- Man vs. Debt

- China’s Leverage Could Become A Global Concern

- The Drive to Extend Debt Maturities

For much of human history, debt has been frowned upon. The Bible advises, “Owe no one anything, except to love each other.” In Shakespeare’s Hamlet, Polonius says, “Neither a borrower nor a lender be; For loan oft loses both itself and friend, and borrowing dulls the edge of husbandry.” Debtors’ prisons, whose inhabitants were forced into labor to work off what they owed, were common until the mid-19th century.

Whether for religious or cultural reasons, an aversion to indebtedness has deep roots in many parts of the world. And yet the ability for savers to lend their money to others and earn interest in return is at the core of modern financial systems. The arrangement, properly controlled, has immense benefits for both parties and facilitates economic growth.

Today’s societies have therefore sought balance in their use of debt, taking advantage of its benefits while guarding against its potential to foment moral corrosion and financial crisis. No one knows exactly where the line is that separates the two; it can only be viewed in retrospect. Nonetheless, the battle lines over debt are being drawn by politicians and policy makers at the moment, with the future of global economy hanging in the balance.

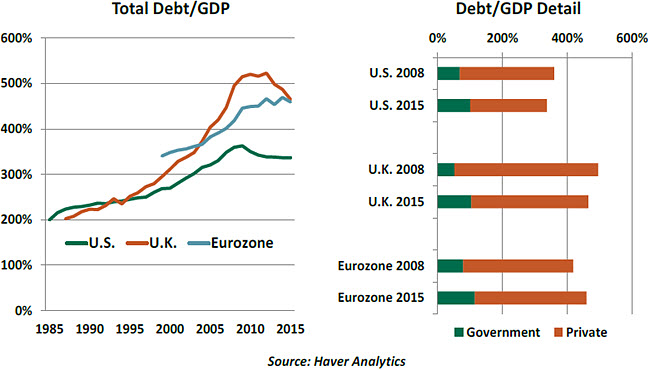

Many countries are presently carrying a degree of leverage that our forebears would probably have considered sinful. There has been some moderation since the financial crisis, but where households have generally become more frugal, governments have become more active.

To a certain degree, this substitution makes a good deal of sense. In his “General Theory of Employment, Interest and Money,” Keynes described a “paradox of thrift.” When times become difficult, individuals and businesses tend to watch their balance sheets much more closely, limiting their consumption and exacerbating recession. To counter this countercyclical behavior, Keynes argued that governments should step in, borrowing and investing more actively. The trend toward private saving would presumably allow this fiscal expansion to occur when interest rates are modest.  This narrative seems to fit very well with patterns seen in post-crisis economies. Personal savings rates are up, partly out of cyclical conservatism and partly because there are large demographic cohorts nearing retirement age. Firms have also become more cautious, holding back on capital expenditures. Much of the corporate borrowing done in recent years has been employed to reduce interest costs, buy back shares or pay dividends.

This narrative seems to fit very well with patterns seen in post-crisis economies. Personal savings rates are up, partly out of cyclical conservatism and partly because there are large demographic cohorts nearing retirement age. Firms have also become more cautious, holding back on capital expenditures. Much of the corporate borrowing done in recent years has been employed to reduce interest costs, buy back shares or pay dividends.

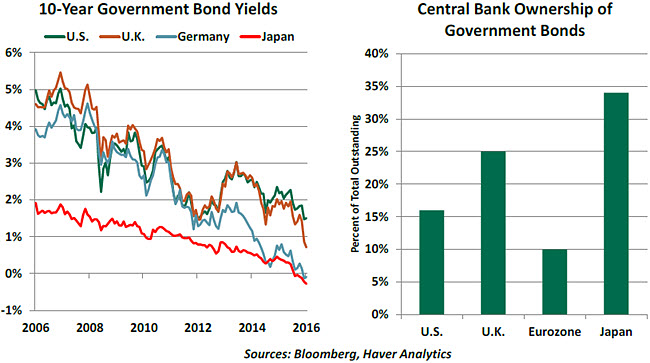

And it is certainly the case that government borrowing costs have declined. That is perhaps an understatement. The Wall Street Journal recently reported that $10 trillion in sovereign debt worldwide now carries a negative interest rate. As investors seek to avoid paying for having the government hold on to their money, yields in other markets have fallen to record lows.

With global growth sluggish and potentially at risk of slipping into recession, this would seem an opportune time for further government leverage. Yet the tone of public discourse has trended in the opposite direction. There is anxiety about current levels of debt, and upcoming costs for public retirement and health programs promise to further challenge fiscal balance. Most eurozone members (including Germany) have surpassed the 60% cap on the ratio of government debt to gross domestic product (GDP). Political platforms in the United States strike a very cautious tone (Democrats) or an outright hostile tone (Republicans) toward the national debt.

Proponents of additional borrowing counter with the following reasoning.

- While public finances are not comfortable, the scale of the fiscal response since 2008 may not be sufficient to address the depth of damage done to economies by the financial crisis.

- We’ve argued that central banks are at the edge of their effectiveness. Pressing ahead with unconventional monetary policy could have limited benefit and increase the risk of financial instability down the road. Fiscal strategies would have a much more direct and positive impact on economic growth.

- Private investors have a robust appetite for high-quality fixed income assets, central banks are buying government debt and banks are required to hold high-quality liquid assets in reserve.

- Disappointing economic growth may be as pernicious (or more so) than renewed borrowing for the sustainability of government debt. If policy can engineer a more robust expansion, debt ratios could eventually be reduced over the long term.

- Wealthy countries with assets to back their national debt can clearly handle higher levels of leverage.

- What to do with additional borrowing? The global need for infrastructure investment is acute. This isn’t just to repair roads; it’s to modernize transportation systems, invest in broadband and increase energy efficiency. These kinds of steps can increase productivity and potential economic growth. It is certainly proper to suspect that the funds might not be wisely spent, but investing nothing earns no returns.

- I was raised by two parents who lived through the Depression. My suggestion that more debt could be a good thing will undoubtedly find them frowning on me. I know that look all too well.

The View of Debt From the Far East

- The Chinese economic profile shows stark contrasts. Its legacy of rapid and sustained growth for three decades is unsurpassed. At the same time, however, China has accumulated debt at an extraordinary scale for a developing economy. This could weigh heavily on Chinese and global economic performance in the years ahead.

- Since the Global Financial Crisis (GFC), credit has driven economic growth in China to the extent that debt in the nonfinancial sector, which was stable before the crisis, ballooned from 117% of GDP in 2007 to 210% of GDP in 2015. Government and household debt are not high by international standards, but nonfinancial corporate debt is huge (170% of GDP) and worrisome.

- Chinese authorities responded to the GFC with an aggressive fiscal stimulus package supported by bank credit. The non-financial sector’s debt-to-GDP ratio jumped 26 percentage points in 2009 alone, which is somewhat understandable given the shock from the crisis.

- However, credit growth continued to climb. “Total social financing,” a measure of credit flow to the Chinese economy, rose by about $1 trillion in the first quarter of 2016. The large credit extension should help to boost economic activity in the short term. But it raises questions about whether this is a sustainable strategy.

- A bit of history helps to put things in perspective. China entered the World Trade Organization (WTO) in 2001, and the fruits of belonging to it exceeded expectations. China became the largest exporter and the second biggest importer in the world.

- Exports as a percent of GDP doubled and the direct contribution to growth was substantial. The domestic ripple effects were also large. Excessive business borrowing did not accompany the export-led boom in activity.

- After the GFC, slowing global economic conditions struck a blow to the export sector. Chinese authorities met official growth targets by nudging the growth of debt in the economy as export growth retreated.

- The day of reckoning is not here yet. But history suggests that a debt build up has consequences. In general, China’s economy and financial system are vulnerable and susceptible to shocks when there is a significant accumulation of debt.

- In the 1990s, Thailand and Mexico buckled under the burden of heavy debt. These are relatively small economies, and they had external debt issues. China is a large economy and faces domestic debt problems. The Japanese experience after the 1980s debt boom and the recent U.S. financial crisis following a credit surge are closer to the Chinese situation.

- There is widespread agreement that China’s debt is a threat to economic growth, but the course the economy will take is uncertain. Doomsayers suggest that banks are funded by unstable short-term wealth management products. A loss of confidence in banks could trigger a financial crisis. The less skeptical argue that the People’s Bank of China will provide ample cash to banks experiencing nonperforming loans. About a month ago, a senior Chinese bank regulator assured critics that the banking sector is “stable and risks are under control.” The more pragmatic suggest that China could follow Japan, where sub-par growth and deflation prevailed as authorities postponed appropriate policy actions.

- The International Monetary Fund (IMF) points out that China’s debt problem should be addressed immediately, before corporate debt challenges become a systemic crisis. Its remediation list includes fixing debtor and creditor problems and governance issues to prevent a recurrence of elevated debt levels. Although the IMF’s approach is fitting, such a plan requires an immense political will to face the consequences of cleaning up the Chinese house of debt.

The Long Game

- There is an old joke routinely told on trading desks: “What’s the difference between bonds and bond traders?” Answer: “Bond traders never mature.”

- We may not be able to use that crack much longer. Low long-term interest rates in the developed world are prompting governments to lengthen the maturity of their debt. France and Spain successfully offered 50-year bonds earlier this year, while Belgium and Ireland placed 100-year debt. The average maturity of Treasury debt is at its highest point in 35 years.

- It’s a bit of a wonder why this trend hasn’t been more pronounced. Maturities of government debt remain skewed to shorter tenors in many major markets. Despite negative borrowing costs, Germany has not rushed to issue more long-term debt, even though doing so would improve its budget balance. Why don’t sovereigns move more forcefully in this direction?

- For one thing, yield curves remain upward-sloping in developed markets. This means that issuing short-term debt minimizes borrowing costs, at least in the short term. Short-term issues also offer the flexibility to meet shifting quarterly cash flows, given the irregular timing of federal revenue and expense.

- Some nations may not like to signal that their borrowing needs are so permanent and want to maintain short maturities to make it easier to retire debt if the opportunity arises. The United States has also periodically confronted its debt ceiling, and it can reduce shorter issues to avoid breaching this limit.

- National treasuries also have to listen to their clients, who may not have an unlimited appetite for bonds with very long maturities. Different investors have different time horizons and may not have the flexibility to extend for too long.

- So what seems like an easy decision has its complications. Unless bond traders grow up sometime soon, the old joke will still bear retelling.

© Northern Trust