Summary

- U.S. stocks gained ground in the first half of 2016, but that masks significant volatility, particularly at the beginning and end of the period.

- The second half of the year is chock full of likely market catalysts, including potential Brexit fallout, the upcoming presidential election, Fed meetings and more.

- Against this uncertain backdrop, we continue to believe that equity investors should remain focused and opportunistic.

The first half of 2016 was a wild ride for equity markets. In the end, the S&P 500 Index delivered a total return of 3.84%, but that masks significant volatility, particularly at the beginning and end of the period. The market was down 10.27% through February 11, 2016. From that point on, U.S. stocks returned 15.73%. The final days of June included the highly uncertain “Brexit” vote and the annual rebalancing of the Russell indexes, two volatility-inducing events.

Much of that is now in the rearview mirror, although ongoing fallout from Britain’s vote to leave the EU will likely continue to influence markets in the coming weeks and months. That aside for now, let’s look ahead to the many other catalysts on the calendar for the remainder of 2016.

July 11 – Earnings season kicks off

By tradition, Alcoa is the first company to report earnings each quarter. Banks are also early reporters. As companies in other industries release results, investors will be looking for clues as to the health of the economy. We expect overall earnings for U.S. companies to be broadly in line with consensus forecasts. Investors will likely look most favorably on those companies that deliver strong revenue growth, not simply earnings that are “manufactured” from cost cutting and stock buybacks.

There will likely be a number of companies that are forced to lower earnings guidance for the second half of 2016, as soft trends fail to support the acceleration that is currently imbedded in numbers. At around midyear, the consensus EPS forecast for the S&P 500 was $122, representing 9% year-over-year growth. We could see that forecast fall to a level that would imply growth of around 5%.

July 18-21 – Republican National Convention in Cleveland

This year, the Republican National Convention is likely to be more contentious than usual. As of this writing, there was continued speculation about a potential contested convention. The decisions of the rules committee at the start of the convention, the party platform, the choice of vice presidential candidate, and the tone and content of the prime-time speeches will all have an impact on how the convention is perceived by voters and investors.

July 25-28 – Democratic National Convention in Philadelphia

During the primary season, conventional wisdom was that the Republican convention might be contentious, while the Democratic one would be straightforward. However, with the strong showing of Bernie Sanders, it will be interesting to see how much voice is given to his supporters and their priorities. Health care and financials are two sectors that might experience volatility, depending on what is emphasized at the convention. Also, during the convention, the Fed will meet and make a decision on interest rates.

August

August should be relatively quiet, as investors take vacation and turn their attention to the Olympics in Brazil. That being said, if there is an unexpected exogenous event, light trading volumes may exacerbate volatility, as happened in August 2015 (when China surprised markets by devaluing the yuan, leading to a global market sell-off).

September

September is likely to be a busy month. Post-Labor Day is when many voters will begin to pay close attention to the presidential election. Having skipped August, the Fed will meet again on September 21 to make a decision on rates. There are also a large number of industry conferences, where company management teams will give updates on their businesses. One of these, the “Back to School” conference, held each year in Boston, involves the largest consumer companies.

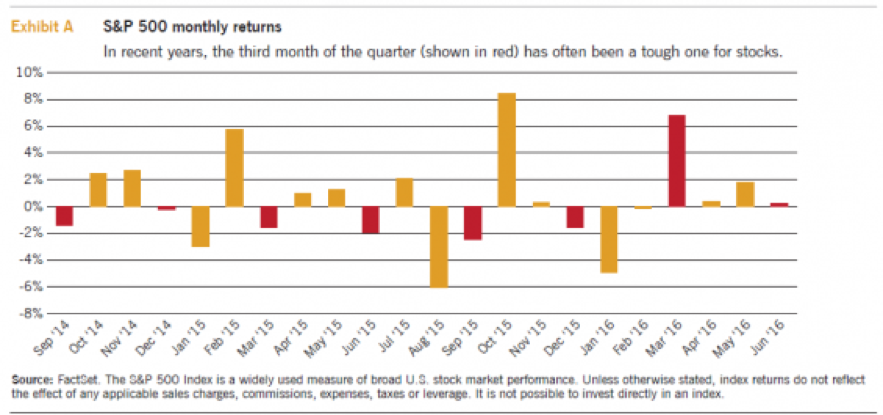

September is also important in that it is the third month of the quarter. Many companies have “blackout” periods in the final weeks of each quarter and into the early part of the next quarter, when they report earnings. During these blackout periods, companies suspend their share buyback programs in order to avoid accusations of trading on material, nonpublic information. Given how important corporate buybacks have become to the market, this temporary removal of demand for equities has coincided with several of the market’s pullbacks in the past two years (Exhibit A).

October

Like July, October is a busy month for corporate earnings releases. With three quarters of the year complete, companies and investors will begin to think about 2017 and the trajectory of earnings into the approaching year. We will likely have a presidential debate in October, perhaps the only debate of this cycle. Television ratings may well set records.

November 8 – Election Day

At the November 2 Fed meeting, Janet Yellen and her colleagues are likely to take no action in order to avoid roiling markets six days prior to Election Day. We expect the market to be focused on the election throughout the summer and into autumn. If the likely result appears clear, Election Day may not produce much of a market reaction. Regardless of who wins the presidency, the equity market may prefer to see the same party capture the House of Representatives and the Senate. The reasoning would be that a new president will be more effective if he/she has the support of Congress.

Under either party, increased fiscal stimulus in 2017 seems likely. This could include corporate tax reform (lowering rates, reducing deductions and encouraging companies to repatriate overseas cash) and an infrastructure spending bill. If modest regulatory relief is also part of the agenda, then the economic outlook for 2017 may be stronger than many currently believe.

November 30 – OPEC meeting in Vienna

OPEC typically meets twice a year, with its next meeting to be held six days after Thanksgiving. At its November 2014 meeting, OPEC surprised global oil markets by maintaining an elevated level of production, which exacerbated the already-falling price of crude. We expect supply and demand to continue to rebalance between now and the end of 2016. A production cut at the November meeting would be supportive of oil prices, but is unlikely, in our view.

December 14 – Final Fed meeting of 2016

In December 2015, the Fed raised the federal funds rate by 0.25%, which led, in part, to market volatility in early 2016. The expectation at the beginning of 2016 was that the Fed had embarked on a path to normalize the level of interest rates. In the first half of the year, however, the Fed failed to follow through with further rate increases. The market has begun to doubt the Fed’s will: At around midyear, the implied probability of a rate increase on or before the December 14 meeting stood at less than 11%.

December is also the month when many investors choose to conduct tax loss harvesting, selling losers in their portfolios to take advantage of the tax benefit that comes from booking the loss before the end of the year. This activity sometimes puts further pressure on stocks that have performed poorly earlier in the year.

Stay focused and opportunistic

The second half of 2016 is full of potential catalysts – including not only the specter of further Brexit turmoil, but also Fed meetings, a presidential election, corporate earnings and incoming economic data. There will likely be a few surprises along the way. In our equity portfolios at Eaton Vance, we are staying focused on the long-term prospects of our holdings and will look to take advantage of any opportunities thrown our way by the uncertainty of these events.

About Risk

Investments in equity securities are sensitive to stock market volatility. Equity investing involves risk, including possible loss of principal. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging countries, these risks may be more significant.

Past performance is no guarantee of future results.

The views expressed in this Insight are those of Edward J. Perkin and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

Not FDIC Insured • Not Bank Guaranteed • May Lose Value ©2016 Eaton Vance Distributors, Inc. • Member FINRA/SIPC Two International Place, Boston, MA 02110 • 800.836.2414 • eatonvance.com