- Decision Day Nears for Britain

- The Fed Defers, But Won’t Stand Pat Forever

With the European Union (EU) referendum now less than a week away, it is difficult here in Britain to think about much else. Given market movements this week, it appears this is the case throughout much of the globe. We visited the topic of Brexit in this space back in February; here, we’ll revisit what’s at stake and provide an update on recent developments.

The EU has been an evolving project of integration for many decades. At its heart, the Union was intended to bring European nations closer together following the two World Wars. In this respect it has been successful, and the closer integration has bought many benefits to its members. As a single entity, the EU is the largest economy in the world and a third of global trade is conducted with the Union. It therefore carries substantial clout internationally.

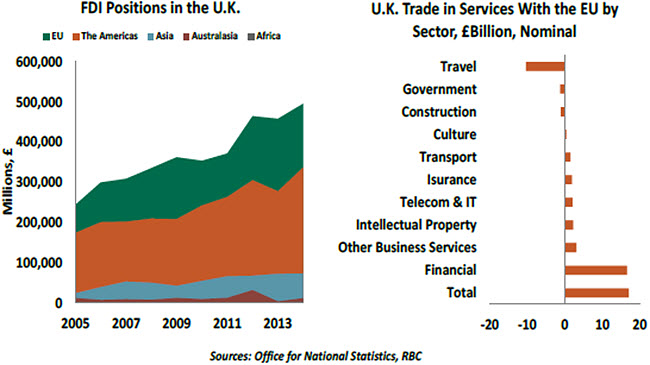

The United Kingdom benefits from membership through various channels. Exporters can sell goods tariff-free to all other members, and workers can move freely (in both directions) between member countries. The U.K. service sector runs a surplus with the rest of the EU worth £17.1 billion. Financial services are particularly important, with London the financial capital of Europe, and EU countries make substantial direct investment into the United Kingdom.

Since February, the rival groups have been doing the rounds in what has become an increasingly bitter debate. The Remain camp has largely focused on the potential loss of commerce and capital as a main campaign theme. While significant, the potential economic consequences have apparently not alarmed the average voter. The tactic of stressing the negatives instead of highlighting the many benefits of membership has earned the Remain camp some critics.

Immigration has emerged as a focal point for Leave supporters, with many citing a “lack of control” over borders as a swing factor. (This despite the fact that the majority of immigrants travel to the United Kingdom for work and contribute more to the economy than they receive in welfare benefits.) The bureaucrats in Brussels have also been singled out for scorn by the Leave platform, whose posters ask the question: “Who really runs this country?”

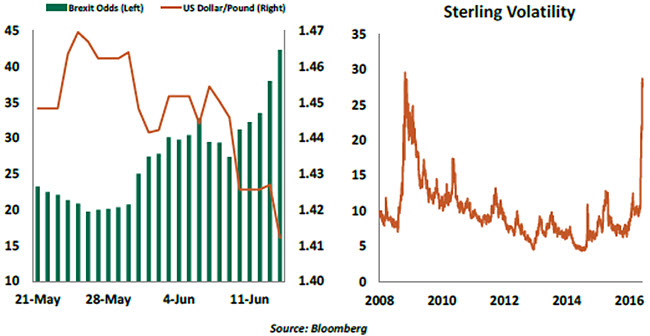

Markets have been watching polls and betting probabilities closely. Polling numbers have been volatile, but the gap between the Remain and Leave camps has narrowed substantially, with one poll at the end of last week suggesting a 7% lead for Leave. Implied probabilities from betting markets have consistently been in favor of remaining, with the likelihood of staying in the EU as high as 80% before declining recently.

The moves in the polls have rattled markets. The 10-year U.K. gilt recorded a new low of 1.1% this week and the 30-year dropped below 2% for the first time, suggesting investors are seeking safety before the vote. Other investors pulled out of sterling and U.K. equities, with the former falling to $1.41 and the FTSE 100 dipping below the 6000 mark. Sterling volatility touched highs not seen since the Great Recession and German 10-year bund yields traded below zero for the first time ever as concerns spread across the Channel.

So how might the landscape look in the event of a departure? Initially, a harsh market reaction is expected, with sterling and U.K. equities falling further. There would likely be action by central banks to support market liquidity (indeed, the Bank of England has said it will do this in the run up to the vote), but it is fairly unlikely there would be any interest rate moves initially. Headwinds from markets could impair consumption and business investment.

U.K. growth would also be adversely affected as trading relationships fall into limbo. The Leave side is adamant that Britain would be able to negotiate new terms with both the EU and other countries easily and quickly. But it would be in the EU’s interest to make an exit as painful as possible for the United Kingdom to send a message to other members that an exit attempt is not worthwhile. One commenter compared the situation to a divorce where the jilted spouse gets to set the terms unilaterally.

Two possible models are frequently cited as examples the United Kingdom could follow. Norway has an agreement that allows access to the EU free market, but in return the Norwegians contribute to the EU budget and have to accept free movement of people and adhere to EU laws. All three of these are certainly unpalatable to the majority of Brexiteers. The second is the recently agreed EU/Canada trade deal, but the agreement took over 7 years to negotiate, and it does not include financial services.

A protracted and volatile set of negotiations could easily ensue if Leave voters carry the day. Following that outcome, there would likely be an emergency meeting of EU leaders, and Prime Minister David Cameron would be under pressure from the Leave camp to begin the exit process as quickly as possible.

It is hard to see Cameron remaining as leader of the Conservative party, let alone Prime Minister, in this scenario. Given the party’s deep divisions over Europe, it is plausible the party could fracture completely. This could add to the sense of instability that would almost certainly spread if Brexit occurs.

In the event of a Remain vote, a relief rally and overshoot in equities and sterling is expected, with a moderation soon after. Growth in the second half of the year would likely be stronger as confidence returns and postponed demand is realized.

Politically, the situation would be slightly more complicated. If the vote is only slightly in favor of remain, Cameron could face a leadership challenge, and again, it is not out of the realm of possibility that the Conservative party could fracture further given the level of party infighting. This is despite the fact that, in the face of a weak opposition leader in Jeremy Corbyn, Conservatives have a real opportunity to maintain power for a prolonged period of time if they can remain united.

In an awful turn of events, a pro-EU Member of Parliament was slain on Thursday by an attacker who allegedly shouted the name of an anti-EU political party. The incident caused a temporary cessation in the campaign, an interlude of civility which one hopes will offer time for all to reflect and pay respects.

Uncertainty and volatility are the only sure bets between now and next Thursday. Results will be available early morning on June 24 London time. We continue to think that Britain will choose to remain part of the EU, but the vote will be very close. Either way, the U.K. economy and its political process may turn up losers.

The Federal Reserve Bides Its Time

As we wrote last week, it was unlikely that the Federal Reserve would move to change U.S. monetary policy this week. The heightening anxiety surrounding Brexit, combined with concern over the U.S. employment situation, made the timing difficult. But while the outcome was nearly preordained, the meeting nonetheless produced some interesting insights. The most significant, to us, was the plurality of participants who still expect at least two rate increases this year, despite international risks and the disappointment of the May employment report.

The post-meeting statement and the updated forecasts offered additional insights into the following issues:

- The U.S. employment situation. The May payroll reading apparently had little impact on the Fed’s formal outlook for the labor market. The statement noted that “the pace of improvement in the labor market has slowed,” but that language implies that improvement is ongoing. The Fed’s Summary of Economic Projections (SEP) showed little change in the expected path for the jobless rate.

- In her prepared remarks for the press following the meeting, Fed Chair Janet Yellen noted that wages had been increasing more rapidly, and she cautioned against overreacting to one or two months of disappointing data. She noted, however, that upcoming employment reports will be watched carefully.

- If the Fed thinks that the employment situation is deteriorating, it is not apparent from anything that it offered us this week.

- The path of U.S. inflation. The expected course of inflation was raised slightly, but longer-term expectations were unchanged. Tellingly, there is virtually no sign in the SEP that participants foresee allowing inflation to run “hot,” exceeding the 2% target in any meaningful way.

- The statement acknowledged the decline in market-based inflation expectations, but participants do not seem to think this will affect the progress of the price level. Yellen noted that “financial market-based measures of inflation compensation … reflect many factors and therefore may not provide an accurate reading on changes in the inflation expectations that are most relevant for wages and prices.”

- Participants seem reasonably confident that inflation will progress towards the targeted level, despite the recent drop in market-based expectations. That said, Yellen made the case for an “asymmetric bias” in her prepared remarks, meaning that the FOMC finds less risk in waiting than it does in acting too soon.

- Financial conditions. Little detail was provided on how the FOMC is thinking about international risks. The statement offered that “The Committee continues to closely monitor inflation indicators and global economic and financial developments.” Yellen added, “Vulnerabilities in the global economy remain.”

- Brexit was not mentioned in either the post meeting statement or the Chair’s prepared remarks. But it came up immediately in the question period (from Sam Fleming of The Financial Times). Yellen acknowledged that it had been a factor in the Fed’s discussions, and offered that a decision by the United Kingdom to depart the European Union would affect the economic outlook. But she seemed anxious not to get into too much depth on the topic, and certainly not to offer advice to British voters.

- The prospect for rate hikes. Interestingly, 11 participants are still calling for at least two interest rate increases during the balance of 2016, leaving the median forecast unchanged from last quarter. This seems to suggest that the remainder of meetings this year could be “live,” meaning that a change of policy could arrive at almost any juncture. Tellingly, no participants expect the Federal funds rate to close the year at its current level, which is the expectation currently implied by markets.

- Even if Brexit is averted, making a case for a move in July will be challenging. The timeline is short, the data is limited and steering markets to the right conclusion will be difficult. The absence (for now) of a scheduled press conference is also a factor. Movements in September and December might be more logical, if the data cooperates.

- There was an important adjustment in long-term expectations for the Federal funds rate. The median forecasts for 2017 and 2018 were lowered by 0.3% and 0.6%, respectively. And the long-term funds rate (which some associate with equilibrium) was reduced from 3.3% to 3%. Yellen noted that “headwinds weighing on the economy mean that the interest rate needed to keep the economy operating near its potential is low by historical standards. These headwinds … include developments abroad, subdued household formation and meager productivity growth.”

- The group is increasingly concerned about the long-term capacity and potential of the U.S. economy, anticipating an even more gradual return to a lower destination.

- In sum, the Fed provided a modicum of reassurance around the medium-term outlook while acknowledging that long-term performance might not meet previous expectations. We continue to look for the next increase in interest rates in September, with a gradual removal of accommodation to continue from there.

(c) Northern Trust