These Olympian Gold Royalty Companies Are Insanely Attractive

In a note this week, UBS echoed its earlier assessment that gold has indeed “entered a new bull run,” as I shared with you last month. The precious metal had a spectacular first half of the year, with total global demand reaching 2,335 tonnes, the second-highest on record, according to the World Gold Council (WGC).

Despite this, gold is still under-owned, accounting for only 3 percent of total ETF assets under management, UBS writes. The group adds there is room for new or returning market participants who might have cleared out their gold positions during the recent bear market.

Driving the bull run, according to the group, are “a prolonged period of depressed real yields” and “elevated macro uncertainty.” These are themes I’ve returned to many times in the past six months, with global government bond yields continuing to drop below zero and economic and geopolitical unrest advancing following the Brexit referendum and ahead of the U.S. presidential election this November.

Confidence in monetary policy and appetite for government debt continues to erode. According to Zero Hedge, foreign central banks dumped a record $335 billion in U.S. Treasuries during the last year. The top seller in June was China, which cleared $28 billion in Treasuries off its balance sheet. Over the same period, the world’s second-largest economy added to its official gold reserves—500,000 ounces in June alone—in an effort to diversify its holdings.

Investors should take heed of the fact that even central banks have become net buyers of gold. It’s always been my recommendation to maintain a 10 percent weighting in your portfolio—5 percent in gold bullion, another 5 percent in gold stocks.

A Superior Way to Gain Exposure to Gold

One of the best ways to play gold, I believe, is royalty and streaming companies. As a reminder, these companies serve as specialized financiers to explorers and producers. In return for upfront financing, they can receive one of two different types of payments. In one way, they can receive a royalty, or percentage, on whatever future sales the debtor company makes during the life of the mine.

In another way, they can buy a stream of precious metals at a low, fixed price. Discounts on gold, for instance, could be as much as 75 percent. This has typically been the preferred method for paying back the royalty company.

Some of our favorite names in this space include Franco-Nevada Mining, Silver Wheaton, Royal Gold and Sandstorm Gold, all of which have outperformed underlying gold for the 12-month period. Click the hyperlinks to read my special reports on Franco-Nevada and Silver Wheaton.

Better Allocators of Capital

Royalty and streaming companies show great opportunity on the upside but avoid many of the risks and operating expenses that explorers and producers must deal with.

Interestingly, they all employ a small group of technically skilled mining geologists, engineers, metallurgists and financial mining executives to analyze and monitor their investments.

Because they’re not responsible for buying mining machinery and building, operating and maintaining mines, they have a much lower total cash cost per ounce of gold than miners do. (In this context, cash cost refers to operational expenses that are paid using cash, rather than credit.) Their overhead is kept at a minimum, and they have some of the highest sales per employee in the world. As you can see below, their debt per share is much lower than senior miners Newmont Mining and Barrick Gold—the Army to royalty companies’ more agile and tactical Navy SEALs. Last year, Barrick cut $3.1 billion in debt last year and is on track to pay down an additional $2 billion this year.

Their margins have typically been much larger than traditional explorers and producers, allowing them to remain profitable even during gold bear markets.

Take Sandstorm, one of the younger royalty companies. Its second-quarter cash cost per ounce of gold was a mere $261, giving it operating margins of $994 per ounce.

Compare this to Barrick, the world’s largest gold producer. Barrick reported cash costs of $578 per ounce, nearly double that of Sandstorm—and Barrick has some of the lowest costs compared to other miners, according to Motley Fool.

| Mining Companies | Royalty Companies | |

|---|---|---|

| Precious metals price upside | X | X |

| Exploration upside | X | X |

| Production rate upside | X | X |

| No sustaining costs | X | |

| No exploration costs | X | |

| No capital expense overruns | X | |

| Fixed cash costs | X |

Investors like royalty companies because they’re a skilled team of former miners and mining executives who generate substantially greater gross margins and have materially fewer employees, with less general and administrative expense.

Further, they offer spectacular optionality. They often buy an asset with a payload over 10 years. However, these deposits often extend for 30 years, so they have potential for a much bigger payback. If the mining company expands production, it’s free additional cash flow, and if they make a large discovery near the producing mine, the royalties have free upside growth.

For further reading, one of the strongest overviews of royalty companies is Streetwise Reports’ “Precious Metal Royalties: The New Landscape.”

A New Entrant

Just as there still might be ample scope for gold investors to participate in the market, one CEO is betting there’s still room for another entrant into the precious metals royalty company space. Long-time precious metals commentator David Morgan recently helped found Lemuria Royalties, which reported in June that it had acquired its first silver royalty from a Peruvian mine operated by a subsidiary of Fortuna Silver Mines.

In January of this year, Morgan summed up his reasoning for establishing a new royalty company: “We favor the streaming and royalty companies a great deal because the risk is very low relative to, let’s say, an exploration company or even a producing company.”

This is precisely why we continue to find the royalty business model very attractive.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.13 percent. The S&P 500 Stock Index fell 0.01 percent, while the Nasdaq Composite climbed 0.10 percent. The Russell 2000 small capitalization index gained 0.57 percent this week.

- The Hang Seng Composite gained 0.87 percent this week; while Taiwan was down 1.27 percent and the KOSPI rose 0.28 percent.

- The 10-year Treasury bond yield rose 6 basis points to 1.58 percent.

Domestic Equity Market

Strengths

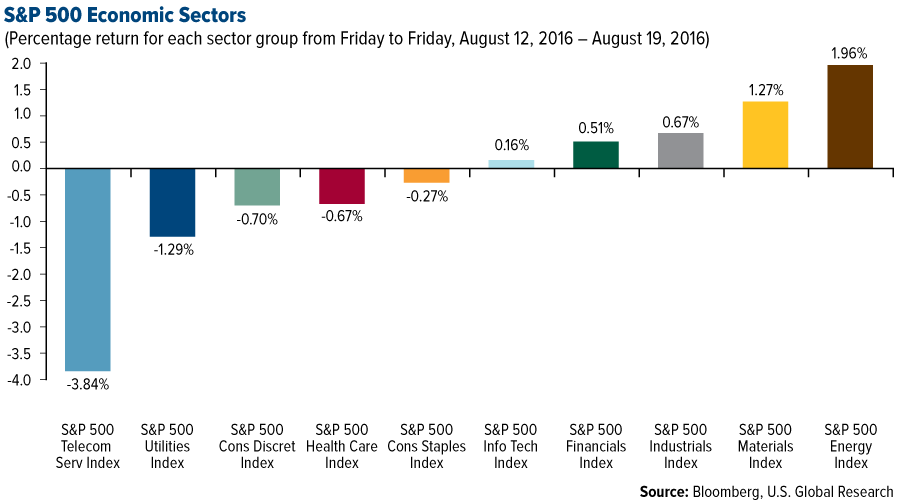

- Energy was the best performing sector for the week, increasing by 1.96 percent versus an overall decrease of -0.02 percent for the S&P 500.

- Urban Outfitters was the best performing stock for the week, increasing 23.36 percent. The company’s shares surged after its sales and earnings outpaced Wall Street estimates, helped by new fashions that resonated well with consumers.

- Netapp surged 22 percent during the week as the data management and storage company swung to a profit in the fiscal first quarter.

Weaknesses

- Telecommunications was the worst performing sector for the week, falling by -3.84 percent versus an overall decrease of -0.02 percent for the S&P 500.

- Verisign was the worst performing stock for the week, falling -9.85 percent.

- Prison stocks crashed this week. The Department of Justice is phasing out contracting to privately run prisons, according to a memo. After this news crossed, shares of Corrections Corporation of America, the largest publicly traded prison provider, fell in half, while Geo Group fell by more than 40 percent. Trading in both shares was halted for volatility. Private prisons are less secure than those run by the Federal Bureau of Prisons, the DOJ said.

Opportunities

- Walmart, the world's number-one, brick-and-mortar retailer reported second-quarter adjusted earnings per share of $1.07 ($1.02 estimated), revenue of $120.9 billion ($120.3 billion estimated), and raised its outlook for full-year EPS. Sales at stores open for at least one year were positive for a seventh straight quarter.

- Home Depot reported second-quarter earnings that met and raised its full-year outlook amid a strong U.S. housing market.

- Urban Outfitters beat on the top and bottom lines. The retailer earned an adjusted $0.66 a share on revenue of $890.6 million, easily beating the $0.55 and $885.6 million that analysts were expecting. Comparable-store sales unexpectedly rose 1 percent, outpacing the 1.2 percent decline that was expected. "These results were driven by a positive retail segment 'comp' and substantial improvement in merchandise margins," CEO Richard Hayne said in the earnings statement.

Threats

- Target struggled to sell electronics in the second quarter, especially Apple products. The retailer reported earnings that were stronger than expected, but it lowered its outlook for the rest of the year as it plans for a "challenging environment," according to CEO Brian Cornell.

- T. Rowe Price is suing Valeant Pharmaceuticals, alleging fraud. The mutual fund, which invests in the company, alleges that Valeant is running a "fraudulent scheme" through its now shuttered pharmacy, Philidor.

- Volkswagen could face civil and criminal penalties because of its emissions scandal. The German automaker has been found liable for criminal wrongdoing by the U.S. Department of Justice, CNBC reports. Volkswagen may be forced to pay damages that exceed Toyota's $1.2 billion settlement, the largest on record, for intentionally concealing acceleration problems.

![[thumb]](/images/content_image/data/62/62cb569ada1842b6f1b91159c7f8fbbe.jpg)

August 18, 2016Gold Spending in India Is Set to Get a Boost from a Strong Monsoon Season |

![[thumb]](/images/content_image/data/a5/a58b173de776d3f0dca249ae8dcb6af8.jpg)

August 15, 2016Go Gold! |

![[thumb]](/images/content_image/data/fc/fc52bcaa60b10b9bbf0537a80edf0f1d.jpg)

August 11, 2016The Olympic Games Reflect Our Love of Gold |

The Economy and Bond Market

Strengths

- Housing starts unexpectedly jumped 2.1 percent at a seasonally adjusted annual rate of 1.21 million in July. It was only the third time since the Great Recession that starts surpassed 1.2 million.

- Initial jobless claims fell more than expected last week, by 4,000 to 262,000. Claims have now been below 300,000 for 76 straight weeks — the longest stretch since 1970.

- U.S. industrial production picked up in July. Output rose in all sectors: manufacturing, utilities and mining, according to the Federal Reserve. The 0.7 percent monthly advance was the largest since November 2014. A weaker U.S. dollar and firmer commodity prices contributed to the improvement, economists said.

Weaknesses

- The Consumer Price Index was flat in July, depressed by lower energy costs.

- As expected, the Philly Fed index improved to 2.0 in August from -2.9, suggesting expansion in manufacturing activity. However, the details of the report were much weaker than the headline. If you look at the ISM-adjusted Philly Fed index, which averages five components of the report like how the national ISM index is computed, it deteriorated to 45.4 in August from 49.9.

- The debate over the path for U.S. interest rates heightened as hawkish comments from another Federal Reserve regional chief sent Treasuries and stocks slumping. Benchmark 10-year notes halted a two-day rally after San Francisco Fed President John Williams said the central bank’s September meeting is “in play” for a rate hike.

Opportunities

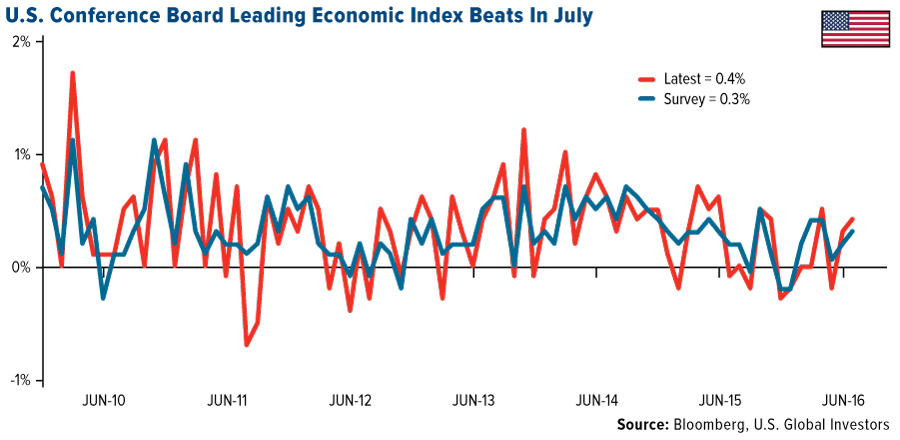

- The Leading Index reading for July beat the survey expectations. This is a bullish forecast for the economy.

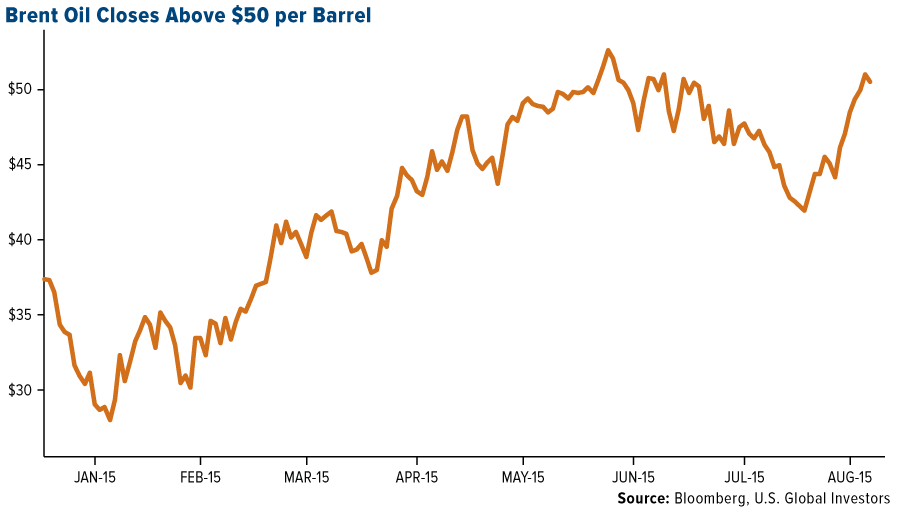

- The market for Brent crude oil has shifted from a bear market to a bull market in just over two weeks. Prices have risen over 20 percent since August 2, with the latest surge tied to the possibility of an OPEC output cap being negotiated at long last. Brent crude ends the week above $50 per barrel for the first time since late June.

- Flash readings of the Markit purchasing managers' indices are released globally on Tuesday, August 23.

Threats

- According to Nautilus Investment Research, with the U.S. dollar index having fallen below the 100-day moving average, a "major long-term trend change" is about to take place. The firm’s research found the index's performance in the three months following a break below the 100-day moving average is a loss of 3.29 percent on average during a three-month period, compared with the typical loss of 0.02 percent over the same time frame.

- The Fed is worried about a couple of things. The minutes from the July FOMC meeting had a little bit of everything, suggesting the Fed still wasn't sure when the next rate hike would occur. While there were numerous positives, the Fed suggested it was particularly worried about banks in Italy and stretched valuations in the U.S. commercial real estate market.

- Subprime credit-card lending is making a comeback. TransUnion's second quarter 2016 Industry Insights Report shows that 11 percent of the 10 million new customers entering the credit-card marketplace in the past year were subprime borrowers. Additionally, the data suggests subprime borrowers are seeing the biggest increase in balances, up 14 percent versus a year ago.

Gold Market

This week spot gold closed at $1,341.47, up $5.62 per ounce, or 0.42 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, fell 3.42 percent. Junior miners outperformed seniors for the week, as the S&P/TSX Venture Index came in nearly flat for the week with a slight loss of 0.02 percent. The U.S. Trade-Weighted Dollar Index was off 1.25 percent, despite the rally on Friday.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Aug-16 |

Germany ZEW Survey Current Situation |

50.2 |

57.6 |

49.8 |

|

Aug-16 |

Germany ZEW Survey Expectations |

2.0 |

0.5 |

-6.8 |

|

Aug-16 |

U.S. Housing Starts |

1180k |

1211k |

1186k |

|

Aug-16 |

U.S. CPI YoY |

0.9% |

0.8% |

1.0% |

|

Aug-18 |

U.S. CPI Core YoY |

0.9% |

0.9% |

0.9% |

|

Aug-18 |

U.S. Initial Jobless Claims |

265k |

262k |

266k |

|

Aug-23 |

U.S. New Home Sales |

580k |

-- |

592k |

|

Aug-25 |

Hong Kong Exports YoY |

-2.0% |

-- |

-1.0% |

|

Aug-25 |

U.S. Durable Goods Orders |

3.5% |

-- |

-3.9% |

|

Aug-25 |

U.S. Initial Jobless Claims |

265k |

-- |

262k |

|

Aug-26 |

U.S. GDP Annualized QoQ |

1.1% |

-- |

1.2% |

Strengths

- The best performing precious metal for the week was palladium, up 3.57 percent. Speculators have been piling into platinum and palladium futures, largely based on improved car sales in China, but position sizes are approaching all-time highs for both metals.

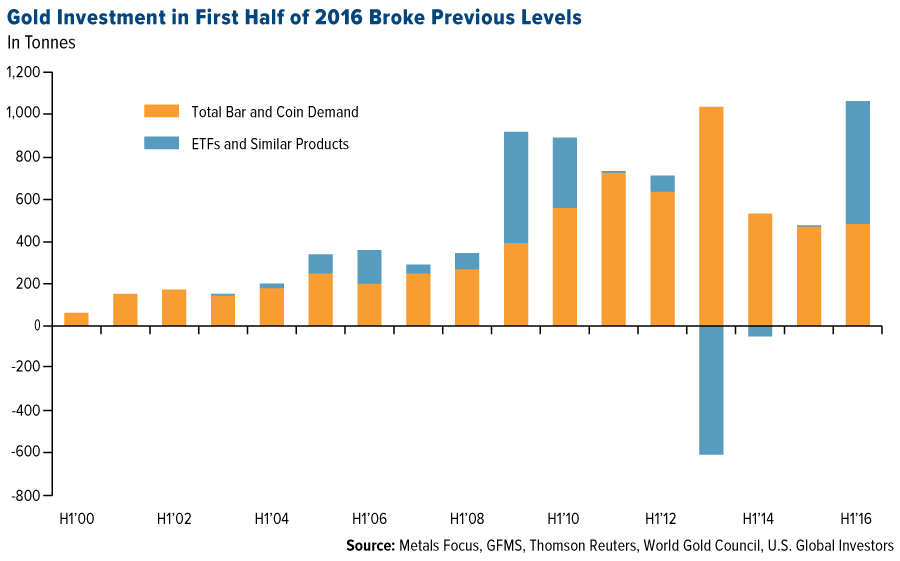

- Gold investment in the first half of the year broke previous levels, as seen in the chart below, with both coin and bar demand, as well as ETF product demand, soaring to record levels. Gold demand will get another boost in India as wedding season starts to heat up, particularly with the metal currently trading at a $40-$50 discount in the country, reports Bloomberg. Bullion traders noted persistent buying by jewelers at domestic markets to meet festive season demand.

- Gold got a boost on Thursday on dollar weakness following the release of the Fed minutes, which showed that U.S. interest rates should stay low. According to futures prices compiled by Bloomberg, the odds of an increase in borrowing costs in December fell to 49 percent from 51 percent a day earlier. “From looking at the data, and looking at the minutes, I don’t think we’re any closer to a rate increase,” Chris Gaffney, president of EverBank World Markets said.

Weaknesses

- The worst performing precious metal for the week was silver with a 2.05 percent fall, of which most of the losses came on Friday when we had renewed strengthening of the dollar.

- There have been a number of mixed signals from Federal Reserve policymakers this week, sending gold lower on Friday. The jawboning from these officials include a comment from New York Fed President William Dudley, for example, who reinforced his confidence in a possible rate hike for the second time in a week, reports CNBC. Bullion for immediate delivery fell 0.5 percent an ounce in London, reports Bloomberg, as other officials say the U.S. is strong enough to warrant an increase in interest rates sooner than markets expected.

- Gold consumption in China fell during the first half of the year, primarily due to a surge in price by 24.6 percent, reports Bloomberg. The Asian nation did keep its top spot as the world’s leading gold producer, however, for the ninth-straight year. Similarly, as the foreign currency crisis deepens in Venezuela, the country’s international gold reserves slumped 25 percent in the first half of the year as they swapped gold for dollars.

Opportunities

- According to a piece from SmarterAnalyst.com, the FOMC members see the futility in their tools and announced this week that the Fed is rethinking its monetary stance. President of the St. Louis Fed James Bullard explains that the old model was a long-run equilibrium which averaged past economic variables. The new model, however, includes a set of possible regimes that the economy may visit and are not forecastable. The Fed’s new framework would be positive for gold, the article continues, as it would lower market expectations of interest rate hikes and support the price of the shiny metal. It makes the Fed even more agnostic and less inclined to provide clear guidance.

- CNBC reports that gold’s relationship with stocks reached an all-time low in the 60 sessions through Wednesday’s close. The correlation between gold futures and the S&P 500 was -0.63, the lowest ever between gold and stocks based on CNBC analysis of Factset data going back to 1984. This could be a reason for many investors to buy gold, as the “two unrelated assets will together have a smaller amount of volatility than two identical assets, all else being equal.”

- Global central banks dumped a record $335 billion in U.S. debt over the past year, according to an article from Zero Hedge. While the author points out his expectation that Saudi Arabia would be one of the biggest sellers (or other “petrodollar-reliant nations”), China, Japan and Hong Kong were the largest sellers of Treasuries in June. The largest buyer in June was the Cayman Islands with purchases of $28.3 billion – another name for “hedge funds,” the author states.

Threats

- As Islamist militants pose a growing threat at mines in Burkina Faso, the government announced plans to deploy more than 3,600 soldiers and police to secure its mines, reports Bloomberg. According to Francois Etienne Ouedraogo, the head of the National Office for Securing Mining, the police and soldiers will be “deployed gradually” at the 18 mine sites in Africa’s fourth-largest gold producer. In a report from the IMF last June, the group said that fragile security is one of the main threats to the nation’s economic outlook.

- Gold equities have re-rated to historical peaks or above, reports Morgan Stanley, with an average 24 percent upside to spot gold already priced in. Similarly, analysts at UBS believe that mining stocks have priced in the gold bull run, and that the underlying metal provides more upside than the stocks. Despite gold being one of the top performing assets year-to-date, the metal’s 26 percent gain pales in comparison to the 110+ percent average lift across the senior producers, UBS continues.

- A piece from All Africa Global Media this week points out that the lethal toll of informal gold mining is on the rise. Although deaths at formal mines have come down (fatalities numbered 77 in 2015, making it the least deadly year on record), “zama-zama” or informal fatalities have gone up. By 2015, the official number of informal mining fatalities reached 124 (a 150 percent increase in reported informal mining deaths from three years prior).

Energy and Natural Resources Market

Strengths

- Brent crude prices topped $50 per barrel as analysts suggest the rally will persist in the mid-$50 range. Prices have roared back to enter a bull market fueled by a drop in U.S. inventories. Macquarie’s oil economist Vikas Dwivedi believes the current crude oil rally will persist into the low- to mid-$50 per barrel range.

- The best performing sector for the week was the S&P 500 Oil & Gas Exploration and Production Index. The index of major U.S. oil producers rose 3.7 percent on the back of strong crude prices, which continued to outperform after a drop in U.S. inventories.

- Unit Corp, an Oklahoma-based junior oil and gas producer was the best performing stock in the broader natural resource space for the week. The stock gained 17 percent supported by bullish sentiment and a crude oil rally as U.S. inventories dropped for the first time in four weeks.

Weaknesses

- Platinum group metals (PGMs) could be at risk as self-driving cars continue to make headlines this week, reports Macquarie. On Tuesday Ford announced that it aims to sell a ‘high volume’ of self-driving cars by 2021; on Thursday Uber said it would begin a trial run of self-driving cars in Pittsburgh this month. While self-driving cars remain a long way from going mainstream, they could eventually reduce the number of cars sold each year, reducing PGMs demand.

- The worst performing sector for the week was the NYSE Arca Gold Miners Index. The index of major gold producers dropped 3.4 percent for the week, underperforming the commodity. The move came after UBS published a report calling for investors to rotate into the physical commodity, from the equities, as the equities have already priced in the upside.

- The worst performing stock for the week in the broader natural resource space was Newcrest Mining Ltd. The major Australian gold producer dropped 6.7 percent after the UBS report recommended selling and it suggested there could be more upside in the commodity than in the stocks.

Opportunities

- The cyclical highs for the U.S. dollar are behind us, according to Renaissance Macro. Jeff DeGraaf, RenMac’s head technical analyst suggests the U.S. dollar is putting in an 18 month top, which should lead to a shift in market sentiment. Such a move would take a lot of pressure off of China’s currency, and would help boost commodities and overall risk-on sentiment.

- Steel industry participants are increasingly positive on the outlook for this fall, reports Macquarie. With profit margins having improved, and the “golden season” for construction ahead in September and October, traders are planning to increase inventories and mills to lift production and restocking of raw materials at the same time.

- The U.S. oil rig count rose for an eighth-straight week, a first since 2011. U.S. oil and gas producers increased drilling activity for an eighth week in the longest string of gains since July 2011, reports Bloomberg. The increase in rigs may suggest that producers are comfortable assuming risks at these levels, boosting activity in the space as a result of the 63 percent crude rally over the last six months.

Threats

- Copper prices will slide from today’s levels and remain subdued until the end of the decade, according to Macquarie Research. Despite fast-recovering construction activity in China, anticipated stronger mine output in the second half of 2016, suggests that the market will continue to be in surplus ranging from 290-370,000 tonnes per annum through 2019.

- BHP CEO Andrew Mackenzie provided a gloomy outlook for the steel and iron ore market. In his view, the recent rise in iron ore prices is temporary, driven by stimulus measures in China and a slower ramp-up of new low-cost supply. However, he argues that iron ore prices have more risk to the downside as the cost curve "should continue to flatten as new seaborne supply ramps up," and Chinese steel production begins to soften over the rest of the calendar year.

- Rising supply drives negative sentiment in paper and forest. UBS analysts report that suppliers comment that current high inventories and capacity growth is likely to prevent a sustainable price recovery. A total 1.5 million tonnes per annum of new softwood capacity are expected to come online, which according to UBS will weigh on fundamentals.

China Region

Strengths

- The Shanghai Composite Index rose 1.91 percent, finishing as one of the strongest performers in the region despite pulling back from multi-month highs made earlier in the week. The Index jumped in expectation of an imminent announcement of a new Shanghai-Shenzhen stock connect program. Although some of the chronological details with respect to the new stock connect program’s timeline are still forthcoming, markets generally savored the anticipation of the announcement before a bit of profit-taking on the news.

- Nexteer Automotive Group Ltd. (1316 HK) was the best performer in the Hang Seng Composite Index over the last five trading days, soaring nearly 39 percent in that time to new 52-week highs after the auto parts manufacturer reported better-than-expected revenue in the first half of the year along with good EPS numbers.

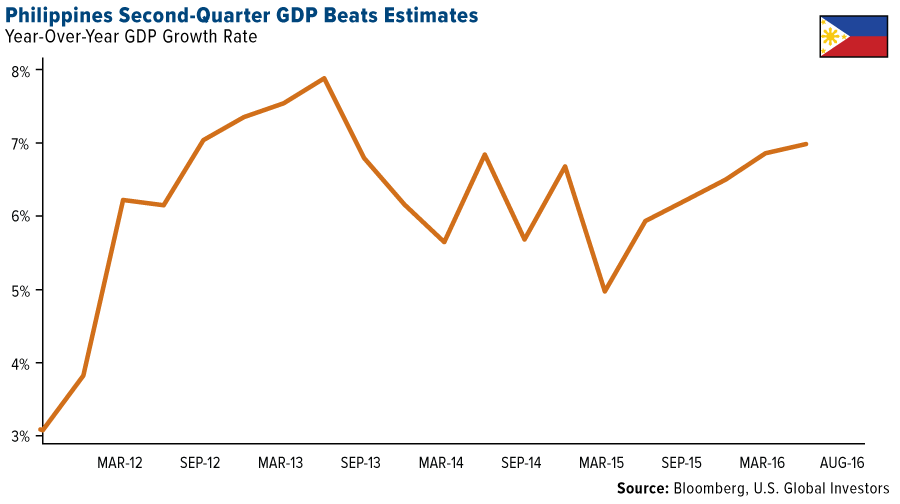

- The Philippines reported a year-over-year second quarter GDP growth rate of 7.0 percent, surpassing analyst expectations for 6.6 percent, while quarter-over-quarter GDP came in in-line at 1.8 percent.

Weaknesses

- Thailand’s SET Index dropped 0.71 percent for the week, falling in the five trading days following last week’s bombings in tourist destinations, and making Thailand the worst performer in the region during the timeframe.

- China State Construction International Holdings Ltd. (3311 HK) fell more than 17 percent for the week, as the construction and civil engineering company reported first-half margins and core earnings that failed to meet analysts’ expectations.

- Retail sales for the June period in Singapore missed expectations for a gain of 2.0 percent, coming in at a gain of only 0.9 percent year-over-year growth. Month-over-month June data missed as well, with a decline of 1.5 percent falling short of an anticipated gain of 0.7 percent.

Opportunities

- MGM Resorts International announced that it will increase its stake by 4.95 percent in MGM China Holdings, meaning the company will own around 56 percent of MGM China’s outstanding common shares. “MGM Resorts is committed to the long term growth of Macau as a premier international tourism destination,” said Jim Murren, Chairman and CEO of MGM Resorts.

- Tencent’s second-quarter sales and profit beat analysts’ estimates this week, reports Bloomberg, as users surged and online advertising revenue grew 60 percent. Tencent’s shares, which rose 5.2 percent on Thursday to a record in Hong Kong, is paying up front for popular media titles in order to tap the purchasing power of its users and appeal to advertisers.

- “China has launched a 200-billion-yuan, government-backed venture capital fund as part of Beijing’s move to shake up its bloated state sector and foster innovation in the overall economy,” writes the South China Morning Post. The State Council approved the fund, which serves as an attempt to consolidate state assets in more “market-friendly” ways, rather than direct administrative orders.

Threats

- According to reports from Chinese state media this week, pollution as well as overfishing is depleting the Asian nation’s fishery resources, reports Bloomberg, including the East China Sea where there “are virtually no fish left.” The fishing industry generates more than $260 billion annually, or 3 percent of Chinese GDP, the article continues, and China accounted for 35 percent of the world’s seafood consumption last year. The government recognizes that the annual sustainable catch limits are routinely exceeded by 30 percent or more.

- On Wednesday, the Ministry of Public Security said that police in China busted underground banks handling around 200-billion-yuan in illegal money transfers this year, reports Reuters. The Ministry reported the arrest of 450 suspects involved in 158 cases of underground banking and money laundering. According to the article, Beijing has been fighting illegal cross-border outflows in an attempt to slow capital flight as the yuan currency weakened to near six-year lows in recent weeks before recovering of late.

- Following a recovery in home prices and sales in China during the first half of the year, July numbers showed signs of easing, reports Reuters, adding to concern that a key growth driver for the economy is losing steam. Policymakers concerned about property bubbles, however, may find relief in the slowing price growth and weakening property investment.

Emerging Europe

Strengths

- Romania was the best-performing country this week, gaining 1.75 percent. GDP grew 6 percent as of the second quarter on year-over-year basis, and 1.5 percent on a quarter-over-quarter basis. The government of Romania supports growth and the country is now one of the fastest growers in Europe.

- The euro was the best currency this week, gaining 1.4 percent against the dollar. Currencies appreciated as the dollar weakened on speculations that the Federal Reserve will not hike rates in September.

- The energy sector was the best-performing sector among Eastern European markets this week.

Weaknesses

- Greece was the worst-performing market this week, losing 2.6 percent. Greece announced that building activity (measured by the number of new building permits issued) decreased by 31.5 percent year-over-year in May, and exports fell by 8 percent in the first half of 2016 – the third largest drop in the 28-member European Union.

- The Ukrainian hryvnia was the worst-performing currency this week, losing 80 basis points against the dollar. Escalation of the Russia/Ukraine conflict, spurred by Russia’s annexation of Crimea two years ago, put pressure on the country’s currency. The president of Ukraine, Petro Poroshenko, said he wasn’t ruling out a full-scale invasion by Russia as tension is rising rapidly.

- The utility sector was the worst-performing sector among Eastern European markets this week.

Opportunities

- U.K. retail sales unexpectedly surged in the month after the nation voted to leave the eurozone area. Retail sales rose 1.4 percent month-over-month in July, well ahead of forecasts of a 0.2 percent rise. Warm weather and the plunge in the pound, which boosted tourism spending, contributed to the jump in retail sales volumes.

- On Monday, Russian equites reached the highest level in the last year supported by the rebound in oil prices. Even after a rebound in crude prices this year, Russia’s Micex Index lags its peers and it has the lowest price-to-estimated-earnings ratio among countries included in the MSCI Emerging Markets Index. That may lure investors into Russia seeking profits in riskier, higher-yielding assets as global central banks keep rates close to zero.

- Emerging market equites may continue to advence on speculations that the Fed will keep rates low for longer. Emerging market currenies may keep climbing higher against the dollar as the dollar slides lower. This week dollar slid to an almost-three-month low as investors doubt that the rate hike will materialize soon.

Threats

- Fitch will announce its credit rating for Turkey late on Friday and if Fitch decides to cut, Turkey will lose it investment grade. The credit rating agency currently rates Turkey at BBB-, with a stable outlook. Fitch was the first international credit rating agency to upgrade Turkey to investable level in November 2012. Moody’s rates Turkey at investment grade and has put the country under review for possible downgrade after the failed coup attempt. Standard & Poor’s rates Turkey below investment grade.

- On Tuesday the Polish government published 21 top court rulings which it previously declined to recognize, but this move still did not erase EU rule-of-law concerns. The European Commission says these publications address “some but not all” EU recommendations.

- Russian’s finance ministry released estimates for the federal budget deficit that were higher than expected. Russia’s budget deficit was 3.3 percent of GDP, RUB 1.52 trillion (US$23.8 billion) in the first seven months of 2016 and ahead of the 3 percent cap that President Vladimir Putin called at the start of the year. Oils and gas revenue are substantially behind target having reached just RUB 2.5 trillion or 42.2 percent of the full year goal, while non-oil and gas revenue reached RUB 4.4 trillion or 57.4 percent of the full-year target.

© US global Investors