“Positive anything is better than negative nothing.”– Elbert Hubbard

“Once you replace negative thoughts with positive ones, you’ll start having positive results.”

– Willie Nelson

If you have any doubt that we’ve wandered into a new and unexplored economic universe, consider this number: $12.6 trillion. That’s the face value of government and corporate bonds currently trading worldwide with nominal yields below zero.

Note that word trading. These bonds are in fact trading. Liquidity has not dried up. An active market exists for negative-yield bonds. Buyers haven’t gone on strike, and sellers aren’t desperately dumping the bonds. This is weird. None of it should be happening. Plainly, however, it is happening.

Have traders and investors lost their minds? No. They are making the most rational decisions they can in an increasingly irrational world. And therein lies the problem with negative interest rate policies, or NIRP, as we now call them (not so fondly).

We don’t have infinite choices. Our decisions spring from the alternatives available to us. When all the alternatives are bad, any choice we make will be bad, too. Today we will start a two-part series on how central banks and specifically NIRP are hurting the global economy. First, a little background.

The Price of Liquidity

What is an interest rate? You might describe it as the price of money, or in investment terms it is the price of liquidity. You don’t have cash now, but you expect to have it in the future. If a lender believes your expectation is plausible, you can borrow the cash now in exchange for promising to replace it tomorrow. But you don’t just replace what you borrowed. You add an additional amount to compensate the lender for giving up liquidity on that money. That additional amount is what we call interest.

Now, thinking through this lending scenario, is there any way in which negative interest makes sense? Maybe. It makes sense if liquidity is undesirable. Or it makes sense, at least to some central bankers, if you want to make liquidity undesirable in order to encourage people (and lenders) to take more risk. However, the data is all beginning to show that consumers and even some businesses are actually saving more money in low-interest-rate or negative-interest-rate environments.

Why would liquidity be undesirable? It would be if there was nothing of value to buy with your money. If you’re lost in the desert, having a thousand dollars in your pocket does you no good. You would trade it all for a gallon of water. There isn’t any water, so your money is worthless. So is your credit card.

How can undesirable liquidity pertain in a whole economy? Cash is useful to the extent that you can buy goods and services, but you can only buy so much. Beyond a certain point, liquidity becomes bothersome because you have to store and protect it. This effort consumes time – the one resource we can’t replace.

Is it coincidence that cash is losing value at the very time technology has brought the whole world to our fingertips? What would the knowledge you can now get for free on the internet have cost in the 1970s? Quite a lot, I assure you.

I say all this to make a point: Even if we didn’t have central banks manipulating interest rates, rates might be very low just by virtue of our modern technology and circumstances. I actually think they would, but that is not an experiment we will be able to run. I’m just speculating about what might happen – which, come to think of it, is what central banks now do. They speculate that their radically new actions will have particular results, but they have no empirical evidence to verify that this is true. So when you add central banks to the equation, interest rates get even lower because they manipulate them down. But that’s quite a different scenario than the below-zero yields we see in Europe and Japan right now – and may well see in the US when the next recession strikes.

NIRP Problem #1: Failure to Stimulate

The Federal Reserve’s mission is to maintain a stable inflation rate while spurring employment. Its main tools are control over the money supply and interest rates. Lately exercising that control has meant keeping interest rates extremely low, especially by historical standards.

That’s simple enough, but recognize the grand and unproven assumption here: Lower interest rates will create higher demand for goods and services. If that’s true, the Fed can stimulate economic activity by pushing rates lower and keeping them there.

But is it really true? Certainly not for the last eight years. We’ve had short-term rates near zero the entire time and long-term rates at historical lows. Yet, as measured by GDP or any other standard, economic growth has been mild at best. This dearth of desired results is a real problem for central bankers everywhere

It gets worse. Not only have very low or negative interest rates failed to stimulate demand, they have arguably reduced demand as people save more and spend less.

Why do people do this? Imagine you’re a retiree trying to live off the interest on your savings. In order to get any income at all, you’ve had to take on more risk by holding long-maturity bonds, junk bonds, preferred stocks, etc. You compensate for this risk by giving yourself a bigger savings cushion. That means you have to reduce spending somewhere else.

Do central bankers not see this? They can surely read the same studies I do. In any case, the financial industry is waking up to the fact that something is very wrong.

Last week the Financial Times had an excellent column by Eric Lonergan, a macro fund manager at M&G Investments and proprietor of PhilosophyofMoney.net. He quickly and eloquently dismantled the foundation of modern central banking.

The idea that lower interest rates raise demand is based on the view that households attempt to smooth their consumption over time. This assumed relationship has little empirical support, and there are good reasons, particularly when rates are extremely low or negative, to doubt it. High existing debt levels, or poor creditworthiness, are more realistic constraints on spending than higher interest rates.

And what of savers? Lower rates have a depressing effect on household incomes, through reduced interest on savings and pensions. It is likely that in relatively wealthy economies – with rising healthcare costs, increasing longevity and uncertainty over pension funding – households respond to lower income on their savings by trying to save more. If this outweighs the reduced incentive to save, the actions of central banks are self-defeating. The relationship of spending to lower interest rates may well be the reverse of that assumed by policymakers. If consumers do not respond to lower rates by spending more, this places an additional onus on the corporate sector.

Yet corporate investment appears similarly unresponsive. Investment decisions have financial consequences over many years, and are more influenced by beliefs about future growth and attitudes to risk than by overnight interest rates set by central banks.

Indeed, cash hoarding is exactly what we see corporations doing, or at least those corporations that can make a profit in this environment. Apple, Microsoft, and all the other US tech giants have billions stashed outside the country for tax reasons. But they would still keep much of that money in cash even if the tax disadvantage went away. They have no need to spend it, very little to invest in, and see no reason to risk losing it or to bring it back into the United States to pay high corporate taxes. So there it sits, not stimulating anything.

As for consumers, I think Lonergan explained it well: “High existing debt levels, or poor creditworthiness, are more realistic constraints on spending than higher interest rates.” Most Americans have excessive debt, low credit ratings, or both. Low or even negative interest rates will not make them spend more money as long as that is the case.

NIRP Problem #2: Betraying Lord Keynes

In 2008 the whole financial system was on the verge of collapse. Then-Fed Chair Ben Bernanke saw little choice but to use every tool in the Fed’s toolbox. So he cut rates, among other things. As Walter Bagehot noted (there’s more on him below), the purpose of a central bank is to provide liquidity at a price in the middle of a crisis. The Fed decided to set the price very low, but they did do the appropriate thing by adding liquidity. However, they overstayed their welcome because of lingering timidity.

I think they made the right move in 2008, even if I disagreed with the actual way they implemented it, but keeping rates near zero years later is harder to defend. Doing so has punished savers without stimulating growth. Why the Fed’s hundreds of PhDs didn’t know this would happen is beyond me. Even their demigod, John Maynard Keynes himself, said interest rates have to reflect reality.

Even if I disagree with some of Keynes’s conclusions, and especially with the way his disciples have used his work, I have to recognize and acknowledge his brilliance. In his magisterial General Theory of Employment, Interest and Money, chapter 21, Keynes describes his “theory of prices.” This includes interest rates, which as we saw above is simply the price of liquidity. I will quote from its last section (this gets a little academic, but work through it, especially the areas that I put in bold). Remember, this was in the ’30s, in the middle of the Great Depression.

Today and presumably for the future the schedule of the marginal efficiency of capital is, for a variety of reasons, much lower than it was in the nineteenth century. The acuteness and the peculiarity of our contemporary problem arises, therefore, out of the possibility that the average rate of interest which will allow a reasonable average level of employment is one so unacceptable to wealth-owners that it cannot be readily established merely by manipulating the quantity of money. So long as a tolerable level of employment could be attained on the average of one or two or three decades merely by assuring an adequate supply of money in terms of wage-units, even the nineteenth century could find a way. If this was our only problem now – if a sufficient degree of devaluation is all we need – we, today, would certainly find a way.

But the most stable, and the least easily shifted, element in our contemporary economy has been hitherto, and may prove to be in future, the minimum rate of interest acceptable to the generality of wealth-owners. [Footnote 2: Cf. the nineteenth-century saying, quoted by Bagehot, that “John Bull can stand many things, but he cannot stand 2 per cent.”] If a tolerable level of employment requires a rate of interest much below the average rates which ruled in the nineteenth century, it is most doubtful whether it can be achieved merely by manipulating the quantity of money. From the percentage gain, which the schedule of marginal efficiency of capital allows the borrower to expect to earn, there has to be deducted (1) the cost of bringing borrowers and lenders together, (2) income and surtaxes and (3) the allowance which the lender requires to cover his risk and uncertainty, before we arrive at the net yield available to tempt the wealth-owner to sacrifice his liquidity. If, in conditions of tolerable average employment, this net yield turns out to be infinitesimal, time-honoured methods may prove unavailing.

To paraphrase, Keynes is saying here that a lower interest rate won’t help employment (i.e. stimulate demand for labor) if the interest rate is set too low. Interest rates must account for the various costs he outlines. The lender must make enough to offset taxes and “cover his risk and uncertainty.” Zero won’t do it, and negative certainly won’t.

The footnote in the second paragraph is important, too. Keynes refers to “the nineteenth-century saying, quoted by Bagehot, that ‘John Bull can stand many things, but he cannot stand 2 per cent.’”

Is Keynes saying 2% is some kind of interest rate floor? Not necessarily, but he says there is a floor, and it’s obviously somewhere above zero. Cutting rates gets less effective as you get closer to zero. At some point it becomes counterproductive.

The Bagehot that Keynes mentions is Walter Bagehot, 19th-century British economist and journalist. His father-in-law, James Wilson, founded The Economist magazine that still exists today. Bagehot was its editor from 1860–1877. (Incidentally, if you want to sound very British and sophisticated, mention Bagehot and pronounce it as they do, “badge-it.” I don’t know where they get that from the spelling of his name. That’s an even more unlikely pronunciation than the one they apply to Worcestershire.)

Bagehot wrote an influential 1873 book called Lombard Street: A Description of the Money Market. In it he describes the “lender of last resort” function the Bank of England provided, a model embraced by the Fed and other central banks. He said that when necessary, the BoE should lend freely, at a high rate of interest, with good collateral.

Sound familiar? It was to Keynes, clearly, since he cited it in the General Theory. Yet today’s central bankers follow only the “lend freely” part of this advice. Bagehot said last-resort loans should impose a “heavy fine on unreasonable timidity” and deter borrowing by institutions that did not really need to borrow. Propping up the shareholders of banks by lending low-interest money essentially paid for by the public when management has made bad decisions is not what Bagehot meant when he said that the Bank of England should lend freely.

How did the Fed act in 2008? In exact opposition to Bagehot’s rule. They sprayed money in all directions, charged practically nothing for it, and accepted almost anything as collateral. Not surprisingly, the banks took to this largesse like bees to honey. Taking it away from them has proved very difficult. We now find ourselves in an era of speculation about what will happen when interest rates are raised.

(By the way, thanks to reader Richard Field for pointing me to the above Keynes quote. It’s amazing how much help you can get from complete strangers on Twitter. I will admit that I ignored Twitter for a long time, but now I find myself roaming it when I’m sitting around with nothing else to do and my iPad in hand.

NIRP Problem #3: Policy Paralysis

What would Keynes and Bagehot say about today’s interest rates, or lack thereof? Their beloved Bank of England last week cut its benchmark rate to a record-low 0.25%. That is not what anyone would call a “heavy fine on unreasonable timidity.”

The problem is how to correct this policy error without causing yet more turmoil in the markets. On that, I’m stumped, and so are the central bankers. If they could wave a magic wand and get short-term rates back to, say, the 3% region where they were at the end of 2007, I’m sure they would be delighted. And we might see some positive effects. Savers would receive more income, for sure. However, this magic trick would also crater the stock market. The one thing we know is that the Federal Reserve is now in the thrall of the stock market.

The S&P 500 dividend yield is currently around 2%. To earn it, you have to accept the principal risk and volatility inherent in stocks. No one would do this if they could earn the same or even more in Treasury bills or bank savings accounts. An unexpected rate normalization by the Fed would jar the stock market downward to restore balance to the equation of risk and reward.

So we are stuck. The Fed can’t use the only available exit without slamming the markets. The only alternative is to stay in the trap and walk around in circles, hoping something will change. Someday it will, but I expect that it won’t be a pleasant change – but rather one that, in the minds of the central bankers, requires an even more unusual monetary policy. We will examine that potential in depth and detail next week. Until then, the room will get increasingly uncomfortable.

NIRP Problem #4: Killing Insurance Companies and Pension Funds Softly

Insurance funds make a profit by taking your money and turning it into long-term loans. They use the money they make, along with your premiums, to cover your insurance risk in the event of need. Pension funds generate profits from long-term loans to grow the money they need, along with your contributions, in order to pay for your retirement. They have built into their models a reasonable long-term return – at least from a historical perspective – on bonds and the stock market.

This model can turn fall apart very quickly under a very-low-interest-rate or NIRP regime. The returns insurers and pension plans make on their investments no longer adequately fund the promises they have made. It gets even worse with NIRP. Think of the poor insurance companies, monstrously bigger than banks in Europe, that are forced by regulations to invest in long-term government bonds, many of which are now earning negative returns. How in the Wide, Wide World of Sports can you make a positive return when you are forced to invest in negative interest-rate bonds?

Then we come to the banks. What happens when they make negative returns on their cash? We haven’t seen extreme scenarios yet, as far as I can tell, but the banks are definitely getting squeezed. Last week Royal Bank of Scotland warned some corporate customers that it may start charging interest to hold their deposits. Some German banks have already done so.

Knowing this practice is a problem, banks try to offset NIRP by cutting other costs: by automating more tasks, laying off employees, closing branches, etc. This year we’ve heard a lot about banks investing in blockchain ledger technology – the same engine that drives Bitcoin digital currency. The banks aren’t doing this because they love Bitcoin. Their interest is in reducing costs, and blockchain applications promise to help them do it. That technology will lead to more job losses down the road.

Between NIRP and assorted technology and regulatory changes, the banking industry is on its way to becoming a kind of regulated utility. This shift might mean fewer bailouts in the future, but it will certainly mean less risk-taking and speculative lending and investing by banks. To the extent this dynamic makes it harder for worthy businesses to get capital, it will contribute to the generally low-growth economic conditions we’ve seen since the crisis.

I have written several letters about the plight of pension funds worldwide. I am gathering information on the situation with insurance companies, which my initial research shows is even more dire. If you have something I should know, please send it to me.

NIRP Problem #5: Distorting Signals

ECB President Mario Draghi famously pledged to do “whatever it takes” to restore eurozone growth. His attempts to fulfill that promise have led to NIRP and other bizarre policies like the central bank’s massive asset purchases.

Whether the ECB’s various interventions are helping the eurozone economy is not yet clear, but they are certainly having consequences, among them the appearance, if not the reality, of central bank interference and favoritism.

The ECB’s corporate bond-buying program, for instance, was originally going to purchase already existing bonds on the open market. However, it has evolved into a kind of closed market in which a favored group of companies issue bonds customized to the ECB’s specifications.

Last week the Wall Street Journal reported that the ECB had gone a step further, buying bonds directly from two Spanish companies through private placements. In other words, the ECB bypassed public markets completely and simply loaned money to selected companies. They weren’t even going to tell anyone. Someone at the WSJ, God bless their attention to detail, did some data mining and found the two private placements. One was to the Spanish oil company Repsol and the other to Iberdrola, an electric power utility. Morgan Stanley acted as underwriter in both cases. I wish my friends at Morgan Stanley would arrange to give me long-term money that cheaply. Just saying.

Now maybe the ECB had good reason to make these two transactions privately. I don’t know, and they won’t say. But we shouldn’t have to wonder. The reality is that the ECB is buying so much of the corporate bond market in Europe that it is becoming difficult for the bank to find things to purchase on the public markets, and so they are beginning to look into the private markets. One of the great ironies is that European divisions of US companies are creating loans so they can get the ECB to buy them. It makes perfect sense from the company’s standpoint, of course – let’s hear it for replacing expensive loans with cheap ones. That’s an easy way to make an executive look smart.

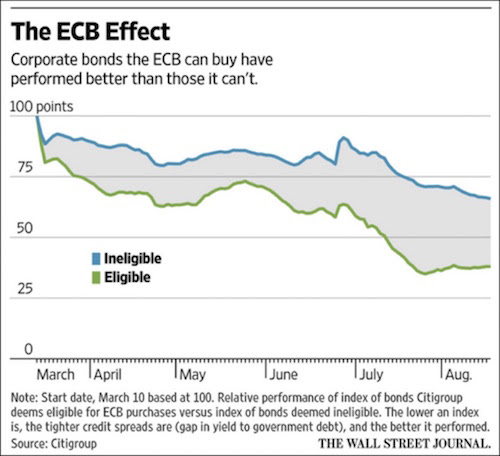

The problem is that this sort of thing generates false market data that leads other players to make bad decisions. Consider this chart from the WSJ. It depicts credit spreads of European corporate bonds. Lower numbers mean a tighter spread, which is good from the issuing company’s point of view because it means their cost of capital is lower.

We can see here that bonds eligible for ECB purchase (the green line) have consistently outperformed other bonds since the program launched. The advantage seems to be growing with time, too. Are these bonds really better, or are they just getting the benefit of ECB’s buying – buying that could end at any time? Technically, we don’t know. There is no way to tell. My guess? We will know when the ECB runs out of bonds to buy and starts having to loosen its determination as to what it can buy, such that more corporate bonds become eligible. If this new category of bonds sees its credit spread drop, too, we will know for sure that the critical variable at work is not bond quality, per se, but the ECB’s purchases.

European bond investors don’t have clean data that will let them make confident decisions. Some will no doubt withdraw from the bond market, leaving the ECB even more of a monopoly purchaser than it already is. That’s the opposite of what ECB claims to want, but its strategy is making the problem worse, not better.

NIRP Problem #6: Repressing Retirees

I saved this one for last because it is, for me, the most enraging consequence of ZIRP, NIRP, QE, and all the rest. Savers, the people who read my newsletters and buy my books, are paying the price of our central bankers’ mistakes and arrogance. People who did nothing to cause this situation are getting punished for it.

Back in February I wrote about how ZIRP and NIRP are “Killing Retirement As We Know It.” I don’t often quote myself, but this is important. Follow the link if you want to read the full section. I was talking about how retirees could once live off their savings without too much trouble.

It was even simpler if you had an employer or union pension plan to do the work for you. Pension plans pooled people’s money, calculated how much cash they would need to pay benefits in future years, and built portfolios (mainly bonds) to match the liability projections. Government and corporate bonds yielded enough to make the process feasible.

Younger readers may think I just described a fantasy world. I assure you, it was very much a reality not so long ago. Ask your grandparents if you don’t believe me. However, you may find them in a state of shock today because they thought the fantasy would last forever. Indeed, their financial planner probably told them they could count on drawing down 5% of their portfolio per year to live on, because the income from the investments in their portfolio would more than make up for the drawdown.

None of this is possible today. Neither you nor a massive pension plan acting on your behalf can generate enough risk-free income to assure you a comfortable retirement.

Why not? Because our monetary overlords decreed that it should be so. Retirees and their pensions are being sacrificed for what now passes as “the greater good.” Because these very compassionate overlords understand that the most important prerequisite for successful future retirements is economic growth. And they think that an easy monetary environment is the necessary fertilizer for that growth. So, when they dropped rates to zero some years ago, they believed they would soon be able to raise them again – and get people’s retirements back on track – without risking future economic growth. The engine of growth would fire back up, and everything would return to normal.

So much for the brilliant plan. You and I, the expendable foot soldiers in the war to reignite growth, now gaze about, shell-shocked, as the economic battlefield morphs from the Plains of ZIRP to the Valley of NIRP.

Note: Next week we are going to examine the “causality” of low interest rates and easy monetary policy and their connection with the mediocre recovery we have experienced. I am going to argue that the US economy has recovered (to the modest extent that it has) in spite of monetary policy, not because of it, just as economies have in every recovery since the Medes were trading with the Persians. Current Fed policy is actually distorting the process, not helping it.

The Federal Reserve’s choice to keep interest rates near zero for years on end has exacted a direct and sometimes devastating human cost. Real people who worked hard all their lives and made sensible decisions about retirement are, to be blunt, getting the shaft.

I thought about this at the Camp Kotok economic retreat in Maine a few weeks ago. The little town of Grand Lake Stream is beautiful, remote, and poor. Our group’s annual visit gives a big boost to the local economy. The residents roll out the red carpet and make us feel very much at home.

Attending the event every year for over a decade, I’ve come to know many of the locals. They are fine people who love their home and want only to live there in peace. They are far more like the people I grew up with out in the West Texas country than many of the denizens here in downtown Dallas. I know they struggle financially but had never really asked them for details. This time I did.

My son Trey, my colleague Patrick Watson, and I were out in a small boat in the middle of a big lake. With us was our guide, Jeff Cochran. Jeff spent 30 years working hard at a Maine paper mill. Patrick and I were talking about economics, of course, and we drew Jeff into the conversation.

Jeff retired from the paper mill with a small pension that he had to roll into a 401(k) that at one time would have enabled a modest living. Now, thanks to the Fed, it doesn’t. He earns extra income as a fishing and hunting guide but is still drawing down his pension far faster than experts would advise. I asked him about that, and he admitted that he was truly living on the edge.

He’s not the only one. Many of his neighbors are in similar situations. People all over the country are just folks who played by the rules and then found out the rules could change. It’s easy for someone like me to look at aggregate numbers and pontificate. Then I see the people behind those numbers, and it all becomes very real. I have been carrying around a true sense of outrage ever since that morning at Grand Lake Stream.

The folks of Grand Lake Stream don’t sit around waiting for charity. They work hard and always with a smile. I’ve actually never been there except to attend Camp Kotok, but I need to go more often. For a lifelong Texan, upstate Maine is about as far out of bounds as you can get.

If you want a Maine fishing or hunting getaway, Jeff can fix you up. You can reach him by email at [email protected]. I also recommend either Leen’s Lodge or Canalside Cabins for lodging. All these people know each other and will take good care of you.

Consider the trip to Grand Lake Stream your own little economic stimulus plan. I guarantee it will be far more effective than anything the central banks are doing. And you might find it as restful and stimulating as I have.

Next week we are going to continue with our thoughts on central banks, but focus on the Jackson Hole speeches and activities. A lot of what came out of that august gathering has helped me to realize that we are truly in a world where the unthinkable is now thinkable. Maybe I am just sensitive to it, but ever since I wrote that letter, I have seen the word unthinkable entering more and more into the discussion. Then again, I often use a concept in a letter and am then reminded that somebody else wrote about it six months earlier, and it just entered my mind and gestated there, which is what good concepts are supposed to do.

I am now fully operational, at least computer-wise, and hopefully can spend the next few days paying attention to the 415-odd emails in my inbox and whittle them down to under 30 over time. I will admit that the fuller my inbox is, the higher my stress level is; and over 400 is about as high as it has got in many, many years. And with that said, I think I will go ahead and hit the send button and wish you a great week.

Your frustrated with central banks analyst,

John Mauldin

subscribers@MauldinEconomics.

© Copyright 2016 John Mauldin. All Rights Reserved

.