Last week, the United States celebrated 240 years of independence from the United Kingdom. While relations after the separation were initially complicated, the two countries have grown to become close allies.

Economic linkages between the United States and the United Kingdom have also grown significantly over time. And so, when the results of the Brexit referendum became apparent, some wondered whether U.S. economic performance would be at risk. The answer, for now, seems to be no. Our outlook for American growth is little changed from last month, although we have revisited our expectations for U.S. interest rates.

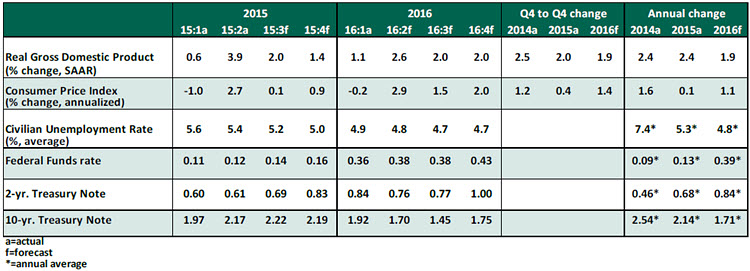

Key Economic Indicators

Key Elements of the Forecast

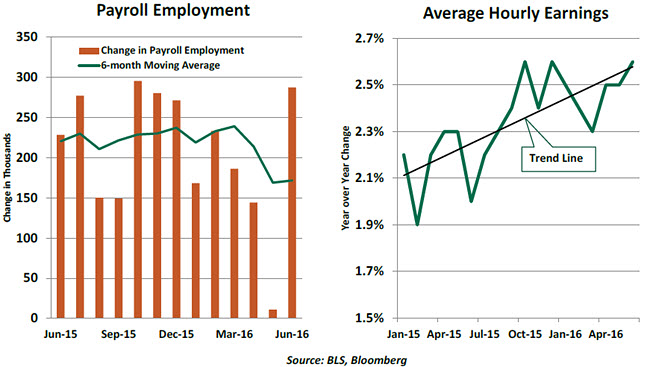

- The outlook for consumer spending remains positive. We anticipate a gain in real consumption of 3.3% in the second quarter, followed by progress at a slightly more moderate pace during the balance of this year. The employment situation has provided key support.

The June employment report was a welcome antidote to its predecessor. Payrolls expanded by 287,000, up from just 11,000 the prior month. (We should note that striking Verizon workers took 35,000 positions from May’s gain and added them to June.) This restored the sense that the U.S. labor market is continuing to progress. Wage gains crept upward last month, boding well for personal income.

Rising energy prices represent a slight dampener to the consumption outlook. As of this writing, regular gasoline costs 33% more than it did in February.

Brexit’s impact on U.S. consumer spending should be very modest. U.S. equity markets reached new record highs in early July, which should sustain positive wealth effects. Barring broader global contagion, the U.S. labor market should retain its positive tone. And low interest rates should help borrowers.

- The outlook for U.K. economic performance has been downgraded significantly, with some forecasters calling for a recession in 2017. In light of this, the U.S. dollar strengthened by more than 10% against the British pound in the weeks after the referendum. The shifting terms of trade would tend to hinder the U.S. balance of payments, but the impact is likely to be small. The dollar’s value against a trade-weighted basket of currencies is virtually unchanged since late June, and exports to the United Kingdom account for less than 6% of total exports and 0.7% of U.S. gross domestic product (GDP).

We have not made any changes to our projections of net exports in the coming quarters. If the uncertainty related to Brexit affects economic performance in other regions, we’ll revisit our expectations.

- The most significant effect of Brexit in the initial weeks after the referendum has been its influence on the path of global interest rates. In the United States, the benchmark 10-year Treasury yield is almost 40 basis points lower than it was prior to the balloting. A global flight to quality is behind the dramatic correction.

Our central expectation is that uncertainty related to Brexit will gradually diminish in the months ahead, and that the ultimate rearrangement between the United Kingdom and the European Union will be a modest correction and not a chasm. If we are correct, risk assets should recover some of the capital lost to fixed income. We anticipate that the 10-year yield will move upward, cautiously, through the balance of the year.

We have updated our expectations for the Federal Reserve. The United States is close to full employment, and inflation is converging on the target of 2%. But international uncertainty stemming from Brexit will likely keep the Fed on hold until December of this year. The cost of waiting, for now, seems far less than the cost of moving pre-emptively. From there, we expect three rate increases in 2017. Of course, that path will depend very much on the course of the data.

As we discussed in last week’s commentary, low rates are not likely to provide much of a boost to U.S. economic activity. We may have reached the point where damage to savers outweighs benefits to debtors.