Elections and the Markets: Do Stocks Reward Continuity?

Now that we have the Brexit referendum behind us, more investors are beginning to refocus on the U.S. presidential elections. I’ve written a couple pieces on this subject this year:

In the first post, I showed how parties don’t matter as much as policies, and you should be very skeptical of any claim that one party is definitively better for the markets than another.

In another post I showed how, statistically, markets don’t seem to care about which party wins, as long as the winner commands a majority of the popular vote.

With those warnings in place, here are some interesting, data-driven findings about how the stock market has performed in election years. I looked at the inflation-adjusted total return on the S&P 500 Index from August 1 to the day of the presidential election for every election since 1928 (prior to the 1950s, the data comes from Global Financial Data). Here are the key findings:

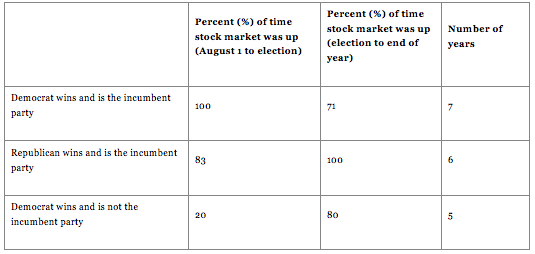

- The S&P 500 Index has performed best when the incumbent party won the White House.

- In seven out of seven elections in which Democrats retained the White House, the market was up from August to the election.

- Five out of six times when Republicans maintained control of the White House, the market was up.

- When one party wrestled control away from the other, the market was down more often than not in the pre-election period.

- The November-to-end-of-year period has been pretty good for the markets, in general (stocks were up 65% of the time in nonelection years), but the odds seem to tilt more favorably during election years, regardless of the victor.

Sources: Global Financial Data and author’s calculations

Besides the presidential elections, there’s likely an infinite number of other factors that could have moved the markets, but it is interesting to note that continuity of control seems to be better for markets than change of control. This is particularly interesting given that only 45% of the time in nonelection years was the S&P 500 Index up during the pre-election period. One interpretation is that, if the market is up in the August–November period, the market is signaling the incumbent party will win. Another interpretation is that the incumbent party wins because the market goes up. Take your pick!

There are also many stories about how one party winning the White House was good or bad for particular industries. You can actually test that hypothesis using data available from Professor Ken French’s database on daily returns for 49 different industry portfolios, spanning from 1926 to the present. To test this hypothesis, you have to do two things:

- Ask whether any difference in average returns is unlikely, due to the noisiness of the data. In any given year, returns can be pretty volatile, so to attribute a difference to whether one party wins or not requires the difference to be big enough to be unlikely, due to natural variation in returns. This is a test of statistical significance.

- Next, ask whether any statistically significant difference is also economically significant. If it’s a matter of a fraction of a percentage point, who really cares?

For a test of statistical significance, you have to pick a significance level, which is the probability of finding the observed value (or a more extreme value) when there is indeed no difference between the different groups (say, average returns when a Republican wins versus when a Democrat wins). Traditionally, 5% or 1% is chosen, but these are just conventions.

Using the 5% level of significance, from Election Day to the end of the year, these industries have historically benefited after an incumbent party wins, regardless of which party it is:

- Beer (+10%)

- Chemicals (+9%)

- Computer hardware (+8%)

- Computer software (+13%)

- Electrical equipment (+12%)

- Insurance (+11%)

- Laboratory equipment (+12%)

- Mining (+13%)

- Pharmaceuticals (+10%)

Whether any of those past patterns will hold or not depends on many other factors, including shifting platforms of the parties and changes in the relative lobbying strengths of the industries. This year, it will be important to listen to the candidates and decipher who may win or lose from their proposed policies. To figure that out, we’ll likely have to wait until the candidates confront each other in the presidential debates. My take: Past patterns are unlikely to repeat in this rather unique election.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 7-26-16 and are those of Dr. Brian Jacobsen, CFA, CFP, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management