Three Trends to Watch as the Tech Sector Evolves

When market certainty is in short supply and scant growth seems to be on the horizon, it helps to focus on the future—specifically on identifying sources of future growth. In the information technology (IT) industry, this means identifying a strong, secular trend that’s robust to market shocks and can lead to growth in a variety of economic scenarios. It also means looking for opportunities, not just within but outside the traditional definition of IT.

New Software calls for new thinking

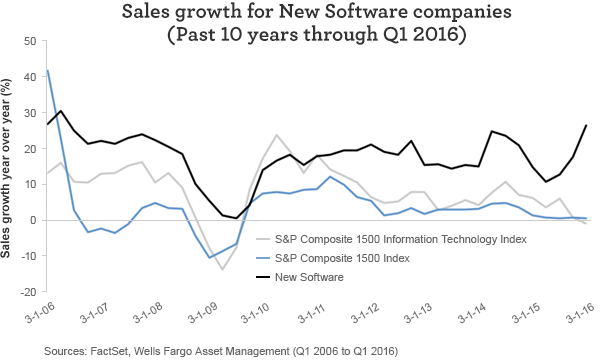

Investors should dig deeper into IT to study what we call New Software companies, which benefit from both company-specific drivers and strong, secular trends in areas such as cloud services, data analytics, network security, and online/mobile advertising. Companies fitting this profile have been experiencing much stronger growth compared with the broad economy and the overall IT sector.

In a limited economic growth environment, we believe that tech companies like these—with the potential to deliver solid, long-term growth—may command premium valuations. This is especially relevant for investors with longer-term investment time horizons that could allow them to capitalize on the ever-morphing technology landscape.

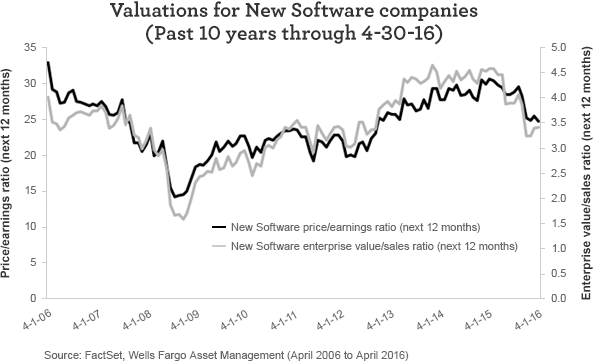

In recent years, these companies’ stock prices have not been immune to market volatility, especially in early 2014 and early 2016. However, their fundamentals—as illustrated by sales growth—generally stayed intact, and valuations have since become much more attractive as a result.

The New Software peer group highlighted in the above charts consists of companies that are typically found in the software, internet software and services, and IT services industries. However, investors should also look in other sectors, such as consumer discretionary and health care. After all, there are innovative firms bringing technology to bear on these sectors as well: think medical record analytics for the health care sector and data-driven marketing tools in the consumer arena. And, in some cases, the lines have blurred, with many firms in non-IT sectors becoming technology companies.

We’ve listed below three types of companies to consider within the New Software category:

- New innovation and market opportunity (the little engine that could)

- Barbell (the inventive behemoth)

- Higher quality (the risk-minded pivot)

Each approach exhibits unique risk and return characteristics. The highest-risk approach is the new innovation and market opportunity given that many of these companies are less established and their eventual success is sometimes more uncertain. The other two approaches could offer ways to invest in New Software with potentially less overall risk.

1. New innovation and market opportunity (the little engine that could)

This approach seeks to identify the most innovative IT companies early in their lifecycle that can generate rapid growth for a sustained period.

Companies fitting this profile typically have a small share of a large and expanding market. The hope among investors is that the company will be one of the winners, experiencing substantial growth and becoming an acquisition target of larger competitors.

In recent years, many of these companies have generated strong revenues but have spent substantial capital to expand their sales forces and enhance their products, with an aim to gain market share and expand into new markets. In essence, they’ve been willing to achieve only limited profitability in the near term, recognizing the potential reward of capturing market share. They have prioritized market-share growth over profit growth. Even though profit margins have remained challenged for these companies, we’ve recognized that several have begun to demonstrate evidence that they are on the right track toward stronger profitability.

- When investors are more risk-averse, or when investors have demanded more visibility into near-term profitability, these companies have tended to exhibit significant volatility.

- A good example that comes to mind of this type of company is an industry leader in machine-learning data technology that offers analytics and security solutions. The company has been actively spending capital to expand its sales force and improve its products with a goal of capitalizing on the large market opportunity in Big Data and cyber security. This strategy has resulted in revenue growth exceeding 45% in each of the past three years but clearly has limited the firm’s profitability potential over the same period. However, the company has shown some recent profit-margin improvements.

2. Barbell approach (the inventive behemoth)

This strategy recognizes the potential volatility in less-established companies and seeks to mitigate risk by investing in secularly advantaged, mega-cap IT firms that place a significant focus on experimentation and innovation.

While several mega-cap IT companies have been slow to innovate, others have been much more effective through internal operational changes or through acquisitions. One place to look is mega-cap companies in the internet software and services field that have had dominant market leadership in areas such as mobile advertising and mobile search. In recent years, ad spending has increasingly trended toward online and mobile channels, and it’s no coincidence advertisers are also trending toward established and dominant firms that offer these services. This is especially relevant, as consumers are spending more time online and on mobile devices. Companies in this field have also successfully monetized new business segments, which have enhanced their growth potential.

The barbell approach was particularly effective in 2015 when investors often became defensively minded yet still favored a select group of well-established companies with solid visibility in their growth potential. Several of these companies were mega-cap IT companies with a dominant presence in rapidly growing areas.

- Depending on their goals, risk mindset, and time horizon, investors could be well served by allocating to companies with multiple proven concepts and solid profitability as well as companies that perhaps have a less-established market presence but significant room to grow.

- Investors should also pay attention to innovative mega-cap companies outside of the IT sector that have benefited from secular trends in areas such as cloud services. A classic example is a dominant online retailer whose cloud-services platform for businesses has generated strong growth. The company has also been successful in increasing its operating margins despite the money it’s been investing in its overall business.

3. Higher-quality approach (the quality pivot)

This approach seeks to capture the benefits of powerful secular trends while striving to lessen fundamental risks. These companies often have relatively proven concepts and typically have at least a fairly established market presence, making them high-quality companies. However, they may also be moving (hence, the pivot) increasingly toward larger business customers, which can lead to increased revenues and profitability. As a result, these firms typically have attractive profitability and the potential for sustained growth, both in cash flows and earnings.

- In times of market uncertainty, investors tend to prefer companies with proven concepts and higher-quality fundamentals. Another way to approach this category is by sifting through select companies that are potentially at an inflection point where profitability is likely to significantly improve in the coming quarters as a result of increased sales productivity or stable-to-lower operational costs.

- A great example of this concept is a digital content and marketing technology company that pivoted a few years ago from a more traditional license-based software approach to a subscription-based model (cloud services). The company initially felt some pressure on its fundamentals as it successfully navigated this transition. However, over the past several quarters, it began to reap the rewards of this initiative, as it now has much more visibility in its revenue-growth rate and its profitability has significantly improved.

New software: Understand the risks and company-specific fundamentals

Looking ahead, we believe investors could be well served by allocating a portion of their portfolios to companies with sustainable sources of revenues and earnings. However, investors should consider multiple factors when investing in higher-growth stocks within the IT sector:

- First, it’s important for investors to identify companies that are not only benefiting from positive secular trends but also have company-specific drivers that could generate future success for the company.

- Second, companies benefiting from secular trends come in various forms with unique risks, so—again—careful stock selection and risk management are key.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 6-1-16 and are those of Dr. Brian Jacobsen, CFA, CFP, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management