Newsletter - September 2016

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSUBTLE

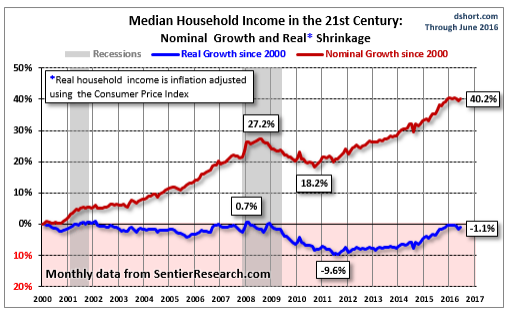

If you wonder why rising income doesn’t seem to provide much bang for the buck (pun intended), as the graph below shows, you can blame the subtle erosion of inflation. I doubt many investors realize that, in real dollars, median household income is just slightly less than it was 16 years ago in 2000.

Of course, it could be much worse. I can’t imagine how Venezuelans deal with their inflation. From the New York Times:

“While most advanced economies struggle to lift inflation, none would want Venezuela’s situation: Consumer-price inflation is forecast to hit 480% this year and top 1,640% in 2017, according to the International Monetary Fund.”

YOU CAN’T BLAME ME

I do my part drinking wine, but obviously it’s not enough for the U.S. to compete with France. According to a story in the Lubbock Avalanche Journal, the city that drinks the most wine (surprise) is Paris, “…with 690 million bottles guzzled each year, almost 14 gallons (71 bottles) for each man, woman and child.” That’s some guzzling! Buenos Aires is a distant second with 457 million bottles (8.5 gallons/person). New York City and L.A. are pikers on the board at 301 million bottles and 241 million bottles, respectively.

HAPPY BIRTHDAY TO THE INDEX FUND

From Jason Zweig’s always-worthwhile WSJ articles:

Forty years ago this week (September 1), the index mutual fund was born when Vanguard Group’s First Index Investment Trust (now Vanguard 500 Index Fund) opened for business with $11.3 million in assets.

That was far short of the $150 million target that Vanguard’s founder and the fund’s creator, John Bogle, had set. The investment banks underwriting the fund were so disappointed by the measly amount they had raised that they wanted to give investors their money back. “I said, ‘Hell no,” recalls Mr. Bogle, 87 years old.

Today Vanguard 500 Index Fund holds more than $252 billion, and index mutual funds and exchange-traded funds invest nearly $5 trillion in combined assets.

DISAPPOINTED

I have the greatest respect for Kiplinger, but I was disappointed by the Kiplinger ETF 20 Update. Only a year after launching, Kiplinger wrote, “Three Funds In, Three Out… It’s time for some changes.” Although the article provided credible reasons for the changes, one year smacks of market timing, not long-term investing.

I LIKE IT

Of course I may be a bit biased; however, I’m not surprised that a number of recent studies conclude that clients who receive advice get their money’s worth. Here are some examples of the estimated value added by working with a competent financial advisor:

• Vanguard’s “Advisor’s Alpha” – 3%/year

• Morningstar’s Gamma – 1.82%

• Financial Engines (2009-2010) – 2.92%

• Investment Funds Institute of Canada

Multiple attributable to advice for those receiving

4–6 years of advice – 1.58

7–14 years of advice – 1.99

15 or more years of advice – 2.73

https://practicemanagementblog.onefpa.org/2016/08/04/you-cannot-do-this-alone/

GOOD NEWS, BAD NEWS

The good news is that we’re living longer; the bad news is that we’re living longer and it’s expensive. Here are some sobering numbers from a most excellent article by my friend Kate McBride. “The Longevity Paradox: As Americans live longer, they run the risk of outliving their money”

http://www.investmentnews.com/article/20160822/FEATURE/160809926/the-longevity-paradox-asamericans-live-longer-they-run-the-risk-of?issuedate=20160822&sid=Longevity20160822

• $464,000 – Total lifetime healthcare cost of a 55-year-old couple planning to retire at 65.

• 83% – The rate hike the federal government just approved on its long-term care policies.

• $90,500 – The annual cost of a private room in a nursing home; $42,600 for an assisted-living community; $21,840 for a home health aide; and $18,200 for adult daycare.

• According to an earlier study, 42% of people who live to age 70 will spend time in a nursing home.

• To deal with this reality, more than 50% of advisors are recommending: o Deferring Social Security benefits o Planning for a bigger healthcare budget o Setting lower withdrawal rates

PERKS OF REACHING 60 OR BEING OVER 70 AND HEADING TOWARD 80!

From my friend Phil:

1. Kidnappers are not very interested in you.

2. In a hostage situation you are likely to be released first.

3. No one expects you to run — anywhere.

4. People call at 8 PM and ask, “Did I wake you?”

5. People no longer view you as a hypochondriac.

6. There is nothing left to learn the hard way.

7. Things you buy now won’t wear out.

8. You can eat supper at 5 PM.

9. Your supply of brain cells is finally down to a manageable size.

10. You can’t remember who sent you this list.

11. You notice these are all in Large Print for your convenience.

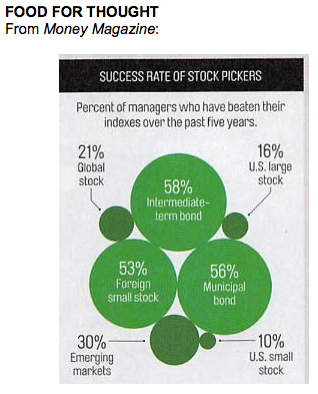

IT’S NOT LOOKIN’ SO GOOD…

…for broad-based active management.

Ever wonder why E&K has such a significant allocation to passive equity managers? Here’s a story from ThinkAdvisor that highlights the issue.

Performance of Active Management

S&P DOW JONES INDICES REPORTS THAT MOST RETAIL MUTUAL FUNDS UNDERPERFORM THEIR BENCHMARKS EVEN BEFORE FEES ARE CALCULATED

Fees are not the only reason that actively managed funds often underperform passive index funds, as commonly believed. According to the latest SPIVA Institutional Scorecard report from S&P Dow Jones Indices, at least two-thirds of mutual funds and institutional accounts in multiple asset classes underperformed their respective benchmarks even before fees were included in the calculation. Eighty percent of domestic mutual funds underperformed the S&P 500 before fees were calculated — a calculation the report calls “gross-of-fees.” After fees, also known as net-of-fees, the number jumped to 88%.

For institutional equity accounts — defined as separately managed accounts or co-mingled trusts — the underperformance rate was 85% before fees (there was no net-of-fees calculation for those accounts).

SOME INTERESTING STATISTICS

From Forbes via my friend Bob Veres:

Most Americans work in one of five different sectors:

14% in professional and business services

13.5% in production and manufacturing

13.4% in state or local government

13.2% in healthcare and social assistance

11.0% in retail

Most of us work long hours:

Fewer than 40 hours – 8%

40 hours – 42%

41–49 hours – 11%

50–59 hours – 21%

60+ hours – 18% (I’m pleased to know I have company.)

In 2015, 24% of employed people did some or all of their work at home.

What are the highest-paying jobs in America? The MyPlan.com website lists the top 300 jobs in terms of average salary, and the top of the list is dominated by medical professionals:

Anesthesiologists: $258,100

Surgeons: $247,520

Oral Surgeons: $233,900

Obstetricians and Gynecologists: $222,400

Orthodontists: $221,390

Radiologists, Pathologists, Neurologists, Allergists and Immunologists, Urologists, Preventive Medicine Physicians, Ophthalmologists, Hospitalists, Sports Medicine Physicians, Physical Medicine and Rehab Physicians, Nuclear Medicine Physicians and Dermatologists all finish in a tie for sixth ($197,700), and you have to go all the way down to number 22 on the list, to Chief Executives, before you reach a nonmedical professional on the list.

Lawyers come in way down at number 38 ($136,260), Physicists come in at number 50 ($118,500), Economists at number 77 ($109,230), Art Directors at 105 ($101,990), Veterinarians at 112 ($99,000), Automotive Engineers at 171 ($88,190), and Video Game Designers at 190 ($87,310).

Finally, according to the U.S. Census Bureau, there are 5.4 million companies that provide employment for American workers, with an annual payroll totaling $5.6 trillion, or roughly $48,997 per employee. A surprising 8.9% of these employer firms (481,981) have been in business for fewer than two years, and only 3.1% of them (167,917) have existed for more than sixteen years. Most firms (78.5%) employ fewer than ten workers, while 17,982 companies employ 500 or more Americans.

HAVIN’ FUN WHILE DOIN’ GOOD

For over two decades Hospice of Lubbock has sponsored Grief Camp for Children. The camp is for children five to seventeen years of age who have experienced the death of a family member or friend within the past two years. Katie is a Board Member and a long-time participant in Grief Camp. This year John and I joined her, and as you can see, we looked sterling as we dished out hot dogs, sausage (delicious), and hamburgers.

WEDDING $$$

Also from Money:

• Gender Gap: Wedding Dress $1,216 versus Tuxedo $203

• 30% – The typical venue markup when the event is a wedding.

• Average amount spent on gift

Close family member ....$180

Close friend...................$120

Friend .............................$80

Co-worker.......................$65

• Who Pays?

Bride’s Parents ..............43%

Groom’s Parents............12%

Bride & Groom...............43%

Other................................2%

MORE WINE FACTS FROM THE AJ

(I like wine.)

• It takes about 2½ pounds of grapes to make a standard bottle of wine.

• California produces 85-89% of U.S. wines.

• There may be more than 10,000 different wine grapes. Italy grows more than 400 varieties.

Finally, my compliments to Gus Clemens, the author of the column who concluded: “I pity empty wine glasses, and I empty full wine glasses.”

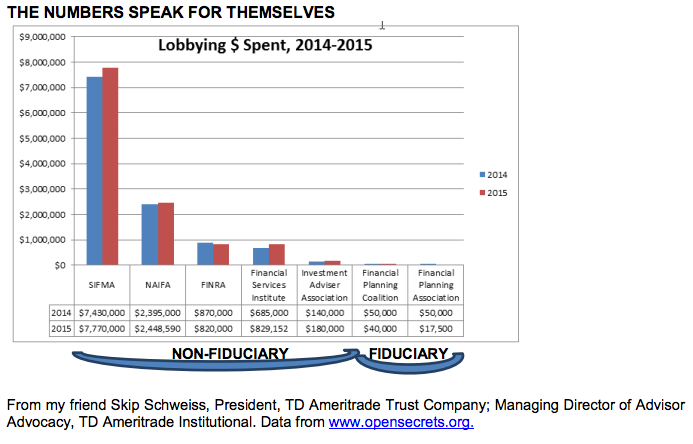

WHY WE REALLY NEED A FIDUCIARY STANDARD!

Headlines from recent publications:

Securities America to pay $1.5 million for mutual fund overcharges The independent broker-dealer is paying restitution for failing to waive sales charges for some retirement plans and charitable organizations

Morgan Stanley Reaches $4.7M Settlement with the State of Mississippi Investors at its Ridgeland branch, where client risk tolerance data was entered incorrectly, will get $4.2 million

Morgan Stanley Faces $150M Suit Over its Own 401(k) A $150 million class action suit against Morgan Stanley alleges the firm mismanages its employees’ retirement funds by placing them in inferior products and charging excessive fees

BNY Mellon to pay $714 million to settle foreign exchange cases Bank of New York Mellon Corp has agreed to pay $714 million to settle allegations that the bank overcharged pension funds and other clients for foreign exchange services

State Street will pay $530 million to settle foreign exchange cases

Morgan Stanley and its board were accused of mismanaging the firm’s 401(k) retirement plan and costing 60,000 employees hundreds of millions of dollars by picking inappropriate and high-priced investments, some of which were managed for the firm’s own profit

Edward Jones faces proposed class action lawsuit over excessive 401(k) fees Another of the large brokerages, Morgan Stanley, was also sued Friday for fiduciary breach in its retirement plan

And the gorilla earlier this year: Goldman Reaches $5 Billion Settlement Over Mortgage-Backed Securities. Pact marks largest settlement in history of Wall Street firm

What is really depressing is how easy it is to find these stories.

HOW COOL IS THIS?

To close on a more positive note, from my friend Judy. At the click of a button you can listen to hundreds of songs from practically any good old classic artist you can think of. Here’s a list of the top 100. http://www.songs-tube.net/

Hope you’ve enjoyed,

Harold R. Evensky, CFP, AIF

Chairman

Evensky & Katz / Foldes Financial Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits