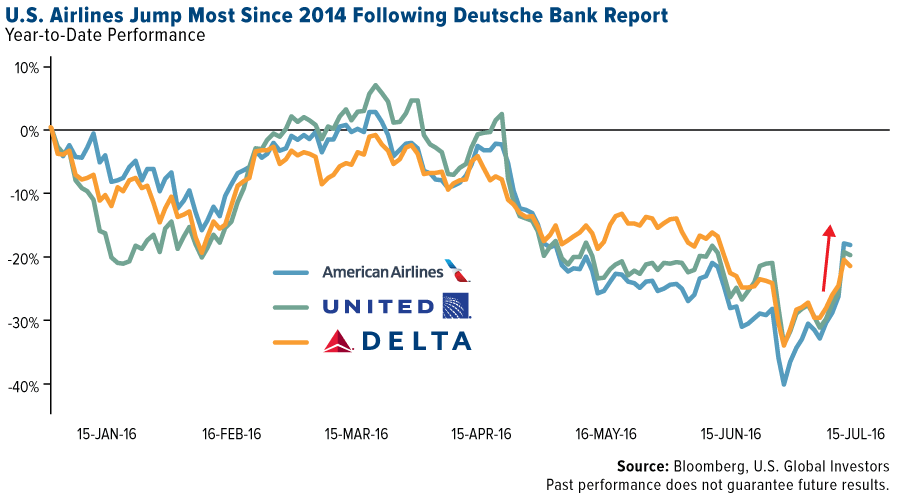

Is this the Airlines Liftoff Investors Have Been Waiting For?

A flurry of good news lifted airline stocks higher this week, reversing a drop in altitude that’s weighed on the industry so far in 2016. Fueled primarily by a bullish report from Deutsche Bank, American Airlines, Delta Air Lines and United Continental collectively advanced 6.5 percent on Tuesday alone. The German bank’s all-clear signal halted a six-month slide on overcapacity, Brexit uncertainty and heightened fears of global terrorism.

(Speaking of which, I’m very saddened to hear of the heinous and cowardly attack in Nice this week, during Bastille Day celebrations no less. Just last month I was in the southern French city with friends. It’s easy to see why it stands as a perennial vacation spot, rich with culture, beautiful architecture and promenades, a warm climate and welcoming people.)

Leading the group was American Airlines, which announced Tuesday that it would renew its credit card deals with both Citigroup and Barclays, a move that’s estimated to add $1.55 billion to the carrier’s pretax income over the next three years—$200 million this year, $550 million in 2017 and $800 million in 2018.

The agreement will allow Citi to offer its credit cards to new customers on American Airlines’ website and mobile apps, through direct mail and in Admirals Club lounges, while Barclaycard will be permitted to reach customers in airports and during American flights.

Investors also rewarded Delta for better-than-expected profits, which rose 4.1 percent to $1.55 billion in the second quarter. In an effort to push up fares, the number two carrier announced plans that it would cut capacity on U.S.-U.K. flights due to British pound weakness following Brexit.

Playing the Long Game with Near-Term Results

Looking ahead, aircraft-makers Boeing and Airbus both see huge growth in deliveries as the global middle class continues to swell in rank. In its Current Market Outlook, Boeing projects total demand for nearly 40,000 new jets over the next 20 years—a 4 percent increase over last year’s forecast—with a large percentage of the growth occurring in Asia. Altogether, these deals are valued at a monumental $5.9 trillion.

Airbus’ forecast, while somewhat more conservative, is no less impressive. The French airline manufacturer sees demand for more than 33,000 new aircrafts between now and 2035, all with a market value of $5.2 trillion.

The lion’s share of this expansion is expected to take place in emerging and developing countries such as India and China, where middle class growth is booming. Higher incomes should heat up flight demand and help air traffic double over the next 15 years, according to Airbus. In India alone, air traffic is expected to accelerate fivefold between now and 2035. The Federal Aviation Administration (FAA) sees the number of global revenue passenger miles rising from 877 billion in 2015 to 1.02 trillion in 2024.

In the near term, domestic airlines continue to trade at extremely low multiples compared to other stocks in the industrials sector. Compare airlines’ price-to-earnings (P/E) ratios to transportation stocks and the broader stock market. Whereas American is trading at a little over 4 times earnings, transportation stocks—which include trucks, railroads and other industrials—trade at more than 14 times earnings. The S&P 500 Index, meanwhile, currently trades at more than 20 times earnings.

| American Airlines | 4.15 | |

| United Continental | 4.11 | |

| Delta Airlines | 7.1 | |

| Southwest Airlines | 11.53 | |

| S&P Transportation Select Industry Index | 14.06 | |

| S&P 500 Index | 20.06 |

Domestic carriers also continue to return money to shareholders in the form of dividends and stock buyback programs. American, for example, repurchased more than 50 million shares, worth $1.7 billion, in the second quarter. As of March, Southwest Airlines had a phenomenal three-year dividend growth rate of 101.2 percent, according to GuruFocus data. This helps support the thesis that the industry offers many attractive buying opportunities right now.

How Regulations Have Hurt Retail Investors

In past weeks and months, I’ve written about how excessive regulations are atrophying global economic growth. Granted, regulations are often well intentioned and necessary to create a level playing field. But when they grow too large in number and scope, it’s a little like having more referees than players on the basketball court.

Here in the U.S., federal regulations cost U.S. businesses more than $1.88 trillion a year. If they were their own economy, American regulations would be the ninth largest in the world, just ahead of Russia. Small businesses, which are responsible for more than half of all U.S. sales and employ 55 percent of all American workers, increasingly rank regulations as one of the top challenges facing their growth and survival.

This isn’t just an American phenomenon, of course. Last month, Brits voted to leave the European Union largely because they recognize overzealous regulation and envy policies as impediments to innovation. They’re tired of falling behind. Why else did the European Commission recently require American tech giants Netflix and Amazon to guarantee that at least 20 percent of their streaming video content is shot in Europe? Were EU rules not so corrosive to innovation, the continent might have its own Silicon Valley and its own Netflix (and, I might add, more attractive tax incentives to produce movies and TV shows in their countries).

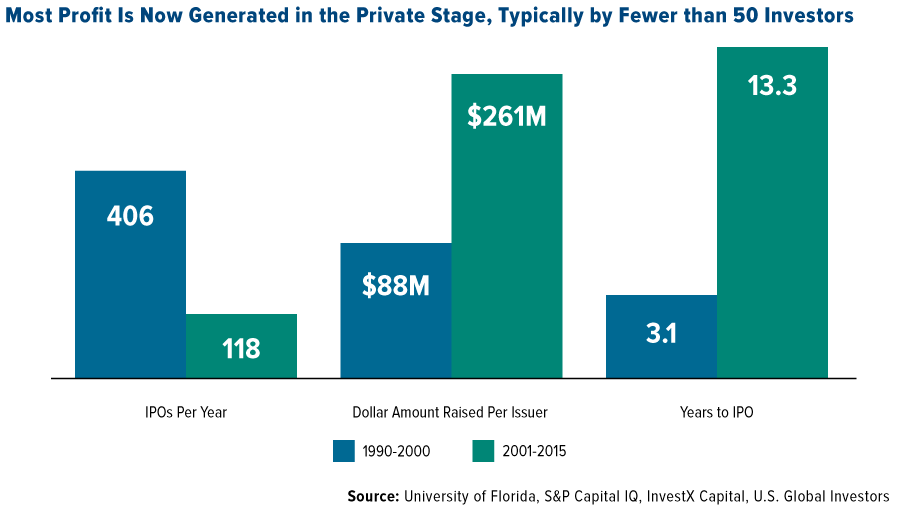

Now, thanks to a slide deck from InvestX Financial CEO Marcus New, it’s clear just how detrimental U.S. regulations have been in the formation of capital. In the years preceding 2001, we could have expected to see 100 new companies on average go public every quarter. Since then, that number has fallen to around 30. Because of the mounting risks involved, the gestation period leading up to an IPO has ballooned from three years to more than 13 years, with an average $261 million raised per issuer, compared to $88 million between 1990 and 2001.

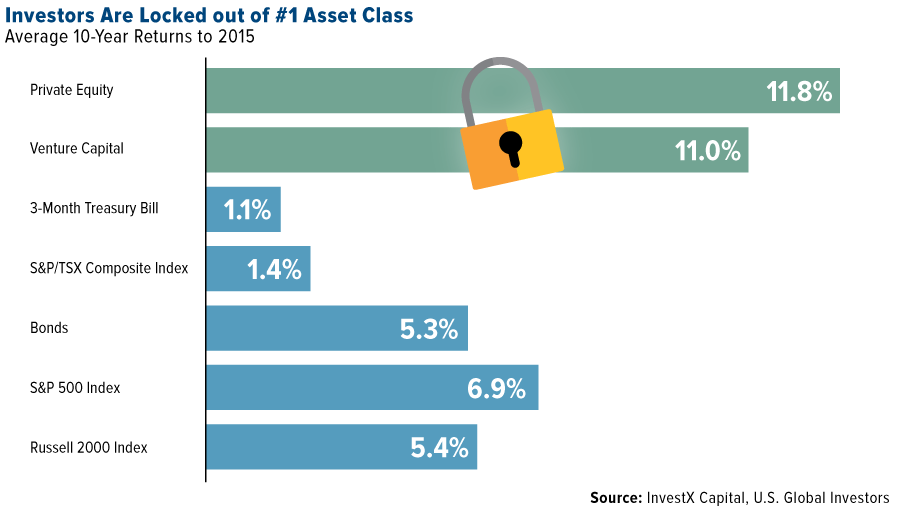

Also because of regulations, smaller retail investors have effectively been blocked from participating in higher-yielding investments—namely, private equity and venture capital, whose 10-year compound annual growth rates have averaged 11.8 and 11 percent, quite a bit more than Treasuries, equities and other common asset classes.

For the most part, only accredited investors—those who have earned income that exceeds $200,000 or a net worth of over $1 million—are permitted to participate. As a result, it’s only the rich who get, well, richer.

Again, these rules are well intentioned. The justification is that everyday investors should be protected from the heightened risks involved in more sophisticated assets. At the same time, many people are being restricted from opportunities that might help them move up the socioeconomic ladder—opportunities that are open only to those who’ve already “made it.”

It seems, then, that the Occupy Movement and other class warriors who criticize and bash the 1 percent for “stealing all the wealth” would do well to direct some of their ire at the socialist rules responsible for restricting their social mobility.

Personal finance and investing are among the many topics discussed this week at FreedomFest, “the largest gathering of free minds,” which I regrettably couldn’t attend this year. FreedomFest was founded in 2002 by my friend Mark Skousen, then-president of the Foundation for Economic Education and author of several books, including one of my favorites, The Big Three in Economics: Adam Smith, Karl Marx and John Maynard Keynes. I highly recommend you check it out.

Keep Munis Tax-Free

You might be aware of the debate happening right now on whether to lift the tax exemption on municipal bonds. Just today, Municipal Bonds for America (MBFA) sent a letter to Speaker of the House Paul Ryan to affirm its opposition “to any legislative proposal that taxes, in whole or in part, municipal bonds.”

Tax-free munis, as the coalition points out, have long been responsible for funding public infrastructure projects, from schools to highways to airports to seaports.

Part of munis’ appeal as an investment is that they are tax-free at the federal level and often the state and local levels. Removing the exemption could dramatically limit their attractiveness, which would ultimately affect America’s ability to maintain livable communities.

But here’s why I believe it won’t happen. Both major candidates for president, Donald Trump and Hillary Clinton, strongly support increasing infrastructure spending. In fact, it’s the one thing they have in common with each other. I don’t believe either President Trump or President Clinton would be in favor of allowing munis to be taxed, thereby risking financing for new projects.

A Brokered Democratic Convention?

|

In closing, it might seem like a done deal that Hillary and Trump will be our nominees. After all, just this week Senator Bernie Sanders finally threw in the towel, endorsing his Democratic rival.

But don’t count Sanders out just yet, especially now that the investigation into Hillary’s private email server has bruised her poll numbers. There’s historical precedence for a contested convention. In 1932, Franklin Roosevelt—who, like Sanders, was considered by many to be too far left to win the general election—failed to garner the necessary two-thirds majority of delegates. He was even rumored to have endorsed his rival, Governor Al Smith. And yet, Roosevelt brokered a deal at the convention that won him his party’s nomination and, eventually, the presidency.

Will history repeat itself? Could Sanders attempt to do the same? We’ll find out soon enough.

With political uncertainty high, and with fiscal and monetary policies imbalanced, gold remains an attractive asset class. As always, I suggest a 10 percent weighting in gold bullion and gold stocks, with a rebalance either quarterly or annually.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.04 percent. The S&P 500 Stock Index rose 1.49 percent, while the Nasdaq Composite climbed 1.47 percent. The Russell 2000 small capitalization index gained 2.37 percent this week

- The Hang Seng Composite gained 4.77 percent this week; while Taiwan was up 3.58 percent and the KOSPI rose 2.76 percent.

- The 10-year Treasury bond yield rose 19 basis points to 1.55 percent.

Domestic Equity Market

Strengths

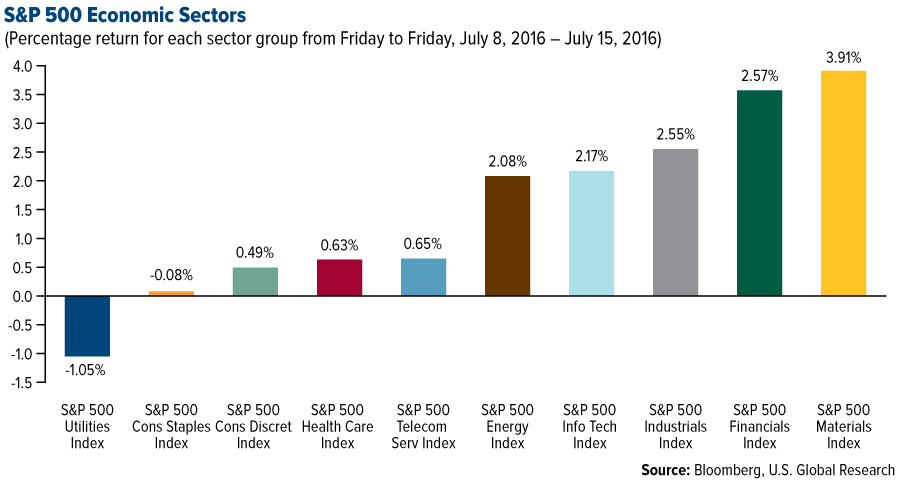

- Materials was the best performing sector for the week, increasing 3.91 percent compared to an overall increase of 1.49 percent for the S&P 500 Index.

- Seagate Technology was the best performing stock for the week, increasing 20.37 percent. The data-storage solutions company announced an ambitious restructuring plan and preliminary fiscal fourth-quarter 2016 results that topped expectations.

- Line exploded in its trading debut. The Japanese mobile-messaging app surged as much as 30 percent in its trading debut before finishing up 26.5 percent at $41.55 a share. Line raised more than $1 billion in its initial public offering as it became just the fifth tech company to go public this year. The stock trades on the New York Stock Exchange under the ticker LN.

Weaknesses

- Utilities was the worst performing sector for the week, falling negative 1.05 percent compared to an overall increase of 1.49 percent for the S&P 500.

- Fastenal was the worst performing stock for the week, falling negative 3.94 percent. The company posted fiscal second quarter results that missed expectations and had its price target cut by BMO Capital.

- Short seller Andrew Left is back to shorting Valeant. According to an interview with James Passeri at The Street, Left has entered into a short position against the troubled pharmaceutical company that he helped bring down last October.

Opportunities

- According to BCA, the current environment contains plenty of fundamental supports for gold. They include the trade-weighted dollar having trouble breaking out, a falling opportunity cost of holding gold and an equity risk premium that has upside, which historically tends to be correlated with higher gold prices. Thus, gold and gold equities seem to have enough support to sustain their momentum.

- U.S. bond yields are testing multi-decade lows as a consequence of global deflationary forces and unorthodox monetary policy abroad. This is a welcome assist to the U.S. housing market, as these exogenous factors have pushed down the U.S. 30-year mortgage rate, providing an incentive for consumers to reenter the housing market. With the ratio of new home sales expectations versus new home inventories rising, homebuilders look poised to outperform.

- Credit card interest rate spreads have widened in recent weeks, diverging from the overall yield curve and signaling that historically cheap relative valuations are not sustainable. Importantly, consumer income expectations have perked up on the back of labor market tightness, suggesting that revolving consumer credit will continue to grow. These are positive signs for consumer finance stocks.

Threats

- In a note on Tuesday, Alan Ruskin, global head of G10 FX strategy at Deutsche Bank, identified six issues that investors had about the economy that seem to be correlated with the latest stock surge, including June's strong jobs report and the fact that the People's Bank of China's "stealth devaluation" of the yuan did not result in crazy market turmoil. But in the same note, he wonders how long this can last. "Something has to give—either the risk rally is hopelessly misplaced or Fed rate expectations are," Ruskin said.

- An increase in the federally mandated minimum wage would result in a small boost to the trend in wage growth. The leisure and hospitality industry, where about 15 percent of workers are paid at or below the floor, would feel the impact the most.

- The short-covering bounce in many deep cyclical sectors is reversing, and persistent weakness warns that downside risks remain intact.

![[thumb]](/images/content_image/data/2b/2b013b131709e7dbdcdcf62b0af72126.jpg)

July 14, 20168 Ways Short-Term Munis Can Make You Scream “Oh Yes!” |

![[thumb]](/images/content_image/data/3d/3d35cda42eb4d1fc960dc9913a9da213.jpg)

July 12, 2016Gold Is Just Getting Warmed Up: UBS Analyst |

![[thumb]](/images/content_image/data/f6/f684f8cea9c0fc5008ded1d3c15e7728.jpg)

July 11, 2016Silver Takes the Gold: Commodities Halftime Report 2016 |

The Economy and Bond Market

Strengths

- Headline retail sales popped up 0.6 percent month-over-month (MoM), and core a similar 0.5 percent. This was well above expectations and a positive sign for the U.S. economy. Industrial production also ramped up 0.6 percent, primarily driven by strong autos.

- The Federal Reserve’s latest outlook on the economy is positive. The Fed was out with its latest Beige Book, a collection of economic anecdotes compiled on or before July 1 from its 12 districts. It highlighted further tightness in the labor market, with "the strongest pressures linked to skilled workers and difficult-to-fill positions." Moreover, the housing market continues to improve, and many districts were upbeat about future conditions, although most of them continue to report tight inventories.

- Producer prices rose more than expected. The producer price index (PPI) for final demand rose by 0.5 percent in June, according to the Labor Department. Economists were expecting a 0.3 percent increase. Meanwhile, the index for final demand goods jumped by 0.8 percent, the most since May 2015, and was led by a 9.9 percent jump in the gas-price index.

Weaknesses

- Dutch 10-year government bond yields dropped below zero for the first time ever, making them the latest to join the negative yield club. Amazingly, there's nearly half a millennium of records to compare that against, as record keeping began in 1517. As a historical reference point, that's the same year that Marin Luther published his 95 Theses. On a global scale, there's roughly $13 trillion of global negative-yielding debt now. By comparison, there was about $11 trillion ahead of the U.K.'s vote on EU referendum.

- Japan lowered its growth and inflation forecasts. The Japanese Cabinet Office lowered its 2016 growth forecast to 0.9 percent from 1.7 percent as a result of the delayed consumption tax hike. Additionally, the government cut its inflation estimate to 0.4 percent from 1.2 percent.

- The University of Michigan consumer sentiment index slipped to 89.5 in the preliminary July report from 93.5, owing largely to weaker expectations.

Opportunities

- Given recent trends, a variety of U.S. housing indicators - NAHB survey on Monday, starts and permits on Tuesday, existing home sales on Thursday – are likely to show continued firmness in residential real estate.

- Brexit has been scheduled. The Evening Standard reported that the British exit from the European Union will occur in December 2018, citing new Brexit Secretary David Davis. "This means that some of the economic benefits of Brexit will materialize even before the probable formal departure from the EU around December 2018," Davis told the Conservative Home website. Davis said that the U.K. could immediately begin making trade deals and that negotiations could take 12 to 24 months.

- High yield and corporate credit spreads have tightened over the past week. If economic data continues to surprise to the upside and the risk-on sentiment in the equity markets hold, we could see a continued rally in credit spreads.

Threats

- The front-runners for the U.S. presidency have tax reform plans that could imply reducing the tax exemption for municipal interest as part of a broader push to cap deductions and exclusions, according to a Morgan Stanley report.

- Expectations for U.S. short-term interest rates have fluctuated widely this year. In January, the market was braced for further Fed rate hikes. However, the early year swoon in financial markets forced the Fed to turn dovish. Once asset prices recovered, the Fed began to prep investors for a rate hike in June. However, the weak May nonfarm payrolls report and the Brexit vote forced the Fed to make another turn. Now that markets have absorbed the results of the U.K. referendum with no lasting negative effects and U.S. data are surprising on the upside, investors should prepare for another hawkish shift from the Fed. This would likely cause a sell-off in the short end of the curve.

- July flash purchasing managers’ index (PMI) data on Friday will provide the first read on the eurozone economy post-Brexit. A disappointment would exacerbate fears about the negative implications of the British exit.

Gold Market

This week spot gold closed at $1,337.50, down $28.88 per ounce, or -2.11 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, slipped 1.78 percent. Junior miners outperformed seniors for the week as the S&P/TSX Venture Index traded up 1.89 percent. The U.S. Trade-Weighted Dollar Index moved higher with a 0.37 percent gain.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Jul-12 |

Germany CPI YoY |

0.3% |

0.3% |

0.3% |

|

Jul-14 |

U.S. Initial Jobless Claims |

265k |

254k |

254k |

|

Jul-14 |

U.S. PPI Final Demand YoY |

-0.1% |

0.3% |

-0.1% |

|

Jul-14 |

China Retail Sales YoY |

9.9% |

10.6% |

10.0% |

|

Jul-15 |

Eurozone CPI Core YoY |

0.9% |

0.9% |

0.9% |

|

Jul-15 |

U.S. CPI YoY |

1.1% |

1.0% |

1.0% |

|

Jul-12 |

Germany ZEW Survey Current Situation |

51.5 |

-- |

54.5 |

|

Jul-14 |

Germany ZEW Survey Expectations |

9.0 |

-- |

19.2 |

|

Jul-14 |

U.S. Housing Starts |

1165k |

-- |

1164k |

|

Jul-15 |

ECB Main Refinancing Rate |

0.000% |

-- |

0.000% |

|

Jul-15 |

U.S. Initial Jobless Claims |

265k |

-- |

254k |

Strengths

- The best performing precious metal for the week was palladium, up 4.89 percent. Wage negotiations started this week in South Africa with opening demands including a 15 percent hike for the highest paid employees and a 47 percent hike for the lowest paid. With the threat of possible strikes and the 19 percent rise in auto sales in China reported for June, related to tax cuts on auto purchases, we could see further upside in palladium prices.

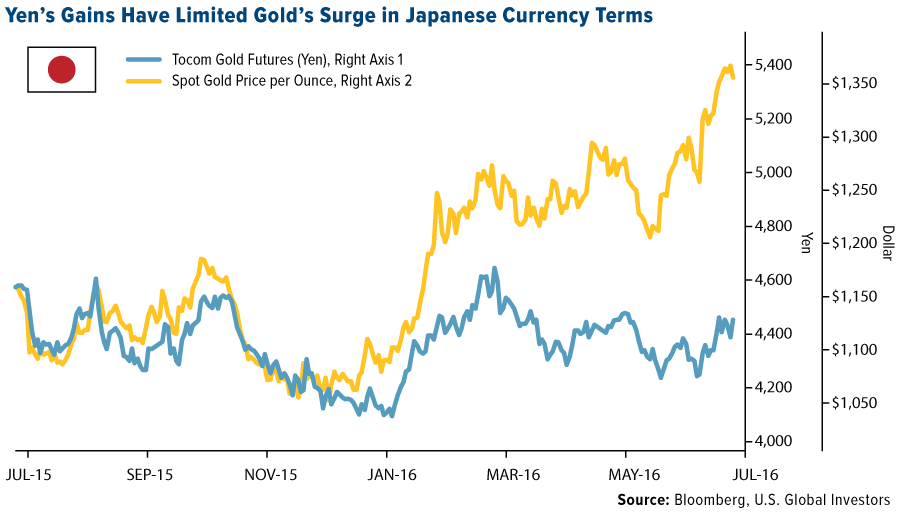

- “Gold is the unprintable currency, unlike the yen,” said Itsuo Toshima, former regional manager for the World Gold Council in Tokyo. According to Bloomberg News, Abenomics skeptics are selling the yen to buy this unprintable currency – gold. Individual investors drove a 60 percent jump in sales of the precious metal in June from May at Tanaka Holdings, the operator of Japan’s largest bullion retailer.

- Tanaka Holdings announced this week its plan to buy Metalor Technologies International SA, a privately held Swiss precious metals refiner, reports Reuters, expanding into precious metals recovery and refinery in Europe, North America and Asia. The aim is to boost Tanaka’s business as local growth stagnates due to a falling population by expanding their presence in the supply chain. No terms were given yet in the statement.

Weaknesses

- The worst performing precious metal for the week was gold with a loss of 2.11 percent. At the end of last week, the net long gold futures position on the COMEX had reached an all-time high, thus when we were in line for a possible correction. Interestingly, the gold equities did not fall as much as the gold price over the past week.

- Gold assets held in the world’s largest ETF backed by the metal, the SPDR Gold Shares fund, dropped the most in three years, reports Bloomberg. Holdings fell 16 metric tons to 965.22 metric tons on Tuesday as U.S. equity markets reached record highs. Following the U.K.’s decision to keep rates at 0.5 percent, gold dropped to a two-week low. The outlook for more central bank stimulus is curbing demand for the metal as a haven, notes Bloomberg, while a decline in demand from jewelers and retailers is also pushing the price lower.

- Gold was also impacted by a strong U.S. jobs report against signs of risks to the global economy, reports Bloomberg. Payroll data exceeded analysts’ expectations, buoying stocks and other risky assets, the article continues. In related news, SoGen announced Monday that gold producers expanded the hedge book 1.6m ounces in the first quarter, and stood at delta-adjusted 8.7m ounces at March 31. The majority of net hedging in the first quarter came from Newcrest and Polyus Gold.

Opportunities

- In its Global Gold Outlook this week, RBC Capital Markets increased its gold price assumption from $1,300 to $1,500 in 2017 and 2018, which is 12 percent above the current spot price. Citing one of the key gold price drivers, RBC notes that “a negative real rate of -1.0 percent suggests a $1,546 gold price.” Bank of America agrees that the yellow metal could move higher, stating that gold is headed to $1,500 an ounce, while also pointing out that silver can overshoot $30 an ounce. A combination of a weaker U.S. dollar and previously deferred demand from Asia should support the gold price in the second half of the year, according to a report from Citi analysts.

- Jeff Gundlach of DoubleLine Capital discussed his investment portfolio with Barron’s this week, the composition of which ZeroHedge broke down as follows: “high-quality bonds, gold, and some cash.” In response to inquiries about what kind of portfolio is he running, Gundlach said the following: “I say it’s one that is outperforming everybody else’s...Most people think this is a dead-money portfolio. They’ve got it wrong. The dead-money portfolio is the S&P 500.”

- Klondex Mines reported its preliminary quarterly production results this week of 41,436 ounces, according to a statement released by the company. This apparently beat expectations as the stock rose better than 1 percent this week while the averages were down almost 2 percent. Jaguar Mining also reported strong second quarter production this week of 24,222 ounces of gold, a 17 percent increase year-over-year. The company also cited high-grade gold mineralization recently encountered, confirming downward extension at depth at its Turmalina gold mine. Jaguar says the drill results provide potential to upgrade current inferred resources to higher category.

Threats

- For the first time ever, Germany issued a 10-year bond at a negative interest on Wednesday, selling more than 4.0 billion euros with a yield of minus 0.05 percent, reports the Bundesbank. Negative interest rates in Japan are also present, and seem to be backfiring in a big way, reports Bloomberg. The article reads, “Instead of encouraging spending, people are stashing their cash in safes, with sales of house safes increasing 250 percent over the last year.” What’s even more troublesome, is many elderly Japanese people are purposely committing crimes to end up in prison – a place with free food and health care, since negative rates are eating up their savings.

- In Brazil, bitcoin seems to be gaining more and more momentum, reports NewsBTC.com. The digital currency trading volumes in Brazil have actually surpassed that of gold in the last six months. “The recent rise in bitcoin prices from about $450 to over $700 before stabilizing at around $650 is attributed to increased demand in the Chinese market, Brexit and other external factors,” the article reads.

- According to portfolio strategist Martin Roberge of Canaccord, gold could correct in the summer. Roberge noted that gold stocks have outperformed the broader S&P/TSX Composite Index by 71 percent this year, and while this does not mean the bull market is over, he believes this kind of run is usually followed by a “higher risk” phase.

Energy and Natural Resources Market

Strengths

- Nickel prices climbed to their highest level this year as the Philippines threatens to crack down on local miners. The new president, Rodrigo Duterte, ordered a review of the country’s mining industry after stating publicly that open pit mining should be banned due to its effects on the environment. Philippines is the largest producer of mined nickel and supplies 97 percent of nickel used in China.

- The best performing sector for the week was the Thomson Reuters CRB Industrial Metals Producers Index. The index of global industrial mining companies rose 9.6 percent for the week as copper prices had their best week since March, on speculation that China and Japan may introduce new easing measures.

- Freeport-McMoRan, a major copper producer, was the best performing stock in the broader natural resource space, rallying 17.0 percent for the week. The stock rallied on the back of strong base metals prices.

Weaknesses

- A global gasoline glut is weighing on crude prices. This week the Energy Information Administration (EIA) reported a surprise build in gasoline and diesel inventories, which, according to Desjardins analysts, suggests that refiners may cut runs—a bearish prospect for crude prices given the high level of crude inventories.

- The worst performing sector for the week was the NYSE Arca Gold Miners Index. The index of gold mining companies dropped 1.7 percent for the week as gold prices posted their first weekly decline in seven weeks.

- The worst performing stock for the week in the S&P Global Natural Resources Index was Newcrest Mining. The Australian gold major producer dropped 6 percent for the week as investors took profits on gold miners following a six-week rally.

Opportunities

- Citi is especially bullish on commodities for 2017. Ed Morse, Global Head of Commodities Research at Citigroup, is bullish on commodities including oil, as the impact of the U.K.’s vote to quit the European Union fades away. The report also states that while the bear market in oil is now over, a bull market hasn’t yet begun and “prices are expected to resume their ascension in 2017 as the market rebalances further.”

- Demand for crude is set to rise more than initially expected in 2017, says the Organization of Petroleum Exporting Countries (OPEC). Higher demand will mainly originate in non-OECD countries, and will support oil prices as market conditions alleviate the overall excess inventories, and non-OPEC production continues its contraction, said OPEC in its Monthly Oil Market Report for July.

- The zinc rally may have legs. Following a 50 percent rally since bottoming in January, zinc has taken over setting the pace in the base metals market. The gains have been powered by greater-than-anticipated Chinese steel output and expectations for a global deficit after major producers curtail supply. Despite the sharp rally in prices, treatment charges continue to decline which suggest physical players are struggling to deliver sufficient supply.

Threats

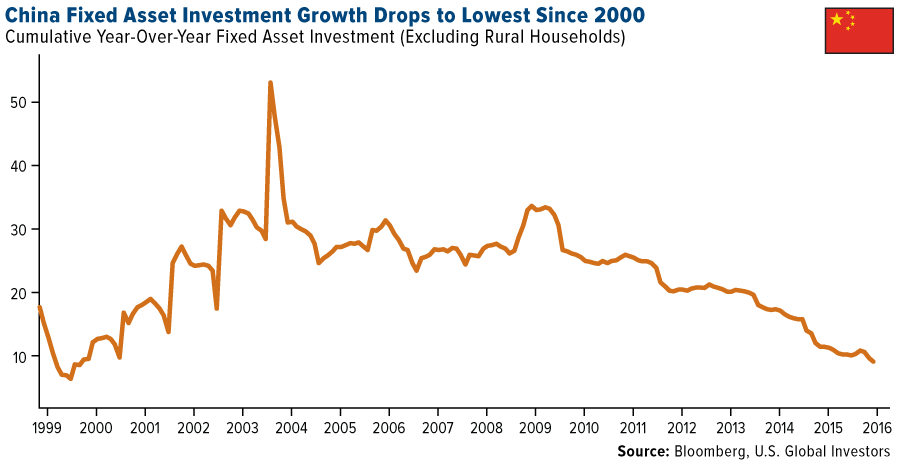

- China’s June data paints a weak outlook for commodities. The key negative data was fixed asset investment (FIA), a key source of commodity demand, which dropped to 9.0 percent, its lowest growth rate since at least 2000. VTB analysts suggest the data implies a significant slowdown in the second quarter, validated by private sector investment data, which fell to a new record low of just 2.8 percent from last year.

- China commodity imports, while growing, point to a recent deterioration in fundamentals. Despite most commodity imports still showing double-digit growth from a year ago, June data continued to weaken from peaks earlier in the spring. For the month of June, crude oil imports dropped 5 percent month-over-month, with iron ore and copper dropping 5.9 percent and 2.3 percent respectively over the same period.

- Iron ore prices are running ahead of fundamentals, again. Macquarie Research points out that iron ore prices have continued to move higher this week as investors speculate about more stimulus coming out of China. Despite the speculation, there is little fundamental support for this recent move given abundant iron ore supply and multi-year high port inventories.

China Region

Strengths

- A number of better-than-expected Chinese data on Friday cheered investors. June year-over-year Industrial Production came in at 6.2 percent, ahead of expectations for a rise of 5.9 percent and better than last month’s 6.0 percent. June retail sales were up 10.6 percent, better than May’s 10.0 and ahead of analysts’ expectations for a rise of 9.9 percent. New yuan loans and aggregate financing were well ahead of expectations at 1.380 trillion and 1.630 trillion respectively, M2 money supply was up 11.8 percent year-over-year, and China’s second quarter GDP was 6.7 percent, beating analysts’ expectations for a year-over-year growth rate of only 6.6 percent.

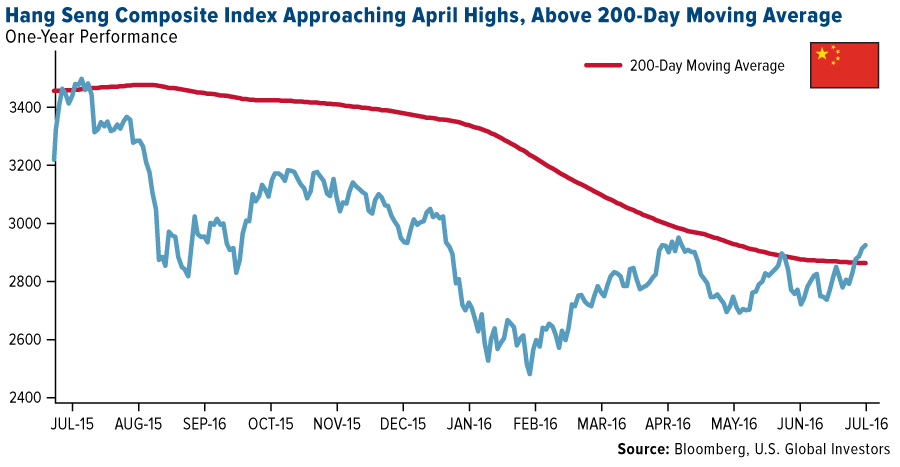

- The Hang Seng Composite Index rose above its 200-day moving average to a multi-month high, leaving the index now just shy of its April highs. The Shanghai Composite is also now just below its April highs, while the H-shares (Hang Seng China Enterprises Index) had its best weekly gain in four months this week.

- Texhong Textile Group Ltd. (2678 HK) was the top-performing stock in the HSCI for the week, rising just under 20 percent in that time frame after the company guided up and announced that it expects better gross margins and higher sales volumes than originally anticipated.

Weaknesses

- Bloomberg reports that Bank of America, UBS, Goldman Sachs, and RBS have all lowered their outlooks for the Chinese yuan to 7 and beyond.

- Bank Negara Malaysia caught most analysts by surprise this week as the new central bank governor Muhammad Ibrahim announced an unexpectedly dovish 25 basis point rate cut as a “pre-emptive move” against a slowdown in inflation. The Malaysian ringgit has been a strong performer this year, which surely factored into the BNM decision.

- The one disappointment in the Chinese data this week was poorer-than-expected Fixed Assets Investment, or FAI, which came in for the June period at only 9.0 percent year-over-year, missing expectations for 9.4 percent, and down from May’s print of 9.6 percent.

Opportunities

- Navip Singh Judge, an ex-trader at Lehman Brothers and JPMorgan Chase, believes the global capitalist system is broken and he is looking to fix it, reports Bloomberg. Last week Judge announced his aim to create a crowdfunded budget airline carrier by raising 8.5 million pounds. According to Judge, who is a Briton of Indian origin, the carrier will fly a single plane between London and several Indian cities.

- Future Mobility Corp., a Chinese electric-vehicle company backed by Tencent Holdings (and Foxcom Technology), is planning to complete its first round of financing in the third quarter, reports Bloomberg, targeting to sell its first model by 2020. As the government seeks more innovation within its auto industry, Future Mobility is one of several electric vehicle startups getting backed by technology companies, the article continues.

- Airbus closed four deals on Tuesday at the 2016 Farnborough Air Show, and AirAsia was the biggest buyer, spending $12.57 billion worth of list prices for 100 Airbus A321neo airliners. “The A321neo will help us to meet ongoing strong demand as well as further reduce our costs across the group, which will translate to lower air fares for our guests,” AirAsia CEO Tony Fernandes said in a statement.

Threats

- An international court ruled on Tuesday that China exceeded the law in its efforts to assert control over the South China Sea, reports Bloomberg. China said it neither accepted nor acknowledged the ruling and reaffirmed its views the proceedings went against international law, the article continues. The ruling, which is seen as a setback for the Asian nation, went beyond what analysts had expected.

- China’s trade surplus narrowed in June, reports Bloomberg, as exports fell 4.8 percent year-over-year and imports dropped 8.4 percent. A spokesman for China’s General Administration of Customs said that China’s economy was facing “increased downward pressure” from Brexit and expectations of further interest-rate increases in the U.S. Global Investors, Inc.

- As global risks mount, Malaysia joined its Asian counterparts from Indonesia to Taiwan in easing policy, reports Bloomberg, cutting its interest rate for the first time in seven years. The decision to cut rates by 3 percent, made by new central bank governor Muhammad Ibrahim, came as a surprise to a majority of economists surveyed by Bloomberg.

Emerging Europe

Strengths

- The Czech Republic was the best performing country this week, gaining 6.5 percent. Erste Group, the Austrian bank listed on the Prague Exchange increased by almost 19 percent in the past five days as management raised guidance for 2016 on the back of better operations and Visa Europe sales

- The Romanian leu was the best performing currency this week, gaining 83 basis points against the U.S. dollar. Romania is one of the fastest growing emerging markets. The country’s latest GDP data was reported at 4.3 percent on a year-over-year basis and 1.5 percent growth was recorded in the first quarter of 2016.

- The materials sector was the best performer among Eastern European markets this week.

Weaknesses

- Hungary was the worst relative performing market this week, gaining 24 basis points. Moody’s decided not to update the country’s sovereign rating last Friday, leaving it at Ba1, one notch below investment grade. Fitch upgraded Hungary back to investment grade in May and many expected Moody’s to follow the same path.

- The Turkish lira was the worst performing currency this week, losing 5.5 percent against the U.S. dollar. The currency declined sharply in the late trading session on Friday after gunfire was heard in the Turkish capital. There were reports of unusual military activity, with a military chopper opening fire near the national intelligence headquarters.

- The health care sector was the worst performer among Eastern European markets this week.

Opportunities

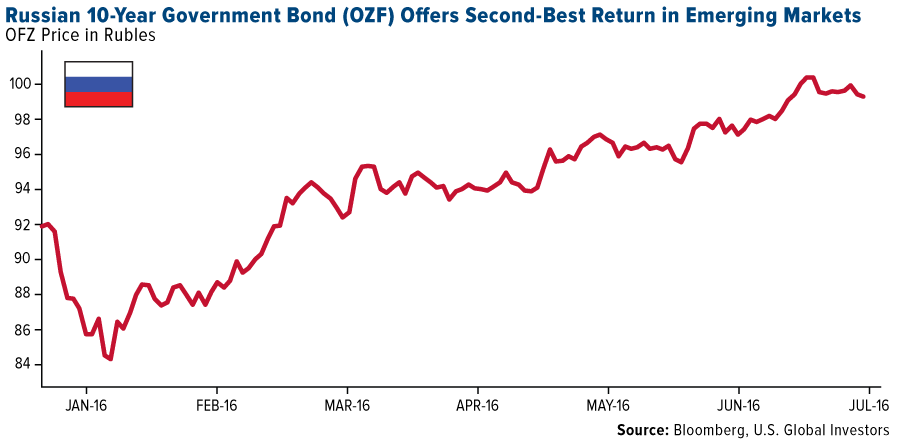

- According to Bloomberg, the Russian government bonds known as OFZs have offered investors a return of 23 percent in U.S. dollar terms in 2016, the second best performance after Brazil. Yields have been falling and bond prices are rising as investors pile into local debt on bets that the central bank will continue monetary easing. Citigroup estimates Russia to cut the benchmark rate to 6.8 percent by the end of 2017. The current Russian main interest rate stands at 10.5 percent. The next central bank rate decision will be announced on July 29.

- HSBC has a positive view on Russia. In its latest Russian Monitor, one analyst wrote that the economic cycle and corporate earnings are stabilizing, with the market potentially close to bottoming out and a recovery expected in 2017. Consumer confidence in the second quarter is up for the first time in 18 months with an increase in nominal income.

- The Bank of Greece submitted a series of proposals to creditor institutions for easing capital controls. Proposals include excluding new deposits in cash from restrictions on withdrawals, lifting a ban on advance payment of loans and allowing lump sum ATM withdrawals of EUR 840 every two weeks. Proposals also include allowing 30 percent of sums transferred from foreign accounts to be withdrawn in cash, from 10 percent currently.

Threats

- The U.K. Conservative Party named Theresa May as its new prime minister. On Monday, May said she would move decisively to leave the eurozone bloc. Although the U.K. has a new prime minister and some political uncertainty has been lifted, new appointments of pro-Brexit leaders including Boris Johnson (foreign office), Liam Fox (trade department), and David Davis (new minister for Brexit) signal that Brexit does in fact mean Brexit.

- The Bank of England left its benchmark interest rate unchanged on Thursday after the economy stumbled under Britain’s decision to exit the European Union. The benchmark rate is set to 0.05 percent for another month but officials say they expect to launch fresh stimulus next month.

- Eurozone Industrial Production (IP) declined by 1.2 percent month-over-month, a greater drop than the 0.8 percent forecast by the consensus. This month-over-month decline in IP will weigh on GDP in the second quarter

© US Global Investors