- Where’s the Inflation?

- Time to Stop the Dots

- The Maradona Theory of Oil Markets

During the initial phase of my career, inflation was the enemy. Fed by years of overly easy money, inflation had become deeply embedded into contracts, asset prices and psyches. At its peak, the United States was experiencing 15% inflation, a level that is now seen as unconscionable even in emerging markets. The problem seemed intractable.

A generation later, developed countries can’t seem to generate inflation no matter how hard they try. Monetary policy has flooded financial systems with reserves, to little avail. The 2% inflation target adopted by most central banks has apparently become a bridge too far.

Why haven’t prices reacted to the stimulus? Should monetary authorities push harder to reach their objectives, and if so, how should they go about it? These questions have already been debated in Frankfurt and London this month, and they will certainly be front and center in Washington and Tokyo next week.

There are many schools of thought on how inflation evolves in an economy. Some look at inflation from the bottom up, analyzing markets for key goods and services. Others are convinced that monetary conditions are the predominant influence, and that digging through details is a fool’s errand. Demand pull, cost pushes, resource shocks and paradigm shifts periodically elbow their way into the conversation.

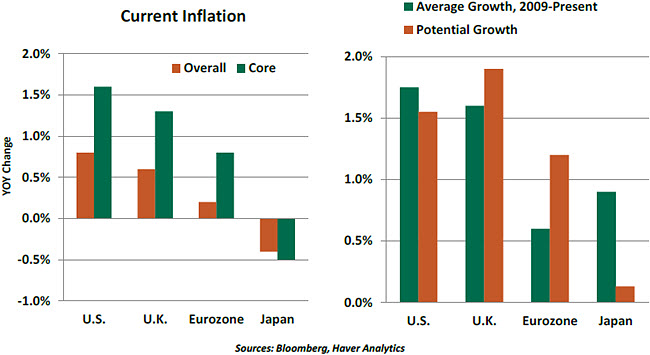

A good place to start the analysis of inflation’s recent course is to look at the rate at which economies are growing versus their long-run potential. In theory, if the former exceeds the latter, resource usage will increase and the prices of those resources will eventually rise. Inflation is typically low coming out of recession, escalating as the business cycle progresses.

Gross domestic product (GDP) in developed markets has increased steadily, but modestly, since the 2008 crisis. The rate of advance in the past eight years has been about half of what was achieved during the prior expansion; deleveraging and government austerity have been persistent headwinds. Developed nations’ potential for growth nations has also diminished in the past decade, thanks to a rising retirement wave and frustratingly slow productivity readings.  The chart on Page 1 suggests that the United States and Japan have been growing faster than their potential during the past seven years. But the former remains shy of its inflation target, while the latter remains in deflation. The United Kingdom has enjoyed a substantial decline in its unemployment rate despite underperforming its potential, which is also somewhat counterintuitive.

The chart on Page 1 suggests that the United States and Japan have been growing faster than their potential during the past seven years. But the former remains shy of its inflation target, while the latter remains in deflation. The United Kingdom has enjoyed a substantial decline in its unemployment rate despite underperforming its potential, which is also somewhat counterintuitive.

One potential explanation for these apparent inconsistencies is that we are mismeasuring GDP, productivity or both. Potential could be higher than some suspect, meaning that the current expansion is not creating resource pressures. Central banks are struggling to understand these dynamics. In the United States, we see this reflected in the discussion surrounding the “neutral” Federal funds rate; estimates for this have declined during the past year.

It might also be the case that our measures of supply are myopic. Capacity is global in nature; focusing on domestic utilization may miss reservoirs of capability. Faced with constraints in one market, international firms can simply change their sourcing or production patterns to limit price pressures. The international character of sourcing hinders the ability of any individual central bank to achieve its inflation objective.

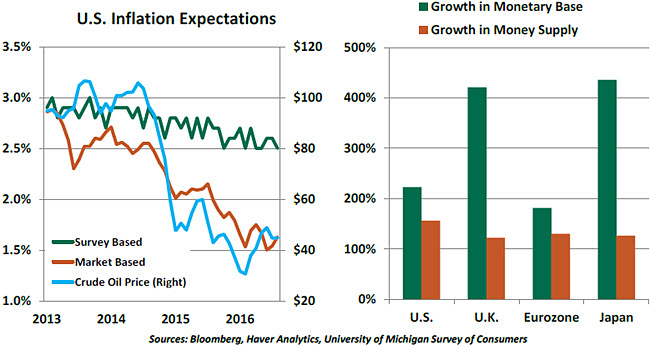

Ironically, monetary policy may also be partly at fault for today’s low levels of inflation. In bringing inflation to heel and then committing to inflation targets, central banks have tamed the psychology that is so important to determining the course of inflation. (The two-year-old crack in oil prices has provided a considerable assist in this department.) Even if money and credit are expanding rapidly in the short-term, investors and households have come to believe that prices will never again break containment in the long run.

Official interest rates in developed countries are low or negative, and (as discussed last week) central bank balance sheets are many times larger than they were during the crisis. With inflation still undershooting, some think that monetary expansion has been ineffectual. This is a challenging assertion to substantiate, since we can’t observe how inflation would have progressed in the absence of aggressive central bank policy. But it is true that the translation of reserve creation to the money supply has been blunted by the broad trend toward deleveraging, along with post-crisis capital and liquidity requirements. Banks in the eurozone continue to struggle with crisis-related bad debt, limiting their ability to extend fresh credit.

This is a challenging assertion to substantiate, since we can’t observe how inflation would have progressed in the absence of aggressive central bank policy. But it is true that the translation of reserve creation to the money supply has been blunted by the broad trend toward deleveraging, along with post-crisis capital and liquidity requirements. Banks in the eurozone continue to struggle with crisis-related bad debt, limiting their ability to extend fresh credit.

Faced with these constraints, some would have central banks pass the baton to fiscal policy. Additional government spending would create demand much more directly, and ensure that growth exceeds potential. Measures to raise wages, as have been implemented in the United States and Japan, might also help to boost spending and inflation.

But it is hard for central banks to stand down. Since the crisis, they’ve adopted a cynicism about the ability of legislators to do what’s necessary and an ethic of doing whatever it takes themselves. The latest potential addition to the unconventional policy toolkit is raising the inflation target to steer expectations higher. At some point, however, good leadership requires getting out of the way.

In the mid-1970s, the president of the United States took to wearing a button that said “WIN” (Whip Inflation Now). To deal with more contemporary challenges, I recently proposed that we start distributing buttons that say “RIP” (Raise Inflation Pressures). For some reason, that suggestion didn’t go over very well.

Confusing Points

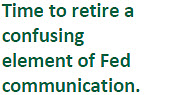

The Federal Reserve publishes the famous “dot plot” four times a year following Federal Open Market Committee (FOMC) meetings in March, June, September and December. We’ll get a new edition of this map On September 21. We wouldn’t be disappointed if this was the last dot plot we see.

The dot plot was introduced in 2012 as a way to increase transparency about how the Fed manages monetary policy. Each dot represents an FOMC member’s projection of the appropriate level of the federal funds rate at the end of the calendar year. The dots accompany summaries of economic projections, which debuted in 2011.

The dot plot shows what both the voting and nonvoting members of the FOMC (currently 17 members) think about the future path of the federal funds rate, based on their view of how the economy will evolve during the forecast horizon. Differences between the dots could therefore be attributable to differences in outlook or differences in what is viewed as the appropriate level of interest rates for a given outlook.

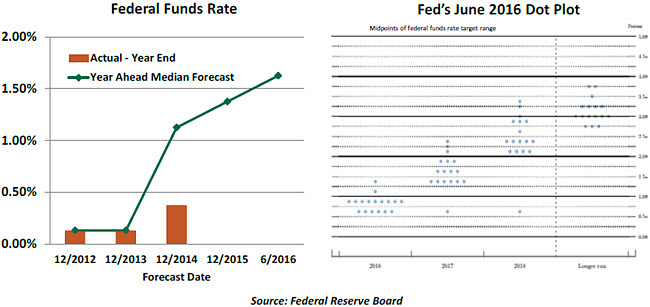

Markets have come to infer the likely path of the policy rate from the median dot in each quarter’s chart. As the chart below indicates, the Fed’s optimistic expectations of the policy rate at the end of each year have consistently exceeded the actual path of the federal funds rate. To some observers, this has damaged the Fed’s credibility.

But markets have come to misinterpret the dot plot as a commitment by the FOMC about the path of federal funds rate. FOMC participants continuously adjust their expectation of economic performance based on incoming data. The dot plot becomes stale as new economic reports become available. Therefore, it not surprising that there are disagreements between Fed’s policy rate path depicted in the dot plot (which is updated only quarterly) and the financial market view (which is updated in real time).  Further, some dots are more influential, and other dots are not at all helpful. James Bullard, president of the Federal Reserve Bank of St. Louis, proudly identified himself as the lowest dot in the June array, offering further that he had declined to submit his projection for the long-term funds rate because he did not find it useful. Bullard garnered some attention for his out-of-consensus view, but it confused markets (and likely his FOMC colleagues). The place for expressing those opinions should be in the board room, not in the dot charts.

Further, some dots are more influential, and other dots are not at all helpful. James Bullard, president of the Federal Reserve Bank of St. Louis, proudly identified himself as the lowest dot in the June array, offering further that he had declined to submit his projection for the long-term funds rate because he did not find it useful. Bullard garnered some attention for his out-of-consensus view, but it confused markets (and likely his FOMC colleagues). The place for expressing those opinions should be in the board room, not in the dot charts.

A retirement of the dot plot should not be seen as reducing the transparency of the Fed’s monetary policy actions because it has been the source of uncertainty. The minutes of FOMC meeting published three weeks later convey the range of views of the FOMC, which is adequate guidance for markets.

All of that said, the Fed will press ahead and publish a new dot plot next week. Since the dots are based on a calendar year, the 2016 dots will provide meaningful input about the willingness of the group to raise rates at their December meeting. Markets will also be focused on the outlook for 2017. A projection of three policy rate increases will be seen as aggressive, based on projections of modest growth and inflation. Markets will respond to a prediction of a 50 basis points increase during 2017 more calmly.

Forecasts of economic growth, inflation and unemployment are appropriate for publication after each Fed meeting, much like the practice of other major central banks. The Fed is the only major central bank that also offers a prospective path for interest rates. The dot chart creates more confusion than clarity and should be discontinued.

Talk Is Cheap

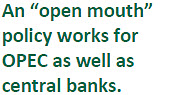

Former Bank of England Governor Mervyn King has observed that expectations of policy changes can be more important than actual policy changes. Shifts in market expectations of policy rates were at times sufficient to achieve economic activity targets, even as the policy rates were kept unchanged. King had playfully christened this as the “Maradona Theory of Monetary Economics” after the legendary Argentinian footballer. During the 1986 World Cup, Maradona scored after running 60 yards in a straight line, dodging five English defenders who had expected him to move left or right.  Russia and Saudi Arabia are trying achieving something similar in the oil markets. One of key themes in the energy arena this year has been the ongoing saga of a so-called “production freeze” by Saudi Arabia-led OPEC (Organization of the Petroleum Exporting Countries) and Russia, but an agreement has remained elusive. On the contrary, most exporters are producing at near-record levels in a bid to protect market share. Nevertheless, every stray comment supporting a freeze has moved oil prices up and it’s quite clear that senior oil officials are trying to guide the market like central bankers without acting on production levels.

Russia and Saudi Arabia are trying achieving something similar in the oil markets. One of key themes in the energy arena this year has been the ongoing saga of a so-called “production freeze” by Saudi Arabia-led OPEC (Organization of the Petroleum Exporting Countries) and Russia, but an agreement has remained elusive. On the contrary, most exporters are producing at near-record levels in a bid to protect market share. Nevertheless, every stray comment supporting a freeze has moved oil prices up and it’s quite clear that senior oil officials are trying to guide the market like central bankers without acting on production levels.

The threats have just enough credibility to be taken seriously. The economies of many oil producers are struggling mightily, and supply restrictions would be mutually beneficial.

However, as in central banking, there are limits to expectations management. Rallies based on rumor are regularly matched by declines after data releases. Still, verbal guidance does change the risk-reward metric for investors and effectively scares away short sellers.

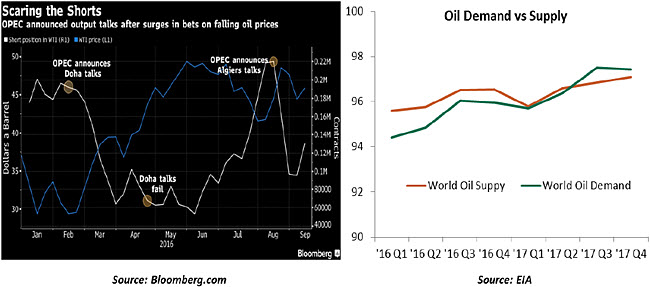

Oil surplus is estimated to be exhausted sometime in 2017, which would then render a freeze irrelevant. Until that time, verbal interventions would likely provide a floor to oil prices — much like the threat of returning shale oil supply at higher prices has provided a cap. The risk is that repeated failure to deliver on a freeze would make verbal guidance lose credibility and relevance. But since supply management is difficult, and coordination among producers even more so, it looks like verbal intervention is the only game in town.

© Northern Trust