Why U.S. Business Investment Is Evolving, Not Fading

ACapex 2016, where are you?

Investors wonder what it means when they see headlines declaring that businesses just aren’t spending like they used to. These days, investment spending on capital—capital expenditures, or capex—appears to have taken a backseat to cash hoarding and stock buybacks.

But capex isn’t dead. Investment spending by U.S. businesses is actually on an upward trend; you just need to know where to look.

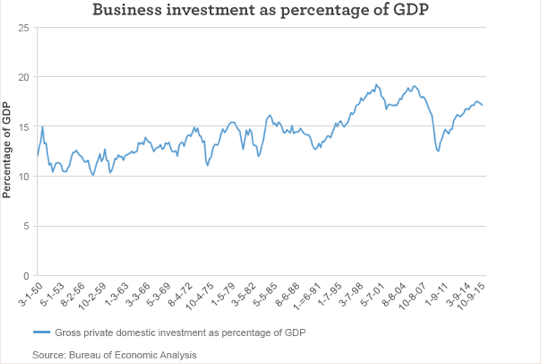

Is capex really that bad? It’s all relative (to GDP).

As you’ll see, investment spending overall actually doesn’t look that bad relative to gross domestic product (GDP). Why is relative to GDP such an important qualifier? Economic data often needs to be looked at on a relative basis. For example, a slow economy may be responsible for slow business spending. Or perhaps the two factors feed on each other, with low business spending not fostering faster economic growth.

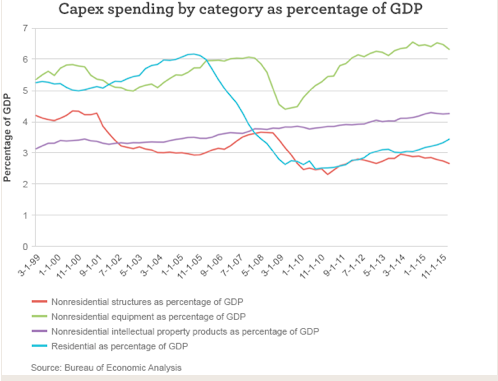

The following chart breaks down how different types of business investment—from nonresidential structures (new offices, plants, facilities) to nonresidential equipment (machinery, telecommunications, data processing technology)—contribute to U.S. growth.

The productive capacity of the economy, at least in terms of equipment and intellectual property that companies tend to invest in, has surpassed pre-financial-crisis levels, at least relative to GDP. However, corporate investments in structures—mainly buildings but also things like energy pipelines—are still low relative to GDP.

Why are businesses sitting on cash instead of spending on capital? Businesses could be hoarding cash and buying back shares because they lack confidence in their demand outlook. However, sitting on cash might not be all bad.

It’s all about weighing expected relative returns and risks. If a business can’t reinvest for growth, it may as well distribute money to shareholders instead. High cash balances may not be bad if you consider our convoluted tax code may be encouraging firms to invest abroad. While they have a lot of cash, a lot of that might be outside the U.S., unavailable for distribution or spending in the U.S. without a big tax hit.

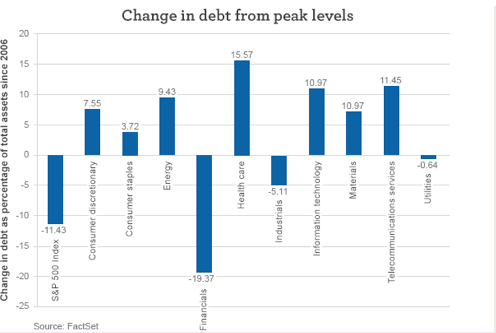

There’s been a perception that companies have been deleveraging, or shedding debt. But that view is skewed by one sector: financial firms lowering their leverage. As you’ll see below, almost every other U.S. sector has been releveraging rather than deleveraging.

Companies’ unwillingness, or inability, to take on debt—at least for large publicly traded companies—hasn’t restrained their spending on capital. Most of the decline, especially with publicly traded companies, is due to the energy boom and bust. Companies in the oil, gas, and consumable fuels industry represent a full 22% of capital expenditures for publicly traded companies overall. Yet, their expenditures are down more than 31% from their peak. At the peak, energy companies represented 32% of U.S. capital expenditures for businesses.

When it comes to capex, the energy sector has left a big hole to fill, and no other single sector is large enough to fill that hole. The second-closest industry would be electric utilities, which represent just over 8% of capital expenditures. Instead, the gap will likely need to be filled by many other industries making many other—perhaps small—contributions.

Look to service-sector businesses for future investment and innovation. I think U.S. services industries are ripe for improvements in investment spending. You can already see it with the proliferation of web-enabled tools that allow businesses to handle tasks more efficiently. This includes day-to-day tasks such as appointment scheduling. This new generation of services also allows for, and demands, more efficient inventory management and flexible manufacturing. Plenty of today’s service providers are augmenting their delivery of service with technology.

One example that is near and dear to my heart is in the field of education (being an educator of 16 years exposes you to a lot of the industry’s ins and outs). Education was thought to be the classic case of where productivity growth went to die. A teacher could only effectively teach a certain number of students. Now, with massive open online courses (MOOCs) and computer-aided lessons and grading, teaching can enjoy some improvements to economies of scale.

The future depends on investment, but not all business investment has to take its classic form. Investment spending is actually on an upward trend. And when you think of the future, don’t just think of information technology or how to make machines run faster or with less waste.

Instead, think of innovation in its classic definition: the act or process of introducing new ideas, devices, or methods. Every company will need to continuously adapt to survive. There are cool and innovative things happening in every industry, from companies that invest in overhauling age-old logistics and shipping processes to companies that spend on revamping their product portfolios to get ahead of shifting consumer tastes and preferences.

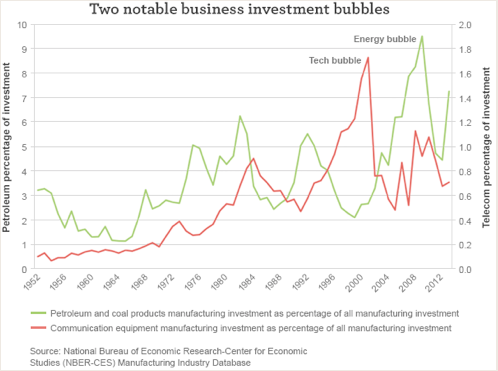

I believe the slowdown in capex spending among U.S. businesses is due to how companies are adjusting to the booms and busts that have beset the economy. It took a while for technology companies to make up the ground they lost in the bursting of the tech bubble. It took—and is still taking—time to adjust to the bursting of the housing bubble. The bursting of the energy bubble will also leave its mark. But the economy will adapt.

Innovations may happen more sporadically than continuously in the service sector compared with innovations in the manufacturing and mining sectors. Predictions of low returns for investors may be due more to a lack of imagination on the part of those making the forecasts than an actual lack of opportunities.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 5-3-16 and are those of Dr. Brian Jacobsen, CFA, CFP®, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management