Not All U.S. Dividend-Payers Are Priced Too High

Everyone seems to be looking for yield. But are people looking for yield in all the wrong places?

There’s potential for yield in the fixed-income space, if you’re willing to look outside the government bond market. Jim Kochan showed how U.S. high yield may still be a great place for yield-hunting .

How about the equity markets? The hunt for yield hasn’t hit emerging markets equities yet, and even in the U.S., I think there may be plenty of yield left—and you don’t have to pay up for it.

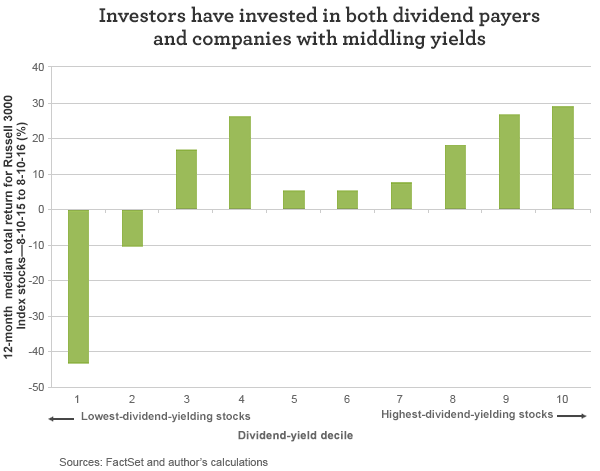

I looked at the constituents of the Russell 3000® Index—which is meant to represent the entire U.S. stock market—and bucketed its stocks into deciles (a decile is 10%) based on dividend yield as of a year ago. For each decile, I then looked at the subsequent median total return and change in price-to-earnings.

The 1st decile (the lowest-dividend-yielding stocks) has dramatically underperformed the 10th decile (the highest-dividend-yielding stocks). Investors have invested in dividend payers, but they have also invested in companies with middling yields (fourth decile). Thus, the market returns haven’t been all about investors scrounging for income.

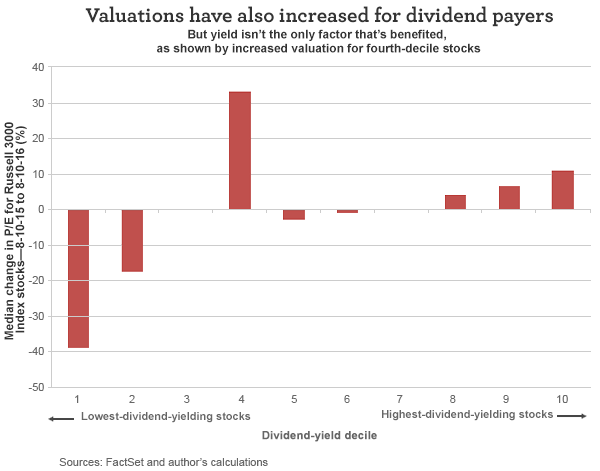

Valuations have also increased for dividend payers, but dividend yield isn’t the only factor that’s benefitted, as shown by the increase in valuation for fourth-decile stocks. Those companies with low dividends have not benefitted, but I think it’s a stretch to say that’s because they lack dividend yield. Whether a stock goes up or down depends on a lot more than just the dividends they’ve paid.

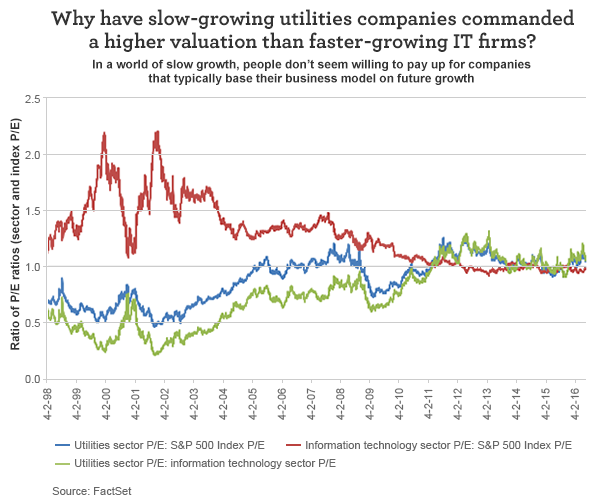

One sector that receives a lot of attention due to its dividend yield is the utilities sector. The dividend yield on the S&P 500 Utilities Index is 3.53% as of August 11, 2016. Granted, there are only 28 stocks in the sector, so it’s not that large. There was quite a bit of attention given to utilities when the valuation (based on price-to-next 12 months’ earnings) exceeded the valuation of the information technology (IT) sector.

Why have slow-growing utilities companies commanded a higher valuation than faster-growing IT firms? It’s a good question, but it’s a question that should have been asked in 2011 when utilities’ valuations first surpassed IT’s. The hunt for yield could be part of it, or it could be because IT is cheap. In a world of slow growth, people don’t seem willing to pay up for companies that typically base their business model on future growth. I think the latter is a dominant force, as shown by how IT’s valuation relative to the broader market was always higher leading up to 2012.

I don’t think the hunt for yield is over, and I don’t think it’s pushed all dividend-paying stocks to too lofty valuations. Some? Maybe—but not all dividend-paying stocks. Keep in mind that the published dividend yield of a stock can change, as there’s nothing that says the dividend has to be paid. A high yield can reflect that the dividend is likely to be cut, so don’t get duped by dividend yields. But, at the same time, don’t be afraid of dividend yields. Just do your homework, or find a portfolio manager that can do the homework for you.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 8-16-16 and are those of Dr. Brian Jacobsen, CFA, CFP®, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Asset Management (WFAM) is a trade name used by the asset management businesses of Wells Fargo & Company. Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management