Property Tax Blues

Dubious Assumptions

Bankruptcy Not an Option

Abandon State

Risk-Adjusted Retirement

Maine, New York, Montana, and Iceland

You made me promises, promises

You knew you’d never keep

Promises, promises

Why do I believe?

– Naked Eyes (1983)

It’s election year in the US, so once again we see politicians promising the moon. That’s what happens in a democracy. Regardless of party or office, all politicians make promises in order to get elected. This is their nature. Dogs bark, birds sing, politicians promise.

In the investment business, we’re taught not to make promises because they create liability. Lawyers and compliance officers review documents for “promissory” language. Instead of “This fund will give you a profit,” firms say things that generally sound like “This will give you the opportunity to profit,” thereby avoiding lawsuits and regulatory action when profit proves elusive.

With the Republican convention just concluded and the Democratic convention just ahead, with the presidential candidates making promises by the dozens, let’s imagine what a presidential promise would sound like if it had to comply with the same rules that investment advisors and brokers must adhere to. It would go something like this:

If you elect me as president, I will (insert promise), assuming of course that I can get both houses of Congress to agree, which means of course that I must persuade enough of the opposition Senators to bring my total up to 60 votes in the Senate, assuming that none of my own party votes against me. And that also assumes we can find the money to fulfill this promise, which is unlikely without some real (and unlikely) compromises.

Would-be elected officials face no such restraints, except from voters, who by the next election tend to forget what they were promised. There are exceptions, though. Some political promises don’t fade away. They come back years later and demand fulfillment. Which brings us to the topic for today’s letter: the promises made by politicians concerning public employee pensions.

Chicago residents are learning about this the hard way. They won’t be the only ones. Voters all over the US will pay for the promises their elected officials made long ago – and broke.

Last week in “The Age of No Returns” we discussed the prospect of persistently low market returns in the coming years. Here is the GMO forecast again.

A portfolio balanced between major equity and fixed-income asset classes will be lucky to break even in the NIRP-heavy world I foresee. Poor returns will be an especially thorny problem for anyone who is contractually obligated to use portfolio returns to pay certain amounts on certain dates but hasn’t set aside funds to do it.

Defined-benefit pension plans are the primary example. Today these exist mainly for public-sector employees. Private industry long ago shifted to 401(k) and other defined-contribution plans.

Public pension plans are rarely fully funded. They assume that future investment returns will make up the difference. What if they don’t? Retirees go back to the taxpayers whose representatives made the promises and demand they pay up.

This is happening in Chicago right now. After years of fruitless argument and litigation, authorities raised property taxes to meet pension obligations. Cook County taxpayers recently received their bills and were not amused.

Outside the assessor’s office, city homeowners told one property tax horror story after another.

“Our taxes increased fivefold,” said William Phillips of Rogers Park. “I was expecting it to go up maybe twice as much but not four to five times as much.”

“My tax bill increased almost $1,200 dollars,” said Cornes King of Chatham.

“More than tripled. The city’s piece more than tripled,” said Logan Square resident Janelle Squire.

The bills that arrived over the weekend reflect rising Cook County real estate values and, in Chicago, the city’s $588 million levy increase. Most of it is to restore police and firefighter pensions that Mayor Rahm Emanuel says his predecessors underfunded.

“A number of people across the spectrum politically, denied, deferred, and delayed the day of judgment,” said Mayor Emanuel.

“I don’t think that I’m getting the services what I’m paying for,” said King.

Unfortunately for the taxpayers, that’s not actually how the system works. Paying your taxes is not a commercial transaction. You don’t give the government money in exchange for goods and services. You must pay taxes, but the government need not give you anything in return. They allow you to go on living somewhere besides a prison cell. That’s all they have to do.

Of course, if we’re unhappy with the way the city, county, or state is administering our taxes, we can vote for different politicians who will spend our money more in line with what the majority of us think. So, in general, we do get roads, police and fire departments, parks, and other services that are paid for by our taxes.

The problem is that, in all too many cases, politicians make promises to various government employees that include future retirement benefits, but they don’t actually spend the money to fund those promises. And those unpaid balances keep adding up until the future becomes today, which is what is happening in Illinois and other states around the country.

When the current political powers that be in Illinois decided that they couldn’t afford to pay for the promises made by past politicians, the unions and retirees (not unjustifiably) asked the courts to force the various government agencies involved to keep those promises.

And the courts determined that, under state law, retirement benefits cannot be reduced after the fact.

Thus Illinois courts have determined that retired public employees have more rights than taxpayers do. Retirees are entitled to what their elected officials promised them, no matter how impossible it may be to keep those promises. So elected officials are forced to either reduce current services such as police and fire and parks and roads, or raise taxes. Paying already contracted retirement benefits is at the top of the list of city expenditures.

Now, let’s go back to that Cook County news story:

[T]he Chicago Public Schools Board is expected to approve a $250 million property tax hike to pay for teacher pensions. The new levy was enabled last week by the Illinois General Assembly and Governor Bruce Rauner. The additional charges, hundreds of dollars more for an average city house, will appear on tax bills a year from now.

“We might have to consider selling. I don’t know if we’ll be able to afford it,” said Phillips of his Rogers Park home.

Mr. Phillips is free to sell his home, but to whom? And at what price? A home’s market value is a function of supply and demand. Prospective buyers want to know more than the building and land costs before they buy – current and future tax liabilities are part of the equation, too. Mr. Phillips will have to set a selling price that reflects the known and unknown liabilities associated with his house.

In the US today, most people who are buying homes look not so much at the total mortgage but at whether they can afford the monthly payments. For instance, I have a mortgage on my apartment. But a prospective buyer of my home would be interested not only in how much my monthly mortgage costs but also in my tax and insurance bills as well as my homeowners association dues and payments for utilities and other services. It turns out that my HOA dues and taxes are significantly higher than my mortgage payments. The total of those costs affects the price I could get for my home if I wanted to sell.

So when Mr. Phillips says he may have to sell his home, those higher taxes are going to reduce its value. He’s going to pay the higher taxes one way or another. He either stays where he is and pays them, or he sells the property at a lower price because of the taxes. Those are his choices.

This isn’t just a Chicago problem or an Illinois problem. A significant number of public-sector pensions everywhere are in the same fix, to varying degrees. They all assume their portfolios will deliver returns well above the 2% to 4% or so that they may actually be able to get in the next decade. They can try to extract more from taxpayers, but at some point the taxpayers will simply leave. That’s what happened in Detroit.

Every state and local government has workers toiling away to provide public services, and their elected leaders have promised them certain retirement benefits. Some states and cities have been more generous than others. Some do a better job of managing their pension obligations. But nationally there is a big problem.

Estimates of the unfunded liabilities vary, not because of dishonesty but because the estimates necessarily involve many assumptions: life expectancies, healthcare costs, interest rates, stock market returns, tax rates, and more. Tweak any of those numbers just a little bit now, and the difference over 30–50 years or more can be dramatic.

An April 2016 Moody’s analysis pegged the total 75-year unfunded liability for all state and local pension plans at $3.5 trillion. That’s the amount not covered by current fund assets, future expected contributions, and investment returns at assumed rates ranging from 3.7% to 4.1%. Another calculation from the American Enterprise Institute comes up with $5.2 trillion, presuming that long-term bond yields average 2.6%.

Are any of those return assumptions reasonable? Over a really long period like the next 75 years, maybe so. I see almost zero chance of hitting them in the next 10 years. Failing to hit them will put many more plans on very thin ice. Baby Boomers will keep reaching retirement out until 2030 or so. If life expectancy keeps going up, people will survive to collect benefits longer. A big crunch is inevitable.

There is a fact about pensions that very few people actually understand. The largest part of the money that a pension manager assumes they will pay out in 20 years comes from the investment returns on current assets. Depending on the rate of return your pension plan assumes, as much as 70% (or possibly more) of your future payments depends on the returns your fund manager will make on investments. If you are a government employee who is 30 years old and expecting to get a pension in 35 years, the money you are putting into your pension fund will cover less than 20% of your expected future payout. Everything, and I mean everything, about your future pension payments depends on the rate of return your pension plan gets on its investments – and on the willingness and ability of future taxpayers to continue funding your underfunded pension plan.

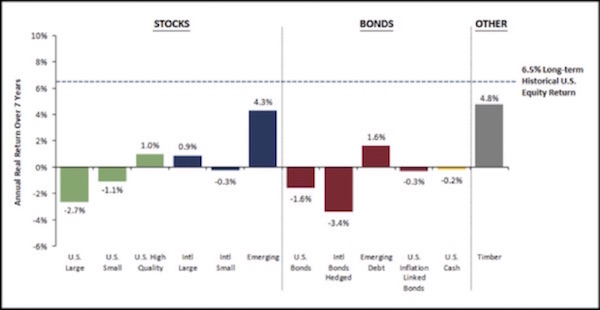

My friend Rob Arnott, founder of Fundamental Research, is one of the most respected financial analysts in the country. He and his very talented staff spend a great deal of their time thinking about future returns for pension and retirement funds. We were together in Las Vegas last week, and one of the topics we discussed was the problem of underfunded pensions. The average retirement plan assumes it will get annual returns north of 7%, and many assume 7.5% or as much as 8%. Rob copied me on an email he sent this week to a high-ranking politician, asking about that very issue. Let me show you his calculations on potential future returns. Remember, he is talking about the long term here, not just the next 10 years. In our conversation in Vegas, we agreed that the next 10 years will be challenging in regards to investment returns. Quoting from his letter (in which he assumes the typical 60% equities/40% bonds ratio that most pension funds use), here’s the math:

40% Bonds. Yield is 2% for the US aggregate bond market.

60% Stocks. Our base case is 5.4% for US stocks, but we think valuations are too high, so we trim this to 3.3% for the coming decade. Here’s our logic:

The yield is 2%.

Earnings growth over the past century has been 4.5%, of which 3.1% was inflation (real growth of 1.4% … far less than most people realize).

Inflation expectations are about 2%, so perhaps we should trim this forecast by 1.1%.

This gives us a base-case of 5.4%.

Valuation multiples are stretched, with the stock market priced at 25 times the 10-year average earnings, against a historical norm of 16.8x. If we’re back to historical norms in 10 years, that costs us another 4.2%. Since valuation multiples could (a) return to historical norms, or (b) remain at today’s lofty multiples, let’s split the difference, and trim our return expectations another 2.1%.

This gives us a likely outcome of 3.3% from stocks.

If our logic is sound, we earn 0.8% from our bonds (40% allocation x 2% return) and 2% to 3.2% from our stocks (60% x 3.3%, or 60% x 5.4%). Add up the return from stocks and the return from bonds, and we get 2.8% to 4% from our balanced portfolio.

Bottom line … US public service pensions are toast. One of three constituencies gets nailed: the taxpayer (keeping in mind that the affluent are mobile!), the current and/or future pensioners (keep in mind that private-sector pensions are now far less generous than public pensions … there’s an inequity here!), or the public services that are on offer to our citizenry, net of sunk costs from servicing past generations. Most likely, it’ll be a blend of the three.

When Bankruptcy Is Not an Option

Our judicial system has a time-tested option for those who can’t pay their debts: bankruptcy. Individuals and businesses use it all the time. The debtor submits itself to a court, which tries to reach the fairest possible settlement with creditors. It’s messy, but it usually works for the best.

Federal bankruptcy code permits cities, school districts, and other local governments to file bankruptcy. Some have done so, and I expect many others will in the coming years. Cities like Detroit and others in California have used bankruptcy to renegotiate their pension plans and other debts.

States are a different matter. Current law doesn’t let them go bankrupt.

In theory, Congress could change the law and let states go bankrupt. For instance, there are those who agree with President Obama, as well as with Newt Gingrich and Jeb Bush, that Puerto Rico should be allowed to go bankrupt. If the law should change and a state actually tried to file for bankruptcy, creditors would immediately file constitutional objections under the contracts clause and the 10th Amendment. Some legal scholars think those barriers can be overcome, but at minimum the argument would go to the Supreme Court and probably take years to be resolved.

But getting Congress to pass such a controversial law could be quite difficult. There are good reasons to prevent state bankruptcies. The fact that they aren’t eligible for bankruptcy allows states to borrow money at lower interest rates. Lenders assume states will always figure out some way to repay their debts. But will they? Recent history says yes. Go back some 80-odd years and the answer isn’t so clear.

In 1933, debt-plagued Arkansas unilaterally restructured and extended maturities on a series of highway and other bonds. Nowadays we call that a default. Bondholders sued, of course. The next year the state and its creditors reached a compromise refunding. Creditors exchanged their old bonds for new ones funded by a 6.5 cent per gallon gasoline tax.

In today’s dollars that would be about $1.16 per gallon, so this was a hefty tax on Arkansas drivers. I am sure they complained. That deal fell apart, and after many more twists and turns, the federal Reconstruction Finance Corporation (predecessor to the FDIC) bought the new bonds.

Back to the present: the Moody’s report cited above sees almost zero chance that the federal government will bail out an indebted state government. I agree; the other state delegations in Congress would quash any such idea. You can debate whether the Arkansas episode was a “bailout” or just a refinancing, but it is one of the few precedents we have for a state default.

That leaves us in a very murky situation with regard to state and local pensions. We know many will have a hard time meeting their obligations. Those at the state level can’t go bankrupt, nor can they expect federal help. Something will have to give in those states. Whatever the outcome is, it won’t be pretty.

And not every government below the state level can declare bankruptcy to discharge its pension obligations. Illinois and other states, including my own state of Texas, have passed laws that require cities to honor their commitments. They can change pension agreements going forward, but they are legally required to honor past agreements.

This leaves an important question: which states and local governments will hit the wall first? Finding the answer is not as easy as you might think.

As noted above, evaluating a pension plan’s future prospects requires all kinds of long-term assumptions. Near-term prospects are hard to judge for a different reason. States and localities all operate under different state constitutions, contract laws, labor laws, and other constraints. Two states might look the same, financially speaking, but have far different pension-system prospects for legal reasons.

Illinois, for instance, is in a jam because its state constitution doesn’t permit it to reduce pension payments. Other states have more flexibility. States also give their pension managers different degrees of authority and liability. It’s a mess. What states are most likely to raise taxes and/or cut government services?

I found one analysis that helps pinpoint the top risks, considering not just pension shortfalls but other financial obligations as well. The Governing Institute, a group for state and local leaders, reviewed three separate studies from J.P. Morgan, PricewaterhouseCoopers, and the Mercatus Center of George Mason University. JPM and PWC both point to the same four states: Connecticut, Illinois, Kentucky, and New Jersey. The Mercatus Center concurred on those four and added Massachusetts to the list.

This doesn’t mean everyone else is safe. You might live in a very sick city in an otherwise healthy state. There are cities in Texas, arguably one of the healthiest states, with significantly underfunded pension plans. In our teacher retirement programs, many school districts are underfunded. You could also be in a sick city that is in a sick state, giving you double trouble if you own property there.

Oddly, you may be at risk if you stay, while your city and state are at risk if you leave. Property tax revenue depends on property values, and property values fall if too many people want to sell. If governments raise tax rates to compensate, then even more people will leave. At some point a death spiral sets in. Detroit went through this and is only now beginning to recover. People left the City of Detroit and moved to the suburbs.

I think we’ll see many more Detroits. Make sure you don’t live in one.

For instance, more and more affluent people are leaving California because of the taxes and other high costs. Dennis Gartman wrote this note:

According to the always interesting and strong proponent of free markets and small government, the Mercatus Center at the George Mason University, California now owes a stunning $118.2 billion. However, when we add to this sum the pension fund shortfalls and other major concerns, California actually owes $757 billion. On a population of 38.8 million, that's a stunning $19.5 thousand per citizen... Children included!

California's problem is that the state is adding nearly $15 billion annually to its deficits, and as those deficits rise the state’s ability to add to its roads, its universities, its hospitals, its bridges, its all-important water supplies et al are falling rapidly.

California, according to the Investor's Business Daily, is a “massive welfare state.” According to the IBD, one/third of all US welfare recipients live in California, which, with its generous welfare benefits, has become a magnet for impoverished immigrants from around the world. A quarter of the population lives near the poverty line.

And the news from California just gets worse. This from Reason magazine:

Another year, another mess with California’s public employee pensions. The California Public Employees’ Retirement System (CalPERS) announced this week that the rate of return for its investments for the fiscal year ending on June 30 was less than one percent. It was .61 percent. As the Los Angeles Times notes, this is the worst returns it has logged since 2009, when the housing bubble burst and hit California particularly hard.

That’s a far cry from the 7½% CalPERS assumes it will get. And the newly passed $15 minimum wage in California will add almost $4 billion of annual cost for government employees as well as increase the state’s required pension payments.

I wrote about the retirement problem in depth a few months ago in “ZIRP & NIRP: Killing Retirement As We Know It.” I won’t repeat that analysis here, but I’ll say this: Whatever amount you are saving for retirement is probably not enough. The pension crisis is one element of a much bigger one.

If you’re a retired teacher, firefighter, etc., you naturally want what you were promised. You probably won’t get it. That’s just simple reality. The taxpayers don’t have the money. Now is an excellent time to accept that fact and make alternate plans.

In fact, that’s good advice for pretty much everyone. Your future plans, whatever they may be, probably won’t protect you from the storm I think is coming.

I may be wrong on this. I hope I’m wrong. There’s still a chance the central banks and politicians will get their acts together and change course. There are things they can do to restore sustainable economic growth and pull us out of the mud. We’ll be dirty but not drowned.

I’ve been having this conversation with my friend Ed Easterling. He pointed out that the crunch I am expecting could come in a very different way. Let me quote a paragraph from a recent email he sent me:

Lots of folks [he left the “like you” unstated] have been worrying about a looming financial catastrophe following policies that have included Fed QE, ZIRP, etc., and near-trillion-dollar stimulus programs. Maybe, just maybe, we’ll look back in five or ten years, after no catastrophe, and applaud that such “good” actions saved the economy without negative consequences. When, in reality, the “catastrophe” will have been the loss of 20%, 30%, or more in our standards of living and wage growth. The anecdote of the Frog-In-Boiling-Water may again prove to be a truism of life….

For planning purposes, however, the prudent course is to assume the worst. How will you retire in a 0% world? In most cases, you won’t. Kicking back at 65 or 70 won’t be an option if your portfolio can’t generate income sufficient to pay your bills.

If you intend to retire in the next few years, you need to do the math that so many pension sponsors avoid. You owe yourself an honest accounting. Will your savings be enough to cover your expenses in a zero-return world? Find a good financial planner to help you run the numbers in different scenarios. If he or she starts telling you that you’ll get 9% long-term (or 7% real, inflation-adjusted) returns on your stock market portfolio, politely glance at your watch and remember an important meeting that you have to go to. Then find another financial planner.

I think it’s important that everyone have a good financial plan and financial planner, someone who will give you a realistic estimate of your financial condition and what your retirement might look like.

If, as is likely, the numbers are discouraging, now is the time to adjust your expectations. If you’re still working, you can try to increase your savings. The statistics say that’s hard for most people. The better idea may be to follow the Mauldin Plan and don’t retire.

I’m almost 67 and not ready to retire. I could probably retire if I downsized my home and lived a much simpler life. I don’t want to do those things, so I’m still “working.” I put working in quotes because if I retired I would want to be doing the same thing I am doing now. I have the advantage of enjoying my work and being in good health. Not everyone is so fortunate.

This brings us to an important point. Adjusting your portfolio is only one of the preparatory steps you should be taking. It’s necessary but not sufficient. There’s much more to do.

Your most important asset is your own earning power. By this I mean the mental and physical ability to generate income. If your portfolio returns drop to zero (or even if they go down), but you still have earning power, you have a chance to recover. So it makes sense to protect and expand your earning power.

Ideally, you want to be in an occupation that won’t cut off your earning power at some arbitrary age. Better to have some kind of work you can do for as long as you wish. It should also be work you actually enjoy. No one wants to “retire” into slavery.

The other thing you should do is protect your health. Doing so gives you a double advantage. First, good health will enable you to work longer and more energetically. Second, people in good health have lower medical expenses.

My friend Patrick Cox talks about “health span” instead of life span. The goal is not simply to live longer but to stay active and independent at an older age. That’s what I hope to do. We are on the cusp of some major breakthroughs in life-extension technologies. I truly believe that 85 will be the new 65 long before I reach 85. Thus I may actually get to age backwards, at least for a few years. It’s what I optimistically tell myself, anyway.

Even without new developments, you can do a lot to increase your health span. Get exercise, lose weight, stop smoking, watch your diet – you know the drill. The hard part is actually doing it. Most people don’t, until it’s too late.

In a low-return world, your health and your earning power may be the best option you have. Preserve them at all costs.

Maine, New York, Montana, and Iceland

I know the original plan was to mostly stay home this summer, but sometimes you have to call an audible at the line. Maine for the annual fishing trip was always in the plan, and you have to go back through New York anyway, so staying around for a day or two to do media and meetings makes sense. Then, how many chances would I get to do serious research on the future of space exploration for my book – but to seize the opportunity I have to go to Montana for a few days; that makes sense, too. Then the chance popped up to go to Iceland and get a new perspective on the future of energy development. It takes a day to get to Iceland, and then meetings and a little looking around for a day and a half, and I’m back in Dallas. And no plans to go anywhere for another month.

A couple weeks ago, I did an interview with my good friend Grant Williams of Real Vision TV. I do a lot of interviews, but Real Vision is different. They feature video-on-demand sessions with global leaders in the fields of finance and investing – people like Jim Rogers, Jeff Gundlach, Neil Howe, William White, Hugh Hendry, and Albert Edwards – with new content appearing every day. For me, a big part of the value of Real Vision is that the interviews are conducted by Grant and his partner Raoul Pal, two guys whose views I immensely respect. Now, they’re offering my readers a 7-day free trial and a 10% discount to anyone who signs up. You can check it out right here.

I have been hobbling around for the last month. I seriously pulled my right quad muscle. There’s not much I can do other than wrap it and ice it. That and allow about three months for it to recover and then another 2–3 months of therapy to restore the strength I am losing by not working out below my waist. I guess the good news is, my upper body is getting stronger. And the pain is considerably less than it was a month ago, so I am recovering. And no, I didn’t strain it working out. I just moved wrong getting out of bed and stretched the leg in a direction that it evidently didn’t want to go. Consulting with the doctors and trainers confirms that there are no miracle cures for pulled muscles other than time. Which seems to be passing faster than ever these days, so before long I should be normal.

It’s time to hit the send button, so I’ll wish you a great week and move on to the next project.

Your not planning on retiring analyst,

John Mauldin

© Mauldin Economics