“Old age doesn’t come alone.” Scottish Proverb

The health care sector of the equity market covers a lot of ground. Constituent groups run the gamut from insurers to device makers to pharmaceuticals to biotech. It is a pretty diverse sector, but most of the groups have something in common: They have lagged a mediocre domestic market in the past year. For some of the groups with higher multiples, the underperformance has been sharp; for others, slight.

One part of the problem was valuation. Historically, high growth, high multiple areas have had fits when investors get a touch of acrophobia. However, these episodes were generally temporary if fundamentals remained intact. Multiples contract because of lower prices or higher earnings. My recollection is that, in many cases, the latter replaces the former and the stocks recover.

I think that the fundamentals (ignoring, for a moment, politics) of the health care industry remain intact. I see a confluence of three powerful forces here: improving demographics as the Baby Boomers enter their seniority and probably need more help in staying alive and healthy; improved technology as the industry turns the pure scientific advancements in DNA analysis and manipulation of 10 years ago into real-world saleable products; and, finally, government programs to inject money into the process. In other words, there is the need for help, there is the ability to help, and there is someone with very deep pockets to pay for it.

Health care creates its own customers

It appears to be a wonderful business model. People quite literally can’t live without health care. The longer people live, the more potential for further treatments as they age further and encounter life’s inevitable frailties. Health care is selling the one product that’s the premise for all other products: longer and healthier lifespans.

The problem is that someone has to pay for it. That’s where the politics come in. We all want the benefits, but no one wants to foot the bill. With the federal elections six months before us, I suspect that the fear of possible price controls or other health care rationing will continue to affect potential investors. However, this perception likely will be temporary and, ultimately, a buying opportunity.

Regulation is one thing; rationing is quite another. Stringent controls likely will be hard to implement on an industry with new products and a strong presence in Washington. I think health care will be a bigger part of our economy and that the added costs will be born somewhere. Staying alive is very high on most peoples’ lists of things to do. The health care industry strives to do exactly that.

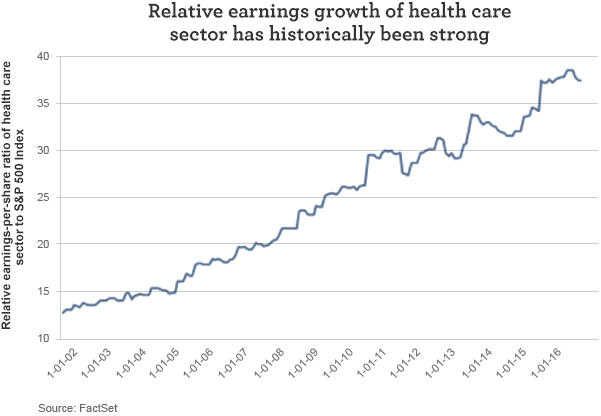

I have included three graphs to make a few additional points. The relative earnings growth of the sector has been quite strong over the past 25 years. It has been more of a step-like progression recently, but, given the demographics and the technology, I don’t see this deteriorating now.

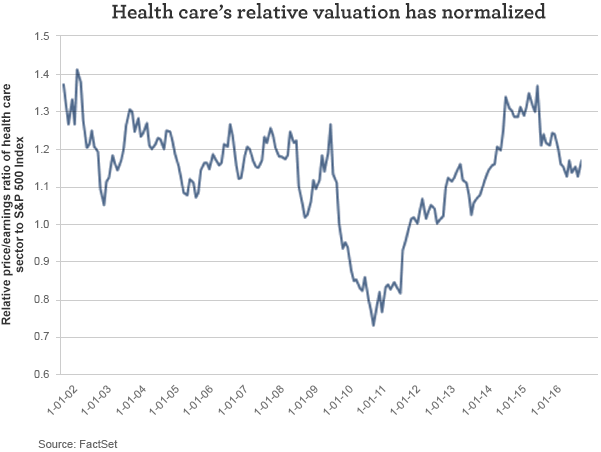

Also, the concerns I mentioned above already have affected the area’s relative valuation. Health care’s relative price/earnings ratio has returned from a rather steep 35% premium to a more normal 15% premium.

The relative price/sales is back to a market level. To me, that’s not cheap, but, given the potential, it’s not bad either.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 5-9-16 and are those of John Manley, CFA, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management