Augmented reality as a concept has been popularized in recent weeks by the smash debut of Pokémon Go. With the seeming illogic of negative interest rates persisting, the term is also a rather apt descriptor for the global interest rate environment in 2016. With Pokémon-obsessed teens tragically wandering into traffic and off cliffs as they chase virtual prizes and British voters famously Googling ‘what is the E.U.?’ the morning after voting to leave it, a surreal veil has descended on recent market and global events. In this piece, we seek to transcend the surreal and the augmented and focus on reality.

‘BR.EU.mance’ ends as U.K. votes to leave

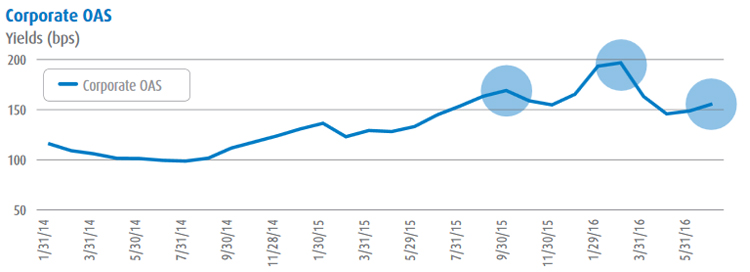

Before the vote, the potential for Brexit weighed on markets in June as sentiment seemed to fluctuate with each new poll. When the Brexit vote did materialize, it came after a period of polling suggesting ‘Remain’ would prevail and the second quarter closed in a bout of volatility. And yet, despite that volatility and the perception of Brexit dominating the quarter, credit spreads and measures of volatility across asset classes ended June lower than at the height of fears in February of this year and the third quarter in 2015. This relatively lower volatility demonstrates just how dislocated markets had been in recent periods.

While the mechanics of Brexit will take years to be worked out, as a market event it has appropriately faded from dominating global discourse to a regional consideration. Nonetheless, certain impacts remain real. Bubbling under the surface are exit movements in other European nations, which could threaten the viability of the E.U. Further, many global growth estimates have been lowered in the aftermath of the vote. For example, the International Monetary Fund reduced its projections by 0.1%, instead of raising them as had been planned absent the vote to leave. While 0.1% is not apocalyptic for the global economy, given the concerns around already sluggish global growth, any hint of slowing is amplified in its significance.

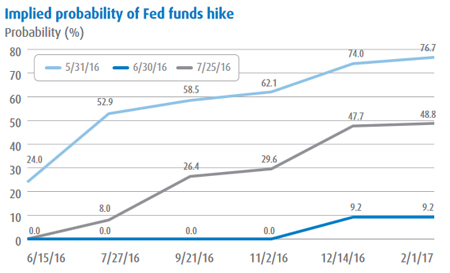

The biggest impact to the U.S. remains in the monetary policy arena, where expectations around Fed rate hikes were reduced to less than 50% even by the end of 2017 in the immediate aftermath of the vote. It is important to realize, however, that the Brexit vote followed on the heels of an awful jobs report in May (11,000 versus 162,000 expected), which in itself had taken a July hike from above a real possibility to a remote one. The subsequent June strong non-farm payrolls (287,000 versus 175,000 expected) and calming of broader market fears have increased expectations of a Fed hike, though they continue to fluctuate. The volatility of the market-implied probabilities of a hike has been significant and bears monitoring with the Fed being keenly aware of market expectations as it considers the timing of the next hike.

Brexit’s other monetary policy impact has been shifting the balance of global central banks further away from the U.S. position. The Bank of England had been viewed as closer to the U.S. camp on the scale of easing versus normalizing prior to the vote. Now it is squarely with the rest of the developed world with expectations for increased accommodation.

The interest rate limbo

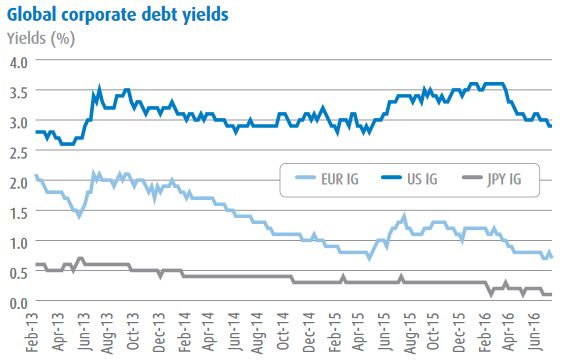

Set against an already low yield backdrop, U.S., British, German and Japanese 10-year government bonds set all-time lows for yields following the Brexit vote and into early July. In our second quarter piece, we noted that an ‘astounding $7 trillion’ of debt was trading with negative yields. Yet, amazingly that number nearly doubled to $13 trillion in the second quarter.

The underpinnings of the global low yield environment – low growth and low inflation – are real. But the extent of European and Japanese negative yields represents the extraordinary efforts of central banks to augment reality to reverse the economic malaise. This campaign entails massive quantitative easing (QE) programs, moral suasion and negative deposit rates.

The support has notably lowered government benchmark rates. Combined with the active purchase of corporate debt by the European Central Bank, a further dramatic step that began in June has created the phenomenon of negative corporate yields. A once unheard of scenario, in early July, over $500 billion worth of European corporate bonds were trading with negative yields. Chasing virtual yellow monsters through real streets seems almost logical by comparison to paying for the privilege of lending money to private companies.

The prevalence of negative rates in the developed world has accentuated the attractiveness of U.S. fixed income as global investors seek yield. We have previously discussed the substitution effect, whereby non-U.S. investors purchase U.S. fixed income assets due to the meaningfully higher interest rate environment in the U.S. versus other developed markets. The recent spate of negative rates has served to further increase the relative attractiveness of U.S. assets.

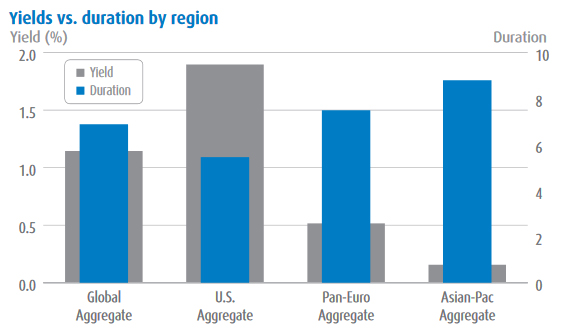

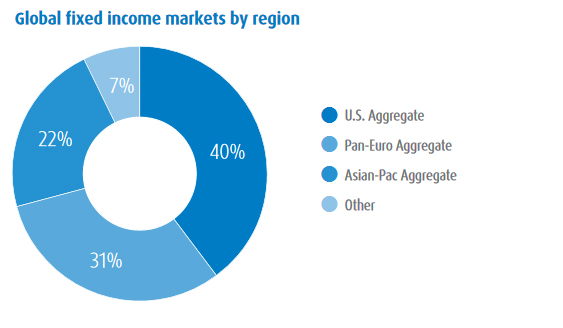

The U.S. bond market offers higher yields compared to developed market peers based on relatively higher growth and inflation expectations. Comprising approximately 40% of the world bond market, the U.S. market, on average, has lower interest rate sensitivity and higher average quality than the global market and the other major regions.

See you in 2116

While the difference in duration between regions is largely a function of relative yields and composition of indices, it is also worth noting that recent months have seen the issuance of significantly longer dated government bonds in the lower yielding regions. These bonds offer higher yield options in developed market government bonds outside of the United States. As rates remain historically low in Europe, the search for yield makes these bonds a stronger consideration than they might otherwise have been.

Ireland and Belgium have issued 100-year bonds while France and Spain have issued 50-year bonds. The longer-dated issuance is a logical step for countries when yields have been pushed as low as they have. Notably though, neither Spain nor Ireland had governments formed at the time of issuance and earlier in the decade Belgium famously went nearly two years without a government. Also noteworthy, many of the countries issuing these long date bonds are the same that five years ago were considered at risk of losing market access.

Looking forward 50 years is a difficult prospect for evaluating much of anything. Looking back 50 years helps illustrate this difficulty. Had Spain issued a 50-year bond 50 years ago, it would have been under the dictatorial regime of General Francisco Franco.

While the ability to analyze these maturity ranges is difficult, these long maturity bonds serve a structural purpose within the market. In addition to those seeking yield, longer maturity securities fit well within a liability matching regime, where similar long horizon uncertainty exists, but can be paired off with long maturity assets. While the U.S. is not extending maturities to such a degree, the Treasury resumed issuing 30-year bonds in 2006 after a several-year hiatus. Resumption of that issuance has served all these purposes, offering higher yield, allowing the government to lock in attractive financing and building out the yield curve for other issuers.

In the 10-year period since 2006, the U.S. fixed income market has matured markedly. The Barclays Aggregate Bond Index (then the Lehman Aggregate Bond Index), a reasonable approximation of the bond market, has more than doubled in size from $8.3 trillion to $19.3 trillion in market value. The growth has come from all major components, including credit and mortgages, not just Treasuries. The number of individual issues in the credit index, for example, has grown from less than 3,000 to more than 6,500, representing a deeper and more diverse universe for investors to select from. At the same time, index duration has extended from sub-5 to 5.5 years as average maturity has lengthened nearly a year in the Treasury component (7.0 to 7.7) and over a year for credit (9.5 to 10.8 years).

Conclusion: separating the yield from the chafe

The economic and monetary policy divergence we have long noted between the U.S. and other developed nations remains a sharp contrast. The Brexit vote, while appearing to be a temporary blip on the global volatility landscape, has again highlighted the relative stability and attractiveness of the U.S. The sharp contrast of the economic and political/policy situations further the appeal of U.S. financial assets, as financial markets remain more intertwined than real economies.

The recent issuance of longer-dated securities is eye-opening in its prevalence. The maturities of these bonds are more extreme, but they are a natural extension of issuers reacting to the low rate environment, their persistent belief that it is an ephemeral moment to be captured and the need for investors to find income in a yield-challenged environment.

For bond buyers, the challenge continues to be separating the yield from the chafe. The evolution of the bond market over the past 10 years has provided a larger sandbox for active managers to add value and with a higher percentage of bonds with negative yields and the accompanying search for positive yield, the importance of sorting the risks has only grown.

In the past quarter, the bond market has made significant strides in returning to a more fundamentals-based as opposed to fear-based valuation of individual credits. Yet, the magnitude of the disruptions in the third quarter of 2015 and the middle of the first quarter of 2016 have left many credits still mispriced in their wake. We have no rare Pokémon to offer enthusiasts, but suggest that a few well-chosen bonds may add more value than a Squirtle. And don’t forget to look up periodically from your augmented reality: be it central bank policy driven negative rates or Pokémon, fundamentals (and oncoming traffic) still matter.

Portfolio positioning

Interest rates/duration: Barbell exposure along the U.S. yield curve to position for flatter term structure with overall duration towards the lower end of relative benchmark range given new lows in absolute yields; Underweight Treasuries, favoring non-government sectors instead

Credit: Global growth concerns have led to a dearth in positive global sovereign bond yields and furthered the demand for U.S. fixed income; U.S. corporate balance sheets have managed the credit cycle well; U.S. IG credit will likely recognize further support from global yield substitution effect

Mortgages: U.S. agency MBS to realize continued support from Fed reinvestment despite potential for increased supply; while the total return potential appears limited relative to cross-sector opportunities, they remain a relative safe haven during periods of uncertainty

High yield (HY) and emerging markets (EM): Market volatility has created bottom-up opportunities in the wake of macro concerns; however, by the numbers, investment grade presents the greater number of opportunities

Taplin, Canida & Habacht, LLC is a registered investment adviser and a wholly owned subsidiary of BMO Asset Management Corp., which is a subsidiary of BMO Financial Corp. BMO Global Asset Management is the brand name for various affiliated entities of BMO Financial Group that provide investment management and trust and custody services. Certain of the products and services offered under the brand name BMO Global Asset Management are designed specifically for various categories of investors in a number of different countries and regions and may not be available to all investors. Products and services are only offered to such investors in those countries and regions in accordance with applicable laws and regulations. BMO Financial Group is a service mark of Bank of Montreal (BMO).