This Election Year, It’s Not Just Trump Investors Should Worry About

Sixteen. That’s the number of Republican presidential candidates who ended their campaigns since last summer, leaving only businessman Donald J. Trump as the presumptive GOP nominee. Love him or hate him, it’s time to come to terms with the reality that Trump’s name will likely be appearing on the ballot in November.

As a money manager, I’ve always said that it’s the policies and not the party that matter. So it is with Trump. Many of his proposed policies certainly bode well for the market, including lowering taxes and scrapping needless regulations that slow business growth. Like his former rival for the GOP nomination, Ted Cruz, he has expressed support for a return to the gold standard and reportedly owns between $100,000 and $200,000 in gold bullion. In 2011, he even accepted a 32-ounce bar of gold as a deposit from a Trump Tower tenant.

However, as I told Kitco yesterday, I believe investors’ fears of a socialist Bernie Sanders presidency, not to mention negative interest rates, have driven a lot of gold’s recent momentum, more so than the idea of a Trump presidency.

At the same time, Trump has taken positions that should concern investors. Besides exhibiting a volatile temperament and leadership style, he’s been a harsh critic of free trade agreements and has made clear his opposition to the Trans-Pacific Partnership (TPP), which aims to eliminate up to 18,000 tariffs among 12 participating countries. Andy Laperriere, head of policy research at Cornerstone Macro, believes Trump’s trade agenda could even pose some risks to American multinationals, especially those dealing with Mexico and China, and the U.S. dollar.

Plus, there’s the troubling comment he made this week on CNBC, proclaiming himself “the king of debt,” before adding: “I would borrow, knowing that if the economy crashed, you could make a deal. And if the economy was good, it was good. So therefore you can’t lose.”

So What Are the Odds, Really?

|

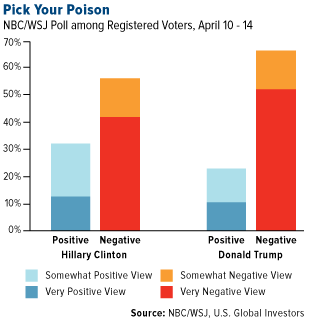

The cards are markedly stacked against Trump when it comes to winning in November. Most national polls show Hillary Clinton beating him in the general election, even though she is nearly as unfavorable to registered voters, according to an NBC/Wall Street Journal survey. Renaissance Macro Research calls Trump’s “net negatives prohibitively high.” And as I shared with you way back in August of last year, Moody’s Analytics forecasts a win for the Democratic nominee, whether that’s Clinton or someone else. Since 1980, Moody’s sophisticated election model has accurately predicted the outcome of every single contest, and in 2012 it even nailed the Electoral College vote.

Trump still has quite a lot of support in the financial industry. A Financial Advisor poll found that, as of today, a little over 50 percent of respondents say Trump will win the White House, while nearly 37 percent say Clinton. Doubleline Capital founder Jeff Gundlach also believes Trump will be the victor, arguing that in the short term, this would be positive for the U.S. economy. The New York billionaire, Gundlach points out, has promised to build up the military and initiate an infrastructure program.

Whomever voters end up electing in November, there will be winners and losers. Again, what’s important to look at are the policies because they’re precursors to change. We’ll be watching the events as they unfold closely and adjusting our allocations accordingly.

Municipal Bonds: The Solution to “Sell in May”?

We’re now in May, which is when many investors consider whether to sell or stay in the game during the summer months, thought to have some of the worst performance of the year.

While there might be evidence to support this strategy, it’s worth digging deeper before making a decision. Again, this is an election year, and today McClellan Financial reports that in the fourth year of a president’s second term—in other words, when he is ineligible for reelection and we must therefore choose a new president—the market has fallen 1.6 percent on average during the May-October period, based on data from 1936 to 2012. This is caused presumably by the uncertainty over who might replace the incumbent, and how his (or her) policies might affect the market.

McClellan also suggests that May might not be the most opportune time to get out of stocks in these years, as the market has typically bottomed mid-month, then rallied into June and July. That means it might pay to hold out until then to sell off, if that’s what you plan to do.

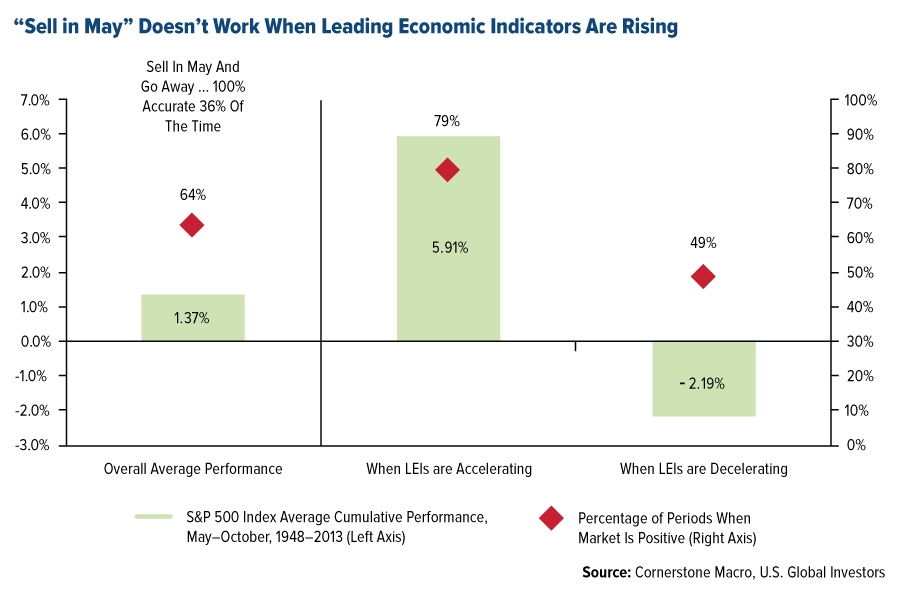

What’s more, Cornerstone Macro says that “sell in May and go away” only works when leading economic indicators are decelerating. (In such years, returns have been negative 2 percent on average.) When they’re rising, the summer months have returned an average 6 percent.

So are the leading indicators rising or lowering? Well, today the Bureau of Labor Statistics revealed that the U.S. added 160,000 jobs in April. Although this figure is positive, it represents a seven-year low and is well below the 205,000 that economists had expected.

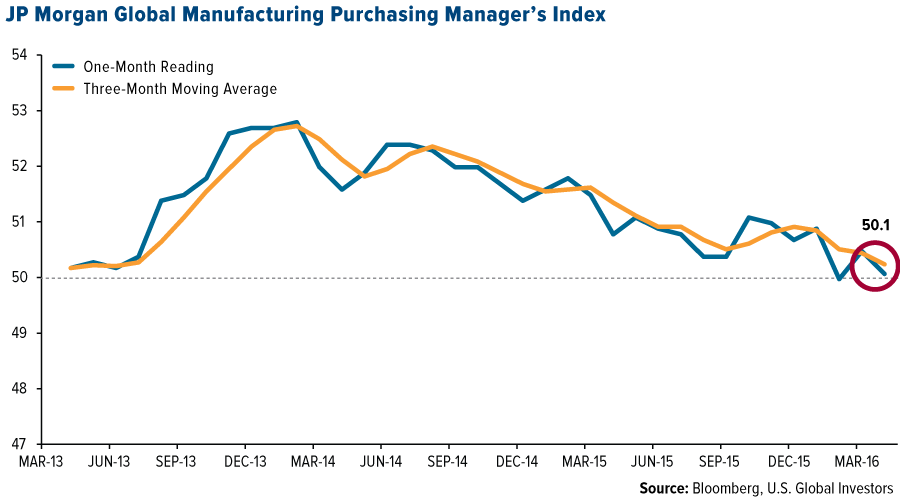

Manufacturing also shows continued signs of weakness. The April global purchasing manager’s index (PMI), which we follow closely, came in at 50.1, a reading that’s barely above the standstill threshold of 50. In addition, the U.S. manufacturing PMI fell to 50.8, its lowest level since September 2009.

There’s also the news that Chinese banks’ bad credit could actually be nine times larger than previously believed. Although not an “economic indicator,” this should give investors pause, as potential losses could reach as high as $1.1 trillion, according to brokerage firm CLSA.

So there’s a lot of overlapping analyses to consider here. Regardless of how you see it, when you take into account the additional volatility this second-term election year could yield, it might be a good time to consider diversifying into investment-grade, short-term municipal bonds. Munis have been shown to perform well over time, even during periods of market instability and rising interest rates. They’re also tax-free at the federal level and often at the state level if you happen not to live in one of the seven states that doesn’t levy a tax on income.

An old investing rule of thumb suggests that whatever your age is, that is the percentage you should have allocated toward tax-free munis. So if you’re 40 years old, 40 percent of your portfolio should be in short-term munis, 50 percent if you’re 50 years old, and so on.

The bottom line is, if you feel skeptical or fearful of the consequences of Election Day, it might behoove you to look into short-term, tax-free munis.

Follow the Money: Druckenmiller Maintains His Massive Bet on this “5,000-Year-Old Currency”

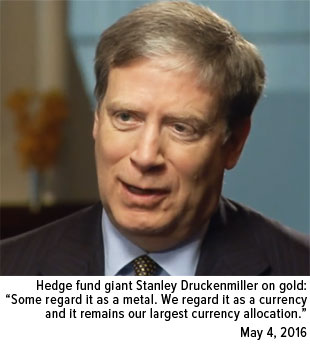

Speaking at the Sohn Investment Conference in New York this week, legendary hedge fund manager Stanley Druckenmiller warned investors that the equity bull market, propped up by “the longest period ever of excessively easy monetary policies,” is now close to exhaustion. He called negative interest rates an “absurd notion” and noted that central banks are now borrowing more “from future consumption than ever before.”

As such, Druckenmiller is wagering on gold. Heavily.

|

“Some regard it as a metal,” he said. “We regard it as a currency and it remains our largest currency allocation.”

Between 1986 and 2010, the year he closed his fund to investors, Druckenmiller consistently delivered a spectacular 30 percent on an average annual basis. That’s a superhuman feat, one that unequivocally demands we take note of his investment choices. His Duquesne Family Office fund is reportedly up 8 percent so far this year.

In August, I reported on his move to make a gold ETF his number one holding, followed by Facebook, a choice that has served him well. The yellow metal is currently up 18 percent since the beginning of August.

As always, I recommended a 10 percent weighting in gold—5 percent in gold stocks, 5 percent in bullion, coins and jewelry. Rebalance every year.

MoneyShow Next Week

Just a reminder, I will be in Las Vegas next week at the MoneyShow, where I will be speaking alongside other highly sought-after investing and trading experts, including Art Laffer, Gary Shilling, Peter Schiff and more.

Registration is absolutely free, but if you can’t make it in person, a free virtual event is also available.

I hope you’ll join me!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.19 percent. The S&P 500 Stock Index fell 0.40 percent, while the Nasdaq Composite fell 0.82 percent. The Russell 2000 small capitalization index lost 1.43 percent this week.

- The Hang Seng Composite lost 4.26 percent this week; while Taiwan was down 2.76 percent and the KOSPI fell 0.87 percent.

- The 10-year Treasury bond yield fell 5 basis points to 1.78 percent.

Domestic Equity Market

Strengths

- Consumer staples was the best performing sector for the week, increasing 1.74 percent compared to an overall decrease of 0.40 percent for the S&P 500 Index.

- Teradata was the best performing stock for the week, increasing 11.23 percent. Shares were boosted by a solid first quarter report and a change in its CEO.

- Stocks closed modestly higher on Friday, ending three days of losses, after the U.S. government's disappointing jobs report added to speculation that the Federal Reserve might keep interest rates low for another year.

Weaknesses

- Energy was the worst performing sector for the week, falling 2.95 percent compared to an overall decrease of 0.40 percent for the S&P 500.

- Endo International was the worst performing stock for the week, falling 40.11 percent. The drugmaker's stock stumbed after management slashed the company's full year annual guidance for both total revenue (cut 11 percent from its former high end estimate) and adjusted earnings per share (revised downwards 23 percent). Endo's revised outlook stems from the loss of exclusivity for the anti-inflammatory medicine Voltaren Gel, as well as increasing competition in the generic drug space.

- Unable to overcome the objections of regulators, Halliburton ended its attempt to merge with Baker Hughes. Regulators worried the deal would decrease competition in the oil services sector.

Opportunities

- REITs (real estate investment trusts) could be in a sweet spot compared to other types of financials—banks, asset managers and the like. The group is still not overvalued, despite the relentless decline in yields on competing assets. This may reflect an undercurrent of skepticism regarding the sustainability of cash flow growth and low cap rates. However, both appear sustainable. The consumer price index (CPI) for homeowner’s equivalent rent—a proxy for REIT pricing power that has a good correlation with relative performance—is still accelerating. Moreover, commercial property price inflation continues to climb.

- Utilities could continue to outperform. The incentive to maintain an overweight exposure to this fixed income proxy is heavily influenced by whether global deflationary forces have finally ebbed. While the U.S. dollar has softened in recent months, it has not caused an upsurge in inflation expectations nor has it failed to cause a selloff in Treasuries. U.S. yields are being pinned down by persistently low global bond yields, which reflect chronic deflationary pressures. As long as the total return of bonds is beating equities, utilities’ relative performance momentum should stay positive.

- According to BCA, recent data are supportive of a continuation of the uptrend in the medical equipment space. The medical equipment shipments-to-inventory ratio is trending steadily higher. Moreover, investment in medical equipment has reaccelerated, as has new health care facility construction. That bodes well for future equipment demand, and should keep factories operating at optimal rates.

Threats

- The latest upleg in steel prices had been driven by a surge in Chinese domestic steel prices. That, combined with news that the country plans to reduce steel capacity in the coming three to five years, was enough to send shorts scrambling for cover. However, it will take time for the global steel market to rebalance. The jump in Chinese steel prices has already encouraged domestic producers to re-ramp production. Persistent sluggishness in indicators of China's domestic consumption mean that steel inventories are likely to build as production picks up, which will put upward pressure on exports to the rest of the world. Fading construction growth and tightening lending standards in many developed countries suggest that increased steel supply from China will have a negative impact on steel prices because demand will be insufficient to fully absorb the increased supply. This is a significant threat to steel companies.

- If oil prices recover on a sustained basis, eventually some of the disposable income benefits enjoyed by the global consumer will start working in reverse, undermining consumer discretionary spending power at the margin.

- The recent broad market “risk on” phase has caused a rebound in the cyclicals/defensives ratio. Nonetheless, a number of macro variables have failed to confirm that this cyclical’s outperformance phase is sustainable.

The Economy and Bond Market

Strengths

- Average hourly earnings rose 2.4 percent on an annual rate for the month of April.

- The ISM non-manufacturing composite increased to 55.7 in April from 54.5 in the prior month.

- Construction spending inched up 0.3 percent month-over-month in March, adding to first-quarter growth.

Weaknesses

- The U.S. Department of Labor released an underwhelming employment report on Friday. Nonfarm payrolls rose 160,000, falling short of the 200,000 consensus. Downward revisions to the prior two months' data trimmed a further 19,000 jobs.

- J.P. Morgan's composite global manufacturing purchasing managers' index, which aggregates PMI data from around the world, registered 50.1 in April, just above the breakeven line of 50. U.S. manufacturing expanded less vigorously in April, as did manufacturing activity in China, the United Kingdom and Japan. Sluggish growth should keep central banks in lower-for-longer mode for a considerable period to come.

- Puerto Rico's Government Development Bank defaulted on $422 million in municipal bonds this week, setting the stage for a larger default on 1 July, when nearly $2 billion in general obligation bonds come due. Puerto Rico carries a total debt load of $70 billion, an amount the governor has said cannot be repaid. The U.S. Congress is considering legislation that might allow Puerto Rico to declare bankruptcy, an option that is unavailable under existing law.

Opportunities

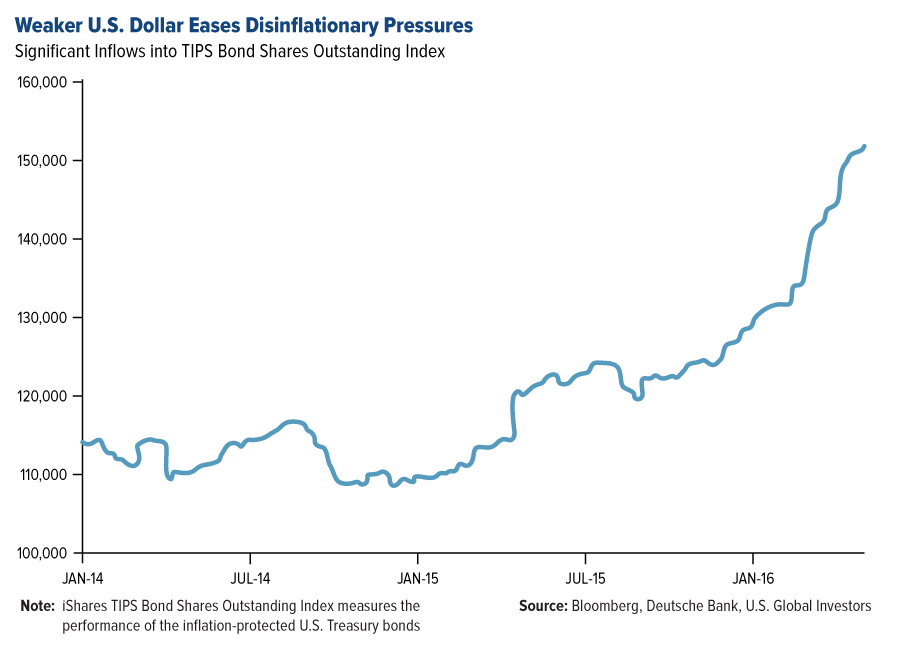

- A weakening in the U.S. dollar is easing disinflationary pressures. This has caused significant inflows into TIPS (Treasury inflation protected securities) funds.

- The NFIB (small business) survey (Tuesday) and the retail sales report (Friday) will provide some visibility on whether the weak first-quarter U.S. real GDP growth figure represented a temporary soft patch or something more enduring.

- S&P Global Ratings has upgraded more municipalities than it has lowered for 13 straight quarters, the longest streak since 2001. Just nine issuers have defaulted in 2016 apart from Puerto Rico, compared with 24 at this time last year.

Threats

- Bank of America is revising its estimates for U.S. multifamily housing starts down, lowering overall starts forecast to 1.175 million this year. Bank of America cites evidence of excess supply of luxury buildings in the top cities while construction in these markets looks set to slow. Lending standards for commercial real estate loans have also tightened, serving as a headwind for multifamily construction.

- An update of household inflation expectations from the University of Michigan survey will be published on Friday. Note that the median long-term inflation expectations from this survey have been bouncing around record low levels since October 2015.

- The European Commission reduced its 2016 GDP forecast to 1.6 percent from 1.7 percent and cut its inflation outlook to just 0.2 percent, well below the 0.5 percent February forecast. Also this week, the European Central Bank's monthly bulletin indicated that economic risks remain tilted to the downside.

Gold Market

This week spot gold closed at $1,287.90, off $5.09 per ounce, or 0.39 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, lost 2.41 percent. Junior miners outperformed seniors for the week as the S&P/TSX Venture Index traded down just 0.82 percent. The U.S. Trade-Weighted Dollar Index bounced up 0.87 percent for the week after last week’s shellacking loss.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

May-2 |

U.S. ISM Manufacturing |

51.4 |

50.8 |

51.8 |

|

May-2 |

Caxin China PMI Mfg |

49.8 |

49.4 |

49.7 |

|

May-4 |

U.S. ADP Employment Change |

196k |

156k |

194k |

|

May-4 |

U.S. Durable Goods Orders |

0.8% |

0.8% |

0.8% |

|

May-5 |

U.S. Initial Jobless Claims |

263k |

274k |

257k |

|

May-6 |

U.S. Change in Nonfarm Payrolls |

200k |

160k |

208k |

|

May-12 |

U.S. Initial Jobless Claims |

270k |

-- |

274k |

|

May-13 |

Germany CPI YoY |

-0.1% |

-- |

-0.1% |

|

May-13 |

U.S. PPI Final Demand YoY |

0.2% |

-0.1% |

Strengths

- It was somewhat of a subdued week for metal prices following the gains of the prior week. The best performing precious metal for the week was platinum, up just 0.32 percent on little impactful news.

- Gold rallied above $1,300 an ounce earlier in the week, reports Bloomberg, the first time since January 2015, on speculation that central banks in the U.S. and Europe will maintain low interest rates. Gold continued to shine even when speculators took a step back. According to Bloomberg, hedge funds missed the party, reducing their wages on a rally by the most since turning bullish in January.

- With gold prices rising the most in 15 months, demand for American Eagle gold coins have strengthened, reports Bloomberg. Sales totaled 351,000 ounces this year, which is double the 175,500 in the first four months of 2015. A similar situation at the Austrian Mint saw sales of gold bars and bullion coins up 45 percent in 2015 over the previous year’s total, reports CoinWeek.

Weaknesses

- The worst performing precious metal for the week was palladium, off 2.39 percent. Bloomberg ran a story trying to highlight that “oil isn’t the only commodity threatened by Tesla’s rise” as they zero in on the woes of platinum demand for electric cars – oops, perhaps the author meant to be talking about palladium as this is the primary platinum group metal used to treat the exhaust gases of gasoline powered cars. Platinum’s use is higher in diesel engines though.

- According to Bloomberg, India’s government has collected 2.8 tonnes by 105 depositors of gold so far under its Gold Monetization Scheme (GMS). The scheme, which has been in place for six months, is intended to mobilize idle gold held by households and institutions of India to facilitate its use for productive purposes, reports Bloomberg.

- Canaccord analysts led by Tony Lesiak wrote this week that the gold sector is reaching fair value, explaining that additional gold price strength is needed for further material performance in equities. Alamos Gold, Barrick and Kinross were cut to hold versus buy by the analysts, reports Bloomberg. In other gold company news, Newcrest announced the completion of additional hedging of a portion of Telfer’s expected fiscal year ’18 and ’19 gold sales (with further 200,000 ounces of gold sales being hedged at an average AUD gold price of A$1,773 an ounce), reports Bloomberg.

Opportunities

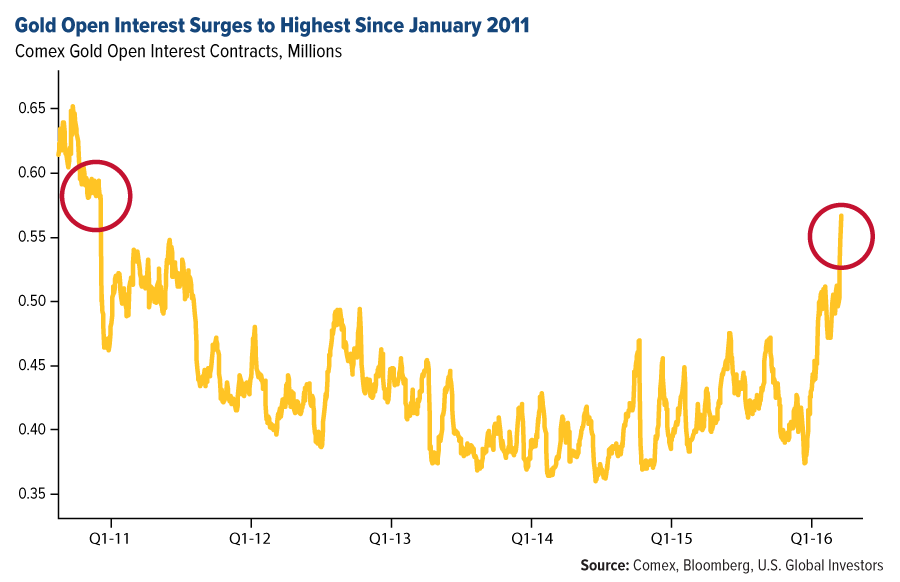

- On Tuesday, gold open interest (a tally of outstanding contracts in Comex futures) rose 3.1 percent to 565,774. This is the highest since January 2011, reports Bloomberg, and could mean the precious metal’s rally may persist. After being shunned for nearly three years, gold is making a powerful comeback.

- According to Randgold’s CEO Mark Bristow, the gold industry needs to invest in exploration, reports Bloomberg. This is indeed one of the best ways to create value in the long run. It is true however, that many companies have cut exploration budgets and may scramble to buy smaller companies. Speaking of exploration, Scotiabank reported on Klondex Mines this week, noting the company’s exploration results from its Fire Creek mine in Nevada (where the latest drilling extended the Karen, Joyce and Hui Wu veins along strike by up to 430 feet as well as down dip by up to 125 feet). “We note that a two-year extension in the mine lives of both Fire Creek and Midas would boost our NAV estimate,” continues the research note. Brian Morris, Vice President Exploration Klondex, notes that the drill results support our belief that Fire Creek is a much larger system than we know today.

- Billionaire investor Stan Druckenmiller is loading up on gold, reports Bloomberg. At the Sohn Investment Conference in New York on Wednesday, he said the bull market in stocks has “exhausted itself” due to excessive borrowing from the future, adding that gold is his largest currency allocation. “We refer to gold as a currency, not a metal,” Druckenmiller said. Hedge fund manager David Einhorn agrees that gold is poised to generate profits, reports Bloomberg, citing increasingly aggressive monetary policies for his view on gold prices.

Threats

- Rising gold prices could smother Indian gold demand for a festival next week and weddings this month, reports Bloomberg. The world’s second-biggest user of the precious metal has seen a surge in local prices to the highest in two years, deterring normal seasonal buying patterns.

- In a report from ICBC Standard Bank this week, the group notes: “Signals that the gold rally has gone too far, too quickly increased in number and intensity at the start of this week.” The report cites options, contract contango, U.S. dollar reversals, and a subdued Indian market. In fact, gold fell for a third day on Wednesday as the dollar rebounded on the possibility of a U.S. interest-rate increase in June, reports Bloomberg.

- As we know, China recently introduced a new yuan priced gold fix. Within a week of the new fix being introduced however, Russia and China announced a new gold trading platform, reports Sputnik News. In a recent interview with Austrian Economist Sandeep Jaitly, Double Down asks him to explain the purpose of the fix and what the gold moves by Russia and China could tell us about the current fiat money system. Sandeep noted that with the demise of the London Gold Fix, which used to be set in pounds sterling and moved to only the dollar fix after World War II, has opened the door for the Chinese to be the price setter of physical gold. Also, Sandeep explained that the gold fix price historically was for setting the price of a fiat currency relative to gold not the other way around as it commonly thought of today. The trading platform the Chinese and Russians have adopted may eventually be a mechanism to set prices for goods or services in terms of gold and to break the dollar’s place as the currency of international trade.

Energy and Natural Resources Market

Strengths

- Gold jumped on Friday as the weak jobs print pushed expectations for the next Fed hike to 2017. Bloomberg data shows odds that the Fed will raise rates next month dropped to 4 percent, from 10 percent on Thursday and 75 percent at the beginning of the year. Low borrowing costs are a boon to gold because it doesn’t offer yields or dividends.

- The best performing sector for the week was the S&P 500 Construction Materials Index. The index rose 4 percent propelled by a leap in shares of Vulcan Materials Co. which reported first-quarter earnings that beat analysts’ expectations. The company also raised its full-year guidance which provided a good read-through for the entire sector.

- Rayonier Advanced Materials, a junior specialty chemicals company, rose 42 percent for the week after first-quarter earnings beat analysts’ estimates. The company announced the results of its successful cost-cutting measures, which came ahead of expectations and allowed the company to upgrade its full year guidance.

Weaknesses

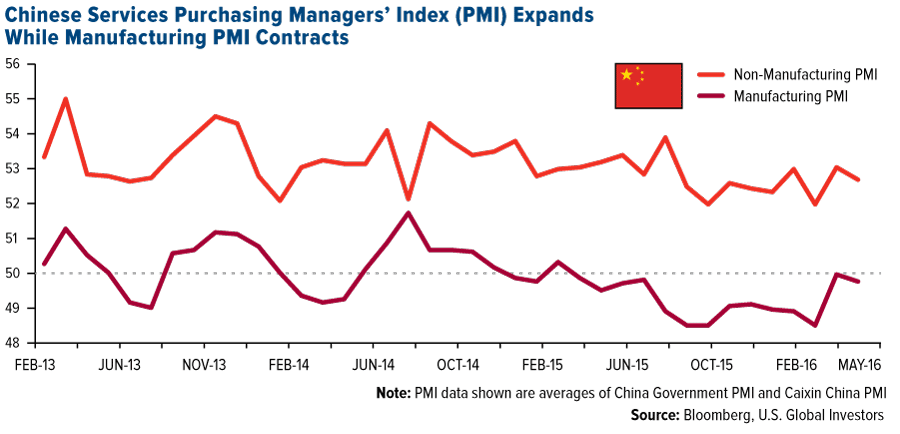

- China’s Caixin April manufacturing PMI dropped to 49.4 vs. 49.7 in March, suggesting manufacturing activity declined further in April. The reading has been in contractionary territory for 14 consecutive months, which suggests that the flurry of rate cuts and monetary easing has been unable to bolster the overall economic sentiment.

- The worst performing sector for the week was the S&P/TSX Diversified Metals and Mining Index. The index of base metals producers dropped 12 percent for the week, tracking a 5 percent drop in copper prices, the worst weekly decline in the metal since early January.

- The worst performing stock for the week in the S&P Global Natural Resources Index was Freeport-McMoRan Inc. The miner dropped 16 percent as global growth cues softened with weak PMI data coming out of China, resulting in weaker metals prices and lesser risk appetite among investors.

Opportunities

- “Sell in May and go away” may not prove a successful strategy in 2016 according to Cornerstone Macro research. The firm’s analysis suggests that the summer period can actually have positive returns when leading economic indicators (LEIs) are rising. As the chart below illustrates, the “Sell in May” discipline yields an average 5.9 percent gain when LEIs are rising, compared to a 2.2 percent average loss when LEIs are deteriorating. If LEIs can maintain the momentum of the seasonally strong March/April period, we may well have an excellent summer for stocks.

- China may hold the answer to the global oil supply glut. An article by consultant Rakesh Upadhyay shows that China has stockpiled a striking 787,000 barrels a day of crude in the first quarter of 2016—the highest stockpiling rate since 2014. In Rakesh’s opinion, it is difficult to conclude that China is calling a bottom in crude prices, however, their purchases do put a floor beneath the current lows, because in all likelihood, China will resume its record buying and top up its Strategic Petroleum Reserves if prices tank.

- The fire in Fort McMurray, home to Canada’s oil sands, is now estimated to knock up to 1 million barrels per day of crude out of global markets. OilPrice.com reports that while infrastructure is yet to be damaged, the evacuation of staff in combination with the precautionary closure of pipelines is what is driving the drop in production. The continued incidence of unplanned supply outages may continue to support a recover in energy stocks.

Threats

- Bloomberg columnist Javier Blas argues that the oil market is still pricing the “lower-for-longer” mantra, despite the 50 percent-plus rally from the year’s lows. Despite strong moves in the front month contacts, the five-year-forward WTI contract has fallen 2.6 percent this year, thus significantly flattening the curve. Although forward oil prices aren’t a predictor, they often signal an anchor for the long term, says Blas.

- Goldman Sachs’ U.S. oil production tracker is falling behind, suggesting U.S. companies aren’t curtailing production quickly enough to help rebalance global markets this year. Based on companies’ reports last week, Goldman has narrowed its 2016 production decline expectations to 665 thousand barrels per day (kbpd) from 725 kbpd. The report concludes by stating that narrower U.S. declines have been temporarily offset by outages elsewhere, but the pace of declines will need to increase for the market to rebalance in the second half of 2016.

- Iron ore prices could continue to tumble after this week’s 12 percent decline. BMO reports that a survey of 163 steel companies in China predicts that blast furnace operating rates will decline to 80 percent by the end of May, from 89 percent currently. This expected decline is driven by anticipated maintenance across many mills and the recent softening of steel prices over the past week.

China Region

Strengths

- The Nikkei Indonesia Manufacturing Purchasing Manager’s Index (PMI) ticked up for the April period to 50.9 from 50.6.

- Aside from the frontier market Vietnam—which rose nearly 1.4 percent for the week—the top-performing regional equity index was Indonesia’s Jakarta Composite, which fell only 0.11 percent for the holiday-shortened week. Indonesia was closed on Thursday and Friday.

- The Nikkei South Korea Manufacturing PMI came in at 50.0, up from its last print of 49.5.

Weaknesses

- Both the official China Manufacturing PMI and the Caixin China Manufacturing PMI missed analysts’ expectations, coming in respectively at 50.1—barely expansionary—and 49.4—signaling contraction—versus expectations for 50.3 and 49.8.

- The Malaysian ringgit fell more than 2 percent this week, following energy prices lower. Malaysia is the region’s only net energy-exporting country. The South Korean won also declined heavily this week, as both imports and exports missed.

- The Nikkei Malaysia PMI for April tumbled to 47.1 from its prior reading of 48.4, marking a full year that the Malaysian PMI readings have been in contraction territory.

Opportunities

- The Philippines will hold presidential elections this weekend, which should bring some resolution to recent election jitters. Rodrigo Duterte, the tough-talking populist mayor of Davao City, maintains his lead in the polls with roughly 30 percent support, even as outgoing President Benigno Aquino is calling for Duterte’s competitors to unite to defeat him. Final polling shows Mayor Duterte with roughly 33 percent support, followed by Senator Grace Poe, with 22 percent, and Mar Roxas, the former Interior Secretary endorsed by President Aquino, with only 20 percent support. For better or worse, the election’s outcome will diminish the recent political uncertainty in the country.

- Recent currency volatility has made Hong Kong a much more affordable destination for Chinese mainland tourists, as the Hong Kong dollar—pegged to the U.S. dollar, which has been weaker of late and which the yuan has closely followed—is now “cheaper” relative to a number of other regional currencies, particularly the Japanese yen and the Malaysian ringgit. Chinese mainland visitors to Hong Kong for the May Day holiday rose 14 percent year-over-year, which may prove to be a boon for Hong Kong retailers.

- This weekend, China releases more data for the April period, including trade balance and import/export numbers, in addition to FX reserve levels. Investors will watch closely for further signs of stabilization.

Threats

- The Chinese government is considering taking board seats and stakes of at least 1 percent in operators of internet portals as well as mobile apps, Bloomberg News reports. The stakes and board seats will come in exchange for the granting of news licenses, and will allow the Chinese government to monitor and block content distributed by internet providers.

- According to the Wall Street Journal, Chinese authorities have reportedly advised a number of economic commentators to avoid making “overly bearish” statements about the economy.

- Non-performing loans (NPLs) in China continue to grab investor attention, and several research institutions have now called attention to the subject. CLSA strategist Francis Cheung suggests that NPLs in China may be running more like 15-19 percent of outstanding credit, far higher than the official 1.67 percent.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 3.76 percent.

- Ukrainian hryvnia was the best relative performing currency this week, losing 22 basis points against the dollar. The International Monetary Fund (IMF) will visit Ukraine next week to evaluate ongoing reforms and to determine whether to release a delayed payment of $1.7 billion.

- The health care sector was the best performing sector among Eastern European markets this week.

Weaknesses

- Turkey was the worst performing market this week, losing 8.16 percent. Political tension between President Erdogan and Prime Minister Ruling Ahmet Davutoglu has been rising. The AKP party announced an extraordinary Grand Congress meeting on May 22 to elect a new chairman, who will also serve as next Prime Minister of Turkey heading a new cabinet.

- The Turkish lira was the worst performing currency this week, losing 4.49 percent against the dollar. Political tension between President Erdogan and Prime Minister Davutoglu cased a selloff in the Turkish equities and lira.

- The industrial sector was the worst performing sector among Eastern European markets this week.

Opportunities

- According to Berenberg Bank Emerging Europe research team, Romania will be the fastest-growing European economy over the next two years and among the top 20 in emerging Europe, offering the highest dividend yield in the world. Retail sales grew 17 percent year-over-year in 2016, the fastest in the Emerging European universe. Romania has robust underlying fundamentals and recent tax cuts boosted consumption. The country is now rated investment-grade at all of the major credit rating agencies. The MSCI and FTSE could upgrade Romania in the coming years from a frontier market to an emerging market.

- Data compiled by the United Nations refugee agency shows that the number of refugees arriving in Europe is declining on year-over-year basis. The reversal comes after the March 18 European Union deal under which so-called irregular migrants who enter the EU in Greece are sent back to Turkey.

- Eurozone Investor Confidence and Industrial Production will be released next week and Bloomberg’s analysts predict stronger readings.

Threats

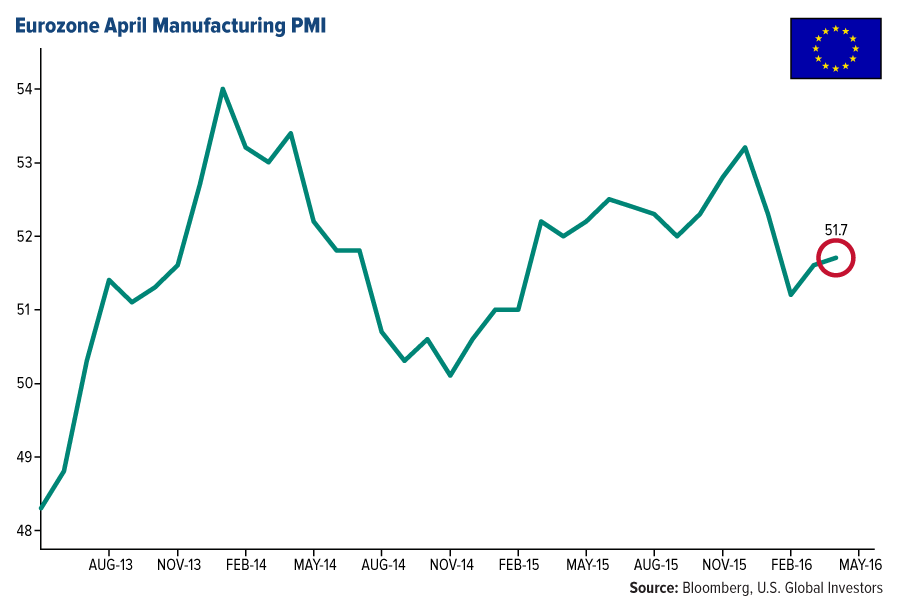

- Eurozone April manufacturing PMI was reported marginally higher at 51.7, up from 51.6, but still well below the 20-month high of 53.2 in December.

- Many investors know a phrase “Sell in May and Go Away” as the summer months have been associated with some of the worst episodes for the market. The MSCI Emerging Market Europe Index has gained 35 percent since the January 21 low and we could see some profit taking in May.

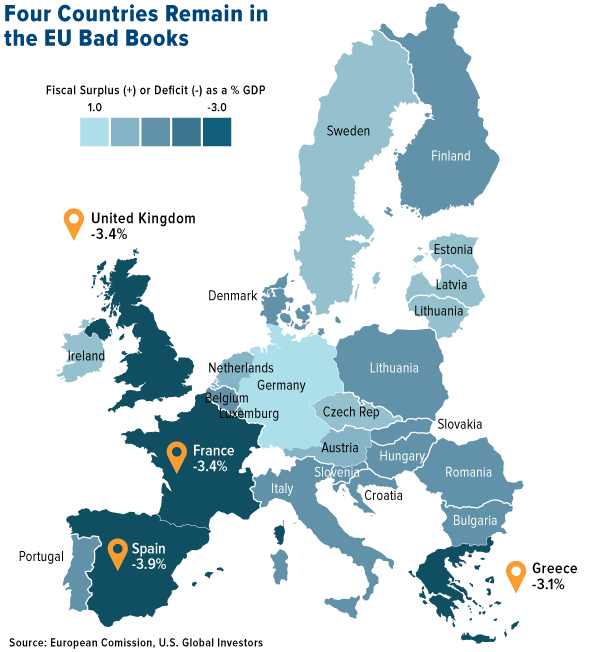

- The European Commission published a budget deficit forecast for 2016 and Spain, France, Greece and UK will breach the EU deficit limit of 3 percent in 2016. Poland and Romania will post deficits next year of 3.1 percent and 3.4 percent, respectively.

© US Global Investors

ww.usfunds.com