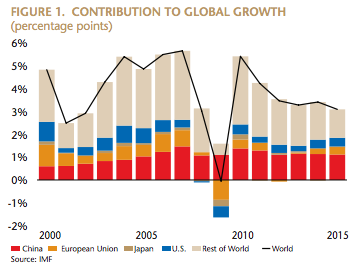

Uncertainty over the impact of the June 23 U.K. referendum to secede from the European Union may rattle Chinese investor sentiment in the short term, but the lengthy process of U.K. disentanglement from the E.U. is unlikely to have a significant impact on the Chinese economy. Last year, China accounted for 35% of global economic growth, and if Brexit results in slower growth in the U.K. and anxiety in the developed West and in emerging Europe, the Chinese share of global growth could rise even higher. China—and the rest of the region that Matthews Asia invests in, which (combined with China) accounted for about 60% of global growth last year—is likely to be considered a safe haven for investors, especially relative to European emerging markets (EM).

CHINA CURRENCY IMPACT

The favorable vote for Brexit does not mean that Britain will leave the E.U. immediately. There is an estimated two-year window for negotiating withdrawal terms. Two years of uncertainty about how this plays out will weigh on sentiment. So one of the most important things to watch is the impact on the U.S. Federal Reserve, and the strength of the dollar.

Keep in mind that the British Pound Sterling is only 4% of the renminbi’s (RMB’s) trade-weighted basket, while the U.S. dollar plus the Hong Kong dollar (which is pegged to the USD) accounts for about one-third of the basket. And it is clear that the direction of the movement of the RMB versus the USD is driven by dollar strength or weakness. The Chinese central bank (PBOC) has the ability to intervene to modulate the degree to which the RMB moves, but the direction of that movement (appreciation or depreciation vs. the dollar) is determined largely by the dollar. In other words, a weaker dollar should lead to a stronger RMB, with the degree of RMB appreciation under the control of the PBOC.

In the near term, there will (obviously) be a lot of currency volatility, but this, plus Brexit uncertainty, means it is even less likely that the Fed raises rates this year (which I thought was unlikely anyway) and probably means any increases next year will be very limited. And once markets digest the fact that the U.K. has an extended period of time to negotiate its withdrawal, the impact on the pound may be reduced. But who knows … if you think the dollar will strengthen dramatically (say about 10% as it did last year) then we could see (as we did last year) RMB depreciation of 5% to 6%, which could lead to more capital outflows. But this outflow shouldn’t be nearly as large a flow as late last year/early this year, because that large outflow followed a multi-year period of steady RMB appreciation, leading Chinese corporates to build substantial offshore positions in U.S. and H.K. dollars, which they then had to unwind when RMB depreciation began. That isn’t the case today. So I think that in an RMB depreciation scenario, outflows will increase, but not nearly to the extent that freaked out markets at the start of this year. (And note that capital outflows have been modest recently, including during periods of RMB weakness.)

Another case that can be made, however, is that a dovish Fed will mean a weak dollar over the coming year, which will mean a bit of RMB appreciation—as was the case in 1Q16.

THE IMPACT ON CHINA’S TRADE

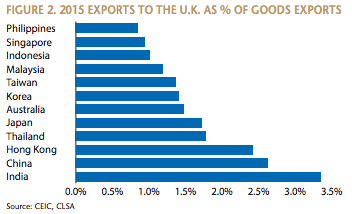

I don’t anticipate that the trade impact of Brexit will have a material impact on the Chinese economy. China’s exports to the U.K. are small relative to total Chinese goods exports (less than 3%). And, unless you expect the U.K. economy to suddenly deteriorate, there should not be a significant, near-term impact on China’s exports to the U.K. And if the U.K. does leave the E.U. a couple of years from now, it is likely that London and Beijing will have already secured a bilateral trade agreement.

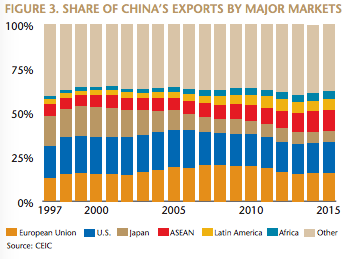

A bigger concern is whether anxiety over Brexit leads to a material downturn in the broader E.U. market, as that (including the U.K.) was China’s second-largest export market last year, taking 16% of China’s exports by value, compared to 18% by the U.S.

Here, my biggest concern is about export-related employment. Remember that in 2009, during the Global Financial Crisis, when China’s exports collapsed and millions of export-processing jobs were lost, Beijing did not devalue its currency. That was because the problem was weak global demand, not weak Chinese competitiveness. That remains the case today. For example, last year, global exports declined 13% year-over-year, but Chinese exports fell by only 3%. (It is also interesting to note that exports by privately owned Chinese firms are up 6% YoY this year, while exports by state-owned firms are down 8%.)

This is why China did not devalue in 2009. Instead, Beijing undertook the world’s largest-ever Keynesian stimulus, using bank loans to fund accelerated construction of public infrastructure. That was the origin of China’s current debt problem, but it also sucked up unemployment from the export factories, preventing social instability, and allowed China to put a floor under global growth. If Brexit were to cause another global financial crisis, and if global demand for goods were to collapse, I would expect another largescale domestic stimulus from Beijing. But I would not expect a competitive devaluation (I think the odds of this second GFC scenario are low).

IMPACT ON CHINESE POLITICS AND REFORM COMMITMENT

I do think that the results of the referendum will further strengthen the Communist Party’s view that democracy is often a messy, unproductive and unstable process, and that the Party must continue to drive more pragmatic economic policymaking. But that is, of course, not a new view on the part of the China’s leaders.

I do not think that concerns about the impact of Brexit will lead Party Chief Xi Jinping to believe that he needs to slow the already modest pace of state-owned enterprise (SOE) restructuring. Instead, I think the fact that the “Leave” majority seems to have come from the parts of the U.K. where economic recovery was the weakest, will strengthen Xi’s resolve to continue to move ahead with further reforms designed to reduce SOE overcapacity and boost growth in China’s rust belt, and to support further growth and job creation in its “tertiary sector” of services and consumption—the largest part of the Chinese economy and the part which already generates all of its new jobs.

Andy Rothman

Investment Strategist

Matthews Asia

The views and information discussed are as of the date of publication, are subject to change and may not reflect the writer’s current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. The subject matter contained herein has been derived from several sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews International Capital Management, LLC (“Matthews Asia”) does not accept any liability for losses either direct or consequential caused by the use of this information.

©2016 Matthews International Capital Management, LLC