This week I was in beautiful Toronto, where I presented the keynote address and participated in a panel discussion at the annual Mines and Money conference. It was the first time the highly respected gathering of precious metals analysts and investors came to the Americas, and they couldn’t have chosen a better city than my hometown. Toronto has long served as a major hub for mining finance and is home to some of the world’s largest gold producers.

Toronto is also one of the most multicultural municipalities on earth. According to its website, over 140 languages and dialects can be heard in the city, with a third of its population speaking a language other than English or French at home. This makes it an extremely attractive destination for professional millennials from all over the globe.

I had the pleasure of attending a Young Presidents’ Organization (YPO) event in Toronto as well. The YPO is the world’s preeminent group for global business leaders and executives, providing peer-to-peer learning and networking opportunities among its 24,000 members. The companies they lead generate an impressive $6 trillion in global annual revenue. The daylong event, titled “Culture Shock,” focused on the societal effects of disruptive technology, including advanced robotics, 3D printing, the internet of things and more.

|

While at the Mines and Money conference, the Mining Journal presented its Outstanding Achievement Awards. I’m humbled to share with you that Ralph Aldis and I were co-recipients of the Best Americas Based Fund Manager award. It’s a great honor to have been selected from among such an esteemed group of portfolio managers.

The award symbolizes U.S. Global Investors’ strong commitment to its investors and shareholders. It’s my firm belief that we’ve consistently been a leader in the metals and mining space. I’m deeply proud of what we’ve managed to accomplish over the years, starting almost 30 years ago when I bought a controlling interest in the company. Since then, our funds have been recognized numerous times by Lipper and Morningstar, two trusted independent financial authorities.

OPEC Decision Helps Oil Post Its Second Straight Month of Gains

You’ve probably heard by now that, in an effort to lift oil prices, the Organization of Petroleum Exporting Countries (OPEC) tentatively agreed to a production cut at its meeting in Algiers this week. The cartel, which controls more than a third of world output, plans to limit daily production to between 32.5 million barrels and 33 million barrels, down from 33.2 million barrels.

|

This comes more than two years since oil prices were kneecapped, wreaking havoc on several OPEC member nations’ economies. Saudi Arabia currently faces a steep budget deficit, as oil revenues make up close to 90 percent of the country’s budget. Meanwhile, Venezuela’s currency, the bolivar, has become so worthless that it’s now cheaper to use it as a napkin than to buy actual napkins. Airlines flying to the U.S. won’t even accept bolivars. (Of course, this has more to do with the government’s woeful mismanagement of the country than oil prices.)

It’s important for investors not to get too excited over OPEC’s decision. At the moment, none of this is set in stone. Some OPEC members are already wavering, with Iraq questioning output numbers and Nigeria moving to boost production.

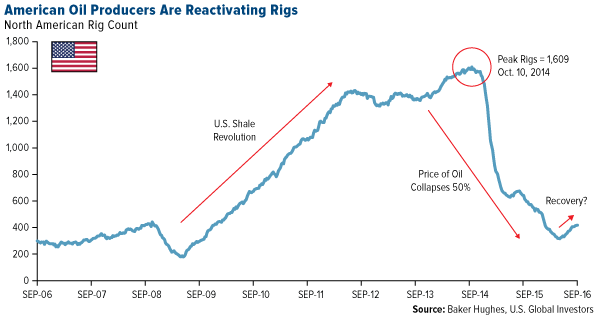

Plus, American producers are likely to step into the void OPEC would create. Compared to last year, production is down only 535,000 barrels a day—and that’s with far fewer operating rigs. But it appears companies are eager to get back to work. In 12 of the last 13 weeks, North American drillers reactivated mothballed rigs. I expect to see the pace rise as it becomes clearer OPEC will make good on its resolution.

Consolidation Could Ease the Pain

For the past two years, OPEC’s pump-at-will policies have flooded the market with cheap supply, causing economic pain for producers with higher cash costs, including those involved in fracking, the Canadian oil sands and deepwater drilling.

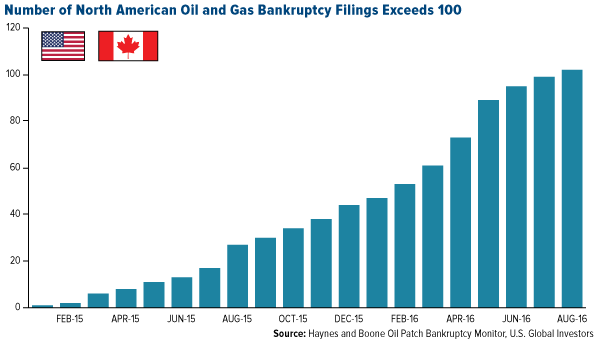

Since January 2015, more than 100 U.S. and Canadian producers have declared bankruptcy, representing a combined $67 billion in debt, according to Dallas law firm Haynes and Boone.

To weather the low-price environment, global exploration spending has been slashed for two consecutive years. As Bloomberg reports, total investment in world oilfields stands at $450 billion, a significant 24 percent decline from last year. The International Energy Agency (IEA) expects the cost-cutting to extend into next year.

This has driven new oil discoveries to their lowest point since 1947.

It also underscores the need for industry consolidation. With exploration budgets down, major oil companies will rely on acquisitions to replace up to half of their reserves, according to energy consultancy firm Wood Mackenzie. When the airline industry was mired in bankruptcies a decade ago, we saw a huge wave of mergers and acquisitions, and we should expect to see the same in the oil patch.

A few big oil and gas deals have come out of the price rout—Royal Dutch Shell’s acquisition of BG, worth $70 billion, is the largest by far—but more will likely take place in the near term. Antitrust officials prevented energy giants Halliburton and Baker Hughes from realizing their $35 billion deal, announced back in November 2014.

America’s Gas Binge Hits a New Record

Oil inventories might be brimming all over the globe, but demand remains strong and expected to swell alongside the global middle class. As I told you in June, India is expected to have the fastest growing demand for crude between now and 2040, replacing China.

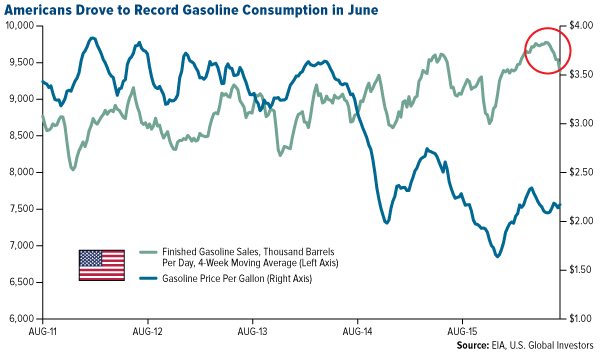

But don’t count the U.S. out. Even with fuel efficiency improving in automobiles, Americans burned through a massive 406 million gallons a day in June, the most recent month of data from the U.S. Energy Information Administration. This sets a new record, beating the previous one set in July 2007, soon before the recession. The record might be short-lived, however, once the July and August data are released.

Low prices have emboldened many Americans to purchase vehicles with lower fuel efficiency such as trucks, vans and SUVs, which has been great for auto companies and lenders.

People are also taking longer road trips. According to the Transportation Department, motorists logged 287.5 billion miles in July, the most ever for the busy summer travel month. That’s the equivalent of taking 3,000 round trips to the sun, which is what it feels like after all the flights I’ve taken recently.

Have a great weekend!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.26 percent. The S&P 500 Stock Index rose 0.17 percent, while the Nasdaq Composite climbed 0.12 percent. The Russell 2000 small capitalization index lost 0.24 percent this week.

- The Hang Seng Composite lost 1.92 percent this week; while Taiwan was down 1.27 percent and the KOSPI fell 0.51 percent.

- The 10-year Treasury bond yield fell 2 basis points to 1.60 percent.

Domestic Equity Market

Strengths

- Energy was the best performing sector for the week, gaining 4.64 percent vs an overall increase of 0.17 percent for the S&P 500 Index.

- Transocean LTD, an offshore drilling contractor, was the best performing stock for the week, increasing 17.14 percent.

- The Chicago Board of Options has agreed to buy Bats Global Markets in a $3.2 billion deal. The deal is valued at $32.50 per Bats share, a 23 percent premium over Bats' closing price on Thursday, when reports of the deal talks first emerged. It consists of 31 percent cash and 69 percent CBOE stock.

Weaknesses

- Utilities were the worst performing sector for the week, falling by 3.88 percent vs. an overall increase of 0.17 percent for the S&P 500.

- Endo International, a provider of specialty health care solutions, was the worst performing stock of the week, declining 13.85 percent.

- Deutsche Bank continues to make new lows. Shares of Deutsche Bank were down close to 5 percent in Germany on Friday, after Thursday's Bloomberg report stating that hedge funds were beginning to pull business from the bank. The stock was down about 9 percent at the open.

Opportunities

- Apple is already developing the iPhone 8. An employee at Apple's office in Herzliya, Israel, told Business Insider's Sam Shead that all new products were worked on at the facility and that the iPhone 8 would have a radical redesign.

- BCA’s U.S. equity strategists came out with their industry group pricing power report. In it, they note positively that pricing power has improved since their last update in March, with over half the industry groups showing a rising selling price trend. The most robust pricing power continues to reside in defensive sectors such as health care and consumer staples. Many domestically-focused consumer discretionary sectors are also showing ability to raise selling prices, but those are also experiencing higher cost pressure.

- Given current market dynamics, rather than pile into high beta sectors, liquidity-fueled equity markets favor a non-cyclical bias. This should also protect portfolios in the event that the uptrend is undermined by a policy mistake and/or downside economic surprises.

Threats

- California dealt a huge blow to Wells Fargo. On Wednesday, the state of California said it would no longer use Wells Fargo as an underwriter for the issuance of state municipal bonds; it also said the bank would not be involved in the state's banking or investment activities for the next 12 months.

- The maker of La Croix soft drinks is crashing after a short seller accused it of cooking the books. Glaucus Research, a short-selling researcher, claimed that National Beverage's CEO had admitted to an attorney that he was manipulating the stock price by creating false invoices for the firm.

- The Federal Reserve is making a big change to how it tests America's banks. The Fed is considering changing the annual stress tests it gives to U.S. banks to see if they can withstand a massive financial crisis, and also using test results to set the capital buffers that banks must maintain to blunt the effects of a downturn, according to its chair, Janet Yellen.

September 27, 2016How Gold Came to South Korea’s Rescue |

September 26, 2016The Case for Natural Resource Equities |

September 20, 2016Welcoming the New Addition to the S&P 500: Real Estate |

The Economy and Bond Market

Strengths

- Consumer confidence surged to a post-recession high. The latest reading from the Conference Board came in at 104.1 for September, up from the prior month's 101.8, and above the expected 99.0.

- GDP for the second quarter came in at 1.4 percent, ahead of the 1.3 percent expectations.

- Durable goods orders were unchanged in August. Economists had forecast that orders would fall 1.5 percent during the month, according to Bloomberg.

Weaknesses

- Inflation-adjusted consumer spending dropped for the first time since January. The figure fell 0.1 percent after climbing 0.3 percent the previous month, pointing to softening consumption after a run of strong gains.

- The Richmond and Dallas Fed Manufacturing Indexes came in weaker than expected. Richmond was -8 vs expectations of -2 while Dallas was -3.7 vs expectations of -2.5.

- Moody’s evaluated the impact of low oil and gas prices on energy-dependent state and local governments. Hardest hit states are Alaska, Louisiana, North Dakota, Oklahoma and New Mexico.

Opportunities

- The Chicago PMI Survey for September came in at 54.2, ahead of expectations of 52 and last month’s reading of 51.5. That is a bullish signal as PMI is a forward-looking indicator.

- According to BCA, leading housing indicators such as homebuilder sentiment and the months’ supply of new homes suggest that residential construction will soon ramp up once again.

- Currencies of oil producing nations rallied on the news that OPEC agreed to implement production cuts. These gains could continue if oil prices rise sustainably.

Threats

- The market’s pricing of a rate hike by the December Federal Open Market Committee (FOMC) meeting is tracking virtually the same as last year. The market is currently priced for a 46 percent chance of a rate hike before the end of the year. This is almost exactly the same as where the probability of a 2015 rate hike was following last September's FOMC meeting. As long as the U.S. economic data remain reasonably firm, then rate hike probabilities should follow last year's path. The Economic Surprise Index shows that overall data releases have been coming in stronger than they were last year. Thus, it will likely take significant disappointments in the employment or inflation data for the Fed to push the next hike into 2017. A December rate hike is not yet discounted in the market. Although lower longer run rate forecasts will cap the upside in yields, the Treasury curve still has room to bear-flatten during the next three months.

- The surge in home prices may be slowing down. Home prices in July fell on a month-to-month basis in 20 major U.S. cities, according to the S&P CoreLogic Case-Shiller Index.

- Business executives in Texas say the U.S. economy is still a "big concern." The latest report from the Dallas Fed's manufacturing survey cited ongoing concerns about the economy, skilled-labor shortages, and oil prices.

Gold Market

This week spot gold closed at $1,315.86, down $21.79 per ounce, or 1.63 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.21 percent. Junior miners outperformed seniors for the week, as the S&P/TSX Venture Index fell back just 1.31 percent. The U.S. Trade-Weighted Dollar Index finished the week flat.

|

Date |

Event |

Survey |

Actual |

Prior |

| Sep-26 |

U.S. New Home Sales |

600k | 609k | 659k |

| Sep-27 |

Hong Kong Exports YoY |

-2.0% | 0.8% | -5.1% |

| Sep-27 |

U.S. Consumer Confidence Index |

98.8 | 104.1 | 101.8 |

| Sep-28 |

U.S. Durable Goods Orders |

-1.5% | 0.0% | 3.6% |

| Sep-29 |

Germany CPI YoY |

0.6% | 0.7% | 0.4% |

| Sep-29 |

U.S. GDP Annualized QoQ |

1.3% | 1.4% | 1.1% |

| Sep-29 |

U.S. Initial Jobless Claims |

260k | 254k | 251k |

| Sep-29 |

Caixin China PMI Mfg |

50.1 | 50.1 | 50.0 |

| Sep-30 |

U.S. CPI YoY |

0.9% | 0.8% | 0.8% |

| Oct-3 |

U.S. ISM Manufacturing |

50.5 | -- | 49.4 |

| Oct-5 |

U.S. ADP Employment Change |

165k | -- | 177k |

| Oct-5 |

U.S. Durable Goods Orders |

-- | -- | 0.0% |

| Oct-6 |

U.S. Initial Jobless Claims |

256k | -- | 254k |

| Oct-7 |

U.S. Change in Nonfarm Payrolls |

170k | -- | 151k |

Strengths

- The best performing precious metal for the week was palladium with a 2.72 percent gain and a quarterly gain of 20.24 percent, its best three month gain since 2010. Global car sales have experienced an improved outlook.

- This week we also had Kirkland Lake Gold make a friendly takeout offer for Newmarket Gold. The transaction almost appeared as a merger of equals as the premium offered had closed somewhat before the deal was announced. The combined companies will produce about 500,000 ounces of gold per year; the operations are in politically safe Canada and Australia with reasonably long mine lives.

- The Delaware Depository, in collaboration with CUSIP Global Services, announced last week its creation of the first-ever CUSIP identifiers for physical precious metals, reports the CPM Group. The CUSIP number previously kept physical metals apart from mainstream investment channels, but now they will be under the same system in which financial assets are bought, sold and managed by individual and institutional investors, along with brokers and sell-side analysts.

Weaknesses

- The worst performing precious metal for the week was platinum, falling 2.66 percent, with silver nearly down as much too. Reuters reported that investors are shying away from the platinum as concerns over supply chain inventories persist. In 2014 there was a five-month strike that left one million ounces of production on hold yet there was little impact on platinum prices. In addition, electric vehicles in the future could further erode the need for the metal.

- European banks have inundated the ECB with their largest request for dollar funding in four years. This week Bloomberg reported that 12 banks sought $6.248 billion in liquidity. What seemed obvious was this was driven by the continued troubles at Deutsche Bank but according to one source there were no German bidders in the mix. This could mean that the banks in Europe were simply taking precautionary measures in case there will be a crisis.

- China imported 251 tons of silver in August, according to data from customs authorities and commented on by Germany’s Commerzbank last week. Lawrie Williams writes that although this import number was 16 percent up from last month’s, it was down 29 percent from August 2015 data. On the gold end, China cut bullion imports from Hong Kong in August to the lowest level since January, reports Bloomberg, amid rising property prices and an improving economy.

Opportunities

- According to the CEO of Randgold Resources Mark Bristow, peak gold production could be reached in the next three years, reports Bloomberg, as miners fail to replace their reserves. The chart below is a good example of how a lack of new discoveries, paired with miners digging out high-grade material for a short-term gain, can quickly diminish the lifespan of a mine.

- Goldman Sachs believes inflation pressures are starting to build. According to data from Bank of America, investors anticipate consumer prices to rise 1.3 percent annually, the highest level in 14 months, reports Bloomberg. “All of the signals are suggesting that we are now pretty close to full employment,” chief economist at Goldman Sachs Jan Hatzius said. “We’re starting to exert some upward pressure on inflation.” Brown Brothers Harriman sees this pressure stemming from two elements: rents and medical services.

- BMO is making revisions to its precious metals forecast, reports Kitco News, and is now saying that safe-haven demand will continue to drive gold and silver prices higher next year (and support the precious metals market in the next three years). The bank revised its outlook for the yellow metal in 2018 and 2019 to around $1,350 an ounce and $1,250 an ounce, up 8 percent and 4 percent respectively from the prior forecast.

Threats

- Shares of B2Gold and OceanaGold fell sharply this week, following notification of environmental breaches for the companies’ mines operating in the Philippines. OceanaGold’s Didipio mine is the only mine affected by the environmental audit rolled out by the Philippines’ Department of Environment and Natural Resources. For B2Gold, the Masbate mine is the only mine affected by the audit; however, it is also the primary driver of outperformance in 2016.

- According to Citigroup Inc., gold may be in for a bumpy ride in the final quarter. With presidential candidate Donald Trump now at a 40 percent chance of winning the election, reports Bloomberg, Citi says volatility in bullion could be on the horizon, in combination with investors preparing for higher U.S. interest rates. A Trump win may indeed be chaotic, but would slashing U.S. corporate tax rates be worse for the market or just the medicine its needs? Contrarily, a democratic win might mean more of the same policy choices which have been keeping gold well bid.

- Deutsche Bank’s counterparties seem to have mounting concerns about doing business with Europe’s largest investment bank, according to an article on ZeroHedge. Bloomberg data show a number of funds that clear derivatives trades with Deutsche Bank AG have withdrawn some excess cash and positions held at the lender. The bank is one of the most interconnected on the planet. Any type of unwinding of Deutsche Bank’s assets would have major repercussions to the global banking system. Perhaps that’s why news stories at the close of the week speculated that the U.S. Justice Department would assess a much smaller fine against the bank for past misdeeds. Ironically, Wells Fargo and other U.S. banks have been in the news for creating accounts for the purpose of collecting higher fees from their customer base, lowering the threshold of trust.

Energy and Natural Resources Market

Strengths

- Crude oil was the top performing commodity for the week, with WTI prices rising 7.9 percent. The commodity rallied after OPEC agreed to its first production cut in eight years on Wednesday. The organization has revealed it seeks to reduce production to a range of 32.5 million to 33 million barrels a day from 33.4 million currently.

- The best performing sector for the week was the S&P 500 Oil & Gas Exploration and Production Index. The index of oil producers rose 7.2 percent for the week as markets reacted favorably to the OPEC production agreement.

- Chemtura Corp., a producer of specialty chemicals, was the best performing stock in the broader natural resource space for the week. The Philadelphia-based company gained 16.4 percent for the week after it agreed to a takeover by German peer Lanxess AG.

Weaknesses

- Iron ore was the worst performing commodity for the week, dropping 6.3 percent. The commodity declined as steelmakers’ margins continued to decline amid high coking coal prices. In addition, high stockpiles in Chinese ports reached a five-week high.

- The worst performing sector for the week was the S&P 500 Utilities Sector Index. The index dropped 3.85 percent for the week as investors rotated to riskier alternatives in the energy space after crude prices rallied in response to the OPEC production deal.

- The worst performing stock for the week in the broader natural resource space was K+S AG. The German fertilizer producer dropped 5.9 percent after Deutsche Bank downgraded its recommendation on the stock to “sell.” The bank cited global crop inventories at the highest level since 2001, negatively impacting farmers’ economics and their ability to increase purchases of fertilizers.

Opportunities

- Macquarie has revised its 2016 metals demand higher to reflect improved conditions in China. The chart below shows Macquarie’s real demand expectations for major industrial metals at the start of the year and where they now sit. All have been increased, with steel now positive. The bank’s analysts argue that 2016 has not been a stellar year by any measure, but has posted decent growth that surprised most proponents of the China “Armageddon scenario.” Moreover, the authors believe China’s fixed asset injection push will be supportive of demand over the coming months.

- The China Caixin manufacturing PMI rose to 50.1 in September. The index posted its third-consecutive expansionary reading, while VTB Capital suggests with the Caixin PMI at or above 50 for the whole of the third quarter of 2016, for the first time since the third quarter of 2014, the signs remain encouraging. The rising PMI should be positive for commodity demand, as studies have demonstrated that a rising manufacturing PMI can be a leading indicator for commodity demand.

- Quarter-end positioning at the Shanghai metals exchange suggests markets may be in for a much better fourth quarter in 2016. As VTB Capital reports, on the last day of the third quarter and ahead of the Golden Week holiday, SHFE base metal stocks fell sharply, with copper down 18 percent, aluminum 19 percent, and zinc down 10 percent. The moves have been attributed to businesses’ anticipation of higher demand to come in the fourth quarter.

Threats

- Global trade will grow this year at the slowest pace since the global financial crisis, warns the World Trade Organization (WTO). The WTO cut its forecast for the growth of exports and imports this year and next, and now foresees an increase of just 1.7 percent in 2016 and as little as 1.8 percent in 2017, having projected rises of 2.8 percent and 3.6 percent, respectively, in April.

- Chinese cities have once again moved to halt a housing market frenzy. The FT reports that following a 15-month price surge in the country’s biggest cities, municipal governments have moved this week to reduce what Beijing sees as excess speculation. Previous attempts to curtail speculation in the housing market have resulted in significant price drops, and a slowdown in new construction activity, with negative follow-through for overall commodity demand.

- Port data suggests iron ore shipments were weaker than expected for the September quarter. Most at risk are the Australian producers, whose shipments may have been as much as 6 percent lower than expectations, according to Macquarie. Lower shipments may result in negative earnings’ revisions and downgrades for a number of diversified global mining companies.

China Region

Strengths

- The September Caixin China Manufacturing PMI came in at 50.1, in line with analysts’ expectations and slightly better than August’s print of 50.0.

- Year-over-year Industrial Production in Taiwan for the August period surged to a gain of 7.74 percent, a high for the trailing year and far ahead of an anticipated gain of only 4.0 percent.

- Vietnam’s third quarter GDP came in at a year-over-year growth rate of 5.93 percent, beating expectations for a gain of 5.83 percent.

Weaknesses

- Year-over-year retail sales in Hong Kong for the August period declined more than analysts’ expectations, falling 10.5 percent rather than an anticipated decline of only 6.9 percent.

- The Hang Seng Composite Industrial sector led declines in the Hang Seng Composite Index (HSCI) for the week, falling 3.22 percent during a week in which the HSCI fell 1.92 percent and only the HSCI’s energy sector gained.

- Singapore’s Industrial Production came in weaker than expected, up only 0.1 percent for August, shy of analyst’s expectations for a gain of 0.5 percent.

Opportunities

- The International Monetary Fund’s (IMF) Christine Lagarde referred to the Chinese yuan’s upcoming inclusion in the IMF Special Drawing Rights (SDR) basket of currencies as an “historic milestone” signifying marked progress in China’s financial system and stability. The yuan takes its place in the SDR basket along with the U.S. dollar, the euro, the yen and the British pound sterling.

- Mainland China will be closed all next week for “Golden Week” celebrations of the People’s Republic of China’s 1949 founding, providing some potentially positive mainland sentiment and a break in trading as investors enjoy a lengthy holiday period.

- This evening China releases its official September Manufacturing PMI (50.5 expected) as well as Non-Manufacturing PMI (last print 53.5), while early next week Caixin will release the China Services PMI (last print 52.1). Investors will also get PMI prints from several other countries across the region.

Threats

- Chatter of a possible upcoming visit to Macau from China’s Premier Li Keqiang may negatively affect gaming revenue for a short period, though perhaps not in the same manner or extent that President Xi Jinping’s 2014 visit did.

- Late next week investors should receive updates on China’s foreign reserves for the September period, an always-closely-watched number that should continue to provide some indication of levels of stability, capital flows, and People’s Bank of China activity.

Emerging Europe

Strengths

- Ukraine was the best relative performing country this week, losing 15 basis points. The government submitted its 2017 budget draft to parliament, targeting a deficit of 3 percent of GDP, down from 3.7 percent projected for 2016. The draft projects real GDP growth of 3 percent and inflation of 8.1 percent.

- The Russian ruble was the best currency this week, gaining 2 percent against the dollar. Currency climbed to a two-month high as crude oil extended gains following OPEC’s deal to cut oil production. Last time when the ruble touched 63 per dollar in July, Vladimir Putin warned that the currency’s advance should be closely monitored.

- The energy sector was the best performing sector among Eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 4.1 percent. Turkish assets plunged the most after Moody’s joined S&P in cutting the nation’s credit rating to junk. Two out of three leading investment agencies now have below-investment-grade ratings on Turkey’s creditworthiness.

- The Turkish lira was the worst performing currency this week, losing 1.1 percent against the dollar. Turkish equities and currency sold off after Moody’s decision. Also,President Recep Erdogan asked the government to extend the state of emergency, saying that “even 12 months” will not be long enough to finish a crackdown following July’s coup attempt.

- The real estate sector was the worst performing sector among Eastern European markets this week.

Opportunities

- OPEC’s decision to cut production to 32.5 million barrels per day is the first reduction since 2008. The details of which country is going to cut and by how much will be negotiated at the November 30 meeting. Russia, which gets most of its budget revenue from the sale of oil and gas, should benefit from higher oil prices.

- The Turkish energy minister stated that there will be a 10 percent cut in natural gas prices, effective October 1, 2016. Cheaper gas could potentially lower production costs for glass, chemical and utilities companies.

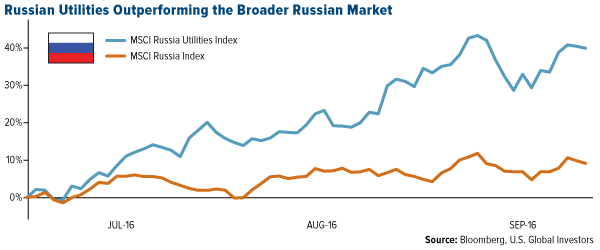

- Over the recent months, there has been a concerted effort to fight corruption in the Russian utilities sector, according to Rencap research team. Company managers have been detained or are under investigation for wrongdoing and acting for their own benefits. The exposure of corruption in the sector may lead utilities to be more transparent and more profitable. The chart below shows the utility sector outperforming the broader Russian market over the past three months.

Threats

- Chernomorskiy Igor from UNLU Securities commented in his research that increasing oil prices are associated with stronger prospects for emerging markets on a broader scale, but it negatively affects countries like Turkey that are major importers of the commodity. Higher crude oil prices negatively affect the energy trade deficit and current account balance. According to his calculation, every $10 change in the crude oil price raises the annual energy bill by $3-4 billion.

- Hungary will hold a refugee referendum on October 2. The referendum question is: “Do you want the European Union to be able to order the mandatory settlement of non-Hungarian citizens in Hungary without parliament’s consent?” At least 50 percent turnout is needed to make the referendum valid. Viktor Orban is working against the EU plan to impose refugee quotas on bloc members.

- Russia’s finance minister Anton Siluanov warned that the budget gap will be wider this year than earlier forecasted. It may widen to 3.5 to 3.7 percent of gross domestic product, beyond the prior estimate of 3.2 percent. The central bank has pointed to delays in improving business climate as the main hurdle for sustained growth in the economy.

© US Global Investors