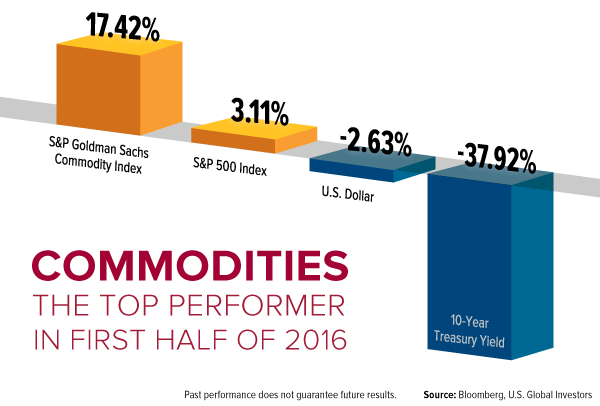

Here we are at the halfway point of the year, less than two months away from the Rio 2016 Olympic Games. As a group, commodities are the top performing asset class, beating domestic equities, the U.S. dollar and Treasuries.

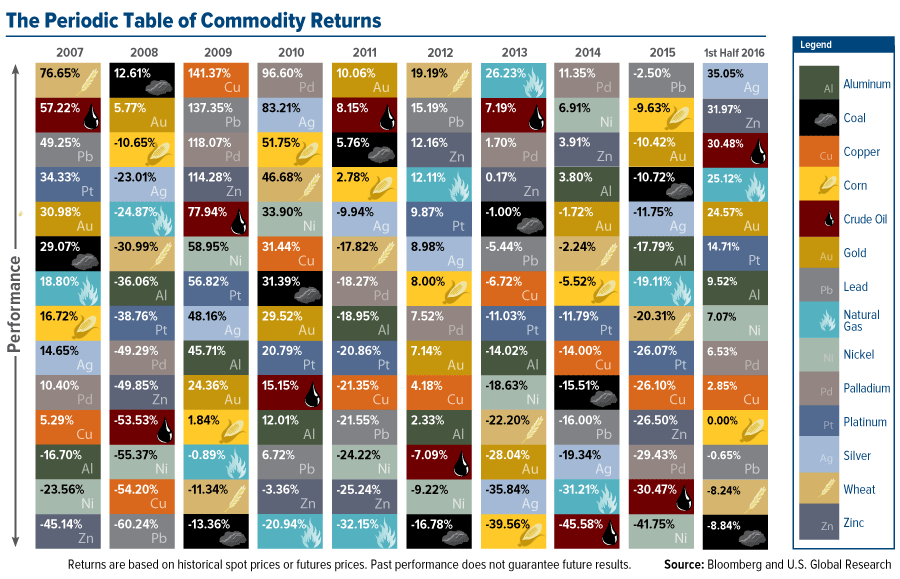

Below is our ever-popular Periodic Table of Commodities Returns, updated to reflect the first half of 2016. Click to see an enlarged version.

Commodities’ performance is quite a reversal from the weakness we’ve seen lately, particularly last year, but we shouldn’t expect another 2004 or 2005, when global trade was humming. Conditions are still not ripe for a real takeoff, with manufacturing activity in China and the eurozone struggling to gain momentum.

But there’s hope. Many of the challenges standing in the way of growth were exposed when Britain voted last month to leave the European Union (EU), which I’ve been writing about for the past few weeks. Most recently, I highlighted some of the winners to emerge from Brexit, among them gold investors, U.S. homeowners and British luxury goods makers.

Hopefully we can add global trade to the list. Brexit has brought to light some of the corruption and economic strangulation by regulation that chokes the flow of capital. This week I had the opportunity to speak with some EU citizens. Their frustration was palpable. The cronyism among the EU’s unelected officials is nothing new, but it’s only worsened over the past decade and a half, they said. The British referendum has encouraged a balanced, intercontinental discussion on the direction Brussels must take now that the corruption and depth of discontent have been exposed for the world to see.

Precious Metals Shine Brightly on Macroeconomic and Geopolitical Concerns

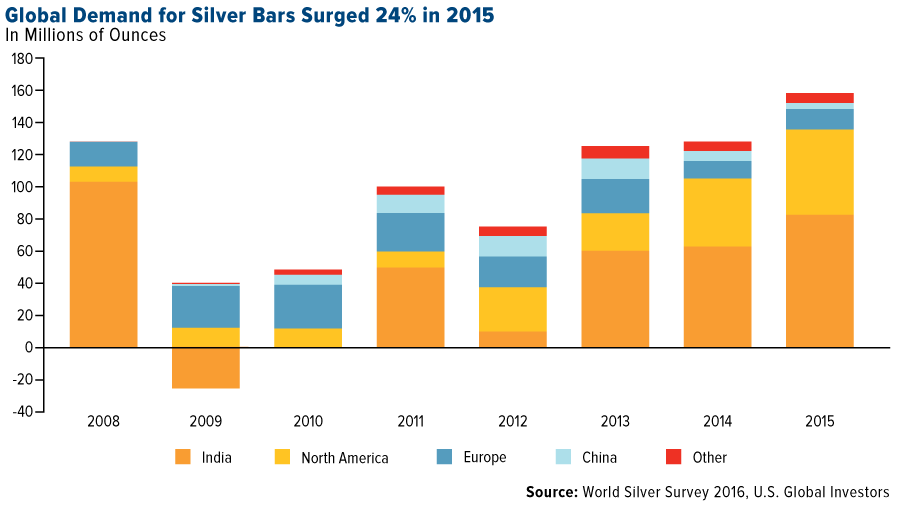

Silver demand had a phenomenal 2015, with retail investment and jewelry fabrication both reaching all-time highs. Led by consumers in the U.S. and India, coin and bar investment soared 24 percent from the previous year, while jewelers gobbled up a record 226.5 million ounces. According to the Silver Institute’s World Silver Survey 2016, metal demand for photovoltaic installation climbed 23 percent in 2015, offsetting some of the losses we continue to see in photographic applications.

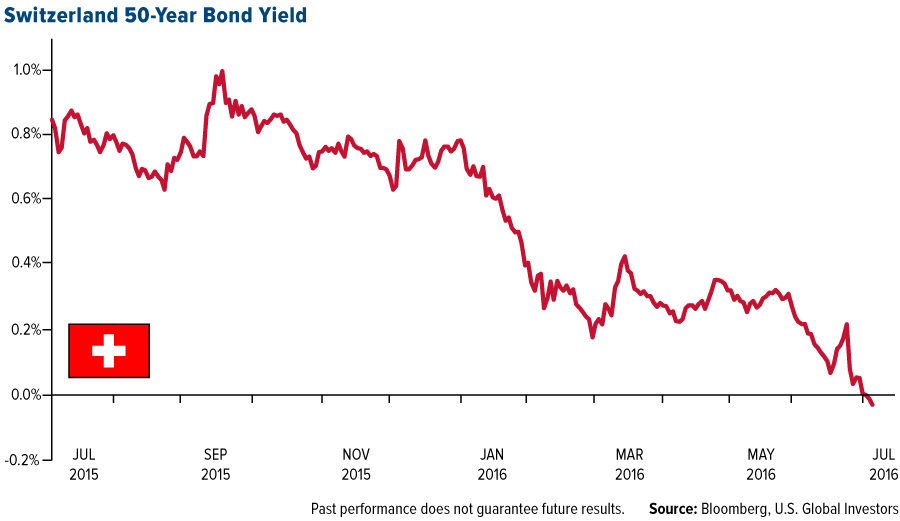

Caused by worries of a summer interest rate hike and uptick in the U.S. dollar, gold and silver both stalled in May but have since rallied on the back of Brexit and with government bond yields in freefall. For the first time ever, Switzerland’s entire stock of bonds has fallen below zero, with the 50-year yield plummeting to negative 0.03 percent on July 5.

All-time low yields can also be found in the U.S.—where the 10-year Treasury yield fell nearly 38 percent in the first half—U.K., Canada, Germany, France, Australia, Japan and elsewhere. Roughly $10 trillion worth of global government debt, in fact, now carry low to subzero yields.

This has been highly constructive for gold and silver, as yields and precious metals tend to be inversely related.

What’s more, the rally doesn’t appear to be done, with UBS analysts making the case this week that we’re in the early stages of a new bull run. Credit Suisse sees gold testing the $1,500 an ounce mark as early as the beginning of 2017. As for silver, some forecasters place it at between $25 and $32 an ounce by year’s end.

The risk now is that higher prices are pushing away some potential investors. Today Bloomberg reported that gold imports in India plunged a sizable 52 percent in the first half of 2016, compared to the same period in 2015.

Supply and Demand Rebalancing?

Much of the price appreciation has been driven by a global rebalance in supply and demand. Dismal prices over the last couple of years compelled explorers and producers to cut activity and other capital expenditures, while demand continues to rise.

This dynamic certainly helped zinc, the best performing industrial metal of 2016 so far. During the first four months of the year, mine production fell 8.1 percent from the same time a year earlier due to declines in Australia, India, Peru and Ireland, according to the International Lead and Zinc Study Group. In January, London-based Verdanta Resources made its last zinc shipment from its Lisheen Mine in Ireland, which for the last 17 years had produced an average 300,000 tonnes of zinc and 38,000 tonnes of lead concentrate per year.

Meanwhile, the demand for refined zinc, used primarily to galvanize steel, is expected to increase 3.5 percent this year. What might surprise you is that a large percentage of this growth can be attributed to China, which is still investing heavily in infrastructure, even as money supply growth has slowed.

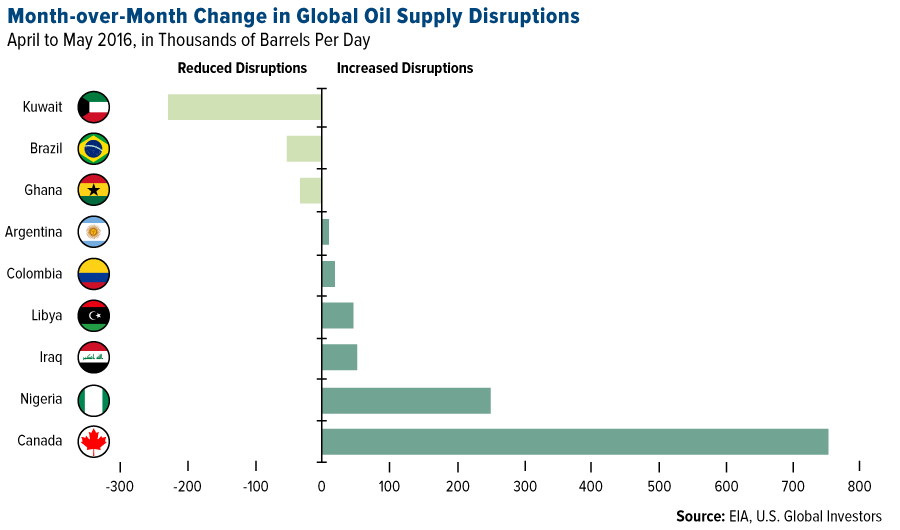

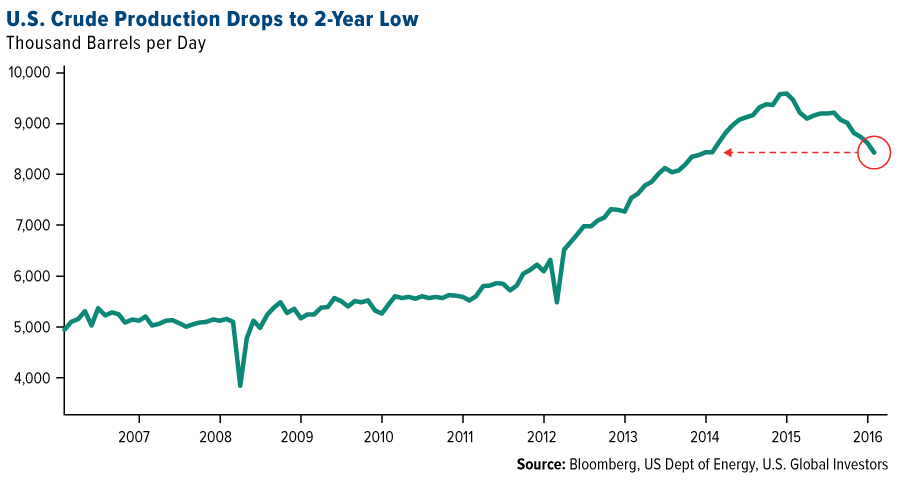

This rebalancing has also bolstered crude oil prices, up 73 percent since its 2016 low in February. Unplanned production outages in Canada, Nigeria, Iraq and elsewhere removed a collective 3.6 million barrels per day off the market in May alone. Coupled with ongoing declines in the North American rig count—U.S. crude production is now at a two-year low—this helped nudge prices up to levels not seen since July 2015.

At the same time, global consumption is expected to increase by 1.5 million barrels a day both this year and next, according to the U.S. Energy Information Administration (EIA), with North America and Asia, particularly China and India, responsible for much of the growth.

Record Automobile Sales Support Commodities

|

Crude consumption is also being supported by robust automobile sales, which set a six-month record in the U.S. following six straight years of growth. Between January and June, sales reached an all-time high of 8.65 million units, up 1.5 percent from the same period last year. In China, the world’s number one auto market, 10.7 million vehicles were sold in the first five months, an impressive year-over-year increase of 7 percent. Sales of light vehicles, especially motorcycles, have been strong in India.

As you might expect, this has likewise benefited demand for platinum and palladium, both used in the production of autocatalysts. The CPM Group anticipates palladium demand to reach an all-time high this year, up 3 percent from last year, on tightened emissions standards and the purchase of larger cars and trucks in the U.S. on lower fuel costs. (The larger the engine, the more palladium or platinum is needed to reduce emissions.)

Since January, the platinum group metals (PGMs) have increased over a third in price, marking the end of an 18-month bear cycle, according to Metals Focus’ Platinum & Palladium Focus 2016. Fundamentals have improved since last year, when EU growth concerns and Volkswagen’s emissions scandal weighed heavily on investment prospects.

Like zinc, crude and other commodities, the PGMs were supported the last six months by lower output levels, as labor disputes in South Africa—the world’s largest platinum producer and number two largest palladium producing country—disrupted operations.

EXPLORE INVESTMENT OPPORTUNITIES IN PRECIOUS METALS

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.10 percent. The S&P 500 Stock Index rose 1.28 percent, while the Nasdaq Composite climbed 1.94 percent. The Russell 2000 small capitalization index gained 1.78 percent this week.

- The Hang Seng Composite lost 0.89 percent this week; while Taiwan was down 1.11 percent and the KOSPI fell 1.22 percent.

- The 10-year Treasury bond yield fell 9 basis points to 1.36 percent.

Domestic Equity Market

Strengths

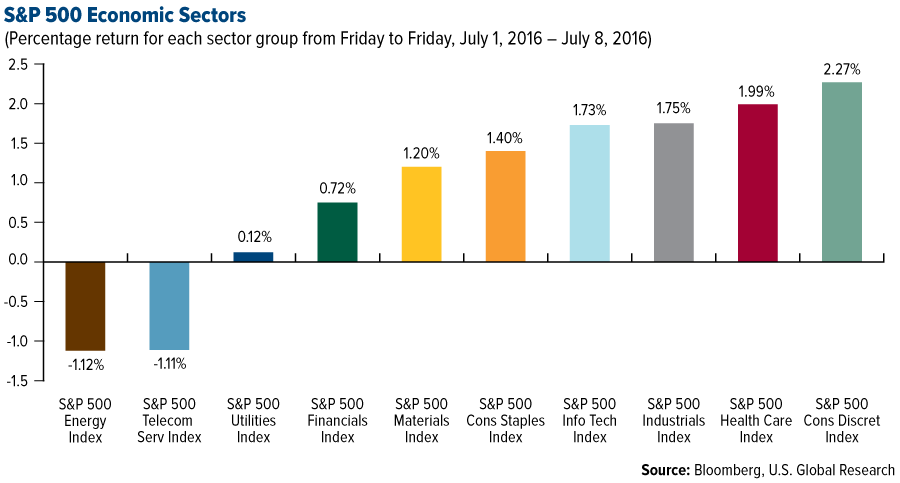

- Consumer discretionary was the best performing sector for the week, increasing 2.27 percent compared to an overall increase of 1.27 percent for the S&P 500 Index.

- Nvidia was the best performing stock for the week, increasing 8.98 percent. On July 7, the company finally announced the GeForce GTX 1060, targeted at mainstream desktop gaming computers.

- Danone has agreed to buy organic food maker WhiteWave Foods, doubling Danone’s U.S. business in a deal valued at $12.5 billion.

Weaknesses

- Energy was the worst performing sector for the week, falling 1.12 percent compared to an overall increase of 1.27 percent for the S&P 500.

- Harley-Davidson was the worst performing stock for the week, falling 10.18 percent. The motorcycle icon saw its stock soar last Friday in light of rumors that the company might be the subject of a takeover bid from a private equity investor. However, when those rumors failed to lead to an immediate definitive offer, investors reversed ground.

- Congress might deny Boeing and Airbus export licenses with Iran. In the wake of the Iran nuclear deal, aircraft manufacturers like Boeing and Airbus were freed to do business with the Islamic Republic. But Congress is debating whether to grant export licenses to the manufacturers for fear that the planes could be used for purposes other than commercial aviation. Airbus, while based outside the United States, still needs U.S. export licenses since 10 percent of its components are U.S.-sourced.

Opportunities

- Consumer staples stocks have been on a tear recently, climbing to all-time highs. According to BCA, while valuations look extended, the conditions to sustain them are in place. A flurry of intra-sector mergers and acquisitions (M&A) activity, anemic global growth and the plunge in global bond yields all point to a premium valuation in long duration sectors. Furthermore, the rising bond-to-stock ratio—coupled with the firming dollar and resurgent volatility across asset classes—is a boon for non-cyclical consumer staples’ relative performance.

- The decline in global bond yields and prevalence of negative interest rates outside the U.S. represent a windfall for U.S. housing, to the extent that U.S. mortgage rates are pushed below levels warranted on U.S. fundamentals alone. As a result, the housing sector is poised to pick up steam.

- U.S. consumer electronics spending is accelerating. If such spending is sustained, consumer electronics makers could see a spark.

Threats

- Government regulators might scuttle $91 billion worth of health care mergers. Both the $57 billion merger of Cigna and Anthem and $37 billion merger of Aetna and Humana drew criticism from lawmakers Thursday. The Aetna-Humana deal reportedly has drawn the attention of the Department of Justice, while the Connecticut State Attorney General cast doubt on the Cigna-Anthem deal.

- Retail sales for June come out next Friday and are expected to slow down to 0.1 percent from the previous 0.5 percent. A confirmation could impact consumer discretionary stocks negatively.

- Airlines have been slammed lately, trailing not only the S&P 500 but also their industrials peers. However, news that Delta would not meet already weak passenger yield expectations demonstrates that analysts still remain overly optimistic. Airlines have expanded capacity too aggressively while fuel prices were low, and are now being hit with pricing pressure as travel budgets are trimmed.

The Economy and Bond Market

Strengths

- June payrolls were far stronger than expected, rising 287,000, over 100,000 more than expected. The economy averaged 149,000 new jobs per month in May and June, a figure that will give the Federal Open Market Committee (FOMC) a bit more confidence as it considers raising rates later this year.

- The U.S. service sector remains strong. Both the Institute of Supply Management and Markit Economics released strong reports on the U.S. services economy on Wednesday. While not overwhelming, the numbers did indicate that the sector which employs a large majority of the U.S. population remained in expansionary territory.

- Initial jobless claims beat expectations on Thursday with just 254,000 Americans filing for unemployment insurance. This continues the longest streak of claims under 300,000 since 1973.

Weaknesses

- Business investment fell more than expected in May. Both factory and durable goods orders missed expectations in May, falling 1 percent and 2.3 percent according to the Department of Commerce. Economists had expected only a 0.8 percent drop for factory orders. The drop in durable goods orders was particularly worrying since it is on track for a third-straight quarterly drop of 2 percent. This has only happened twice outside of a recession, in 1951 and 1986.

- Minutes of the June FOMC meeting released this week show that rate setters were in no rush to hike rates, saying it was prudent to wait for additional economic data before proceeding. The committee also cited the uncertainty surrounding the Brexit referendum, which took place a week after the meeting, as a reason to hold rates steady. Not being able to raise rates is a reflection of global economic weakness.

- The U.K. property market has been considered among the safest havens for global investors over the last 25 years, but given the uncertainties surrounding the fallout from Brexit, that safe-haven status is being called into question. As a result, multiple open-ended funds investing in U.K. commercial real estate have been forced to halt redemptions and dramatically mark down their holdings as investors seek to withdraw funds.

Opportunities

- June consumer price index (CPI) will be released next Friday. Given the overwhelming strength in the recent jobs report, a strong CPI reading could dispel worries about the U.S. economic recovery and put a rate hike back on the table.

- Industrial production for June, released on Friday, is forecasted to improve to 0.1 percent from the previous -0.4 percent. A confirmation of the forecast would assuage jitters stemming from the Brexit vote.

- The Illinois legislature approved a six-month stopgap budget, ending the record long impasse of the spending plan that triggered downgrades to the state’s credit rating. This is a small step in the right direction and provides a temporary reprieve for Illinois, which had faced shuttered essential services, a halt to road construction, and the delayed opening of schools. The compromise gets the state through the November election and allows lawmakers to address a full-year budget in January, when a simple majority is needed to pass legislation. Right now, a three-fifths majority is needed to approve bills, making consensus difficult.

Threats

- The dividend yield on the S&P 500 Index rose above the U.S. government bond’s 30-year yield for the first time since 2009 this week. This comes as bond yields globally continue to slide amid renewed worries over global growth that have resurfaced following the Brexit vote.

- The University of Michigan Sentiment index preliminary reading for July will be released on Friday. The latest readings have been strong, but given Brexit and the fallout in U.K. consumer confidence, the perception of U.S. consumers could be negatively impacted.

- Many Italian banks are saddled with crippling amounts of bad loans, but bailing them out with government money is not an option until bond holders first take a hit, according to European Union rules. In Italy, retail investors are major holders of bank debt, making a so-called “bail-in” politically unpopular. Prime Minister Matteo Renzi is seeking flexibility from the EU in applying the rules, but is running into opposition from German Chancellor Angela Merkel. Fears of a systemic crisis may build until a resolution is worked out.

Gold Market

This week spot gold closed at $1,366.38, up $24.53 per ounce, or 1.83 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, gained 5.16 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index traded up 2.97 percent. The U.S. Trade-Weighted Dollar Index moved higher with a 0.66 percent gain.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Jul-5 |

U.S. Durable Goods Orders |

-2.2% |

-2.3% |

-2.2% |

|

Jul-7 |

U.S. ADP Employment Change |

156k |

172k |

168k |

|

Jul-7 |

U.S. Initial Jobless Claims |

265k |

254k |

270k |

|

Jul-8 |

U.S. Change in Nonfarm Payrolls |

175k |

287k |

11k |

|

Jul-12 |

Germany CPI YoY |

0.3% |

-- |

0.3% |

|

Jul-14 |

U.S. Initial Jobless Claims |

265k |

-- |

254k |

|

Jul-14 |

U.S. PPI Final Demand YoY |

-0.1% |

-- |

-0.1% |

|

Jul-14 |

China Retail Sales YoY |

9.9% |

-- |

10.0% |

|

Jul-15 |

Eurozone CPI Core YoY |

0.9% |

-- |

0.9% |

|

Jul-15 |

U.S. CPI YoY |

1.1% |

-- |

1.0% |

Strengths

- The best performing precious metal for the week was platinum, up 3.38 percent and marking eight straight trading days of gains. China has seen an 11 percent jump in auto sales through May, spurred by a tax cut on purchases.

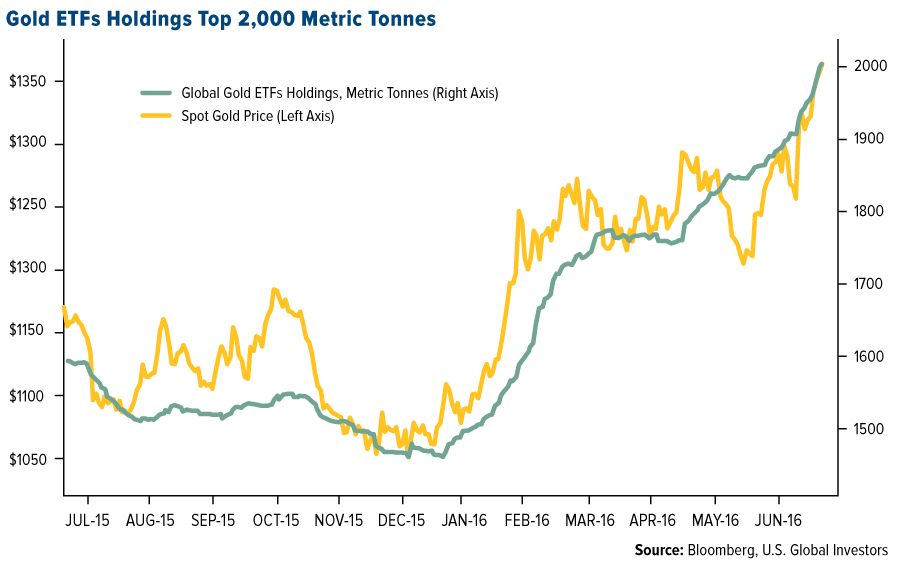

- Gold demand has surged this year as seen in global gold ETF holdings. Holdings have increased by more than 500 tonnes since January, reaching a high of over 2,000 tonnes for the first time in three years. Investor gold demand has been prompted by slow global growth, negative interest rates in Europe and Japan, and the unlikelihood of the Federal Reserve raising rates in the near future.

- China resumed buying gold in June after taking an uncharacteristic break in May. The People’s Bank of China, the country’s central bank, purchased 15.6 tonnes, increasing its reserves to 1,823 tonnes. Retail investor buying is on the increase in China as well, as outstanding shares in the Huaan Yifu Gold ETF, China’s largest bullion-backed ETF, jumped to a record high of 17.58 tonnes of bullion equivalent on Tuesday this week, according to David Xu at Huaan Asset Management Co.

Weaknesses

- The worst performing precious metal for the week was gold, up 1.83 percent, which has been pretty steady as of late marking the sixth consecutive weekly gain.

- Payrolls for June busted through expectations, climbing to 287,000. At the same time, wages advanced less than expected. The news sent gold into a swing between gains and losses. Chris Gaffney, president of EverBank World Markets in St. Louis, commented that members of the Fed “are breathing a sigh of relief after this report, but the U.S. economy and more importantly the global economy is still in a state of uncertainty,” and that those concerns “will keep them from moving rates higher in 2016.”

- India’s gold imports dropped almost by half in June compared to a year earlier. June imports of 32 tonnes were 43 percent less than June last year, at 55.7 tonnes. This is a significant drop for India, which, along with China, are the top two countries for gold consumption.

Opportunities

- Gold forecasts are coming in resoundingly bullish. ABN Amro, rated as the most accurate forecaster by Bloomberg, targets a gold price of $1,425 per ounce, according to analyst Georgette Boele in a report received Thursday. Boele cites prospects for accommodative central bank policies in Europe and elsewhere in the world. UBS also pronounced its target at $1,400, up from $1,250. UBS analyst Joni Teves sees gold reaching this level in the short term, writing that “gold has likely entered the early stages of the next bull run.” Teves also sees prices averaging $1,340 in the second half of this year. State Street, meanwhile, sees a price range of between $1,400 and $1,450, recommending that clients hold between 2 and 10 percent of their portfolios in gold.

- Jeff Gundlach says he’s not selling gold. The DoubleLine Capital founder calls gold the best alternative to stocks and bonds, as reported by Reuters. Gundlach goes on to say that 10-year Treasuries at current yields are the “worst trade location” ever, and stressed the uncertainty seen by policymakers and European banks. Gold options traders are also showing their expectations that prices will keep climbing. Compared to puts hedging against a 10 percent drop, calls betting on a 10 percent gain through the biggest gold ETF are nearing the most expensive since 2009.

- Even while gold has seen a big boost of 7 percent following the Brexit vote, silver is outshining, having jumped 17 percent. Silver enjoys demand for jewelry and “safe haven” appeal, similar to gold, but has more industrial use than gold. Simona Gambarini, an economist at Capital Economics, expects silver supply to contract. Demand in China has been strong, due to consumers seeking a cheaper alternative to gold. Central banks may also start building up their silver holdings, according to Andrew Chanin, CEO of PureFunds. Sean Brodrick of Oxford Club sees silver reaching $25 per ounce by the end of the year.

Threats

- The Japanese yen is in danger of collapse, according to Yukio Noguchi, a university professor and former Ministry of Finance official. He sees a scenario where the yen could drop to 300 per U.S. dollar, compared to last week’s rate of 101 yen per dollar. Amid this uncertainty, along with negative interest rates, Japanese investors are buying gold to store in Switzerland, according to BullionVault. Japanese consumers see Switzerland as a safer place to hold their gold than at home in Japan.

- The United Nations stated last month that Congolese exporters are ignoring requirements to source gold from conflict-free mining states. The illegal gold trade is being smuggled, largely to buying houses in Dubai. Sophia Pickles from Global Witness says that “Congo and the United Arab Emirates have dramatically failed” to uphold their responsibilities to put conflict and human rights abuses in check.

- Centerra Gold agreed to acquire Thompson Creek Metals for $1.1 billion to expand its North American holdings. The deal would represent a 32 percent premium on Monday’s closing prices for the equity, which was essentially worthless unless the debt and unpaid interest were settle too. Centerra has been in a dispute with the Kyrgyzstan government over its Kumtor Gold Mine, which generates most of the company’s revenue. Kyrgyzaltyn, The Kyrgyzstan state-backed gold company, voted against the planned acquisition deal on the basis that it will dilute its shareholding in Centerra. It is unclear what the next move of the Kyrgyz government will be to the proposed deal.

| IN THE NEWS | ||

![[thumb]](/images/content_image/data/c3/c3a2293ac24b96201cfb5c8ccb4c1fad.jpg)

July 7, 201610-Year Yields Drop, Gold Goes Higher |

![[thumb]](/images/content_image/data/3d/3db79a86c66b233355ef6bbf79f2781b.jpg)

July 6, 2016Who Wins Post Brexit? |

![[thumb]](/images/content_image/data/6e/6e50fb1bc52851768140ae32eeef915b.jpg)

July 6, 2016Frank Holmes, Karim Rahemtulla: Where Gold Is Now |

Energy and Natural Resources Market

Strengths

- Money is flowing into precious metals at a record rate. Bank of America Merrill Lynch showed $4.1 billion poured into precious-metals funds in the week ended Wednesday, the largest weekly inflow on record. The team at BofAML expects gold and silver to continue to outperform as the world moves from “crisis to crisis.”

- The best performing sector for the week was the NYSE Arca Gold Miners Index. The index of gold mining companies rose 5.2 percent for the week as gold price continued to outperform on fears of a banking crisis in Europe.

- Klondex Mines LTD, a Canadian gold producer with operations in Nevada, was the best performing stock in the broader natural resource space after rallying 17.9 percent for the week. The stock rallied on the back of strong gold prices.

Weaknesses

- The global economy saw weakest quarter since 2012. The JPMorgan Global PMI held steady at 51.1 in June, rounding off the weakest quarter since 2012, according to Markit, which compiles the PMI data. Emerging markets remained in an overall state of stagnation, continuing the trend seen over much of the past year, negatively impacting demand growth for commodities.

- The worst performing sector for the week was the S&P 500 Oil & Gas Refiners Index. The index dropped 6.7 percent for the week as gasoline oversupply dimmed the outlook for refiners’ profits during the summer travel season.

- The worst performing stock for the week in the S&P Global Natural Resources Index was Fibria Celulose SA. The Brazilian pulp and paper producer dropped 9.8 percent for the week as the Brazilian currency continued its four-month-long rise against the dollar, which negatively impacted the company’s cost structure.

Opportunities

- U.S. crude oil production continued to edge down, helping rebalance global market. The U.S. Department of Energy data shows crude oil production in the country plunged by 2.25 percent last week, marking the single largest weekly drop since September 2013. U.S. crude oil production is sitting at 8.4 million barrels per day, having dropped more than 12 percent from its 2015 highs.

- India’s largest refiner plans a $6 billion expansion to meet growing demand. Indian Oil Corp. will boost capacity by almost 30 percent in the next six years to feed the booming fuel demand in the country. India is poised to surpass Japan as the world’s third-largest oil user this year and will be the fastest-growing crude consumer in the world through 2040, according to a Bloomberg article citing International Energy Agency estimates.

- China will take additional measures to address coal and steel oversupply. China has threatened to punish regional governments for failing to close unneeded coal mines and steel mills, adding pressure to carry out reforms that aim to eliminate as much as 500 million tons of coal production capacity, and cut as much as 150 million tons of steel making capacity by 2020.

Threats

- Oil prices won’t rise further, according to the world’s biggest independent oil trader. Ian Taylor, CEO of Vitol Group, the world’s largest independent oil-trading house, believes that prices are unlikely to rise much further over the next 18 months as demand growth slows and refiners comfortably meet gasoline consumption.

- Weaker gasoline margins may spur a crude sell-off. Just off the 4th July holiday, when a record number of people fill up the tank to hit the road, it has become evident that we are in the midst of a gasoline glut. Crack spreads, which drive profitability for refiners, have been dropping since the spring, and are sitting at less than half the values seen at this time last year. The threat for crude prices lies in the fact that current levels encourage refiners to dial back runs, reducing demand for crude oil at the busiest time of the year.

- China’s steel demand weakens further. The UBS China steel team research suggests lower steel production and higher inventory in mid-June all point to demand further weakening. As a matter of fact, the June Steel PMI for China dropped back below 50 points, implying that the sharp rebound in the spring was short lived and has not carried over to the summer.

China Region

Strengths

- BYD Electronic International was the Hang Seng Composite Index’s (HSCI) top gainer for the week, rising nearly 19 percent in the last five trading days to break out to new multi-month highs, helped at least in part by a rosier outlook for Samsung.

- June Caixin China Services PMI (purchasing managers’ index) came in at 52.7, better than May’s 51.2.

- China’s Foreign Exchange Reserves for the June period came in better than expected, rising to just under $3.21 trillion and beating an anticipated print of just under $3.17 trillion.

Weaknesses

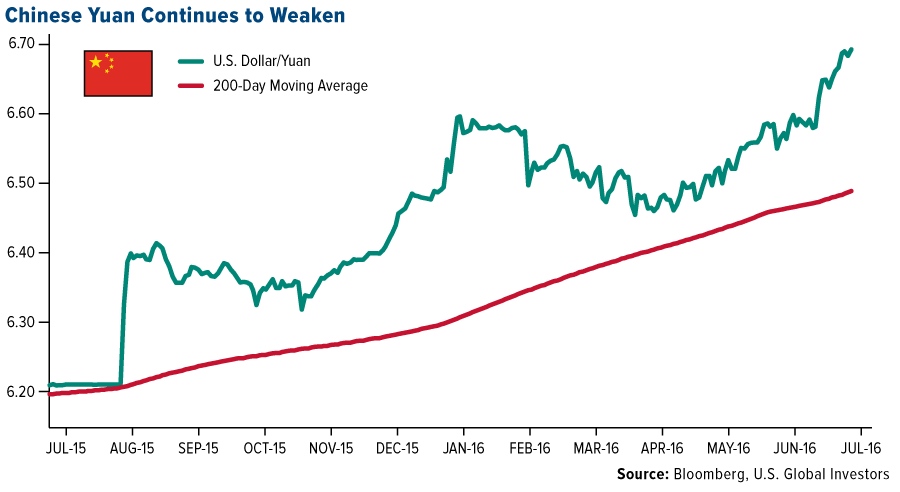

- The Chinese yuan weakened once again this week to new 52-week lows above 6.69.

- West China Cement was the worst performer in the HSCI this week, losing almost a third of its value after the collapse of its planned takeover by Anhui Conch, China’s second-largest cement producer. This resulted in downgrades and reductions in earnings per share (EPS) and credit outlook.

- Singapore’s official Manufacturing PMI missed expectations of 49.8, coming in slightly lower at 49.6 and down from the previous print of 49.8. The Nikkei Singapore Whole Economy PMI, however, remains higher, coming in at a strong 52.3, up from a previous print of 50.1.

Opportunities

- Despite the Brexit hullabaloo, the U.K. will seek closer trade ties with China, according to Reuters. Chancellor of the Exchequer George Osborne met this week with several senior Chinese officials in London.

- Over the next week, investors seeking further information about the state of the Chinese economy will get a slew of data, including consumer price index (CPI), producer price index (PPI), new yuan loans and aggregate financing, money supply, import/export and trade balance data, retail sales, fixed asset investment (FAI) and second quarter GDP. Surveys anticipate a 6.6 percent year-over-year print.

- Both Guangzhou Automobile Group and Geely Automobile Holdings reported upbeat sales numbers for June (27 percent and 41 percent, respectively), as growth in Chinese auto sales continues to climb.

Threats

- While China’s FX Reserves data were better than anticipated this month, some investors worry that perhaps this merely signals that the People’s Bank of China (PBOC) has ceased intervening as extensively in the market at this point, and that any significant pickup in intervention could trigger the rapid resumption of a downtrend in reserves.

- Credit Suisse lowered its targets for the Hang Seng and Hang Sang Chine Enterprise Indices this week, indicating that a second quarter GDP print below 6.5 percent might spell trouble for shares.

- Taiwanese markets were closed Friday because of a typhoon, the first major one of the season.

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 2.65 percent.

- The Turkish lira was the best currency this week, gaining 31 basis points against the dollar.

- The health care sector was the best performing sector among Eastern European markets this week.

Weaknesses

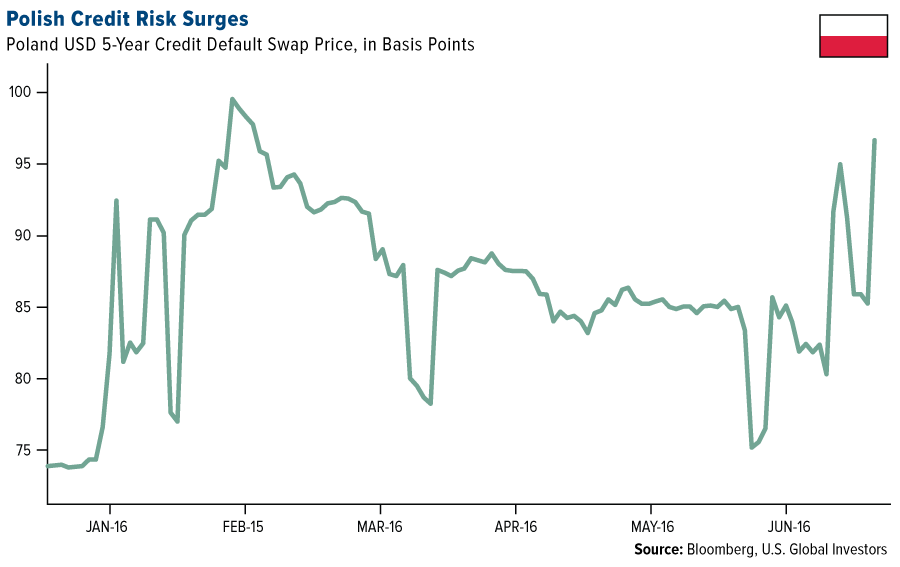

- Poland was the worst performing country this week, losing 1.63 percent.

- The Polish zloty was the worst currency this week, losing 80 basis points against the dollar.

- The utility sector was the worst performing sector among Eastern European markets this week.

Opportunities

- The Bank of England (BOE) agreed to lower capital requirements for U.K. banks in a move that should allow then to lend an extra GBP150 billion ($199 billion) to U.K. businesses and households. The countercyclical capital buffer for banks was reduced to zero, reversing a decision in March to raise the requirement to 0.5 percent. Lee Hardman, a strategist at Bank of Tokyo-Mitsubishi UFJ LTD in London, said that halting the buffer would have no immediate practical impact on banks’ balance sheets as the BOE only told banks in March that they would have to start building extra capital from March 29, 2017, but it provides an important signal showing that the BOE is willing to support credit conditions in a weaker economic environment.

- HSBC economists improved next year’s gross domestic product outlook for Russia from 1 percent to 1.5 percent. The recovery will be mainly consumption-led as labour market tightness and strong corporate profits feed through into gains in real and nominal wages. Last year’s Russian GDP contracted by almost 4 percent. This year activity should strengthen in the second half, leaving the economy flat for the year.

- The International Monetary Fund (IMF) forecasts that the Polish GDP will accelerate from 3.5 percent in 2016 to 3.7 percent next year on the back of strong private consumption supported by new child benefits.

- Both Poland’s and Hungary’s central banks left rates unchanged at record low rates of 1.5 percent and 0.9 percent respectively. Current interest-rate levels help keep Poland’s economy on a path of balanced growth and maintain macro-economic stability, the central bank’s Monetary Policy Council said in statement on Wednesday.

Threats

- The cost of protecting Polish debt against the default climbed the most in three years, rising to the highest level since February, a day after the government announced a plan for pension plan reform. Existing assets in domestic equities (103 billion PLN) will remain with private asset managers while foreign equites, bonds and cash (35 billion PLN) will be transferred to the Demographic Reserve Fund, a state fund which was set up to cut public debt.

- The eurozone services sector PMI increased to a final 52.8 for June from the flash reading of 52.4 previously and an expected reading of 52.5. This was still slightly lower than the May reading while the overall composite reading was unchanged for the month at 53.1 despite a stronger manufacturing release. Growth in the services sector overall was at the slowest pace for close to 18 months with expansion held back by a weaker figure for Germany and contraction in France.

- The Czech President, Milos Zeman, called for a referendum on the country’s membership in the European Union and NATO, adding to concern that more European countries will copy Britain’s Brexit vote. The Prime Minister of Hungary, Viktor Orban, scheduled a referendum on whether the European Union should be able to order the mandatory settlement of non-Hungarian citizens in Hungary without parliament’s consent.

- The Russian Finance Ministry 2017-2019 budget forecasts submitted for the government’s consideration on July 7 calls for faster spending of the reserve fund as well as actual liquidation of the National Wealth Fund. Domestic borrowing planned by the finance ministry will increase the state debt to about 13 percent GDP by 2020. Russia is already running its widest deficit since 2010 this year, with public finances under pressure after the crash in oil.

- The shares of Russia’s biggest telecommunications companies fell on Thursday after President Vladimir Putin signed an anti-terror law that may cost carriers $31 billion to implement. The law will compel carriers to keep recordings of users’ phone calls and internet activity for six months.

- Polish parliament’s lower house passed a new law in the top court on Thursday. Poland is falling out with allies in Brussels and Washington amid concerns it is undermining rule of law by passing legislation to overhaul the media and the country’s Constitutional Tribunal. U.S. President Barack Obama urged all parties in Poland to work together to sustain Poland’s democratic institutions. The European Commission started an unprecedented check into member states’ democratic standards following an overhaul of the tribunal. This law still requires approval of the upper house and President Andrzej Duda to become binding.

- German industrial production fell 1.3 percent month-over-month in May, well short of the consensus forecast of a 0.1 percent gain. The slowdown in Germany suggests that the headwinds from a global economic slowdown and political uncertainty in Europe will weigh on other countries in the eurozone as well. Hungary’s May industrial production fell 0.7 percent month-over-month in May vs. a 5.5 percent increase in April.

(c) US Global Investors