Here's Why Earnings Could Be the Key to This Market

Question: “How many folksingers does it take to change a light bulb?”

Answer: “Five. One to change the light bulb and four to sing about how good the old one was.”

At the risk of sounding like one of those folksingers, I have to say that the factors that I think drive American stock prices up or down have slipped in the past three years. Those factors are not in negative territory, but the zing is gone and it takes a bit more of an effort to arrive at an exclusively bullish conclusion.

I believe that three factors drive the stock market: the Federal Reserve (Fed), the earnings, and the valuation. There is no formula for success, but watching these things can give you a pretty good feel for the lay of the land. In early 2013, all of them were saying “buy.” The Fed had recently embarked on a program of massive stimulus known as quantitative easing. Earnings expectations (as I read them) were rising, and the market’s forward price/earnings ratio was well below its 20-year average (it was around 13X). If you kept your eyes on the instruments, they were saying to “buy”.

Now, it’s not so easy.

The market is trading between 16X and 17X forward earnings. That is roughly in line with the average of the past 20 years and what I would call fairly valued. The good news is that it is not expensive; the bad news is that it’s not cheap anymore.

I believe that the Fed still wishes to encourage (not discourage) economic growth. In my opinion, that means that it will be pushing money toward the economy (through the capital markets) for the next year or so. Again, it’s not bad, but it’s not the cavalry charge we are seeing from the European Central Bank and did see from Dr. Bernanke three years ago. I think that the Fed’s stance keeps a floor under stocks but doesn’t push them higher.

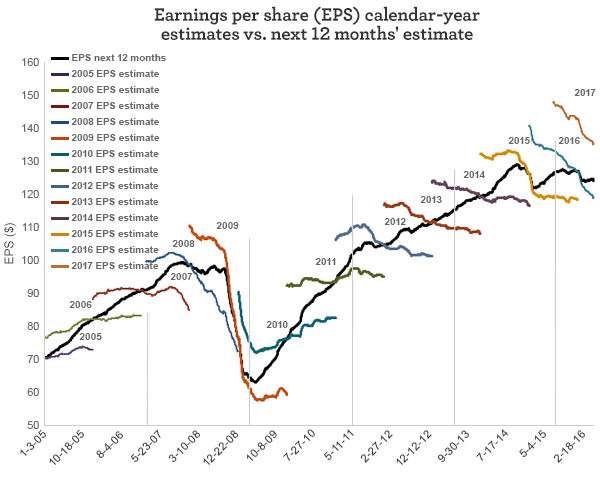

In (and at) the end, it’s earnings. Earnings expectations were rising in 2013, but they have been flat to down in the past two years. Again, it’s not bad, but it is worse than it was. I think that earnings will rise in the second half of this year, but I thought that last year as well. I think that earnings have to rise for the stock market to do the same. In 2013, the earnings card was on the table; today, we’re still waiting for the draw.

I guess that I am part of the general frustration. Why won’t stocks go up or down? Which will they do first? I still think that a resurgent consumer will push the economy and earnings higher later this year. I still think that we will get the euphoria that has usually marked the latter stages of bull markets in the past 50 years. I just wish that it would be easier to get there.

Source: FactSet

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 5-16-16 and are those of John Manley, CFA, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management