There were concerns throughout the summer that U.S. economic conditions had weakened. Based on incoming reports, though, the weight of economic evidence remains positive.

Real gross domestic product (GDP) is predicted to have risen 2.5% in the third quarter, which exceeds the potential capacity of the economy. Inflation is still below the Fed’s target, but it has been rising and is eventually expected to reach this mark.

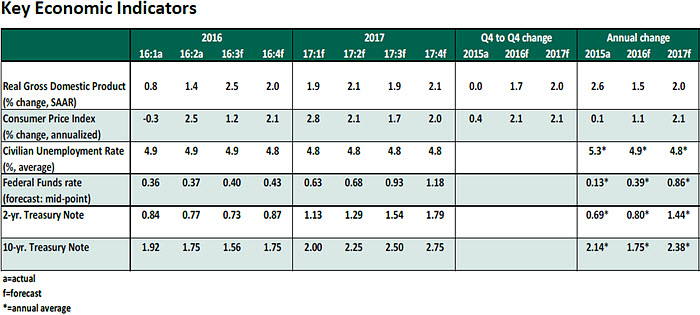

Key Elements of the Forecast

- Real consumer spending slipped 0.1% in August after a 0.3% increase in July. The August spending weakness was in large part due to a drop in auto sales, buy they rebounded in September (17.7 million units vs. 17.0 million units in August). Expenditures on services grew at a slower pace in July and August compared with the recent trend. Reflecting these developments, third quarter consumer spending is predicted to advance, but at a slower pace than the 4.3% increase seen in the third quarter.

- Business investment spending could be turning the corner after a long stretch of weakness. The August durable goods report included an increase in orders of core durable goods. The Institute of Supply Management’s September survey points to a pickup in new orders and production indicating an expansion in activity. The oil rig count rose in the third quarter and suggests non-residential structures are most likely to add to growth in the near term.

- Housing sector data were disappointing. New home sales fell 7.6% August after a nearly 14% surge in July, while existing home sales slipped in July and August. The Pending Home Sales Index, a leading indicator of existing home sales, declined 2.4% in July. Housing starts dropped 5.8% in August. Taken together, these numbers suggest a weak outlook for residential investment expenditures in the third quarter. The fundamentals that drive housing market activity are solid, though, and suggest the third quarter could be a temporary setback.

- The unemployment rate moved up to 5.0% in September from 4.9% in the prior month, despite an increase in employment. It reflects an improvement in the participation rate, which is a positive development. Non-farm payrolls increased 156,000, a smaller gain than in the prior two months but more than the adequate to keep the jobless rate steady. Hourly earnings moved up and the work week was longer. Wage data from other reports point to a larger acceleration. The Employment Cost Index rose 2.3% in the second quarter after a 1.9% increase in the prior quarter. The main message is that the labor market continues to record progress and the economy is close to full employment.

- The personal consumption expenditure price index moved up 0.2% in August, putting the year-to-year increase at 1.0%. The core personal consumption expenditure price index rose 1.7% from a year ago, up 30 basis points from December 2015. This reading is the highest since September 2014. The strength of the dollar exerted downward pressure and held back inflation during most of 2014 and 2015, but it has leveled off this year. Inflation expectations are climbing up gradually. The implied 5-year forward inflation rate at 1.77% is roughly 30 basis points higher than the low recorded in June. Putting these numbers together, there is meaningful movement toward the Fed’s 2.0% inflation target.

- The 10-year Treasury note yield rose to 1.77% on October 11, a 4-month high. A host of bearish factors are governing the bond market. The Fed is predicted to raise the policy rate in December, the increase in oil prices has lifted market-based measures of inflation expectations, and there is concern that the European Central Bank and the Bank of Japan may scale back asset purchases soon. There is a view evolving that fiscal spending should step up to boost growth and combat low inflation. If this policy option is the chosen path, it has the potential to push government bond yields higher. For now, the 10-year Treasury note yield is still far from the 2.36% high seen at the end of 2015.

- The Fed’s latest projections indicate continued forward economic momentum but it revised down the estimate of long-run potential growth to 1.8% from 2.0%. For the near term, the nature of incoming data support expectations of a December rate increase. Also, 14 out of 17 Federal Open Market Committee members project a higher federal funds rate at the end of the year and the Fed sees risks as balanced.