The subdued performance of the U.S. economy in the second quarter planted doubts about the underlying fundamentals. Is activity going through seasonal doldrums, or is something more fundamental at play?

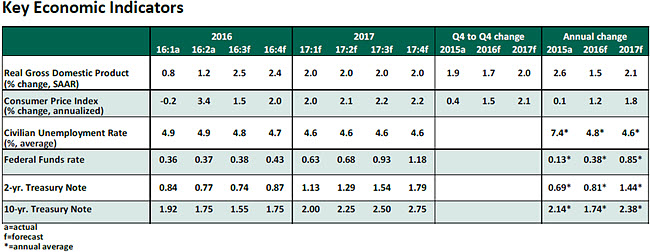

Real gross domestic product (GDP) grew at an annualized 1.2% rate in the second quarter of 2016, far below market expectations. Because this is an advance estimate, revisions will follow in August and September. The decline in inventories was the major highlight of the second quarter GDP report-- inventories have now failed to contribute to real GDP for five consecutive quarters. Inventories are widely expected to snap back in the near term, although the timing is difficult to estimate.

The third quarter began on a strong note with the July employment report. Retail sales numbers dampened expectations, but has only a slight impact because it’s a single data point that will be revised next month. The underlying strong fundamentals of the labor market suggest consumer spending is unlikely to weaken substantially in the very near term.

Key Elements of the Forecast

- The 4.2% jump in real consumer spending during the second quarter was the highest since the fourth quarter of 2014. It was a broad-based pickup, with durables, non-durables and services making significant contributions. It may be difficult to sustain such a strong pace. The sharp increase in auto sales in July (17.9 million units vs 16.7 million units in June) offset the steady performance of July retail sales excluding autos, gasoline and building. It would be premature to significantly downgrade third-quarter consumer spending at the present time.

- Structures and business equipment spending have yet to recover from the slump that began in late 2015. On the negative side, the durable goods report points to weakness in orders and shipments of non-defense capital goods excluding aircraft (considered the less volatile category) for three straight quarters. On the positive side and more recently, the production measure of the Institute of Supply Management’s July manufacturing survey shows the strongest year-to-date reading and factory production recovered in June and July. On net, business spending remains a weak spot in contrast to the strength in consumer spending.

- In the second quarter, new home sales (579,000 units) advanced to a level last seen in 2008 and the level of existing home sales (5.5 million units) stands at the highest level since early 2007. The supply of unsold new and existing homes is below the historical median. Residential investment should have some upside.

- The personal consumption expenditure deflator increased 0.9% from a year ago and the core reading (which excludes food and energy prices) moved up 1.6%. These levels of inflation are below the Fed’s 2.0% target, but other inflation measures are above this threshold.

- In the second quarter, the Employment Cost Index rose 2.3% from a year ago. The change in this index in the last four quarters is high for the current expansion. The firming of compensation costs is consistent with the tightening of labor market conditions. Wage and inflation pressures are gradually building and offer evidence for Federal Open Market Committee (FOMC) members to make a case for a higher policy rate.

- The July employment report showed widespread signs of labor market strength. Hiring rose 255,000 in July, and the unemployment rate held steady at 4.9%. The workweek was longer in July, and the diffusion index, which measures the breadth of hiring gains, rose to the highest level in more than a year. Hourly earnings increased 2.6% from a year ago, the highest increase in seven years, excluding a similar reading in December 2015. Overall, the labor market data suggests that the weakness seen in May is an aberration.

- Brexit does not appear to have significantly affected the U.S. economy. Financial conditions did not tighten as equity prices are up, interest rates are low and the trade-weighted dollar is up only slightly. Outside of the United Kingdom, global economic data also do not yet point to a material impact. These developments justify the Fed’s policy statement following the July meeting that “near term risks to the economic outlook have diminished.” Most importantly, the Bank of England has put in place a strong package of monetary policy support that reinforces this view.

- The 10-year U.S. Treasury note is trading around 1.58%, up from a low of 1.37% following the Brexit referendum. The force of U.S. economic fundamentals has prevailed after transitory concerns about the fallout from Brexit.

- The mix of recent economic data and global economic developments present a stronger case for a higher policy rate when the FOMC meets in September. But we continue to think a raise at the December meeting is more likely. Markets await Janet Yellen’s speech at the Jackson Hole symposium at the end of August, in which she is expected to offer an updated slant on global conditions and monetary policy.