While the U.S. economy has grown at a modest/moderate pace since the end of the Great Recession, one area that has lagged a bit is consumer spending. Consumers took a tremendous hit during the downturn, creating challenges for an economy so dependent on consumer spending. Based on recent consumer and other economic data, however, I believe consumer spending is poised to pick up. While a recovering consumer could benefit the economy as a whole, specific industries and sectors could outperform.

The pain of the Great Recession has taken time to overcome.

For U.S. consumers, the Great Recession didn’t affect just their finances; it took a heavy psychological toll as well. Many people who had felt confident about their financial situations before the financial crisis were shocked to find themselves suddenly dealing with severe financial hardship—including negative net worth—as the values of their homes and stock-market holdings plunged while their debts remained constant or rose. This extreme turn of events was a complete surprise for many Americans because the housing market had been enjoying a long, strong run, and homeowners had come to expect rising home values year after year.

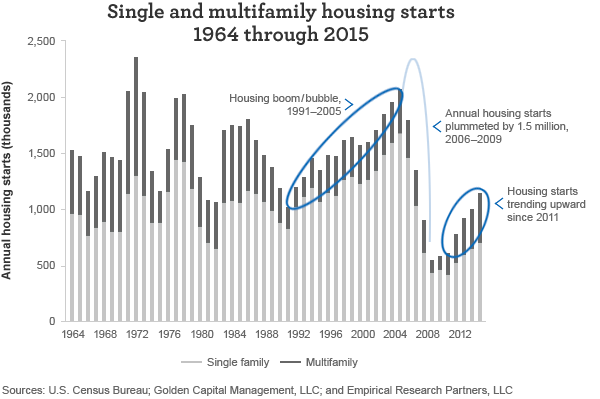

Annual single and multifamily housing starts—perhaps the single most important and most easily measurable indicator of housing-market health—show how dramatically the financial crisis pummeled the U.S. housing market and homeowners. From the early 1990s to the mid-2000s, housing starts grew at a nice, steady pace from about one million per year to nearly two million. But that housing boom turned into a housing bubble as housing starts plunged in the midst of the financial crisis, hitting a bottom of only about half a million starts per year in 2009 and 2010.

As the housing market collapsed, home values also fell, wiping out trillions of dollars of homeowners’ equity.

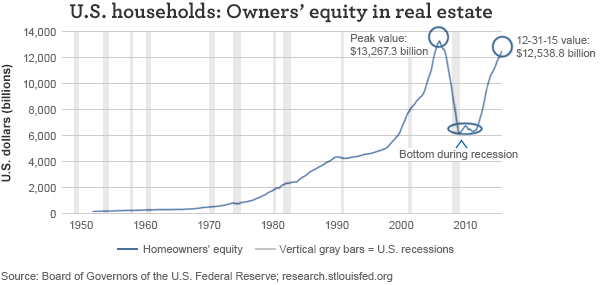

During the Great Recession, U.S. homeowners’ equity plunged more than 50% from its peak reached in the first quarter of 2006. As a result, many homeowners ended up owing more on their homes than the homes were worth. The sustained downturn in the U.S. stock market over the same period further exacerbated consumers’ financial situations. It’s no wonder that consumers emerged very cautiously from the financial crisis—seeking to rebuild their savings, regain confidence, and spend more carefully—and that their caution continued for an extended length of time.

Consumer spending could move higher.

The good news is that this long period of cautious consumers could soon end. A range of economic data support a positive turn for consumer spending. In particular, housing starts and homeowners’ equity have improved significantly since the recession. Looking back at Chart 1, we see a string of annual increases in new-home starts beginning in 2012, reaching a high of 1.1 million in 2015—nearly 11% above the 2014 level. Housing starts are driven by builders’ expected demand for new homes; the rising number of starts reflects an increasing rate of household formation, which means more and more people have begun establishing their own residences. Chart 2 shows that homeowners’ equity has risen steadily since the recession ended, enabling homeowners to regain much of the equity that disappeared from their balance sheets during the recession. Also, the U.S. stock market has recovered and moved beyond its prerecession high, providing consumers with the opportunity to recoup investment losses incurred during the recession. The job market has expanded steadily over the past few years as well. All of these factors combined have helped many consumers regain financial health, which in turn has boosted consumer confidence to a level that has been holding steady near its all-time high. In my view, the improved household balance sheet, the health of the consumer, and the expansionary effects of the housing recovery should provide a fundamental underpinning to the U.S. economy for some time, benefiting both consumers and businesses.

As consumer spending picks up, consumer discretionary and information technology (IT) companies could especially benefit.

With the consumer in a steadily improving financial position, I expect to see acceleration in spending on housing, autos, electronics, and apparel. Within the consumer discretionary sector, I favor investments in home-improvement companies over homebuilders, especially in a transitional environment where household spending is starting to improve. I like the fact that home-improvement stores can make sales to people no matter whether they are selling/buying a home or simply improving their existing home with no intention to move. In contrast, homebuilders are limited to benefiting only when people feel financially prepared to buy.

Although I think strength in apparel should continue, I am wary of the disruptive impact on retailers’ business model due to increased online shopping and purchases. Within the IT sector, the types of companies I think will benefit most as spending picks up are those involved in software development, cloud computing, and internet services as well as companies focused on providing higher electronic content within traditionally manual devices and appliances.

As you invest, I urge you to keep this general rule of thumb in mind: Look for innovative companies capable of adapting their business mix as market conditions change over time. This flexibility can provide opportunities to generate sufficient revenue through weak periods and robust growth through periods of expansion.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 5-10-16 and are those of Jeff Moser, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management