This week, President Barack Obama was in Vietnam and Japan drumming up additional support for the Trans-Pacific Partnership (TPP), and meanwhile I was in the U.K., where Brexit drama is dominating headlines and airwaves. Only a month remains before voters decide whether the country will stay in or leave the European Union. As I said last week, an exit could trigger a currency crisis with both the euro and pound, in which case owning gold might be a good idea.

Speaking of the yellow metal, I had the opportunity to meet with the World Gold Council (WGC) while I was in London. It’s a pleasure to share with you that the group’s CEO, Aram Shishmanian, has agreed to join me as a special guest during our next webcast, scheduled for Wednesday, June 8. We’ll be discussing gold, specifically the reasons behind its rally this year and the pullback we’re seeing this month. I highly urge you to register for the webcast because you won’t want to miss Aram’s rich insights into gold.

As Oil Hits $50 a Barrel, Americans Hit the Road

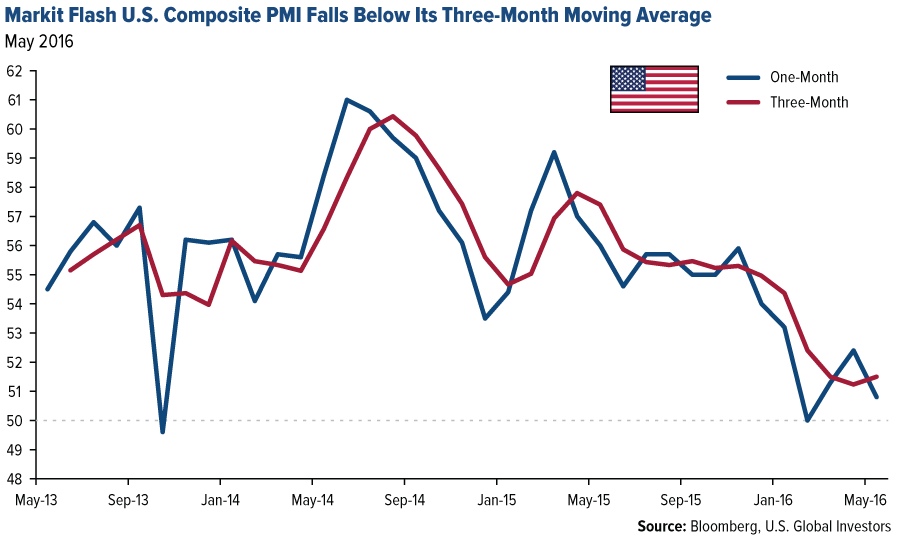

I was disappointed to see that U.S. manufacturing activity showed more signs of slowing growth, according to preliminary purchasing managers’ index (PMI) data. The PMI posted a 50.8, just above the neutral 50.0 threshold separating expansion and deterioration. What’s more, the index fell below its three-month moving average, which we’ve found to be a headwind for commodities and energy three to six months out.

This could threaten additional recovery in the oil and gas industry. For the first time this year, West Texas Intermediate crude briefly touched $50 a barrel yesterday. Prices between $50 and $60 are widely seen as a “goldilocks” scenario: high enough for oil companies to stay profitable yet low enough for consumers.

Gas prices, in fact, are expected to be the lowest in 10 years this Memorial Day weekend, according to the American Automobile Association (AAA). The motor club estimates prices will average around $2.26 a gallon, or 45 cents less than last year. More than 38 million Americans will travel this weekend, AAA says, the second-highest volume on record. If you’re one of them, I wish you happy, safe travels! But however you plan on spending the weekend, remember to honor those who bravely served the U.S. and gave the ultimate sacrifice.

The U.S. Can Now Export Weapons to Vietnam

On Monday, Obama lifted the 40-year-old weapons embargo against Vietnam, ending what many see as the last vestige of the U.S. and Southeast Asian country’s former animosity. It was also part of his administration’s “pivot” to Asia to deepen relations with countries in the fastest growing region of the world.

Indeed, Vietnam is in an exciting position right now. In the fourth quarter of 2015, its gross domestic product (GDP) growth rate expanded an impressive 7.01 percent, and Goldman Sachs predicts its economy will become the 17th largest by 2025, up from 55th today. The most populous city, Ho Chi Minh City, commonly known as Saigon, has blossomed into one of the world’s premier manufacturing and tech startup hubs, with huge investments flowing in from companies such as Samsung and Intel.

Vietnam’s defense spending has also been growing rapidly in recent years, and today a lot of business is up for grabs. Between 2011 and 2015, the country was the world’s eighth largest arms importer, just one rung above the U.S., according to the Stockholm International Peace Research Institute (SIPRI). This year it’s expected to spend $5 billion, a dramatic increase from the estimated $1 billion it spent in 2005.

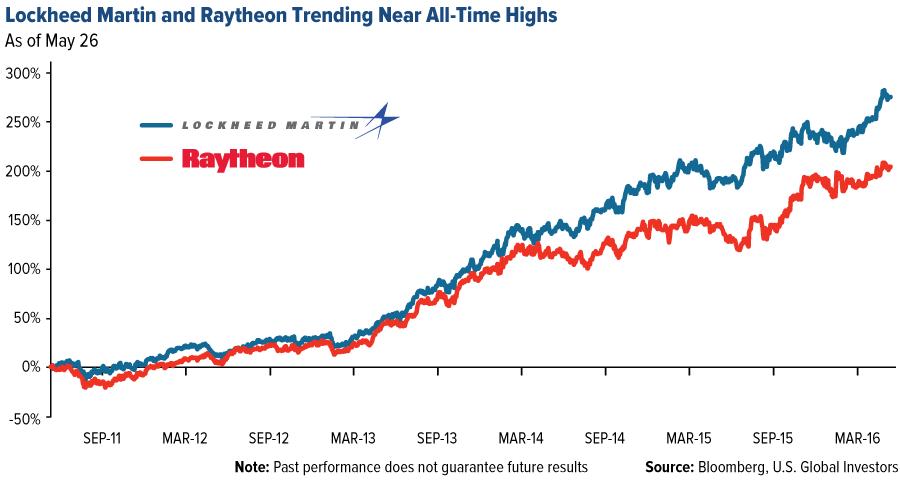

With the embargo out of the way, American aerospace and defense contractors such as Lockheed Martin and Raytheon have the opportunity to move into this new Asian market. Boosted by recent geopolitical fears and terrorist activity, both companies are trending near their all-time highs.

They also provide attractive dividends, which are increasingly sought-after in a world that’s seen a third of all government bond yields around the world turn negative.

Selling the TPP

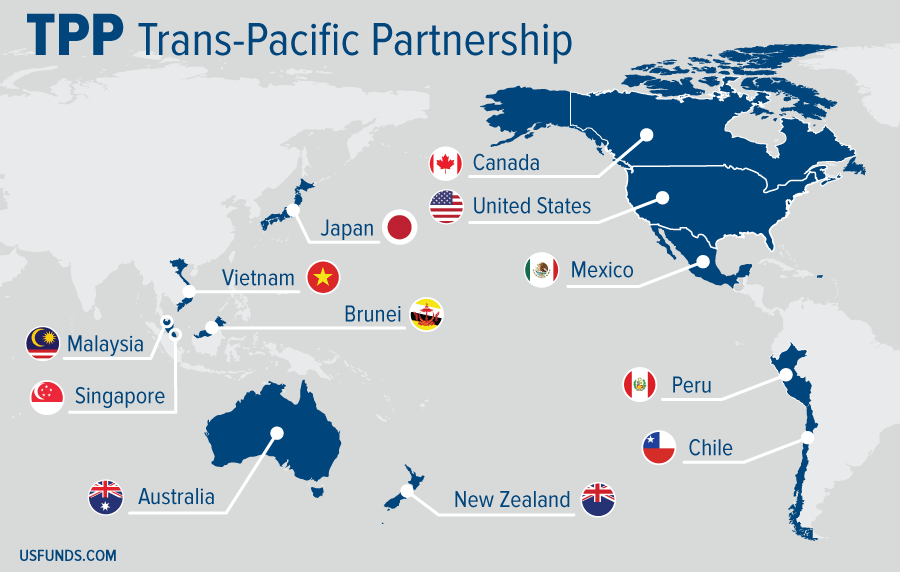

One of Obama’s main objectives in visiting Vietnam and Japan was to shore up support for the TPP, the historic trade agreement that, if ratified by all 12 participating countries, is designed to eliminate as many as 18,000 tariffs. Sixteen to 30 years after ratification, 99 percent of all goods trade among these countries will be entirely liberalized.

In the map below, you can see the massive scale of who’s involved. TPP countries have a combined GDP of $28 trillion, close to 40 percent of world GDP, and they account for almost a quarter of total world exports.

Vietnam has the most to gain from the TPP Eliminating thousands of tariffs should allow its important apparel and textile industry to export even more goods to the U.S. In turn, the U.S. would have the opportunity to sell more vehicles in the Asian country. The World Bank estimates a 10 percent bump in Vietnam’s economy over a decade as a result of the deal.

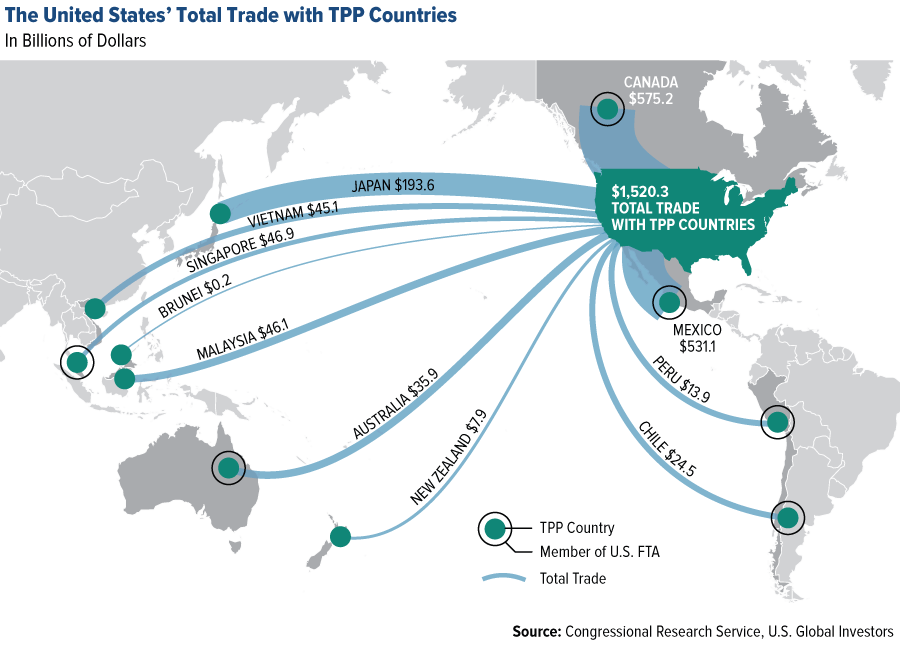

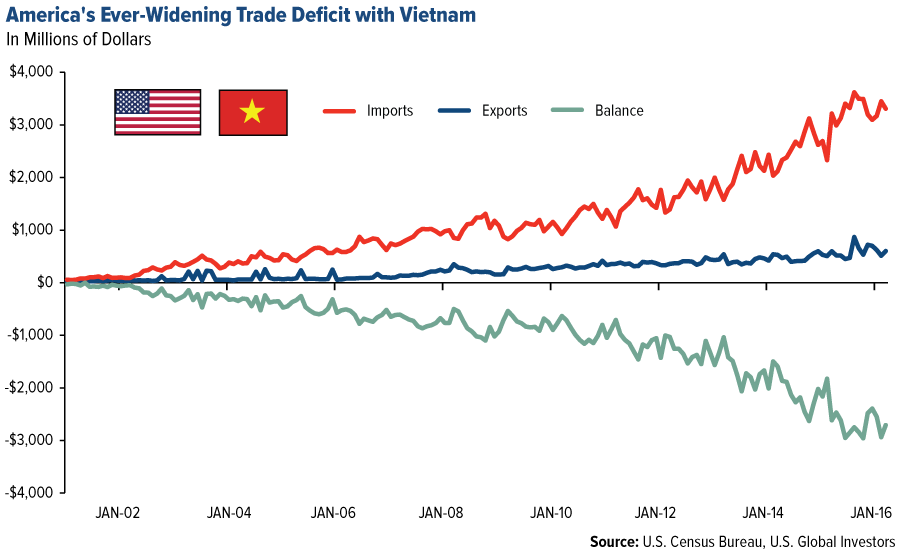

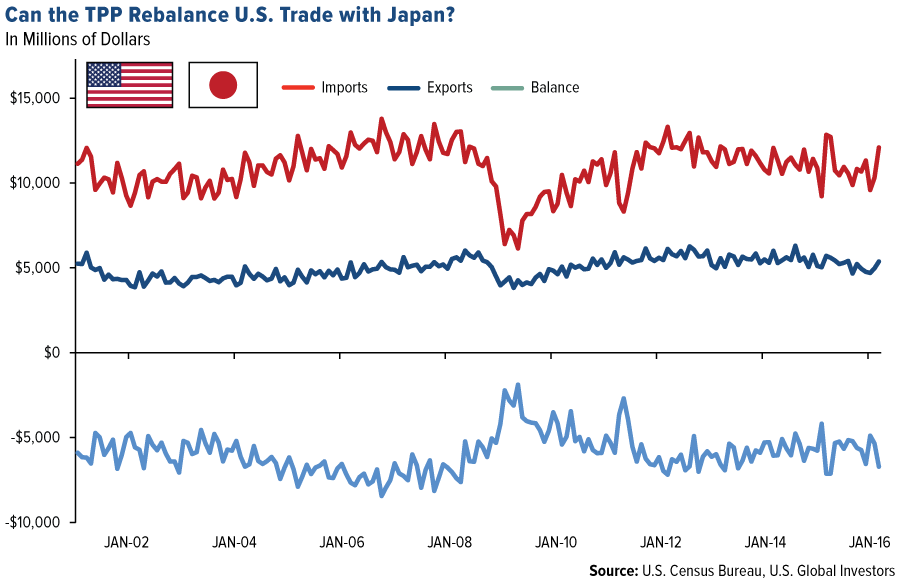

Among the TPP countries, the U.S. runs the largest trade deficit, which widened to $57.5 billion in April. As you can see, the U.S. has an unfavorable (and worsening) trade gap with Vietnam (-$2.7 billion in March) and Japan (-$6.7 billion). The TPP could help rebalance this.

According to the Peterson Institute for International Economics (PIIE), the TPP “will increase annual real incomes in the United States by $131 billion, or 0.5 percent of GDP, and annual exports by $357 billion, or 9.1 percent of exports, by 2030.” For all member nations, the deal is expected to add $492 billion in real income.

Challenges Ahead

Of course, none of this will come to pass if the TPP can’t be ratified. The PIIE warns that delaying the TPP’s launch by even a year could lead to a permanent opportunity loss of between $77 billion and $123 billion for the U.S. Obama has repeatedly said he wants to see it passed by the end of 2016.

Unfortunately, a delay at this point appears highly possible, with both major U.S. presidential candidates opposing it. Support in Congress is muted. Of the 12 TPP countries, only Malaysia has ratified it.

But there’s still strong support for the deal. The U.S. Conference of Mayors, responding to recent positive findings by the International Trade Commission, wrote an open letter asserting its support, stating that passage of the TPP is critical for the U.S. to remain a leader in the global marketplace.

I agree. The deal is far from perfect, but it’s what we need now to help reignite global growth.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.13 percent. The S&P 500 Stock Index rose 2.27 percent, while the Nasdaq Composite climbed 3.44 percent. The Russell 2000 small capitalization index gained 3.43 percent this week.

- The Hang Seng Composite gained 3.13 percent this week; while Taiwan was up 4.09 percent and the KOSPI rose 1.10 percent.

- The 10-year Treasury bond yield rose 1 basis point to 1.85 percent.

Domestic Equity Market

Strengths

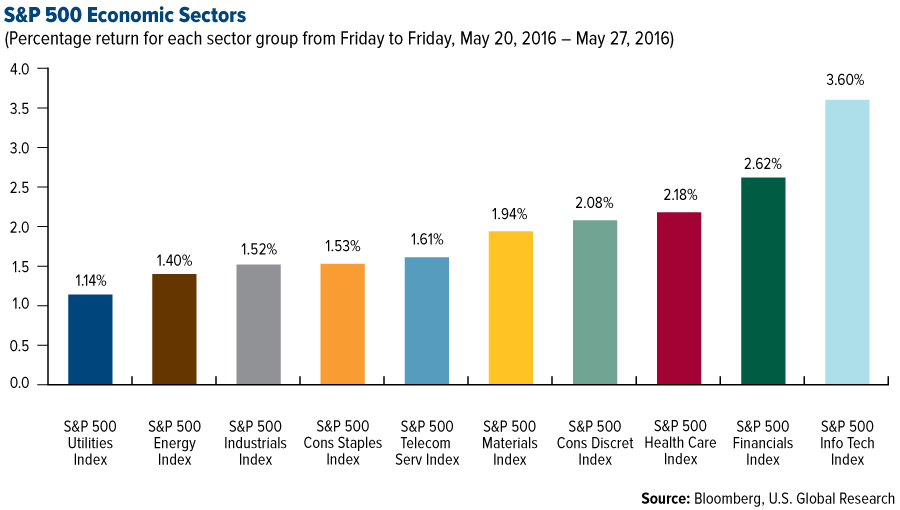

- Information technology was the best performing sector for the week, increasing 3.60 percent compared to an overall increase of 2.28 percent for the S&P 500 Index.

- Dollar Tree was the best performing stock for the week, increasing 15.67 percent. The discount retailer reported stronger-than-expected fiscal first quarter 2016 earnings. Quarterly revenue grew 133.6 percent year-over-year to $5.09 billion, primarily thanks to a $2.7 billion increase included in sales from Family Dollar, which Dollar Tree acquired last year. Meanwhile, same-store sales rose a modest 2.3 percent at constant currencies, driven by increases in both customer transactions and average ticket size.

- Hewlett-Packard Enterprise, a company spun off of HP some months ago, is spinning off its enterprise services business to Computer Sciences Corporation in an all-stock deal. The new company will be worth roughly $9 billion.

Weaknesses

- Utilities was the worst performing sector for the week, increasing 1.14 percent compared to an overall increase of 2.28 percent for the S&P 500.

- Signet Jewelers was the worst performing stock for the week, falling 7.11 percent. Shares slumped following the company's first quarter earnings report. Results were mixed, with the company beating estimates for earnings. However, it missed estimates for revenue.

- Agrichemical giant Monsanto this week rejected a $62 billion takeover bid from Germany's Bayer, but it kept the door open for an agreement should the bid be sweetened, saying it is open to continued and constructive conversations.

Opportunities

- The Obama administration this week tossed out a decades-old ban on weapons sales to Vietnam, potentially opening up a significant new market to American arms makers.

- The housing market remains a bright spot within the U.S. economy, which is not yet fully reflected in relative share performance.

- The recent supply disruptions in Canada and Nigeria could continue to underpin oil prices, possibly causing a short-term rally in oil stocks.

Threats

- While stocks have breathed a sigh of relief following earnings season. cracks are spreading beneath the surface. Market breadth is thinning and sentiment is also poor. Moreover, mergers and acquisitions (M&A) activity is cooling rapidly and recent news has been dominated by deal breakups instead of deal making.

- According to BCA, packaged food sales growth is contracting and return on equity (ROE) has deteriorated on the back of this revenue contraction. This is causing a divergence from the relative valuation expansion. Typically, a sustained multiple increase can only occur within the context of a rising ROE, given the latter’s direct impact on profit growth. As such, packaged food companies could be due for a pullback.

- The industrial sector share price ratio is now near the top end of a 15-year range, suggesting major resistance. Furthermore, BCA highlights that this year’s rally has been based on portfolio repositioning and reversion from oversold conditions rather than expectations of a sustainable earnings recovery.

The Economy and Bond Market

Strengths

- The U.S. economy grew slightly faster in the first quarter, revised data showed on Friday. Economic output advanced at a still-sluggish 0.8 percent annual rate, according to the U.S. Bureau of Economic Analysis. Growth in the second quarter looks to be a bit more robust, with growth estimates running around 2.5 percent.

- The European Union reached a Greek debt deal. Greece will avoid another debt crisis with upwards of 10 billion euros in financial aid from the eurozone. The money will be disbursed in time for Greece to make its next round of debt payments, which comes due in July. The deal was reached between eurozone finance ministers and the International Monetary Fund. It includes limited debt relief for Greece—but not until 2018, after elections in some of the eurozone's largest member states.

- Preliminary durable goods orders for April were reported at 3.4 percent, much higher than the expected 0.5 percent and previous reading of 0.8 percent. Also, sales of newly constructed homes surged 16.6 percent in April, reflecting strong demand from homebuyers and a healthy economy.

Weaknesses

- The preliminary Markit U.S. Manufacturing PMI for May was reported at 50.5, below the expected 51. The Services PMI also came in lower at 51.2, below the expected 53.

- The University of Michigan Sentiment Index for May came in at 94.7, below the expected 95.4.

- Japan’s sluggish economy has forced Prime Minister Shinzo Abe to forgo the consumption tax hike planned for April.

Opportunities

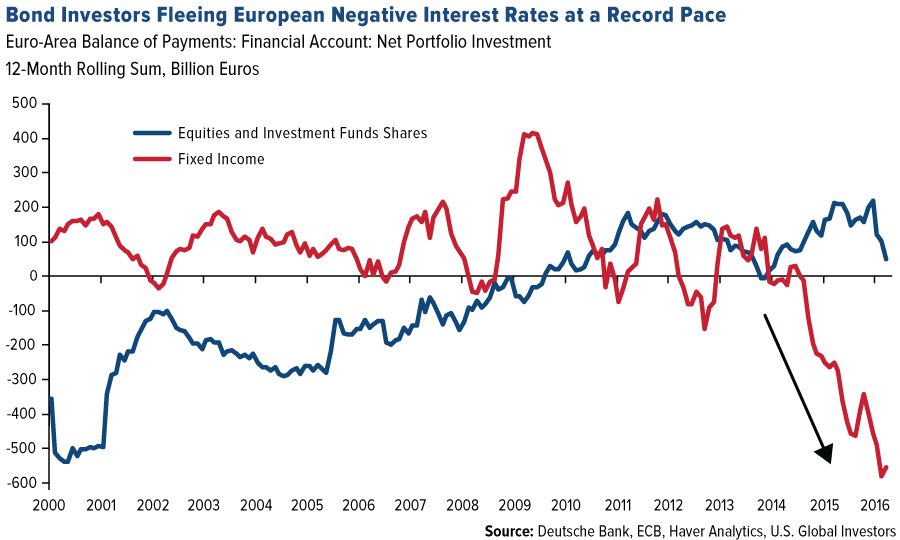

- European investors continue to flee negative interest rates at a record pace. This inflow is likely to continue putting downward pressure on U.S. interest rates.

- G7 leaders vowed to boost global growth. The leaders of the seven leading industrial nations said they will use all of the policy tools at their disposal to boost demand and reduce supply constraints. World growth is moderate and running below potential, and the risk of persistently slow growth remains, the leaders said in a communiqué. While vowing to avoid competitive currency devaluations, the leaders warned against wild exchange rate moves. This part of the statement was seen as a compromise between the United States and Japan, given the recent strength of the yen.

- Next Friday's U.S. nonfarm payrolls report will be one of the most important data releases ahead of the June 14/15 Federal Open Market Committee (FOMC) meeting. Payrolls growth near the three-month average of 200,000 would certainly increase the odds of a rate hike next month.

Threats

- J.P. Morgan estimates its Global Composite Purchasing Managers' Index (PMI) will decline to 51 in May when all the component parts are released. With the PMI at that level, the firm suggests that global growth would slow to just 1.8 percent.

- Important for the Fed's decision will be the April personal consumption deflator (PCD), due on Tuesday. Core PCD inflation currently stands at 1.6 percent, below the 2 percent target.

- Additional key information on the U.S. economy will come from the manufacturing and nonmanufacturing ISM surveys scheduled for Wednesday and Friday, respectively. This week's Markit PMIs surprised on the downside.

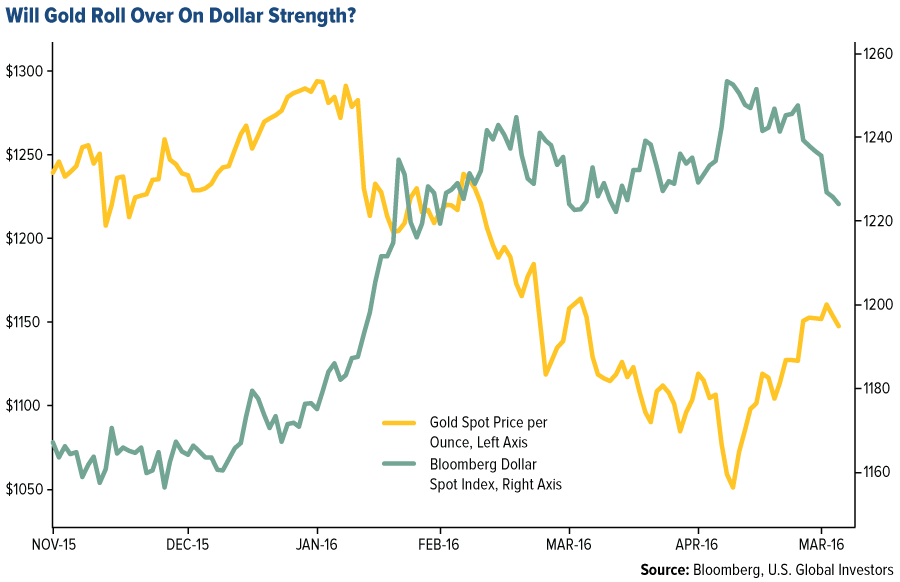

Gold Market

This week spot gold closed at $1,212.95, off $39.20 per ounce, or 3.13 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, lost 6.82 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index traded down 8.59 percent. The U.S. Trade-Weighted Dollar Index remained in recovery mode with a 0.45 percent gain for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

May-24 |

Germany ZEW Survey Current Situation |

49.0 |

53.1 |

47.7 |

|

May-24 |

Germany ZEW Survey Expectations |

12.0 |

6.4 |

11.2 |

|

May-24 |

U.S. New Home Sales |

520k |

619k |

511k |

|

May-26 |

Hong Kong Exports YoY |

-7.1% |

-2.3% |

-7.0% |

|

May-26 |

U.S. Initial Jobless Claims |

275k |

268k |

278k |

|

May-26 |

U.S. Durable Goods Orders |

0.3% |

3.4% |

1.3% |

|

May-27 |

U.S. GDP Annualized QoQ |

0.9% |

0.8% |

0.5% |

|

May-30 |

Germany CPI YoY |

0.1% |

-- |

-0.1% |

|

May-31 |

Eurozone CPI Core YoY |

0.8% |

-- |

0.7% |

|

May-31 |

U.S. Consumer Confidence Index |

96.0k |

-- |

94.2 |

|

May-31 |

Caixin China PMI Mfg |

49.2 |

-- |

49.4 |

|

Jun-1 |

U.S. ISM Manufacturing |

50.5 |

-- |

50.8 |

|

Jun-2 |

ECB Main Refinancing Rate |

0.000% |

-- |

0.000% |

|

Jun-2 |

U.S. ADP Employment Change |

178k |

-- |

156k |

|

Jun-2 |

U.S. Initial Jobless Claims |

-- |

-- |

268k |

|

Jun-3 |

U.S. Change in Nonfarm Payrolls |

160k |

-- |

160k |

|

Jun-3 |

U.S. Durable Goods Orders |

-- |

-- |

3.4% |

Strengths

- The best performing precious metal this week was silver, down 1.82 percent.

- According to data from the Commerce Department on Thursday, orders for U.S. capital goods declined unexpectedly in April for a third straight month, reports Bloomberg. With American manufacturers continuing to pull back, this could indicate a lesser chance for the Federal Reserve to raise rates in June.

- This week the World Gold Council reported that in the first quarter of 2016 global demand for gold was 1,290 tons – the highest ever for a first quarter – as investors seek safe haven investments in a time of economic fragility and uncertainty caused by negative interest rates, reports China Daily. The article continues by pointing out that buying U.S. Treasuries or other sovereign debt from Western countries has also become a “less attractive option for central banks because of their low yields.”

- The global manufacturing purchasing managers’ index (PMI) is on track to decline in May, reports Cornerstone Macro. The research group believes this is a likely outcome given declines in the May Japanese and eurozone manufacturing PMIs, as well as a probable decline in the U.S. manufacturing PMI. Cornerstone points out a handful of important global tailwinds in its report including low interest rates and healthy U.S. growth, but says there are even more headwinds that include a China slowdown, excess emerging market debt and a Brexit risk, to name a few

Weaknesses

- The worst performing precious metal for the week was platinum, down 4.40 percent.

- Gold traders are bearish for a second week – the first successive week since mid-April – as bets increase on an interest rate move from the Fed, reports Bloomberg. The Fed Funds futures show the odds of a rate increase by July seen at 52 percent, up from 48 percent at the end of last week.

- Following a pause in the dollar’s rally this week, Bloomberg reports that gold snapped six days of losses, rebounding from the lowest level in seven weeks. The article continues, stating that gold is still headed for the biggest monthly drop since November on speculation the U.S. Federal Reserve will increase U.S. borrowing costs as early as next month, denting demand for bullion.

- As Venezuela’s economic crisis deepens and the government faces concerns that it could struggle to honor bond payments, the country held the biggest gold sale by a central bank in eight years, reports Bloomberg. According to data from the International Monetary Fund, Venezuela cut its gold reserves by 16 percent in the first quarter, following a 24 percent reduction in 2015.

Opportunities

- The Fed may be bluffing on a rate hike, according to Mark Matthews, Head of Investment Research at Julius Baer Group. In an interview with the Economic Times, Matthews discusses the Fed’s history of contradicting itself, most recently on its stance back in February and March. “I think they did not like the fact that the market was not pricing in any rate hikes this year,” Matthews said. “They wanted to have some implicit threat of a rate hike in the market and they have largely achieved that now.”

- Analysts at RBC Economics have come out stating that despite the “surprisingly hawkish” minutes from the Fed, raising rates in June is “nearly impossible.” In a report released Tuesday by RBC, the group stated “We think a lot of things have to align in order for the Fed to justify a lift at the July confab. September is still complicated by Money Market reform, and November falls right on top of the U.S. presidential election.”

- Deutsche Bank, in a recent note, says that by preparing markets for future interest rate hikes, the Federal Reserve potentially hampers its ability to actually carry out those hikes in the future, reports Business Insider. The article continues by stating, that said in another way, “The Fed appears stuck in a negative feedback loop wherein suggestions that higher rates are coming create the unsettled conditions that ultimately force the Fed to keep rates right where they are.

Threats

- UBS believes that gold is set to “roll over,” reports Bloomberg, forecasting bullion to drop back to $1,150 an ounce. The yellow metal could tumble as the U.S. dollar “erodes demand with the Federal Reserve opting for not one, but two rate increases before the year-end,” according to UBS Group AG’s wealth-management unit. Not everyone sees a retreat in gold however. Citigroup raised its year-end target by $100 to $1,250 an ounce, reports Bloomberg.

- In an interview with CNBC this week, Dennis Gartman cautioned investors on when he believes they should come off the sidelines for gold. He says the time to be bullish on gold is not until after the first interest rate hike of the year. Assuming that a rate increase will happen in 2016, he thinks investors should avoid the precious metal in the near term, as he expects an active market to remain after the central bank acts, reports CNBC.

- Retailers in Hong Kong are forecast to see the worst downturn in gold sales in at least 15 years, reports Bloomberg. Fewer mainland shoppers are spending less money on jewelry, the article continues, and China’s economic slowdown and anti-corruption campaigns have hurt luxury retailers in Hong Kong with visits by Chinese tourists.

Energy and Natural Resources Market

Strengths

- U.S. new-home sales grew at the fastest pace in eight years. Purchases jumped 16.6 percent from the previous month, the fastest recorded rise since January 2008. The news should support the recent outperformance of construction materials stocks and lumber prices.

- The best performing sector for the week was the S&P 500 Fertilizers & Agricultural Chemicals Index. Monsanto Co., the largest weighting in the index, received an official takeover offer from Bayer AG, leading to a rally in Monsanto shares, as well as its peers.

- Monsanto Co., the leading U.S. producer of fertilizer and agricultural chemicals, rose 8 percent for the week after German-fertilizer Bayer AG made an official bid to take over the company.

Weaknesses

- Commodities failed the May test again. VTB Capital reports that the London base metals index has given back more than 50 percent of its January-April rally, pressured by a stronger U.S. dollar, with copper prices having fallen around 8 percent. Meanwhile, Shanghai steel futures and Dalian iron ore futures have fallen about 30 percent from their highs in late April, having relinquished almost 65 percent of their gains since early December. Oil has been surprisingly resilient, mainly due to unplanned supply disruptions.

- The worst performing sector for the week was the NYSE Arca Gold Miners Index. The index dropped 6 percent for the week, led lower by weaker gold prices. Gold prices are headed for the biggest monthly drop since November as expectations for a Fed rate increased, supporting an overdue rebound in the U.S. dollar.

- The worst performing stock for the week in the S&P Global Natural Resources Index was Petrobras SA. The Brazilian major oil producer dropped 9 percent after a convoluted week in which the company raised $6.75 billion in fresh debt, followed by a change in leadership to replace the former CEO who was close to impeached Brazilian President Dilma Rousseff.

Opportunities

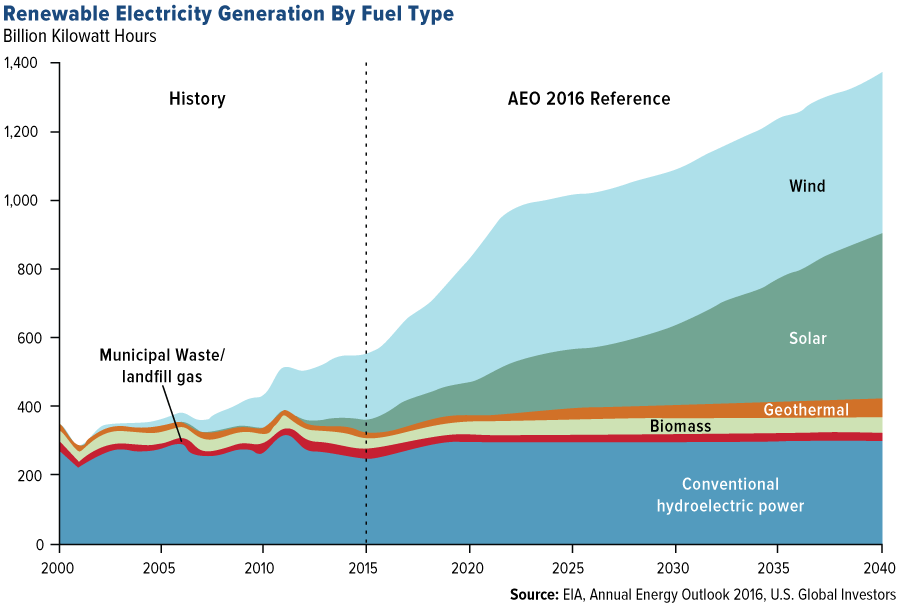

- Copper’s future demand growth catalyst may come from renewable energy given the high intensity use of the metal for conductivity. By 2040, the share of global electricity generated from renewable energy sources, including solar and wind, will double to 46 percent, Bloomberg New Energy Finance estimates. Similarly, the Energy Information Administration (EIA), forecasts a roughly fourfold increase in U.S. solar and wind power generation over the next 25 years.

- Gold’s recent check back is an opportunity to “buy the dip” according to UBS strategist Joni Teves. Recent data points suggesting the Fed may raise rates as U.S. macro data improves have weighed on gold. However, many market participants have expressed their interest to buy a dip in gold, given the underweight allocation across most of the generalist space.

- Unplanned supply outages continue to support an early rebalancing for the oil market. Earlier this week, a militant attack took Chevron’s Escravos terminal in Nigeria entirely offline, further affecting export volumes out of the African country. Just last week, Italian major integrated energy company Eni declared force majeure following an attack on one of its pipelines in the country. Nigerian production has plunged by 40 percent to 1.4 million barrels, the lowest level in decades.

Threats

- The U.S. dollar is looking cheap and may rally from here according to Deutsche Bank, the latest bank to turn positive on the “greenback,” a move that is likely to stem the momentum in commodities. According to the bank’s analysts, the recent correction in the dollar (-8.1 percent) was one of the largest and longest in recent times. However, many of the factors that led to the precipitous decline have now reversed, with rising expectations for a Fed rate hike, leading researchers at the bank to conclude that we have “likely seen the low in the dollar this year.”

- The People’s Bank of China (PBoC) warned this week that M2 Money Supply growth in China is likely to slow down in coming months. The bank argued that there is sufficient liquidity in the banking sector to maintain the current trajectory. However, analysts have noted that China has become more vocal in trying to stem the high levels of speculation that drove a rally in commodities in the first quarter, with major U.S. research firms now forecasting a painful unwinding of those excesses in the second half of the year.

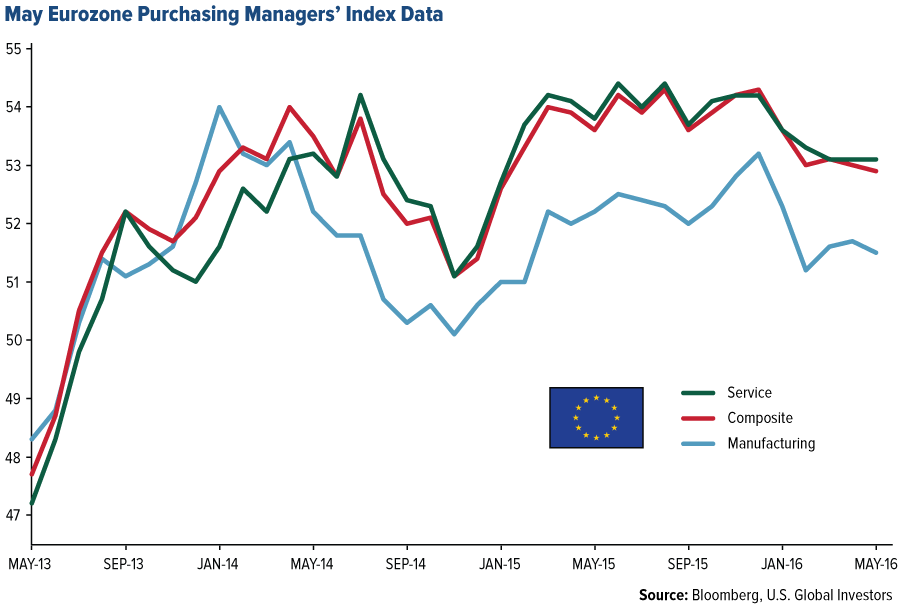

- Flash PMIs for May show further slippage from the year’s highs in the first quarter. The eurozone composite PMI fell to a 16-month low, albeit still in expansion at 52.9, the reading suggests that economic growth in the 19-country block is slowing, with a negative read-through for second-quarter GDP. Similarly, Japan’s flash manufacturing PMI reading dropped to 47.6, the lowest since 2012, as factory output and exports slumped.

China Region

Strengths

- Shenzhen-based technology giant Tencent Holdings soared to new record highs on Friday, rising 4.5 percent as investors are said to speculate that a rumored Hong Kong-Shenzhen stock connect program will increase demand for the stock. Tencent also recently reported its earnings, which came in better than expected.

- The Hang Seng Composite had a strong showing for the week, rising 3.19 percent.

- The Korean won, Indian rupee and Taiwanese dollar all turned in strong relative performances for the week.

Weaknesses

- Singapore’s first quarter GDP came in at 1.8 percent year-over-year, in line with the previous two quarters but nonetheless slightly worse than expectations for a first quarter GDP growth rate of 1.9 percent.

- Both import and export data in Thailand missed analysts’ expectations this week, with year-over-year imports falling 14.92 percent, worse than an expected decline of 7.65 percent. Exports fell 8 percent, worse than an anticipated drop of only 1.50 percent.

- The Shanghai Composite Index was the weakest performer in the region this week, falling just slightly over the last five trading days despite a week of mostly global rallies.

Opportunities

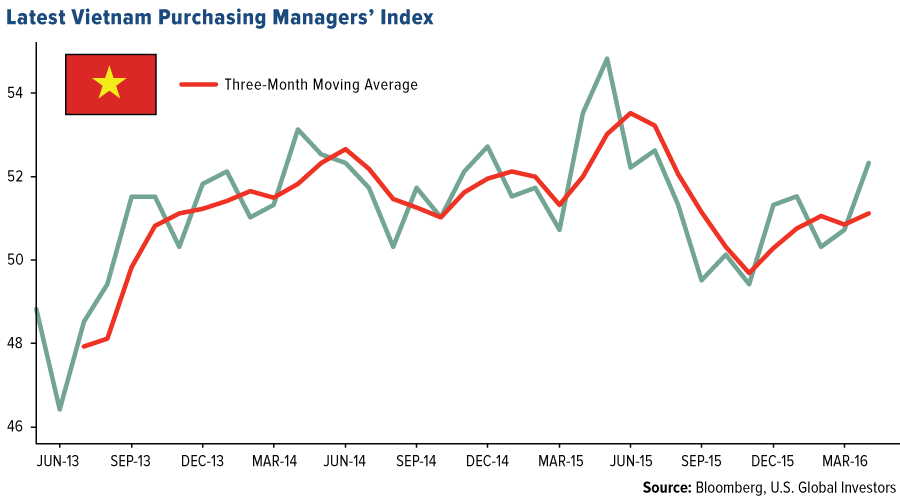

- The most prominent headline from U.S. President Obama’s highly-publicized trip to Vietnam this week was undoubtedly that the U.S. intends to lift its decades-old ban on the sale of arms to Vietnam, but as discussed before, Vietnam also stands to gain as a major beneficiary of the Trans-Pacific Partnership (TPP). Next week Vietnam releases its PMI, which has been climbing of late. Vietnam’s most recent print (for the April period) was 52.3.

- Next week, several other Asian nations release their PMIs as well. As usual, investors will pay particularly close attention to China’s PMI, both the official government Manufacturing PMI (for which a print of 50.0 is expected) as well as the Caixin Manufacturing PMI (for which a print of 49.2 is expected).

- China’s stock exchanges have released an announcement indicating an intention to restrict trading halts in Chinese securities, which should bolster Chinese hopes for eventual MSCI inclusion of A-share stocks.

Threats

- Retail sales in Hong Kong are due out next week, with analysts expecting year-over-year drops in value and volume of -10.0 and -8.0 percent respectively.

- Many may interpret President Obama’s announcement of the lifting of the U.S. ban on arms sales to Vietnam as a potential shot across China’s bow, particularly given increasing regional tension about the South China Sea.

- Despite an upbeat outlook for some potential beneficiaries of freer trade, there remain numerous opponents to global trade deals such as the TPP, with particularly heated rhetoric and apparent opposition in this U.S. election cycle.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 2.2 percent. The new cabinet of the Justice and Development (AKP) party was announced. Despite intensified market expectations for a possible departure by Mehmet Simsek, Deputy Prime Minister in charge of economy, he kept his position in the government.

- The Russian ruble was the best performing currency this week, gaining 1.7 percent against the dollar. The ruble continues to appreciate along with Brent crude oil which traded above $50 per barrel on Thursday, a level it hasn’t reached since in November of 2015.

- The industrial sector was the best performing sector among Eastern European markets this week.

Weaknesses

- Ukraine was the worst performing market this week, losing 1.7 percent. Despite the truce agreement between Russia and Ukraine, fighting is still being reported in eastern Ukraine. Full-scale battles have subsided, but clashes remain frequent. Both sides accuse the other of violating a cease-fire agreement reached more than a year ago.

- The euro was the worst performing currency this week, losing 98 basis points against the dollar. The dollar gained for the week ahead of the anticipated rate hike in the U.S. and the euro declined.

- The utility sector was the worst performing sector among Eastern European markets this week.

Opportunities

- Eurozone Finance ministers reached an agreement for the completion of the First Review on Greece’s bailout plan. Greece is due to receive EUR 7.5 billion in June to covers its debt servicing needs and EUR 2.8 billion will be paid after the summer. Greece’s bailout funding for this summer is safe.

- Russia sold $1.75 billion in dollar-denominated debt; it was the first eurobond sale since the West applied sanctions two years ago after Russia annexed Crimea. Another eurobond sale could follow later this year to reach the government’s $3 billion borrowing target for this year. It is a positive step towards restoring investor confidence in the sanctions-hit country.

- Czech President Milos Zeman named Jiri Rusnok as a central bank governor. Rusnok is well known for advocating a strong currency and he will oversee preparation for scrapping the limit on koruna gains, now set at about 27 per euro. The regulator sees itself keeping the currency regime in place until around mid-2017.

Threats

- The Markit Flash Eurozone Composite PMI that gives an overview of manufacturing and services sectors slipped to a 16-month low of 52.9 in May, down from 53.0 in April. The latest two months' weak data imply that economic growth has likely slowed in the second quarter.

- According to Bloomberg, fund managers prefer to keep underweight positions on Turkish assets as the new government’s main focus remains on the constitutional reforms rather than on the economy. Simsek’s re-appointment as Economy Minister drove the lira to a two-week high against the dollar but this could be a short-lived rally.

- Last week the president of Russia, Vladimir Putin, hosted leaders from across Southeast Asia. Bank of Russia First Deputy Governor Ksenia Yudaeva said that a slowdown of 1 percent in the Chinese economy would translate into a deceleration of about half as much in Russia’s gross domestic product. Russia would be one of the first victims in case of a hard landing by the Chinese economy.

(c) US Global Investors