the United States – and, I should point out, Europe, Japan, and the rest of the world – return to 3%-plus growth. Given that GDP in the first quarter turned out to be just 0.6% and that growth has sputtered along at less than 1% for the last six months, even the 2% growth that we’ve been averaging for the last five years sounds good now. In my just-concluded series, a letter to the next president on the economic situation he or she will face, I laid out my own plan to reinvigorate growth. But I have to admit that plan does face a strong headwind called fundamental economic reality.

Growth in GDP has only two basic components: growth in productivity and growth in the size of the workforce.

That’s it: there are two and only two ways you can grow an economy. You can either increase the (working-age) population or increase productivity. There is no magic fairy dust you can sprinkle on an economy to make it grow. To increase GDP you have to actually produce more. That's why it's called gross domestic product.

The Greek letter delta (Δ) is the symbol for change. So the change in GDP is written as

ΔGDP = ΔPopulation + ΔProductivity

That is, the change in GDP is equal to the change in the working-age population plus the change in productivity. Therefore – and I'm oversimplifying quite a lot here – a recession is basically a decrease in production (as, normally, population doesn't decrease).

Two clear implications emerge: The first is that if you want the economy to grow, there must be an economic environment that is friendly to increasing productivity.

I really want to focus on demographics and the effects that change in the working-age population will have on the growth of the economy, but let me quickly offer a few rather disconcerting graphs on the continuing decline in productivity in the US. I should note that this situation is mirrored across the developed world.

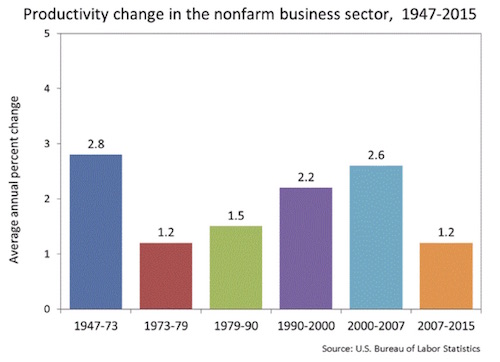

Productivity grew 0.6 percent in 2015, the smallest increase since 2013. Productivity increased at an annual rate of less than 1.0 percent in each of the last five years. The average annual rate of productivity growth from 2007 to 2015 was 1.2 percent, well below the long-term rate of 2.1 percent from 1947 to 2015.

Economists blame this decade’s reduced productivity on a lack of investment, which they say has led to an unprecedented decline in capital intensity. That is why those same economists want to keep interest rates low so that, in theory, businesses will be inclined to invest. However, there are those of us who believe that the artificially low rates put in place by central bank monetary policy actually cause reduced investment, and here’s why. Rather than encouraging businesses to compete by investing in productive assets and trying to take market share, excessive central bank stimulus encourages businesses to buy their competition and consolidate – which typically results in a reduction in the labor force. When the Federal Reserve makes it cheaper to buy your competition than to compete and cheaper to buy back your shares than to invest in new productivity, is it any wonder that productivity drops?

Look again at the chart above. Notice that in the high-inflation years of the ’70s productivity fell to roughly the level where it is today. In this next chart we see that actual productivity has grown less than 0.6% in the last two years. Toward the end of the letter we’ll come back and apply these productivity numbers to our equation above. As you might expect, this exercise will not make for pleasant reading.

The numbers suggest that productivity growth has become hard to achieve in the developed world. Mustering growth is harder in emerging markets, too, due simply to their own success. China moved millions of people from hardscrabble farming to factory floors in a relatively short period. Of course their productivity rose. So did productivity back on the farms, thanks to new machinery. Those easy gains having been booked – further productivity growth will be more elusive.

Part of the problem for the developed world is that much of its economy is now in the services sector. It is much harder to get increases in productivity in dry cleaners, restaurants, and hairdressers than it is in manufacturing or in agriculture. While there is continual growth and improving productivity in the services sector, that sector alone cannot deliver significant increases in the overall productivity rate.

And now back to population and employment, our main focus.

To varying degrees, the nations of the developed world are getting older. This is happening for two basic reasons:

- Improved nutrition and healthcare enable people to live longer.

- Fertility rates are falling toward replacement rate or even lower.

No trend persists forever, but the older-world trend is likely to continue unless something happens to reduce average lifespans and/or produce more babies.

Developed-world aging produces all kinds of economic consequences, in particular for the labor market. The total number of humans in a given place may be relatively constant or even rise, while the number of workers who can actually contribute to that place’s economy falls.

Child labor laws and customs vary. In the United States, the labor force theoretically consists of all those age 16 and over who are either working or actively seeking work. Retirement is fuzzier because people can retire around age 65, but many keep working either voluntarily or out of necessity.

As we saw last week, demographers use a statistic called the “dependency ratio,” which is the ratio of workers to the entire population. The lower the percentage of workers, the bigger each worker’s responsibility becomes for providing support to young and old dependents, either directly or through taxes.

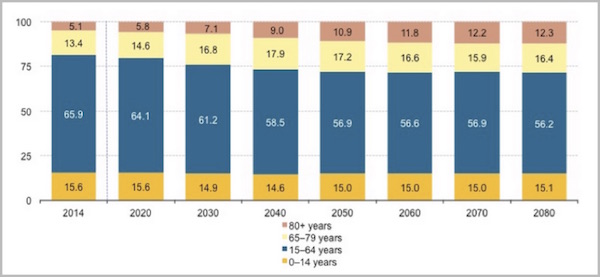

To illustrate, here is a chart from Eurostat on the projections for the EU population from 2014 to 2080.

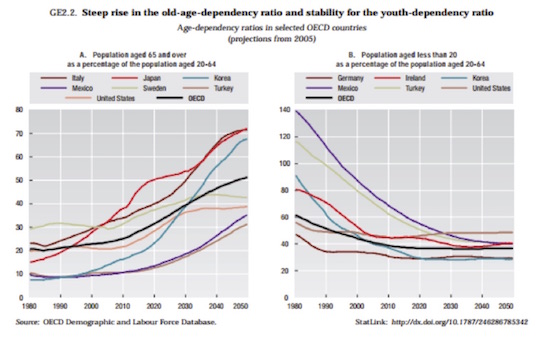

We see that in 2014, 65.9% of the EU was aged 15–64, or what we might call “prime working age.” The number shrinks steadily to around 56% by 2050 and then levels out. Why does it level out? Basically, because the forecasters assume that birthrates won’t drop much lower and that there is a limit on how long people will live. But in this next chart you can see the steep rise in the percentage of the elderly compared to those of working age, all over the developed world.

The number of children (ages 0–20) changes only slightly in the decades to come. The big change occurs in the top two segments on the previous chart, those aged 65–79 and 80+. Combined, they will grow from 18.5% of the population in 2014 to 28.7% in 2080.

These figures involve assumptions that could change. A top issue for Europe is how many immigrants it will accept and how fecund the immigrants will be compared to the current population.

Presuming, for the sake of argument, that ages 15–65 encompasses most workers, in 2014 the EU had 66% of its population working to support the 34% who were not working because they were either too young or too old. By 2040, less than 25 years from now, the EU is projected to have 58.5% working to support 41.5% who are dependents. About two-thirds of the dependents will be those age 65 and over.

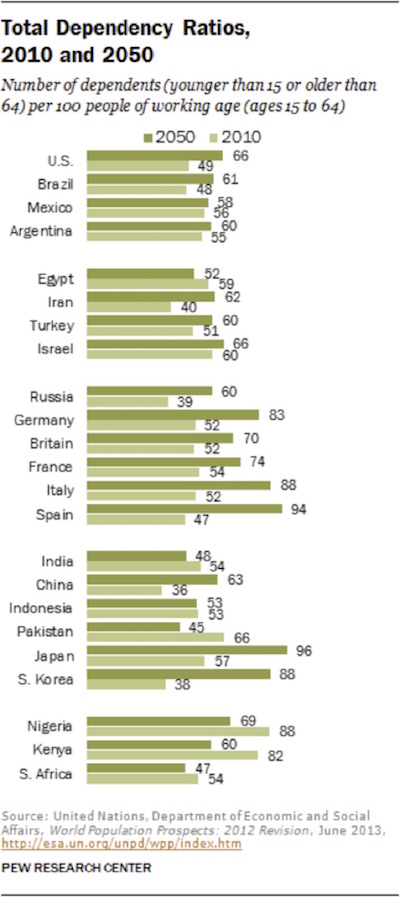

This next chart, from the Pew Research Center (based on UN data), gives us a view on how things will change between now and 2050 in a number of countries around the world. Note that Italy, Germany, and especially Spain will have significant problems with their dependency ratio within 30 years. Only Japan will have a higher dependency ratio than these three. Everyone talks about the aging of Japan, but Spain is not a great deal different; and after Spain’s last recession, so many young people left the country that the statistics are probably worse than what we are seeing in the data.

Can We Have a Little Economic Participation, Please?

Now, you might say that working-age people don’t really support the retirees. This assertion is true to the extent that retirees support themselves from savings. It is not true for retirees whose pensions depend on tax revenue and economic growth.

The number of people aged 15 to 65 doesn’t really equal the number of workers. We measure the number of actual workers by something called the participation rate. And because data for the participation rate is so robust in the United States, I’m going to focus on the US.

In the US, population growth has slowed, and productivity has fallen; that’s why we haven’t been able to boost real GDP growth to the levels seen in previous recoveries. The slow GDP growth we’ve seen in this recovery is precisely due to a much lower annual increase in employment.

What about the potential for future growth? If the “natural” unemployment rate is a little over 4% and the official unemployment rate is sitting at just about 5%, doesn’t that suggest there aren’t many more productive workers who can be added into the GDP growth mix? Actually, that is not the case. It’s really all about the participation rate.

The participation rate is a measure of the active portion of an economy's labor force. It is defined as the number of people who are either employed or actively looking for work. People who are no longer searching for work are not included in the participation rate. During a recession, many workers get discouraged and stop looking for jobs; as a result, the participation rate falls.

Now let’s look at some charts from the FRED database of the St. Louis Fed. For those not familiar with it, FRED is one of the finest databases of all things economic in the world. I am constantly amazed at the breadth and depth and range of data that you can find for free in FRED. I’m not sure just how the St. Louis Fed came to be the main repository of historical economic data, but I am grateful.

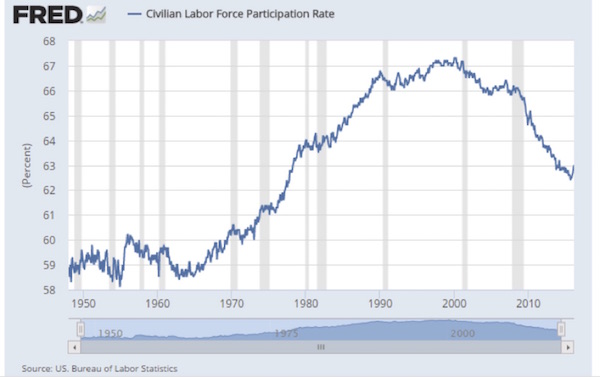

Let’s look first at the actual Civilian Labor Force Participation Rate for the United States. This rate has been falling since 2000. A big part of the dropoff reflects Boomers retiring, but since the Great Recession a significantly steeper decline has resulted as many people failed to find jobs, went back to school, or became discouraged and stopped looking for work. In theory, that means there are now a lot of people on the sidelines who are not counted as unemployed but who could be available if job opportunities materialized. So if the economy started to grow faster and those currently sidelined people once again found jobs, the number of workers would increase, and GDP would get an additional boost.

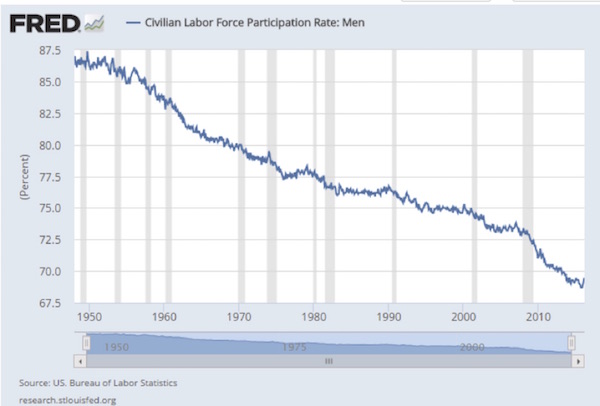

This next chart shows the participation rate for just men. It might seem a little strange that the participation rate for men has been dropping since 1950. Again, part of that falloff is the ever-growing number of retirees, but other factors are in play as well. Even with population growth, a declining participation rate this significant should have dramatically reduced GDP growth since 1950. But GDP growth between 1950 and 2000 was pretty robust, so what happened?

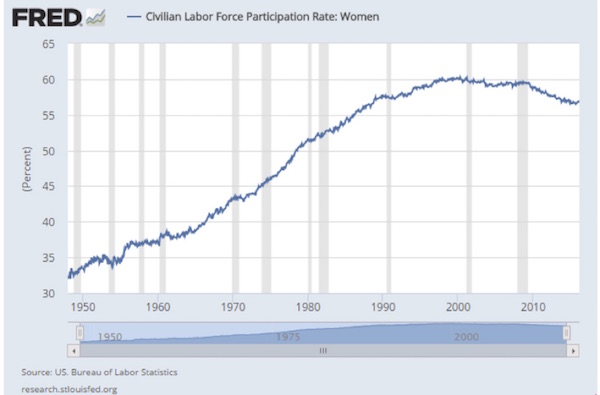

Well, this next chart happened. Women – half the population – doubled their participation rate from 1950 to 2000. In fact, they contributed 100% of the actual overall increase in the participation rate. Without their coming into the workforce, the United States would have fallen into a state of decline. However, since 2000 we have seen the participation rate of women go flat and then begin to fall after the Great Recession. Again, part of this dropoff is due to retirement, but there are other factors as well.

(Side note: Countries that don’t allow their women to participate in the economy to any significant extent are clearly inhibiting their nations’ growth. These countries usually lag the developed world in economic status, and their situation is only going to get worse until they adjust their social parameters. Just saying…)

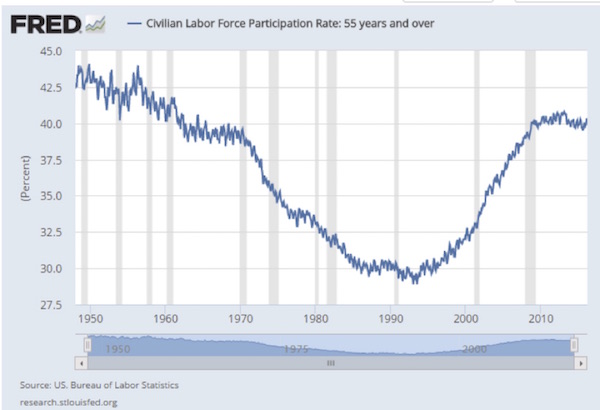

Want to see the effect of retirement on the participation rate? Let’s look at the participation rate of people 55 and older. What we see is that it dropped from 1950 through the early 1990s but has risen since rather dramatically. As we saw last week, most people 65 and over who continue in the workforce are doing so not for economic reasons but because they simply don’t want to quit. This is a new social phenomenon all around the developed world. It is not just that lifespans are getting longer; healthspans are improving as well. Older people want to work longer, be a productive part of society, and contribute to the growth of the economy. That is a good thing.

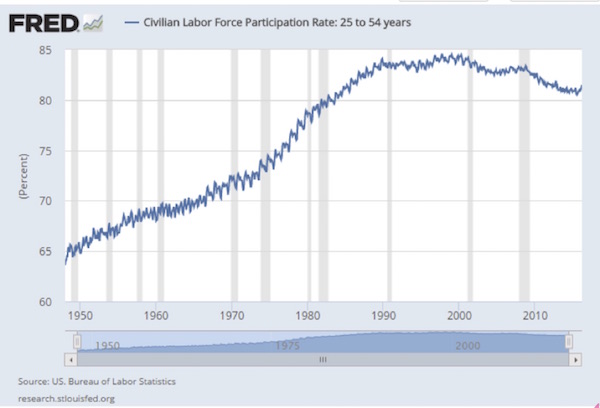

But there is another odd phenomenon going on. We are actually seeing a decline in the participation rate of 25 to 54 year-olds, people of prime working age. The labor participation rate for this group had risen continually for 50 years. There’s something going on here besides “retirement.”

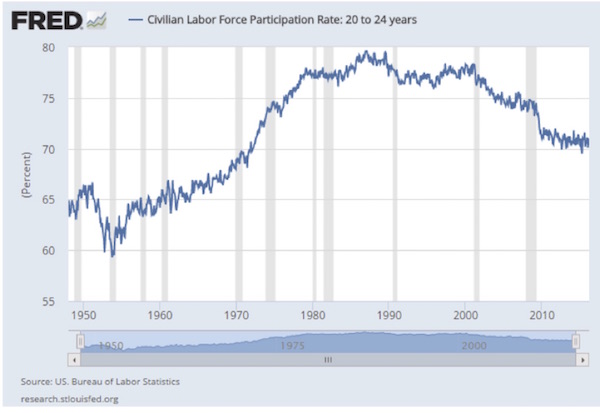

And now we delve into an even stranger phenomenon. Young people, 20 to 24, are increasingly opting out of the workforce. And this is not just a recent phenomenon. It has been happening since 2000, but the trend has dramatically accelerated in the wake of the Great Recession. Research tells us that a lot of those people are still going to school. But there are other things happening here, and we need to try to understand them.

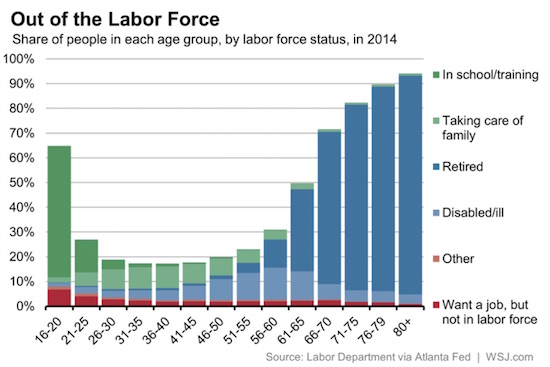

The next two charts are interesting. The first originates from the Atlanta Fed and shows the reasons why different age groups are not participating in the labor force. What I find interesting is the number of disabled people at younger ages. In the 46–50-year-old cohort, we see that 10–15% are classified as disabled. The number of people getting disability benefits has skyrocketed over the past 15 years, and especially since the Great Recession, although growth in the number on disability has flatlined in the last few years as applications have fallen off with the improvement in the economy.

Notice, too, the large numbers of people in younger cohorts who are out of the labor force because they are taking care of family. And while most of these individual situations are probably very necessary, they do have an effect on overall economic growth.

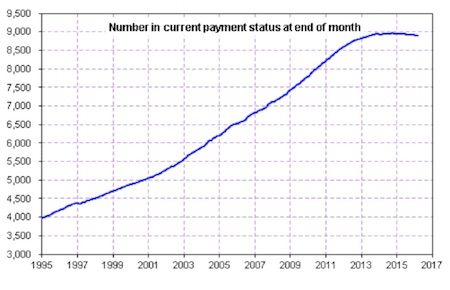

The following chart from the Social Security Administration shows the actual numbers of people with disability insurance claims. But what the chart really tells us is that these 9 million people are not available for the workforce. And while they all have their personal reasons for being on disability, their low incomes and basic lack of productivity do not contribute to the growth of the economy.

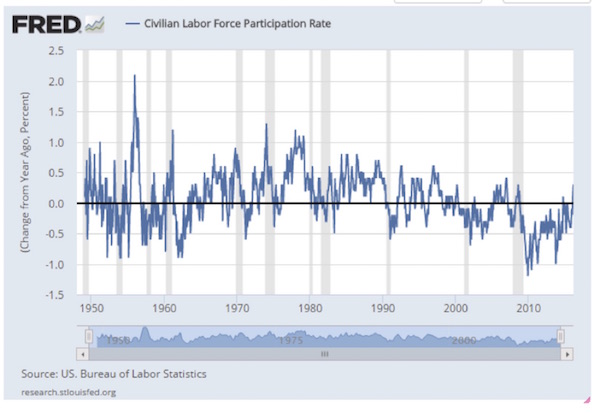

One last chart, and then we’ll try to wrap up. This one shows the percentage change in the labor force participation rate year-over-year. What we see is that the rate has generally declined since the late ’70s, except for a few years of very modest growth within the last 16 years. Returning to our basic equation, if the number of people working is not increasing, then (notwithstanding overall growth of the population) it is very difficult to eke out positive GDP numbers.

The trends we have looked at are not likely to change much, which means we are facing a long period of restrained GDP growth throughout the developed world.

This demographic cast iron lid on growth helps explain why the Federal Reserve, ECB, and other central banks seem so powerless. Can they create more workers? Not really. They can make a few adjustments that help a little – confident consumers are more likely to have children, but it takes time to grow the children into workers.

What Fed policy is clearly not doing is to encourage businesses to invest in growth. Business loan availability is still a problem in many sectors. Increasingly, businesses that can borrow do so not in order to build new facilities but rather to buy back their own stock or to pay dividends. The numbers of mergers and acquisitions, and their value, has been rising since the advent of super-low interest rates. It is cheaper to buy your competitor than to compete. Buyouts help shareholders but not workers, as they typically entail a consolidation of company workforces and a reduction in the number of “duplicated” workers. While this culling may be good for the individual businesses, it is not so good for the overall economy. It circumvents Joseph Schumpeter’s law of creative destruction.

In summary, unless something happens to boost worker productivity dramatically, we’re facing lower world GDP growth for a very long time. Could we act to change that? Yes, but as I look at the political scene today, I wonder where the impetus for change is going to come from, absent a serious crisis. And when we’re embroiled in a crisis, we’re already in a hole, trying to dig out, which means we have even further to go to achieve robust growth – assuming we can even do the right things in a crisis. Given what we did in the last crisis, it is not clear that we still have that capacity.

For investors, this is reality: developed-world economies are going to grow slower. And companies, whose revenue is essentially a function of the growth of the overall economy, are going to grow slower, too, in general.

Dallas, Houston, Abu Dhabi, Raleigh, and SIC

This week I will speak in Dallas for the seventh annual Inside Retirement conference, May 5–6. They have a great lineup of speakers, but I am most excited about getting to hear and maybe even talk with my personal writing hero, Peggy Noonan.

Then on May 10 I fly down to Houston to speak at the S&P Dow Jones Art of Indexing conference. The conference is for financial advisors and brokers who are trying to understand how to manage risk while maximizing returns in the current environment.

I will be in Abu Dhabi the third week of May and then come home and almost immediately go to Raleigh, North Carolina, to speak at the Investment Institute’s Spring 2016 Event. I’m looking forward to hearing John Burbank and Mark Yusko (who will also be at my own conference the same week) and then to being on a panel with them.

Afterward, I make a mad dash for the airport, arrive back in the Dallas late Monday night, and make final preparations for my Strategic Investment Conference, where upwards of 700 of my closest friends will gather to discuss all things macroeconomic and geopolitical. It is going to be a great week! If you won’t be going to the conference, you can have the next best thing: recordings of the speakers, delivered just a few days after SIC 2016 ends. You can order your set here. I should note the price will go up after the conference. A lot. So just jump on this offer now.

And since I’m promoting Mauldin Economics, you will shortly see (if you haven’t already) a promotion for a new investment newsletter service called the Macro Growth and Income Alert. Patrick Watson, Mauldin Economics Senior Economic Analyst, will coauthor the new letter, along with Senior Equity Analyst Robert Ross.

I first hired Patrick in the late ’80s to help me write. He had left the military and had just graduated from grad school at Rice University (which, I must confess, moved his résumé to the top of the list), but what made me take on a budding young writer was the solid portfolio of excellent writing on a variety of topics that he sent me. Not quite sure how long we worked together that time around, but maybe 10 years? He eventually moved to Austin, where he went to work for my partner and then moved on to several other publishing companies. We stayed in close touch and compared notes over the years, and a few years ago I finally persuaded him to come back to work for me.

Patrick has read everything I have written for the last 25 years (and has edited a lot of it), and he feeds me a continuous stream of research. As a result, we long ago became thinking and working partners whose ideas and styles are completely in tune.

I had to persuade my Mauldin Economics partners to pony up to afford Patrick, but I promised I would make up the difference if they didn’t think he was worth it. They now wish they could figure out how to clone him a few times. I do, too.

I think Patrick and Robert’s Macro Growth and Income Alert is going to be very successful and their readers very satisfied. As usual with a new service, we are deeply discounting the initial price, so rather than waiting to subscribe, you might want to try it out. There is a 90-day guarantee for a full and courteous refund, so that you can enjoy a risk-free trial. You can learn more right here. You may also want to follow Patrick’s always-entertaining Twitter feed @PatrickW.

I am going to hit the send button now without adding further personal comments, as I have a few things begging to be done. And it is turning into a beautiful day that I want to enjoy here in Dallas. I hope your day is just as fine, and do have a great week!

Your planning to participate in the labor market a long time analyst,

John Mauldin

© Mauldin Economics