Summer Reading: Bernanke’s Profile in Courage

At a lunch last month, a group of economists were attempting to understand the roots of the popular discontent that has marked this year’s U.S. presidential campaign. One of our number speculated that it began with the bank bailouts in 2008, which appeared to cushion Wall Street while Main Street slipped into a deep recession. The passage of time, he speculated, has not reduced the bitterness; instead, the inequality of fortune that has persisted in the eight years since has only made people angrier.

I think Ben Bernanke might agree. In his memoire The Courage to Act, which I was finally able to enjoy during last week’s summer sojourn, Bernanke defends the Federal Reserve’s actions during the crisis. But he concedes that the public’s appreciation of those efforts may forever lag their public benefit.

In the interest of full disclosure, I worked at the Federal Reserve from 2008 to 2012. And while I certainly was not a decision-maker during the crisis, I was privy to some of the analysis and logic that supported the choices made back then. So as I began digging into Courage, it was with a somewhat sympathetic ear. Published last fall, the book is only the most recent in a long string of crisis retrospectives. But given the author’s prominence, the book yields some interesting additions to our understanding of those fateful months eight years ago.

Bernanke does not offer much new insight into how we got into the mess that began bubbling over in late 2006. While multiple forces were at play, the Fed cannot escape some blame for holding rates too low and regulating mortgage finance too lightly in the years leading up to the crisis. Bernanke was a Fed governor from 2002 through 2005, and (like others) he failed to raise his voice to express concern.

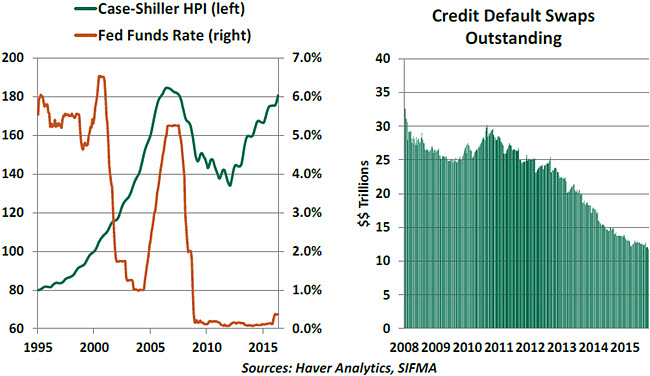

The Fed, among others, also failed to appreciate the rising interconnectedness created by financial derivatives and financial globalization. These linkages were only revealed when the yogurt hit the fan.

If Bernanke was in the background as systemic risk accumulated, he certainly came to the forefront when it surfaced. Constrained by regulatory Balkanization, the Fed nonetheless moved aggressively to stabilize investment banks, insurance companies and federal agencies. Showing incredible creativity, Bernanke’s brain trust (who he affectionately refers to as “the nine schmucks”) designed a series of programs that headed off a worst-case outcome and paved the way for what is now a seven-year expansion.

Bernanke’s account of the darkest days of the crisis vividly illustrates the dynamic of the panic. The rush to the exits of markets was largely behavioral, but it was also accelerated by triggers in financial contracts and trading limits that were not properly understood. Trust eroded, and high-speed platforms were quick to translate anxiety into action. With limited information in hand and immense pressure to perform, the Fed created a firebreak that eventually contained the contagion.  The serial failure of financial institutions would not have been in the public’s best interest. Bernanke offers a spirited defense of the support given to key players during the height of the panic. Letting the firms fail was not an option, because throwing firms into bankruptcy would have triggered contractual and behavioral reactions that would have made matters worse. Nonetheless, the Fed might have used the threat of resolution to allocate the consequences differently, altering bonus payments and settlements on credit default swaps.

The serial failure of financial institutions would not have been in the public’s best interest. Bernanke offers a spirited defense of the support given to key players during the height of the panic. Letting the firms fail was not an option, because throwing firms into bankruptcy would have triggered contractual and behavioral reactions that would have made matters worse. Nonetheless, the Fed might have used the threat of resolution to allocate the consequences differently, altering bonus payments and settlements on credit default swaps.

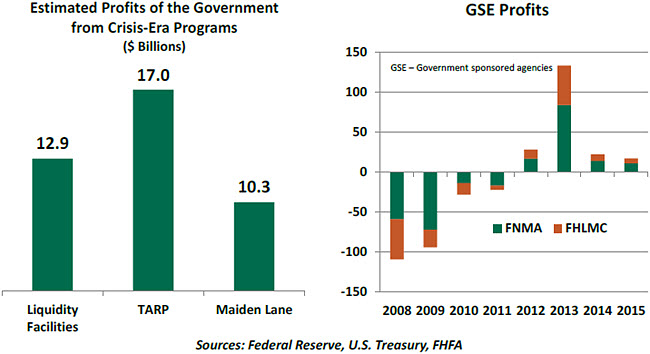

Many still refer to crisis-era assistance as a series of bailouts, but I am not sure that term is appropriate. The consequences for shareholders and senior managers of those companies were substantial. And taxpayers made immense returns on the strategic investments made during the late summer and fall of 2008.

Difficult to account for are the social and financial benefits that accrued to society from avoiding economic disaster. We will never know for certain what might have transpired had nature been allowed to take its course. (Economists refer to these scenarios as “counterfactuals.”) To Bernanke, the costs would have been incalculable, in more ways than one.

Bernanke was not the best marketer of the Fed’s rationale. He did not have the facility with the media that others did, and even his best efforts to promote transparency still left a gap between the Fed’s intentions and public understanding. That gap persists to this day.

The instinct of self-preservation demonstrated by political and regulatory authorities proved that success has a thousand fathers while failure is an orphan. Like the dining partner who refuses to help pick the restaurant but criticizes the choice afterward, Congress tried to wash its hands of responsibility and reserve the right to find fault. During key moments, Congressional leaders seemed more interested in playing to the public than perfecting policy.  Bernanke writes, “It seemed to me that the crisis had helped to radicalize large parts of the Republican Party.” The Tea Party and the End the Fed movement gained strength after 2008, and skepticism about the central bank is a part of both party platforms this year. The Fed is certainly not above review and, occasionally, reproach. But threats to the independence of the central bank must be parried. Had monetary policy been conducted with legislative efficiency eight years ago, we might all have become subsistence farmers.

Bernanke writes, “It seemed to me that the crisis had helped to radicalize large parts of the Republican Party.” The Tea Party and the End the Fed movement gained strength after 2008, and skepticism about the central bank is a part of both party platforms this year. The Fed is certainly not above review and, occasionally, reproach. But threats to the independence of the central bank must be parried. Had monetary policy been conducted with legislative efficiency eight years ago, we might all have become subsistence farmers.

Bernanke has said that “There are no atheists in foxholes and no ideologues in financial crises.” The consequences of moral hazard are difficult to dispute, but teaching miscreants lessons without damaging innocent bystanders is nearly impossible. Alan Blinder’s comment on moral hazard, which centers on the little boy and the dyke, is instructive on this point. Bernanke’s drive to stabilize first and remediate later was undoubtedly the correct strategy.

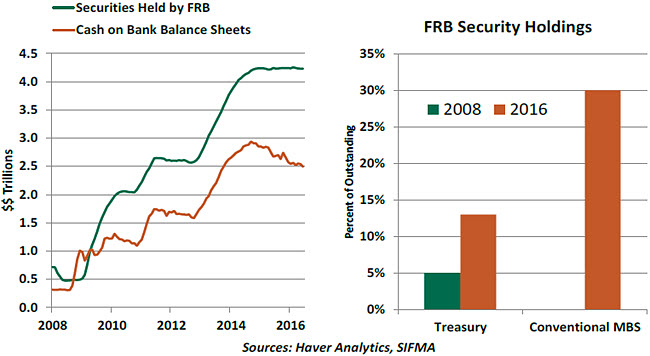

Courage also refers to the pursuit of unconventional monetary policy, which the Fed has applied in a substantial way. Bernanke offers his rationale for beginning and perpetuating quantitative easing, but the final chapter in that effort has yet to be written.

It has become less clear that such programs are beneficial. A large fraction of the reserves injected into the banking system since 2008 remain unlent. Asset price excesses remain a risk. And the exit strategy will be complicated when the time comes, because the Fed now owns a significant fraction of the Treasury and mortgage-backed securities outstanding.

On a personal note, the book facilitated an emotional reminiscence of the darkest weeks of the crisis. The day that Lehman Brothers fell, I was summoned to the New York Fed to assist. It was scary, exhilarating, demoralizing, enlightening and exhausting. It was the most intense and gratifying experience of my career.  I worked there for nearly three months, returning home only for the Thanksgiving holiday. I felt then, and still feel today, that a depression would have started had it not been for the creative and forceful steps taken by policy makers during those challenging weeks.

I worked there for nearly three months, returning home only for the Thanksgiving holiday. I felt then, and still feel today, that a depression would have started had it not been for the creative and forceful steps taken by policy makers during those challenging weeks.

I didn’t exactly expect a hero’s welcome, but I did draw immense satisfaction from playing a small role in the effort to stabilize the financial system. Instead, I was confronted by friends and family members at my Thanksgiving table who were extremely disappointed by the assistance the Fed offered to key financial institutions. It was as if they thought I was personally handing out the cash. Doubts about the crisis resolution remain to this day, even among those who have done relatively well in the years since.

I’m resigned to the notion that outsiders may never fully understand or appreciate what was done in 2008. But for those on the inside, like Ben Bernanke, the intrinsic satisfaction derived from a job well done is reward enough.

Taking Stock of Inventories

The real gross domestic product (GDP) report often contains surprises; inventory investment is usually one of the culprits. The second-quarter assessment was one such example, as inventories detracted substantially from GDP. A look at details seems in order.

Although it is the smallest component of GDP (less than 1%), inventory investment has an important role in short-run variations of GDP growth. An unanticipated increase in inventories could signal future declines in production, and unanticipated drop in inventories may be indicative of a future pickup in production.

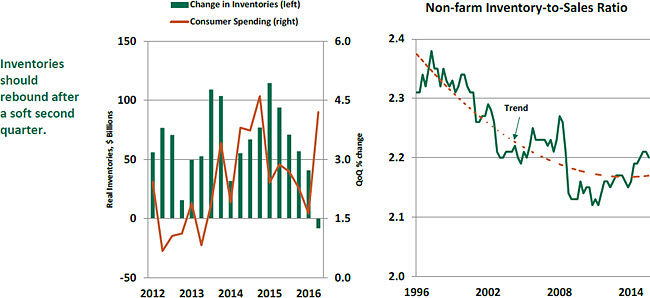

In the second quarter, investment in inventories dropped -$8.1 billion, and it subtracted 1.2 percentage points from the rate of real GDP growth. It was the fifth consecutive quarterly setback to GDP growth from inventories; a similar trend was last seen in the 1950s.

Details of inflation-adjusted data (available for only for April and May) point to a large drop in motor vehicle and petroleum product inventories at the wholesale and factory levels. The Bureau of Economic Analysis includes assumptions about inventories for June in the advance GDP estimate.

The negative level of inventory investment in the second quarter is not sustainable and a resumption of inventory accumulation in the near term is certain. The question is when and by how much inventories will increase.

The timing of a change in inventories is always difficult to pin down. Consumer spending grew at 4.2% annual rate in the second quarter and underlying fundamentals of consumer spending support continued consumer spending growth. This outlook implies that inventories should rebound in the near term.

The inventory-to-sales (IS) ratio for the entire economy offers clues about the likely size of restocking in the quarters ahead. If sales are not improving, firms will pare back production. The IS ratio for domestic business in the second quarter of 2016 stood at 2.21. In other words, it means there was a 2.21-month supply of inventories in the economy.

Historically, the IS ratio has trended down largely due to just-in-time inventory management and technological improvements. The economy-wide IS ratio is not inordinately high, and an expectation of an increase in inventories is reasonable given the extent of destocking that has occurred.

Current projections of GDP include an increase in final sales. The main takeaway is that the contribution of inventories to GDP be positive in coming quarters. Over long periods, quarterly movements in inventory investment are an insignificant component of GDP. But, in the short run, they can befuddle markets.