A couple of week’s ago I discussed the importance of understanding the difference between compounded annualized returns and real annualized returns. To wit:

“The ‘power of compounding’ ONLY WORKS when you do not lose money. As shown, after three straight years of 10% returns, a drawdown of just 10% cuts the average annual compound growth rate by 50%. Furthermore, it then requires a 30% return to regain the average rate of return required. In reality, chasing returns is much less important to your long-term investment success than most believe.

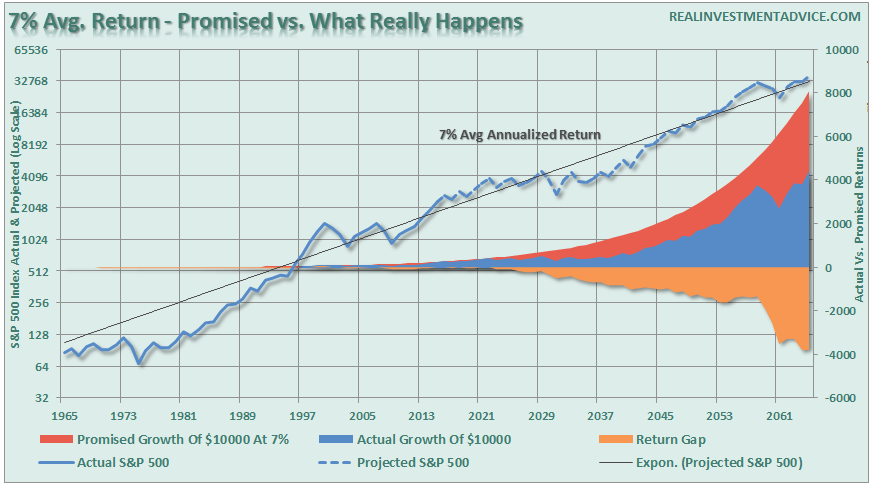

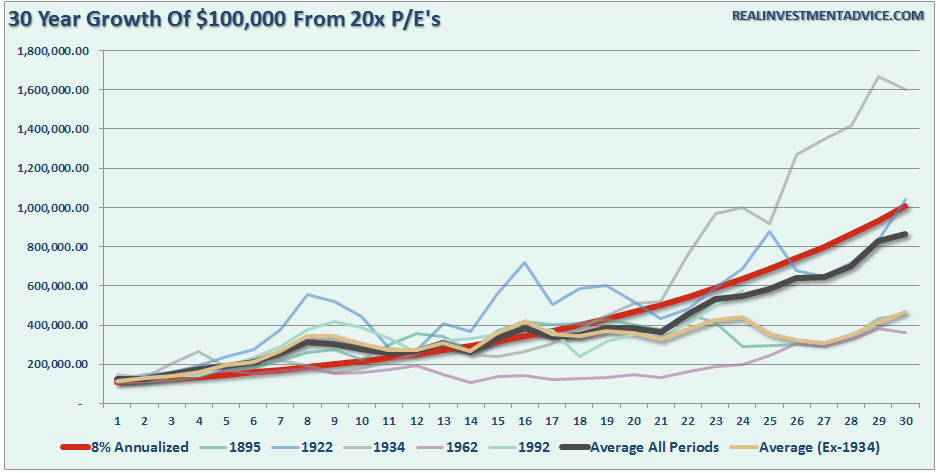

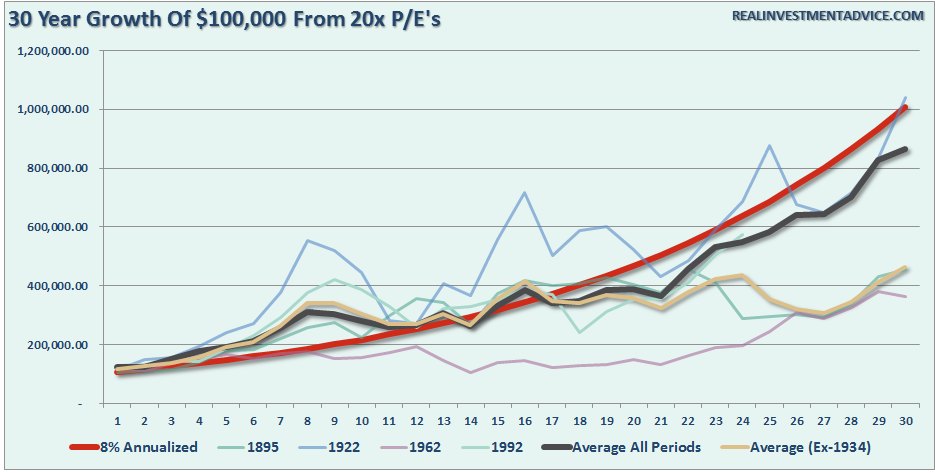

Here is another way to view the difference between what was ‘promised,’ versus what ‘actually’ happened. The chart below takes the average rate of return, and price volatility, of the markets from the 1960’s to present and extrapolates those returns into the future.”

“When imputing volatility into returns, the differential between what investors were promised (and this is a huge flaw in financial planning) and what actually happened to their money is substantial over the long-term.

The second point, and probably most important, is that YOU DIED long before you realized the long-term average rate of return.”

The reason I remind you of this tidbit is due to a very good article recently by Michael Kitces discussing the withdrawal rate in retirement (Why Most Retirees Will Never Draw Down Their Retirement Portfolio.) The whole article is very good and worth your reading, however, I want to expand on the following:

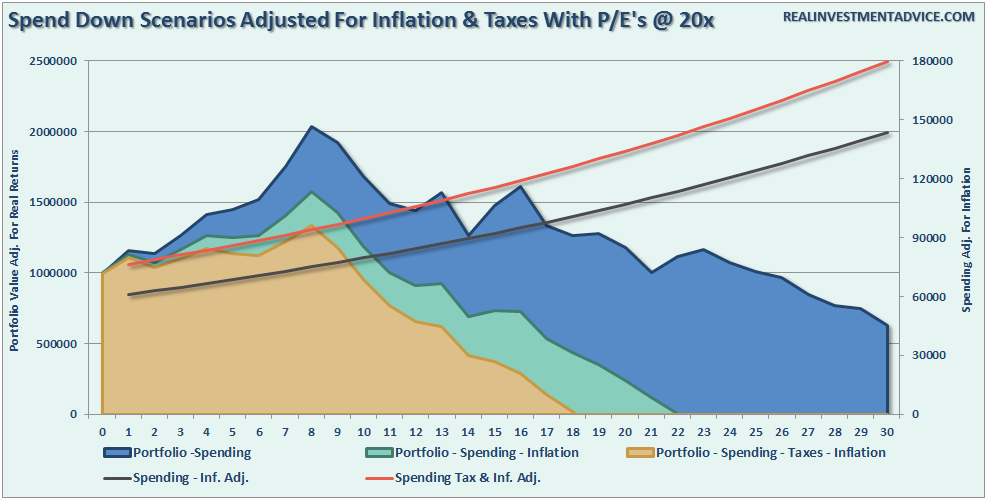

“Given the impact of inflation, it’s problematic to start digging into retirement principal immediately at the start of retirement, given that inflation-adjusted spending needs could quadruple by the end of retirement (at a 5% inflation rate). Accordingly, the reality is that to sustain a multi-decade retirement with rising spending needs due to inflation, it’s necessary to spend less than the growth/income in the early years, just to build enough of a cushion to handle the necessary higher withdrawals later!

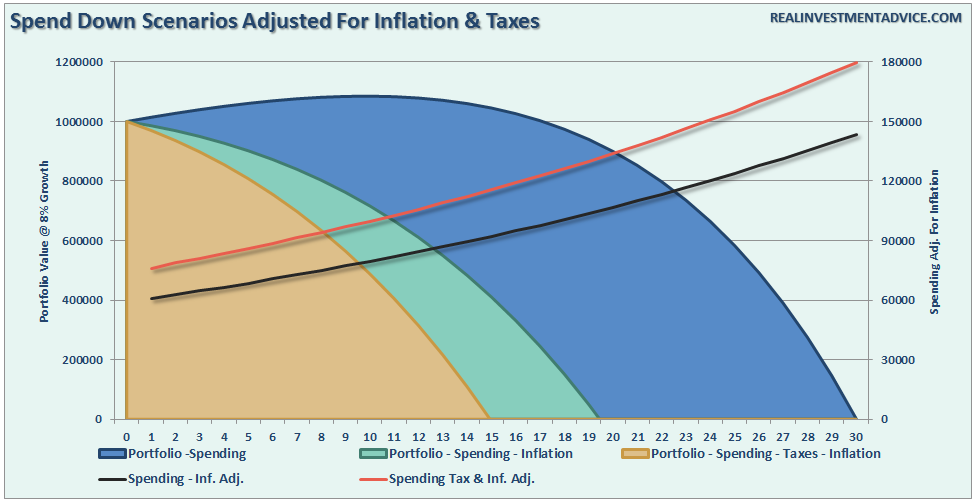

The chart below takes the average of all periods above (black line) and uses those returns to calculate the spend down of retiree’s in retirement assuming similar outcomes for the markets over the next 30-years. As above, I have calculated the spend down structure to include inflation and taxation.

As you can see, under this scenario, due to the skew of 1934 and front-loaded returns, the retiree would not have run out of money over the subsequent 30-year period. However, once the impact of inflation and taxes are included, the outcome becomes substantially worse.

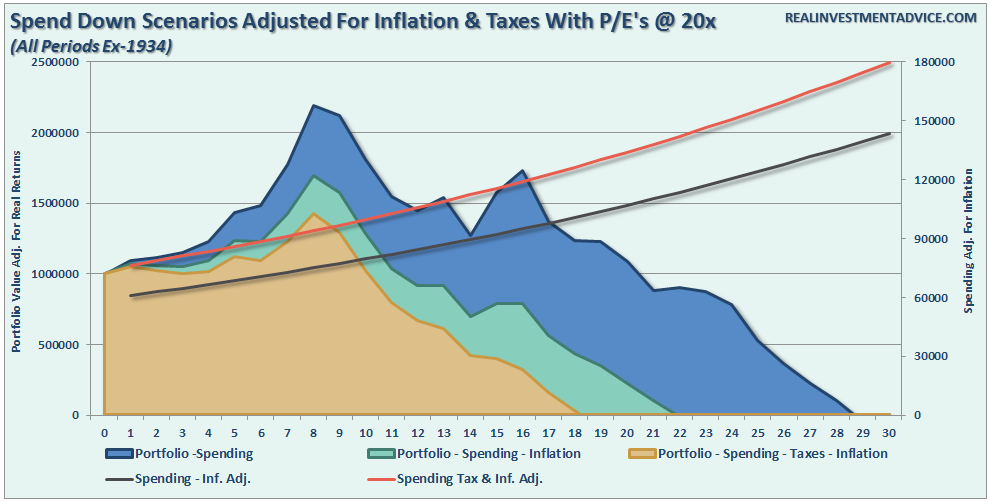

The chart below shows the same as above but with the 1934 period excluded. The outcome, not surprisingly, is not substantially different with the exception of the retiree running out of money one-year short of their goal rather than leaving an excess to heirs.

Important Considerations For Retiree Portfolios

The analysis above reveals the important points individuals should consider given current valuation levels and a Fed-driven bull market advance over the last 8-years:

- Expectations for future returns and withdrawal rates should be downwardly adjusted.

- The potential for front-loaded returns going forward is unlikely.

- The impact of taxation must be considered in the planned withdrawal rate.

- Future inflation expectations must be carefully considered.

- Drawdowns from portfolios during declining market environments accelerates the principal bleed. Plans should be made during up years to harbor capital for reduced portfolio withdrawals during adverse market conditions.

- The yield chase over the last 8-years, and low interest rate environment, has created an extremely risky environment for retirement income planning. Caution is advised.

- Expectations for compounded annual rates of returns should be dismissed in lieu of plans for variable rates of future returns.

As Michael concludes:

He is absolutely correct. In this Central Bank driven world, with debt levels rising globally, interest rates near zero, economic growth weak with a potential for a recession, and valuations high, the uncertainty of a retirement future has risen markedly. This lends itself to the problem of individuals having to spend a bulk of their “retirement” continuing to work.

Of course, this could be why 90% of the jobs in the latest BLS employment report went to individuals over the age of 55. Then there is also the tiny fact the majority of American’s don’t have $1 million for retirement but actually, most have less than $250,000. This is another problem in, and of, itself.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“.

© Real Investment Advice

© Real Investment Advice

Read more commentaries by Real Investment Advice