“There’s a healthy appetite for streams right now.”

That’s according to Randy Smallwood, CEO of Silver Wheaton, who stopped by our office last week during his cross-country meet-and-greet with investors.

Randy should know about the appetite for streams. His company had a phenomenal 2015—“the best year we ever had,” he says—highlighted by two successful stream acquisitions, strong production and fully-funded growth. Silver Wheaton stock is up more than 51 percent for the year. And the company just received the Viola R. MacMillan Award, presented by the Prospectors & Developers Association of Canada (PDAC), for “demonstrating leadership in management and financing for the exploration and development of mineral resources.”

We were one of Silver Wheaton’s seed investors in 2004. In the summer of that year, the company was spun off from Wheaton River, a producer that took its name from a stream in the Yukon where one of its mines, the Luismin property, produced silver. It was founded by Ian Telfer, chairman and CEO of Wheaton River, and the company’s then-chief financial officer, Peter Barnes, who later headed up Silver Wheaton management. My friend, the mining financier and philanthropist Frank Giustra, also had a hand in its conception.

As the only pure silver mining company, Silver Wheaton couldn’t have been founded during a more opportune time. The commodities boom was still young. I remember that when the idea was shared with me, what I found most attractive was that it had virtually no competition. Franco-Nevada, which had been acquired by Newmont in 2001, wouldn’t be spun off for three more years. It was a no-brainer to put capital in this new endeavor.

Wheaton River was eventually bought by Goldcorp—the entire story is told at length in the book “Out of Nowhere: The Wheaton River Story”—and today, Silver Wheaton is the world’s largest precious metals streaming company, with a market cap of over $9 billion.

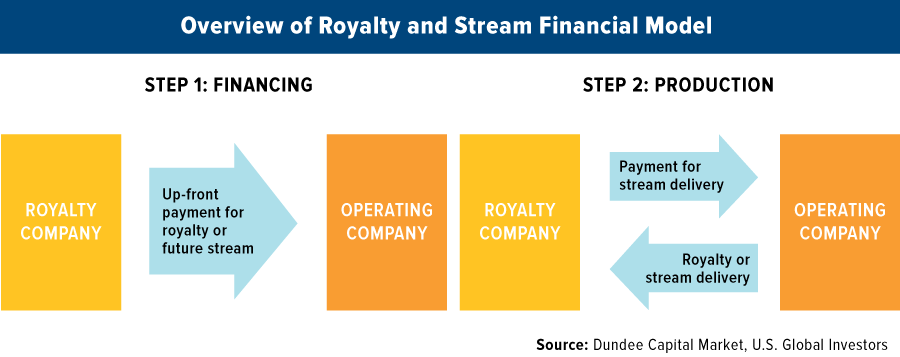

But Wait, What’s a “Stream”?

A “stream,” in case you were wondering, is an agreed-upon amount of gold, silver or other precious metal that a mining company is contractually obligated to delivery to Silver Wheaton in exchange for upfront cash. (The company’s preferred metal is silver because, as Randy puts it, it’s a smaller market and has a higher beta than gold.) The payment generally comes with less onerous terms than traditional financing, which is why miners favor working with Silver Wheaton (or one of the other royalty companies such as Franco-Nevada, Royal Gold and Sandstorm.)

Streaming allows producers to “take the value of a non-core asset and crystallize that into capital they can invest into their core franchise,” Randy explains in a video prepared for the PDAC awards.

With operating costs mounting and metals still at relatively low—albeit rising—prices, royalty and streaming companies have become an essential source of financing for junior and undercapitalized miners. Between 2009 and 2014, operating and capital costs per ounce of gold rose 50 percent, from $606 to $915 per ounce, according to Dundee Capital.

Gold and Silver at 15-Month Highs

Paradigm Capital estimates that between 80 and 90 percent of global miners’ operating costs are covered when gold reaches $1,250 an ounce. The metal is now at this level—it’s currently at $1,295, up 21 percent so far this year—but as recently as December, prices were floundering at $1,050, which cut deeply into producers’ margins.

Royalty and streaming companies, on the other hand, get by with a materially lower cost of $440 an ounce.

From only 11 stream sales in 2015, miners collectively raised $4.2 billion, which is double the amount they raised in 2013.

These partnerships are a win-win. The miner gets reliable, hassle-free funding to cover part of its exploration and production costs, and the streaming company gets all or part of the output at a fixed, lower-than-market price. A 2004 streaming arrangement made with Primero on the San Dimas mine in Mexico entitles Silver Wheaton to buy all of its silver for an average price of $4.35 an ounce. With spot prices now at more than $17.89 an ounce, up 28 percent year-to-date, the San Dimas property is one of Silver Wheaton’s more lucrative assets. (The mine represents an estimated 15 percent of Silver Wheaton’s entire operating value, according to RBC Capital Markets.)

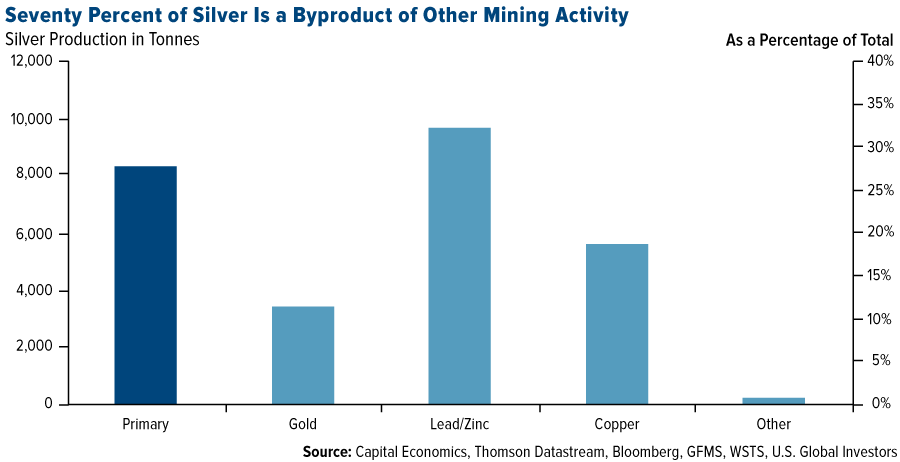

As part of its contracts, Silver Wheaton gets the added value of optionality on any future discoveries. This is important, since an estimated 70 percent of all silver comes as a byproduct of other mining activity, including gold, zinc, lead and copper. According to Randy, all of Silver Wheaton’s silver is byproduct.

Huge Rewards, Minimal Risk

Investors find royalty companies such as Silver Wheaton attractive for a number of reasons, not least of which is that they have exposure to commodity prices but face few of the risks associated with operating a mine.

They have minimal overhead and carry little to no debt. Franco-Nevada, in fact, added debt for the first time ever last year to buy a stream from Glencore. By year-end, the company had already paid down half this debt, and it plans to tackle the rest this quarter.

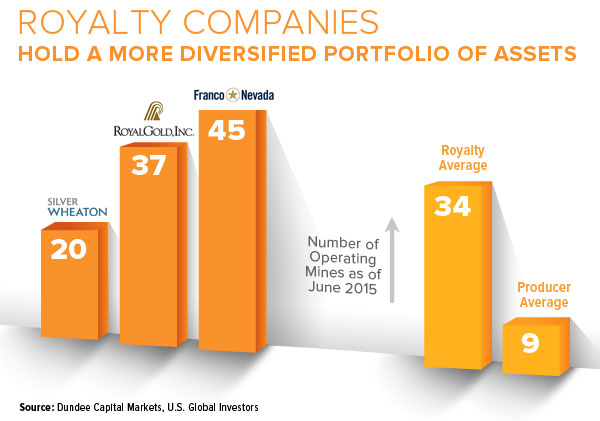

Royalty companies also hold a more diversified portfolio of mines and other assets than producers, since acquiring new streams doesn’t require any additional overhead. This helps mitigate concentration risk in the event that one of the properties stops producing for one reason or another.

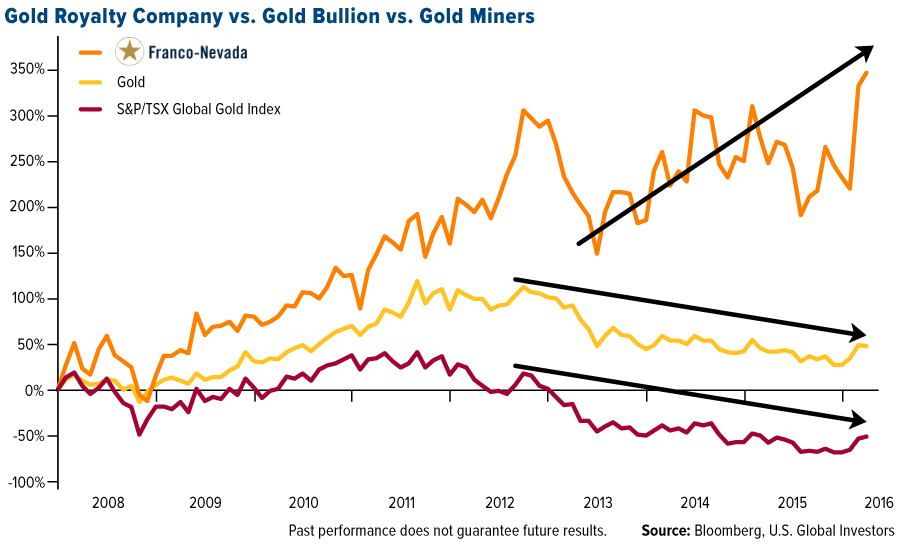

Consequently, margins have historically been huge. Even when the price of gold and gold mining stocks declined in the years following 2011, Franco-Nevada continued to rise because it had the ability to raise capital at a much lower cost than miners. And with precious metals now surging, royalty companies are highly favored, with Paradigm Capital recommending Franco-Nevada, which has “exercised the most buying discipline among the royalty companies,” and the small-cap, highly diversified Sandstorm.

click to enlarge

click to enlargeWith only around 30 employees, Silver Wheaton has one of the highest sales-per-employee rates in the world. According to FactSet data, the company generates over $23 million per employee per year. Compare that to a large senior producer like Newmont, which generates “only” $200,000 per employee.

click to enlarge

click to enlargeRoyalty companies can often minimize political risk because they don’t normally deal directly with the governments of countries their partners are operating in. This is especially valuable when working with miners that operate in restrictive tax jurisdictions and under governments with high levels of corruption. Silver Wheaton’s contract with Brazilian miner Vale, for instance, stipulates that Vale is solely responsible for paying taxes in Brazil, which are among the highest in Latin America. Vancouver-based Silver Wheaton pays only Canadian taxes.

Political risk is still a thorny issue, however. When government corruption is too pervasive, or the red tape too tortuous, the miner’s corporate guarantee is obviously threatened. In cases such as this, Silver Wheaton can simply elect not to work with the producer, as it had to do recently with an African producer.

A key risk right now is Silver Wheaton’s ongoing legal feud with the Canadian Revenue Agency (CRA), regarding international transactions between 2005 and 2010. Randy says the company might finally be nearing a resolution to the dispute.

“We do have resource risk. We do have mining production risk,” he says. “But with that risk comes rewards, and I think if we’re selective in terms of our investments, the rewards far outweigh the risks. I think we’ve been really successful making sure we invest in good quality, high-margin mines. We really put a strong focus on mines that are very profitable.”

A New Precious Metals Upcycle Has Begun

Want more on silver, gold and other precious metals? I’ll be speaking at the MoneyShow in Las Vegas, May 9 – 12. Registration is completely free. I hope to see you there!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost -1.28 percent. The S&P 500 Stock Index fell -1.26, while the Nasdaq Composite fell -2.67 percent. The Russell 2000 small capitalization index lost -1.38 percent this week.

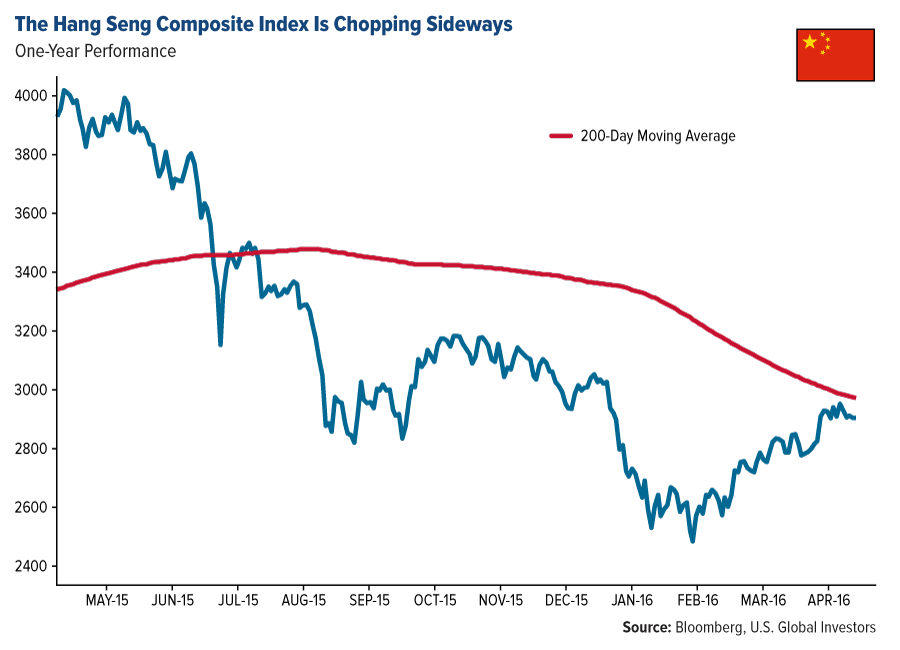

- The Hang Seng Composite lost -1.97 percent this week; while Taiwan was down -1.85 percent and the KOSPI fell -1.06 percent.

- The 10-year Treasury bond yield fell 5 basis points to 1.83 percent.

Domestic Equity Market

Strengths

- Utilities was the best performing sector for the week, increasing 2.24 percent compared to an overall decrease of 1.23 percent for the S&P 500 Index.

- St. Jude Medical was the best performing stock for the week, increasing 25.60 percent. The company is being acquired by Abbott Laboratories in a cash and stock deal valued at roughly $25 billion.

- Three pharmaceutical companies made deals this week totaling a combined $45 billion, including Abbott's $30 billion takeover of St Jude Medical, AbbVie's announced deal to acquire Stemcentrx for $5.8 billion and Sanofi's $9.3 billion bid for Medivation. Additionally, DreamWorks Animation, which produced the Shrek and Kung Fu Panda films, will be folded into Comcast's Universal unit. The deal is worth $3.8 billion.

Weaknesses

- Information technology was the worst performing sector for the week, falling 3.58 percent, versus an overall decrease of 1.23 percent for the S&P 500.

- Stericycle was the worst performing stock for the week, falling 22.92 percent. The company reported lackluster first-quarter earnings. Earnings fell 3.4 percent due to continued weak industrial hazardous waste revenue as well as a delay in capturing the expected synergies from the company’s Shred-it acquisition.

- Credit rating agency Standard and Poor's stripped ExxonMobil of its AAA credit rating this week, leaving just two U.S.-based corporations with the agency's highest rating.

Opportunities

- Movies and entertainment companies could see some upside, as one of the drivers of higher media spending has been recreational outlays. That improvement may reflect a delayed response to the windfall from lower fuel bills. Furthermore, attendance at theme parks, movie theaters and other attractions has been sufficiently strong to generate increased ticket prices.

- U.S. economic surprises have been coming on the upside lately. Housing remains resilient and the recent Institute for Supply Management (ISM) data have improved. This could be bullish for homebuilder and industrial companies.

- According to BCA’s FX strategists, the U.S. dollar’s countertrend move has more downside. This could help ease the FX pain for large multinationals.

Threats

- A slew of tech heavyweights have come up short this earnings season both on the top and bottom line fronts. More importantly, bellwether Apple struck a cautionary note on consumer electronics end-demand, especially in China, and warned that profit would underwhelm in the current quarter. This is disconcerting, especially given Apple’s global reach, and is signaling that the tech sector tide is likely turning following a nearly uninterrupted decade-long relative share price bull market run.

- Cyclical sectors are manufacturing-dependent and are therefore levered to the inventory cycle’s ebbs and flows. According to BCA, the latest durable goods report made for grim reading. Both the new orders-to-inventories and shipments-to-inventories (S/I) ratios remain tepid. The implication is that additional pain looms for cyclical sectors.

- According to BCA, banks are headed for a triple whammy of profit trouble. Loan growth is set to cool, the credit cycle has shifted from tailwind to headwind and the yield curve continues to flatten.

The Economy and Bond Market

Strengths

- Core inflation surprised higher with personal consumption expenditures (PCE) posting a solid 2.1 percent print.

- Home prices continue to climb. National home prices, as tracked by the S&P/Case-Shiller Index, appreciated 0.4 percent month-over-month, leaving year-over-year growth unchanged at 5.3 percent.

- Trade swung higher with the March advance goods trade balance report showing a marked improvement in the trade deficit to $56.9 billion from $62.9 billion in February.

Weaknesses

- U.S. gross domestic product rose just 0.5 percent in the first quarter, the third consecutive anemic start to a new year. Poor first-quarter growth in the prior two years was blamed on severe winter weather, but this winter was seasonal across most of the country. Sluggish net exports and weak corporate profits were notable developments this quarter.

- The U.S. Federal Reserve's Federal Open Market Committee (FOMC) made no move on interest rates this week and sent mixed signals on the timing of its next hike. It removed a reference to global economic and financial developments from the first paragraph of its statement, which some interpreted as a hawkish sign. But the Fed highlighted that although labor markets have continued to improve, economic activity appears to have slowed. There are seven weeks until the next FOMC meeting in June, so the committee will have plenty of data to digest before it meets to set rates again.

- Personal income climbed 0.4 percent month-over-month, but spending only inched up 0.1 percent. As a result, the saving rate picked up to 5.4 percent, matching a cycle high. It is concerning that consumption remains sluggish.

Opportunities

- Next week will see a slew of PMI releases for April, providing important information on the state of the global economy. Particular focus will be on the Chinese and U.S. manufacturing figures scheduled for Monday. Since China is Australia's largest trade partner, investors should monitor Australian data for additional confirmation of the nascent improvement in China. The NAB Business Confidence Index and manufacturing PMIs will be released on Monday.

- Even though U.S. GDP growth has been disappointing, employment has increased at a brisk pace. Continued strong job gains are needed to support optimism that growth will rebound and the Fed will be in a position to raise rates later in the year. Employment data for April will come out next Friday.

- The number of states facing budget shortfalls is declining as they benefit from the U.S. economic expansion, though the drop in oil prices is taking a toll on energy producing regions, according to Standard & Poor’s. Twenty-two states face current or projected deficits this fiscal year, down from 27 a year earlier. While states that rely disproportionately on the oil industry, such as Oklahoma, Louisiana and North Dakota, face pronounced budgetary stress, others are doing better. Revenue collections are exceeding forecasts in California, Georgia, Hawaii, Maryland, Oregon and Washington.

Threats

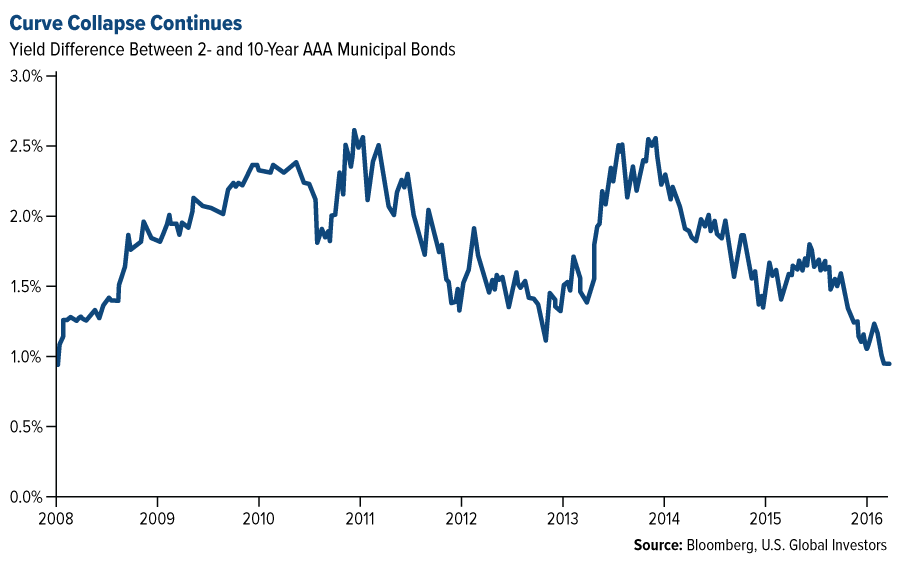

- The extra yield that investors pick up by purchasing 10-year municipal bonds rather than those due in two years has tumbled to less than 1 percent, the lowest since February 2008. That’s down from 2.56 percentage points at the start of 2014 and shows that buyers aren’t fretting about rising U.S. interest rates, which more sharply lowers the value of longer-dated securities.

- Kansas’ credit rating may be cut by Standard & Poor’s after the state lowered its revenue projections, creating a shortfall in the budget.

- Consumer confidence and consumer sentiment both headed lower in April, driven by a decrease in the expectations component. This could affect spending and retail consumption.

Gold Market

This week spot gold closed at $1,292.99, up $60.46 per ounce, or 4.91 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, rose by 12.74 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index traded up 2.85 percent. The U.S. Trade-Weighted Dollar Index slumped -2.14 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Apr-25 |

U.S. New Home Sales |

520k |

511k |

519k |

|

Apr-26 |

H.K. Exports YoY |

-6.7% |

-7.0% |

-10.4% |

|

Apr-26 |

U.S. Durable Goods Orders |

1.9% |

0.8% |

-3.1% |

|

Apr-26 |

U.S. Consumer Confidence Index |

95.8 |

94.2 |

96.1 |

|

Apr-27 |

U.S. FOMC Rate Decision |

0.50% |

0.50% |

0.50% |

|

Apr-28 |

Germany CPI YoY |

0.1% |

-0.1% |

0.3% |

|

Apr-28 |

U.S. Initial Jobless Claims |

259k |

257k |

248k |

|

Apr-28 |

U.S. GDP Annualized QoQ |

0.7% |

0.5% |

1.4% |

|

Apr-29 |

Eurozone CPI Core YoY |

0.9% |

0.7% |

1.0% |

|

May-2 |

U.S. ISM Manufacturing |

51.4 |

-- |

51.8 |

|

May-2 |

Caxin China PMI Mfg |

49.8 |

-- |

49.7 |

|

May-4 |

U.S. ADP Employment Change |

196k |

-- |

200k |

|

May-4 |

U.S. Durable Goods Orders |

-- |

-- |

0.8% |

|

May-5 |

U.S. Initial Jobless Claims |

263k |

257k |

|

|

May-6 |

U.S. Change in Nonfarm Payrolls |

200k |

-- |

215k |

Strengths

- The best performing precious metal for the week was platinum, up 6.38 percent. Platinum largely moved in sync with gold and silver price changes, but has recently outpaced its counterparts and has now begun to play a significant catch-up trade.

- The Bank of Japan (BOJ) opted against boosting stimulus this week, in a decision that battered the U.S. dollar and gave gold a surprise lift, reports Bloomberg. The Japanese yen also reacted to the bank’s decision, surging the most since the 2010 stock-market meltdown. On Wednesday, the Federal Reserve left its benchmark rate unchanged too, helping to boost the yellow metal.

- According to the South China Morning Post, the Chinese Gold and Silver Exchange Society plans to set up a gold vault and office in Qianhai. This will be the biggest in Hong Kong investment in the special economic zone in Shenzhen, reports Bloomberg. Jeremy Wrathall, Investec’s Global Head of Natural Resources, thinks that gold is likely to be the best performer among global metals and minerals for 2016, reports Lawrie Williams.

Weaknesses

- The worst performing precious metal for the week was palladium, still up 3.93 percent, and not far behind the other precious metals (all of which closed in positive territory). Palladium was the best performer in the precious metals group last week, when it closed up 5.99 percent.

- Commodity exchanges boosted margin requirements on more products, reports Bloomberg, sending stocks in China to the lowest in a month. “The boom in the commodity markets isn’t a good thing for stocks as that will distract some investors and divert money away from the stock market,” said Wu Kan, a fund manager at JK Life Insurance in Shanghai.

- The metals and mining sector is the top performer in both high-grade and high-yield indexes this year, according to BI Senior Credit Analyst Richard Bourke. But has the rally in metals and mining bonds come too far, too fast? An analysis of commodity spot prices shows that they are all above consensus forecast price, and may portend a correction.

Opportunities

- RBC Capital Markets released a research piece on its gold companies under coverage on Monday, explaining that a decline in production and growth expenditures is expected in 2016. Overall gold production of the North American companies listed in the report, is expected to decline by 7 percent year-over-year. Exploration and expenditure budgets continue to face downward pressure as well, leading to an ongoing decline in reserve lives. While this may appear negative at first glance, the forecast should bode well for acquisition activity to pick up later this year in a heated gold market.

- HSBC has been bullish on gold since 2015 and the group believes that the strong rally this year could continue. In addition to gold’s inverse relationship with the U.S. dollar, HSBC points out that the group’s counter-consensus view of a strong euro, along with the expectation for the euro-dollar to continue trading higher. Investors may also take a gold position to hedge against the upcoming UK vote to exit European Union membership.

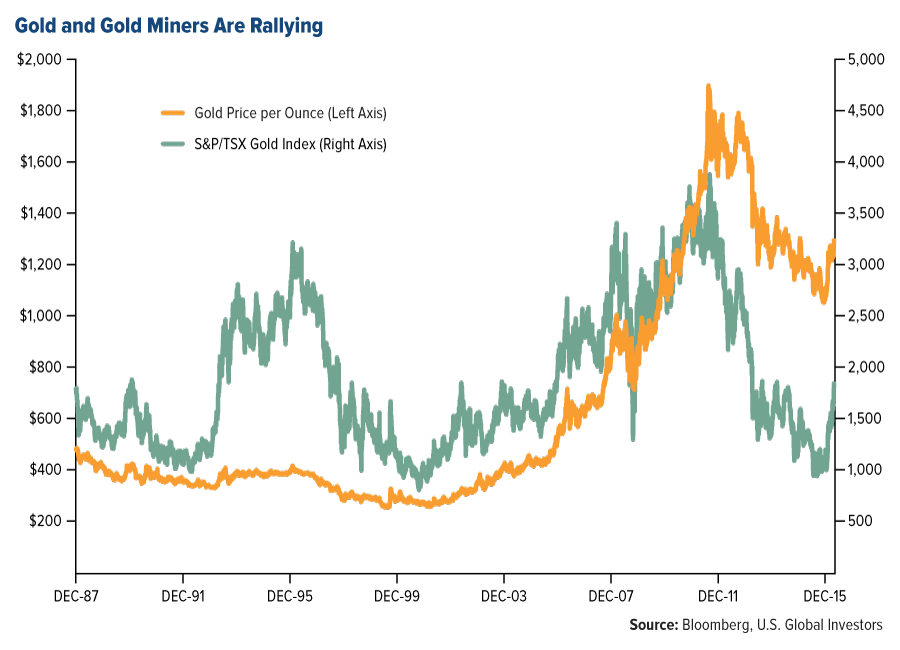

- Paradigm Capital released a comprehensive and informative research note this week, focusing on gold equities and opportunities to be found for the generalist. The group highlights negative interest rates and central banks buying gold (rather than selling it) as a few reasons why this up-cycle is different. Paradigm also states that “Producing gold is a better business than most today, one with expanding margins, yet gold equities still offer excellent relative value.” In the chart below, this shows the long-term price relationship between gold bullion and gold mining stocks. One can observe that the gold miner valuations are currently substantially depressed relative to the change in gold prices.

Threats

- Earlier this month, Deutsche Bank admitted to manipulation of the gold and silver price fix, agreeing to turn in any information about other banks’ wrongdoings over to the authorities. In an article from ZeroHedge this week, the group reminds its readers that the CFTC in 2013 closed its five-year investigation concerning these allegations, proudly stating there was no evidence of wrongdoing. Fast forward to April 22, 2016. The CFTC and its director have come out saying they were unaware of the DB story, finding no reference to it in the commission’s file of “news reports of interest.”

- Could silver’s upswing be due for a correction? Another article from ZeroHedge this week points out that an old indicator, the commitment of traders report (COT), has been a pretty reliable gauge for precious metals’ “short-term trajectory.” However, since speculators are “exuberantly long” silver at this time, this could imply that a correction is coming.

- Although no one is predicting a heavy fall for precious metals, a commodity specialist from the Industrial and Commercial Bank of China (ICBC Standard) thinks now is probably not the time to buy, reports News Markets. The bank pinpoints an already crowded market for this trade, as speculators have increased their long positions.

Energy and Natural Resources Market

Strengths

- The bullish thesis for gasoline should withstand the rise of electric vehicles. Goldman Sachs’ recent gasoline forecast suggests that Tesla’s ability to book 325 thousand reservations for its Model 3 won’t affect the strength of gasoline markets. Gasoline growth in 2016 should continue tracking above the five-year average owing to low oil prices and the low penetration rate of electric vehicles (EVs). Longer term, increased EV sales should be a headwind to U.S. gasoline demand. However, the effect should be manageable as research shows as many as 3.6 million (0.2 million in 2015) EVs are needed to lower U.S. gasoline demand by 1 percent.

- The best performing sector for the week was the TSX Diversified Metals and Mining Index. The index of base metals producers rose 16 percent, helped by a late-week rally in copper prices, supported by a weakening U.S. dollar. In addition, a number of companies in the index posted favorable earnings reports.

- First Quantum Minerals, a Canadian copper producer, rose 23.6 percent for the week after first quarter earnings beat analysts’ estimates. The company boosted its copper output to 131 thousand tonnes, 11 percent above estimates. As a result, the company is no longer expected to breach its debt covenants in 2016.

Weaknesses

- Canada National Railway, one of the five major railway companies in North America, has a bearish outlook on 2016. The company reduced its 2016 earnings forecast following a 4 to 5 percent downgrade to its carload volume expectations. The company mainly transports crude, frac sand, coal and lumber.

- The worst performing sector for the week was the S&P Oil & Gas Refining and Marketing Index. The index fell 5.8 percent following disappointing quarterly results by Marathon Petroleum and Phillips 66, which led analysts to downgrade expectations for the remaining members of the index.

- The worst performing stock for the week in the S&P Global Natural Resources Index was JFE Holdings. Japan’s second largest steel manufacturer dropped 13 percent after reporting a 76 percent drop in net income, while expressing doubts over the sustainability of the recent rally in steel prices.

Opportunities

- High-cost Chinese steel mills may finally be taken off market as China’s top steel making province said it will ban the reopening of steel mills after the May Day holiday. A jump in steel prices this year encouraged many closed mills to restart their furnaces and ramp up production, leading to China's steel output to rise to a record in March.

- The worst is over as China boosts demand according to Tom Albanese, chief executive officer of Vedanta and a former head of Rio Tinto Group. Albanese stressed that policymakers in China have added stimulus, lifting property prices, which translates into improved fundamentals for most major commodities.

- Anglo American, the struggling South African mining company, has agreed to sell its Brazilian niobium and phosphate units for $1.5 billion in cash to China Molybdenum. The deal was priced significantly above analysts’ expectations, suggesting there is still significant mergers and acquisitions (M&A) appetite in the natural resources space.

Threats

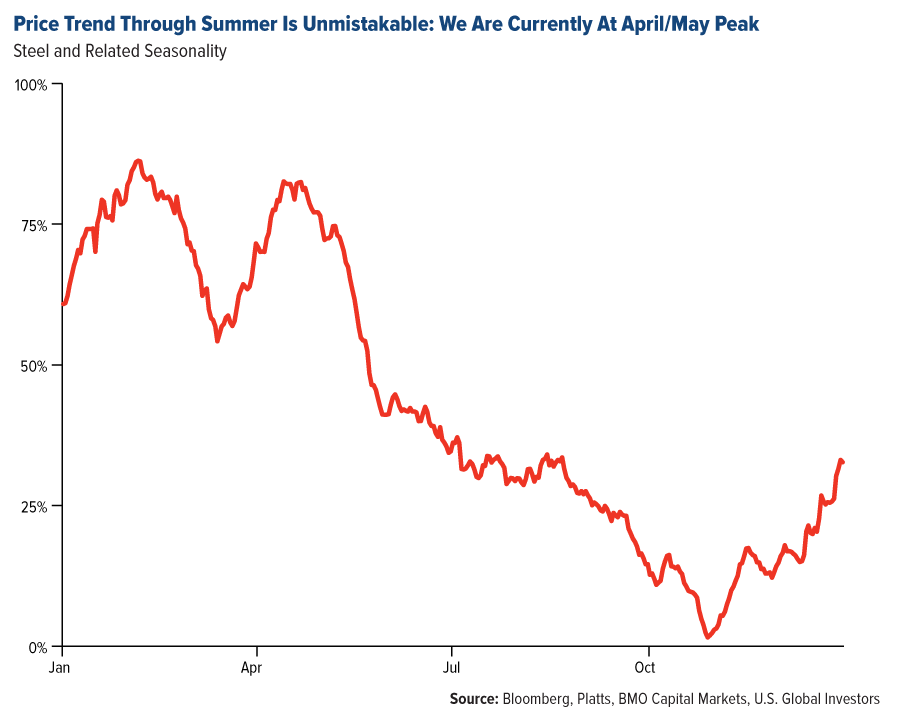

- The seasonality of steel prices suggests a correction is imminent. BMO Research highlights that steel price declines typically start around China’s May Day holiday, and the infamous Tangshan flower show, both of which start this weekend. A pullback in steel prices would more than likely result in a pullback in iron ore prices.

- The recent pick-up in Chinese demand is seasonal and has not yet provided any evidence of a permanent turn as the nation’s growth continues to slow, according to Barclays’ analysts. Metals prices weakened earlier in the week as increases in copper inventories at the London Metal Exchange (LME) supported the view that Chinese imports may stall.

- Crude oil’s rebound may struggle to maintain its level after OPEC's oil output rose in April to close at its highest level in recent history. A Reuters survey showed production increases led by Iran and Iraq more than offset a strike in Kuwait and other outages.

China Region

Strengths

- Thailand’s SET Index finished the week as the top performer, closing the last five trading days just worse than flat in a volatile week around the globe, and as Hong Kong, the Chinese mainland and several other regional markets head into a long weekend.

- Industrial profits rose year-over-year in China for the March period, up 11.1 percent.

- Though a distant second to the obvious global strength of the Japanese yen this week, the Singapore dollar put in a strong performance, rising nearly 0.7 percent. The Chinese renminbi also gained for the week, particularly after a very strong fixing on Friday.

Weaknesses

- Thailand’s Finance Ministry announced it was lowering its expectations for 2016 growth from 3.7 percent to 3.3 percent.

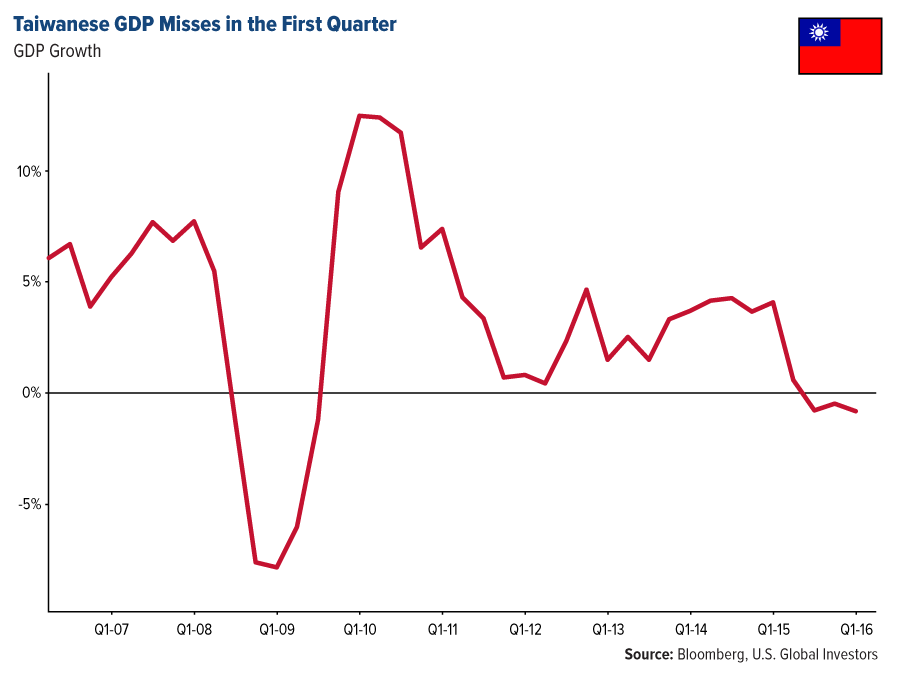

- Taiwan’s economy contracted in the first quarter. Year-over-year GDP declined 0.84, missing analysts’ expectations for a decline of only 0.65 percent.

- Retail investor interest in mainland Chinese equities has waned recently, Bloomberg reported this week, as investors and speculators have instead focused on real estate and the commodities markets. The report comes the same week that Caixin reported the PBOC has asked banks to scale back lending by 30 percent.

Opportunities

- Beijing announced it will sign the Paris Climate Agreement ahead of the September G20 meeting in Hangzhou, which could be another positive long-term catalyst for green energy in China.

- Vietnam Airlines Corp. announced it expects its shares to start trading sometime later this year, as Vietnam continues to develop its economy and as investor interest in the country’s prospects continue to grow. Vietnam remains a major potential beneficiary of the Trans-Pacific Partnership (TPP).

- Evercore ISI anticipates the International Monetary Fund (IMF) will raise its 2016 China GDP outlook to 6.5 percent from current expectations of 6.2 percent. Investors get more data on China starting this weekend, too: Official Chinese government PMI comes out this weekend, and Caixin comes out next week.

Threats

- Indonesia’s OPEC governor suggested that there is no urgency to freeze oil production after the recent rally in crude prices.

- Concerns over corporate debt defaults continue to roil Chinese bond investors.

- Chinese banking authorities in Shanghai placed a one-month halt on business between commercial banks and six major real estate companies in an effort to cool the sizzling Shanghai property market.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 47 basis points. The central bank lowered its benchmark rate by 15 basis points, from 1.2 percent to 1.05 percent.

- The Russian ruble was the best performing currency this week, gaining 2.8 percent against the dollar. The Bank of Russia left its benchmark rate unchanged at 11 percent and signaled future cuts if inflation risks decline. Brent crude continued its uptrend, gaining an additional 6.7 percent in the past five days.

- The energy sector was the best performing sector among Eastern European markets this week.

Weaknesses

- Greece was the worst performing market this week, losing 3.7 percent. Greece’s government and the International Monetary Fund (IMF) did not reach an agreement on the country’s bailout program. Talks ran into trouble over how to find up to 3.6 billion euros ($4 billion) of additional austerity if Greece misses its budget targets.

- The Ukrainian hryvnia was the worst relative performing currency this week, gaining 80 basis points against the dollar. All Eastern European currencies appreciated while the dollar corrected sharply.

- The consumer staples sector was the worst performing sector among Eastern European markets this week.

Opportunities

- The European Economic Sentiment Indicator, which measures consumer and business confidence, rose to 103.9 in April from 103.0 in March. That was a larger rise than the increase to 103.4 forecasted by Bloomberg economists, and it was the first strengthening of confidence this year. Last month, the European Central Bank (ECB) launched a fresh package of stimulus measure that boosted growth in the region.

- In his first appearance, the new governor of the Central Bank of the Republic of Turkey emphasized that curbing inflation remains the bank’s top priority, signaling continuity in monetary policy. Last week, Turkey cut its overnight lending rate from 10.5 percent to 10 percent. It was indicated that rate cut policy will continue as it long as inflation allows it. The cost of funding is coming down and if deposit rates continue to decline, the banks should benefit.

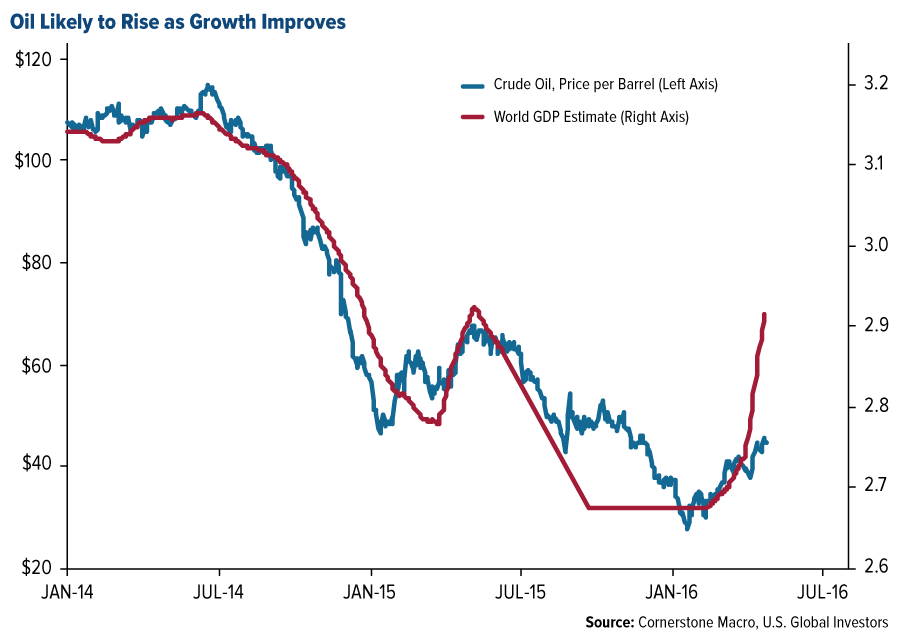

- In its oil research published on April 26, Cornerstone Macro said that oil is likely to rise as long as global growth improves. Russia will be the main beneficiary of continued increases in oil prices as half of Russia’s revenue comes from the sale of oil and gas. The chart below shows crude oil prices along with the estimated world gross domestic product data.

Threats

- Eurozone inflation is not improving. April’s preliminary inflation was reported at negative 0.2 percent on a year-over-year basis. This is below the consensus forecast of negative 0.1 percent. The eurozone’s target inflation is set at 2 percent.

- Tourist arrivals in Turkey continue to decline. Latest data show a drop of 12.8 percent year-over-year versus 10.3 percent. Turkey had another suicide bombing in Bursa near the Grand Mosque, which is one of the city’s biggest tourist attractions. Terrorist attacks and geopolitical tension could put further pressure on airline and leisure industry.

- The United Kingdom’s economy lost momentum in the first quarter. National statistics indicate the economy grew 0.4 percent in the first three months of the year after expanding 0.6 percent in the fourth quarter of last year. On an annualized basis, the economy grew at 1.6 percent, down from 2.4 percent. The UK will vote on whether to stay in the eurozone or stand alone as the world’s fifth-largest economy.

© US Global