Just as April showers bring May flowers, plentiful monsoon rains in India tend to drive up demand for gold jewelry among rural, income-flush farmers, who make up a third of the country’s consumption of the yellow metal.

It’s a relief to hear, then, that India just had its best monsoon season in three years, with heavy rains washing away people’s fears of yet another drought.

Add to that the fact that the yellow metal is now trading in the affordable $1,250 to $1,260 range—a sizeable discount from only a month ago—and gold jewelry sales are expected to surge as much as 60 percent over last year, according to the India Bullion and Jewellers Association.

That would take sales to a four-year high as we near Diwali—traditionally a time when gold-buying is considered auspicious—which would help support prices.

Following Diwali comes the important Indian wedding season. It’s almost impossible to exaggerate how massive this industry is, with one India-based research firm expecting it to hit 1.6 trillion rupees ($24 billion) by 2020.

I’ve shared with you before that between 35 percent and 40 percent of a typical Indian wedding’s expenses is devoted to gold jewelry. If we use the higher estimate, that means close to $10 billion could be spent on gold alone.

But for spending like this to happen, a strong monsoon is needed, which farmers in many parts of India got this year.

A Longstanding History of Driving the World Gold Market

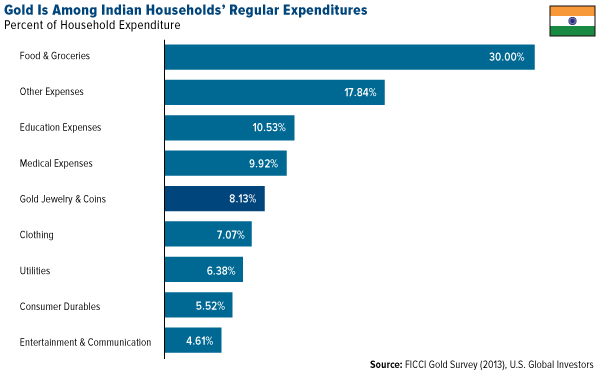

For millennia, gold has played a key role in Indian culture, valued not only for its beauty and durability but also as financial security. That’s no less true today. A 2013 survey conducted by the Federation of Indian Chambers of Commerce & Industry (FICCI) found that more than three quarters of Indians view the precious metal as a “safe investment.”

The same FICCI study also found that gold is a regular line item in most Indian households’ budgets, comparable to what they spend every year on medical expenses and clothing.

It should come as little surprise, then, that Indian households have the largest private gold holdings in the world. Standing at an estimated 23,000 tonnes, and worth close to a whopping $1 trillion, the amount surpasses the combined official gold reserves of the United States, Germany, Italy, France, China and Russia.

Analysts: Gold Is Setting Up for a Big Comeback

After logging its best first half of the year in 40 years, gold is now trading range-bound while we await the Federal Reserve’s decision to raise rates in December. Most, but certainly not all, of the recent economic data seems to be pointing in this direction, with initial jobless claims at a four-decade low, voluntarily quits at pre-recession levels and household income finally on the rise.

Last week was especially brutal. With markets in China, the world’s largest consumer, closed in observance of Golden Week, the short sellers had free rein, driving the price down more than 3 percent on Tuesday alone.

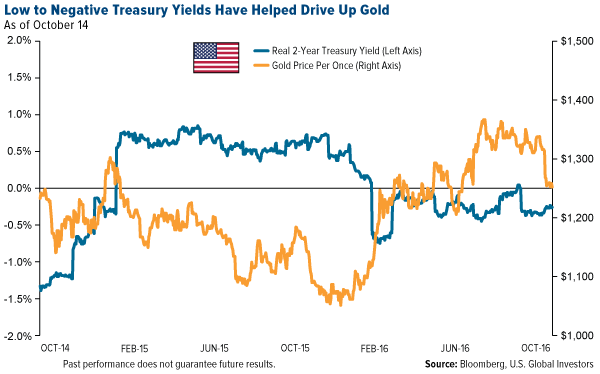

Despite the weakness, inflows into gold ETFs continued to pour in during this week and last, as savvy investors recognize that real, or inflation-adjusted, Treasury yields are still in negative territory. I use the 2-year yield here because it’s what many currency traders look at it.

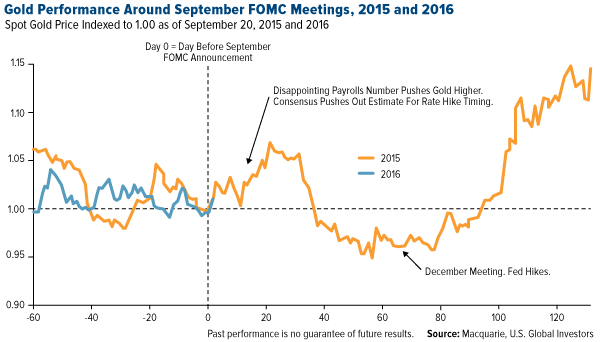

But now some analysts see gold ready to turn again, perhaps prefacing a rally that could carry the metal to an all-time high.

In a note this week, UBS said that as long as the Fed doesn’t hike rates too quickly, gold should resume its upward momentum. And remember, the bull market was triggered last December after the Fed raised rates for the first time in nearly a decade.

Meanwhile, London-based investment firm Incrementum suggested this week that gold could reach a new record within the next two years, supported by higher consumer prices, low to negative government bond yields and a lack of confidence in central bank policy.

“In this uncharted territory, with big monetary experiments going on, it just makes sense” to hold bullion, Ronald Stoeferle, a managing director at Incrementum, told Bloomberg.

Peak Platinum and Palladium Demand?

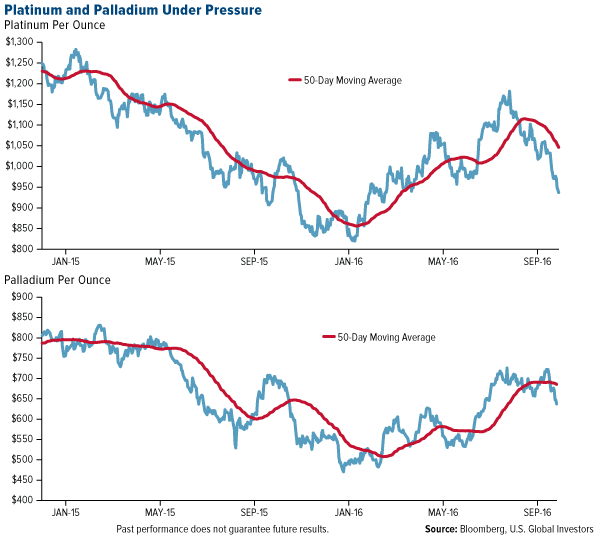

Consensus suggests gold has a positive long-term outlook, but platinum and palladium might be looking at an uncertain future.

As you probably know, the platinum-group metals (PGM) are used predominantly in the fabrication of automobile catalytic converters, which are responsible for reducing emissions. Platinum is used in diesel-powered engines, palladium in gasoline-powered engines.

With vehicle sales in China rising rapidly, demand for PGMs is still strong. In fact, demand for palladium rose 3 percent this year, hitting a fresh all-time high, according to CPM Group.

But trouble could be brewing as more and more automakers, to comply with international environmental regulations and meet consumer demand, deepen their shift toward battery-electric vehicles (BEVs). Since these vehicles don’t have an internal combustion engine, there are no emissions, meaning PGMs are not needed.

Government policy has largely driven the emphasis on BEVs, with a few nations around the world committed to banning internal combustion engines from roads within the next 10 to 20 years.

Norway was the first, pledging to eliminate them by 2025, less than 10 years from now. The Netherlands is considering a similar ban, effective the same year. And India wants to be the first “100 percent electric vehicle nation” by 2030.

This week, Germany—the world’s fourth-largest automobile manufacturer, home to Audi, BMW, Mercedes-Benz, Porsche and Volkswagen—voted to do away with all fossil fuel-powered vehicles within 15 years.

In its platinum and palladium outlook, Metals Focus writes that “for every additional 1 percent of global passenger car production that BEVs claim in 2020, our model suggests a loss of more than 100,000 ounces (3 tonnes) of combined PGMs offtake that year.”

All in all, not good for PGMs.

However, it is good for copper. As I’ve pointed out before, BEVs use about three times as much copper wiring as traditional combustion engines vehicles.

It’s important to recognize that disruptive technologies have always changed markets. Right now, one of them is battery-electric vehicles. Embrace them or not, the decision is yours. But as investors, we must acknowledge which way the wind is blowing, and adapt—or be left behind.

Don’t Forget to Register for MoneyShow Dallas!

Speaking of disruptive technologies, virtual reality is quickly going mainstream, with Facebook’s Oculus Rift and other VR headsets likely to become one of the next must-have consumer items.

You don’t need one of these pricey rigs to enjoy the MoneyShow Dallas virtual event, though—just an internet connection. Next week I’ll be at the MoneyShow, where I’ll be presenting and learning. And if you can’t be there physically, you can always be there virtually to hear from leading economists, premier money managers and top analysts, who will share their best insights, perspectives and strategies to grow your portfolio.

I hope you’ll join me!

The French Are at It Again

One final note: Last month, I shared with you the story that European regulators were going after big Americans companies such as Netflix, Facebook, Amazon and more. Their envy policies demand that, if they can’t build their own companies that are just as successful, they’ll tax and regulate them into non-competitiveness.

This socialist mindset is now taking aim at internet content providers.

This week, according to Zero Hedge, the French parliament introduced a bill that, if enacted, would levy a 2 percent tax on all ad-generated revenue on sites that distribute free content—sites such as YouTube and Dailymotion (a France-based video-sharing site).

This is just the latest example of how Europe is undermining American companies. Why hasn’t Europe created its own Netflix or Facebook? Where’s its Silicon Valley? The continent’s miles of red tape and envy policies have essentially prohibited entrepreneurism and innovation. And instead of relaxing regulations, it chooses to punish U.S. firms for their success.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.56 percent. The S&P 500 Stock Index fell 0.96 percent, while the Nasdaq Composite fell 1.46 percent. The Russell 2000 small capitalization index lost 1.95 percent this week.

- The Hang Seng Composite lost 2.32 percent this week; while Taiwan was down 1.09 percent and the KOSPI fell 1.52 percent.

- The 10-year Treasury bond yield rose, 8 basis points to 4.65 percent.

Domestic Equity Market

Strengths

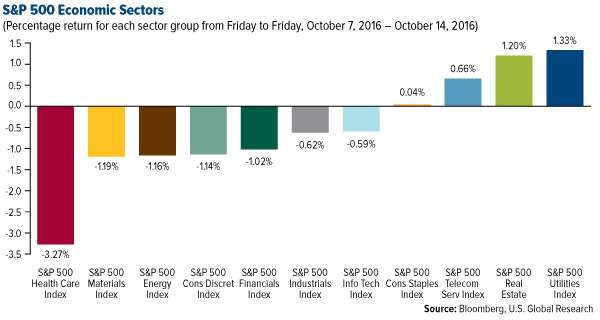

- Utilities was the best performing sector for the week, increasing 1.33 percent vs. an overall decrease of 0.96 percent for the S&P 500 Index.

- Ulta Salon was the best performing stock for the week, increasing 9.91 percent. The company had a successful analyst day and raised near-term guidance on a strong view of where its business is heading. Ulta sees expansion to 1,700 stores in the U.S., while also growing same-store sales at a healthy clip.

- Noble Group is selling its North American energy distribution unit to Calpine. The $1.05 billion deal gets Noble closer to its goal of raising $2 billion and cutting debt, Reuters reports.

Weaknesses

- Health care was the worst performing sector for the week, falling 3.27 percent vs. an overall decrease of 0.96 percent for the S&P 500.

- Illumina was the worst performing stock for the week, falling 25.20 percent. The company’s shares plunged after it warned that its third-quarter sales were likely to come in below its forecast.

- Samsung is taking a big hit because of the Galaxy Note 7 fiasco. Samsung says its recall of the fire-prone Galaxy Note 7 will cost $3 billion (3.5 trillion won) in operating profit, with the majority of that total ($2.2 billion) affecting its bottom line next quarter.

Opportunities

- Goldman Sachs is ready to lend you money. The firm officially launched its consumer loan platform, Marcus, which will offer fixed-rate, no-fee personal loans of up to $30,000 for two- to six-year periods.

- Health insurer Humana raised expectations for its quarter. The firm raised its guidance by $0.25 per share.

- Tesla has a new product in the works. Elon Musk announced on Twitter that a new product "unexpected by most" would be announced on October 17, just 11 days before the SolarCity/Tesla solar roof unveiling.

Threats

- Low global interest rates have enticed CEOs to change the capital structure of the firm by issuing debt and retiring equity, artificially boosting earnings per share (EPS). This is not sustainable, and deteriorating corporate sector health will likely exert downward pressure on equity prices.

- Deutsche Bank raised more cash. On Tuesday, the bank raised $1.5 billion through the sale of five-year notes. That comes after Friday's offering that raised $3 billion.

- Twitter plunged after Salesforce ruled out a bid. Salesforce CEO Marc Benioff told the Financial Times that Twitter "wasn’t the right fit for us."

October 11, 2016What We Look For When Picking Superior Gold Stocks |

October 10, 2016No Love for Gold |

October 5, 2016We Believe Congress Is About to Give this Asset Class a Huge Promotion |

The Economy and Bond Market

Strengths

- Retail sales rose as expected. Sales rose 0.6 climbed month-over-month in September, according to the Commerce Department, right in line with expectations.

- Month-over-month Producer Price Index Final Demand for September came in at 0.3 percent, beating expectations of 0.2 percent.

- Initial jobless claims came in at 246,000, below the expected 253,000.

Weaknesses

- The Univeristy of Michigan Consumer Confidence Index unexpectedly fell to its lowest level since September. The index came in at 87.9 for October, below expectations of 91.8, and below September's final reading of 91.2.

- Job openings fell short of expectations. The Job Openings and Labor Turnover Survey (JOLTS) showed the number of job openings in the U.S. came in at only 5.4 million, less than the projected 5.8 million.

- The NFIB Small Business Optimism Index came in at 94.1, below the expected 95 and the previous month’s 94.4.

Opportunities

- The Federal Reserve looks ready to raise rates. The release of the Federal Open Markets Committee (FOMC) minutes for the September meeting seemed to point to a rate hike in the near future as the members saw a strong labor market and improving inflation.

- The month-over-month Consumer Price Index (CPI) for September will be reported next Tuesday and is expected to come in at 0.3 percent, higher than the previous 0.2 percent. This would be a positive sign for the economy.

- Month-over-month industrial production for September will be reported next Monday and is expected to come in at 0.2 percent, higher than the previous -0.4 percent. A bounce in production is a much needed sign of stability.

Threats

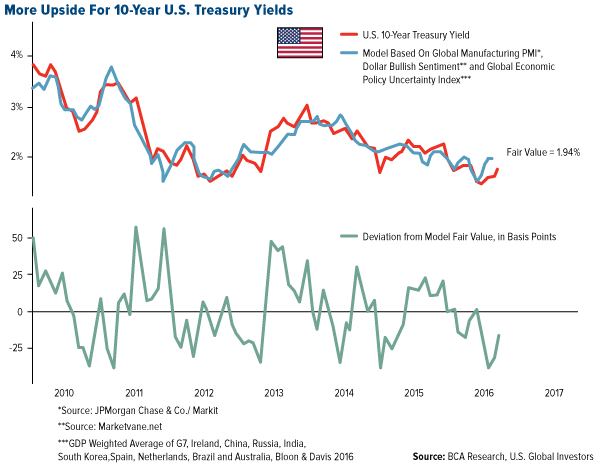

- Even after the recent selloff in bonds, BCA’s fair value model shows that the 10-year Treasury yield still has room to grind higher. The firm’s fair value model is based on economic uncertainty, global growth and the divergence between U.S. and global growth. Spikes in economic uncertainty tend to drive a flight-to-safety into Treasury securities. The Global Economic Policy Uncertainty Index has receded from the post-Brexit highs, which is lifting the fair-value of 10-year yields. U.S. Treasury yields should follow suit. If the model’s forecast materializes, bonds should have more downside in the near-term.

- The Fed is worried about the housing market. As part of the minutes, the Fed mentioned the "sluggish" housing market and cited constrained supply as a reason for the slowdown.

- The U.S. Leading Economic Index (LEI), reported next Thursday, has been in an overall downtrend and an upturn is needed to support the Fed's outlook for continued rate hikes next year.

Gold Market

This week spot gold closed at $1,251.66, down $5.27 per ounce, or 0.42 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week slightly higher by just 0.25 percent. Junior miners underperformed seniors for the week, as the S&P/TSX Venture Index fell back just 1.00 percent. The U.S. Trade-Weighted Dollar Index finished the week up 1.48 percent.

|

Oct-11 |

Germany ZEW Survey Current Situation |

55.5 |

59.5 |

55.1 |

|

Oct-11 |

Germany ZEW Survey Expectations |

4.0 |

6.2 |

0.5 |

|

Oct-13 |

Germany CPI YoY |

0.7% |

0.7% |

0.7% |

|

Oct-13 |

U.S. Initial Jobless Claims |

253k |

246k |

246k |

|

Oct-14 |

U.S. PPI Final Demand YoY |

0.6% |

0.7% |

0.0% |

|

Oct-17 |

Eurozone CPI Core YoY |

0.8% |

-- |

0.8% |

|

Oct-18 |

U.S. CPI YoY |

1.5% |

-- |

1.1% |

|

Oct-18 |

China Retail Sales YoY |

10.7% |

-- |

10.6% |

|

Oct-19 |

U.S. Housing Starts |

1175k |

-- |

1142k |

|

Oct-20 |

ECB Main Refinancing Rate |

0.000% |

-- |

0.000% |

|

Oct-20 |

U.S. Initial Jobless Claims |

250k |

-- |

246k |

Strengths

- The best performing precious metal for the week was gold, losing slightly less than a half of 1 percent, followed closely by silver with just a 0.78 percent decline. These metals largely stabilized following the prior week’s significant decline.

- This week’s combination of weak export data from China and talk of a rate hike from the Federal Reserve sent traders rushing into the safety of bonds, yen and gold on Thursday, reports Bloomberg. “China’s trade data below estimates is an overhang in the market, and from Europe, we’re hearing about a hard Brexit that’s making markets more jittery,” said Jeff Zipper, managing director of investments for the Private Client Reserve of U.S. Bank. The Chinese data boosted gold, but sent copper lower as it undermined the confidence in the global economy.

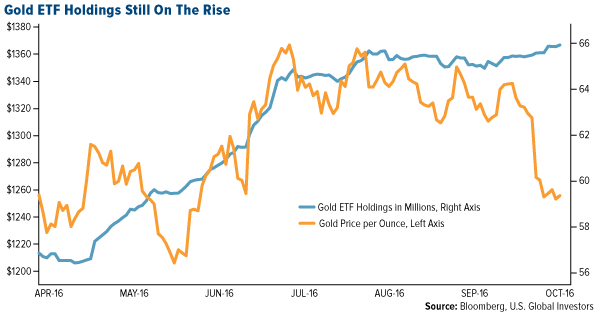

- Despite weak gold futures prices, inflows into gold ETFs continue to strengthen, as seen in the chart below. The worst week for gold futures in a year actually attracted ETF inflows, reports Bloomberg, adding that it “may take a substantial sentiment shift and persistently lower prices to dislodge gold holdings.”

- Nighthawk Gold reported drilling results this week, noting an intersect of 72.65 meters of 5.58 grams per ton gold at Colomac. According to the company’s press release, these results show that the zone continues uninterrupted down plunge and supports its continuity of mineralization to depth. The note also points out similarities between Colomac and Kalgoorlie by President and CEO Dr. Michael Byron—Kalgoorlie is one of the world’s largest Archean gold camps. An additional announcement by the company on Thursday reported that Kinross Gold has made a strategic investment in Nighthawk, and will hold approximately 9.5 percent of Nighthawk’s issued and outstanding common shares on an undiluted basis.

Weaknesses

- The worst performing precious metal for the week was platinum, with a fall of 3.50 percent. Palladium was almost as bad, with prices slipping 3.44 percent. Mineweb noted that the dominant union in the platinum industry in South Africa may be looking to sign off on wage package, thus potentially avoiding a strike.

- According to Bloomberg, the Fed has put gold bulls on the defensive again. Investors cut their bullish bets last week, sending gold’s open interest (a tally of outstanding contracts) near a four-month low, the article continues. Traders are pricing in the odds of a rate hike by year end—at the end of September the chance of a hike by December rose to 68 percent. During the Fed’s latest meeting, several officials said a rate hike was needed “relatively soon,” reports Bloomberg, sending spot gold near a four-month low.

- Bank of America has its own thoughts on how investors and traders should use gold, as recommended in a note out this week. The bank writes to go long Italian shares, while shorting the yellow metal as a source of funds. Their reasoning? A 23-percent slump in Italy’s FTSE MIB Index this year has pushed the gauge’s valuation to a four-year low, reports Bloomberg, while the Fed prepares to increase borrowing costs.

Opportunities

- Klondex Mines reported positive updates on recent and historic exploration results at its Hollister Mine in Nevada this week, noting multi-ounce per ton intercepts. In 2014 and 2015, a total of 36 underground holes totaling 17, 998 feet were drilled by the prior owner of the Gloria zone and not previously released. According to Klondex, these holes encountered multiple veins and extended the Gloria vein approximately 800 feet to the West and around 300 feet vertically. Several members of the company’s team have significant experience with and knowledge of Hollister. Klondex President and CEO Paul Huet also commented on its 2016 production guidance: “Our third quarter production was in line with our mine plans as we advanced waste development at both Fire Creek and Midas. We have positioned ourselves to finish the year on a high note and remain on track to achieve our annual production guidance.”

- Ronald Stoeferle, managing partner at Incrementum AG, believes gold could climb to a record over the next two years, suggesting the yellow metal could reach $2,000 in 2018. According to Stoeferle, rising inflation and sagging confidence in the ability of central banks to revive global growth will drive prices higher, reports Bloomberg, also noting that inflation may “surprise to the upside” which would be good for gold.

- Historically, the months of September and October have been a good time to invest in gold, according to Unum Capital. In an email note, trader Rob Pietropaolo says that over time, the gold price has become quite predictable for a very specific reason. “September is typically the month when traders start buying ahead of India’s festivals and wedding season,” he said. “Gold is India’s biggest import item after crude oil.”

Threats

- The German Federal Council adopted a bipartisan measure last week that would ban the sale of new vehicles with internal combustion engines by 2030, reports Noah Capital Markets. As one of the biggest producers of motor vehicles in the world, car makers like VW, Mercedes and BMW will likely lead the rest of the world, which will follow in the next few years, the note continues. Although small globally, Germany’s car producers do make many diesels driven vehicles, which are important to the platinum market since they are the main consumers of the metal. This new measure would account for a significant loss of market share for platinum, around 5 percent, in Germany. If the rest of Europe followed, it would rise to 20 percent.

- ABN Amro thinks gold’s uptrend is over, noting the price falling below its 200-day moving average. Citing the U.S. interest rate outlook and investors’ large positioning in futures and ETFs, the group has no expectation for substantial pickup in bar demand. It cut its 2016 year-end forecast to $1,200 an ounce, and its 2017 year-end forecast to $1,150. “It is unlikely that investors will add to their positions in the short term, which means that they will sell on rallies,” said strategist Georgette Boele.

- The University of Michigan reported that its preliminary consumer sentiment survey dropped to its lowest in more than a year, falling to a reading of 89 and well below consensus expectations, reports MarketPulse. Gold was in negative territory ahead of the report, and dropped a bit in reaction to the positive September retail sales data, although it’s rebounded a bit since then. “It is likely that the uncertainty surrounding the presidential election had a negative impact, especially among lower income consumers,” survey director Richard Curtin wrote in a release.

Energy and Natural Resources Market

Strengths

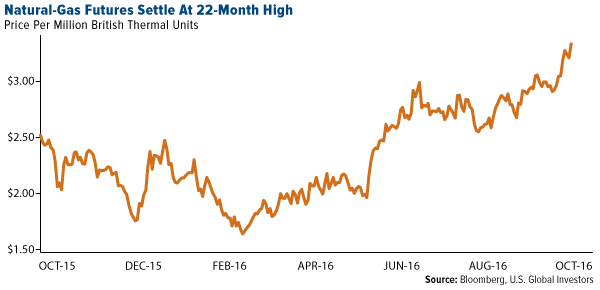

- Natural gas prices rose to a 22-month high after inventories continue to build at a slower pace into what is widely expected to be a cold winter. With inventories building below seasonal norms, a couple of cold weeks before year’s end could result in a very tight gas market over the winter, which could propel gas prices higher.

- The best performing sector for the week was the TSX Diversified Metals and Mining Index. The index of Canadian bulk and base metals producers rose 5.5 percent percent for the week, driven by news of met coal price benchmarks settling at $200 a tonne. Canada is the world’s third largest met coal exporter.

- Klondex Mines, a Canadian junior gold producer, was the best performing stock in the broader natural resource space for the week. The stock gained 7.5 percent percent for the week after reporting promising exploration results at its newly acquired Hollister mine.

Weaknesses

- OPEC oil production set a new monthly record in September. Monthly production climbed to 33.6 million barrels per day last month, a seasonal all-time high that suggests adhering to recently agreed-upon production caps may be difficult. Russia and Kazakhstan, major non-OPEC producers, also boosted production last month by 500,000 barrels per day, adding volumes to an already oversupplied market.

- The worst performing sector for the week was the S&P 500 Auto Parts & Equipment Index. The index dropped 3.9 percent percent for the week as news reports showed Germany is planning to enact regulation to ban gas and diesel vehicles from its roads by 2030.

- The worst performing stock for the week in the broader natural resource space was Alcoa. The New York City-based producer dropped 15.7 percent percent after a disappointing third quarter earnings’ call. The company missed its revenue expectations on weaker upstream pricing. In addition, the company downgraded its profit forecasts for its downstream business segment as it anticipates weaker aerospace deliveries.

Opportunities

- Physical gold ETF holdings continue to rise in spite of the Fed rate hike outlook. Assets in gold-backed ETFs rose to 2,050.3 metric tons as of Thursday, extending gains to reach their highest since 2013.

- Met coal used for steelmaking has seen its benchmark price settle at $200 a tonne, more than twice the price in the previous quarter. Peabody Energy and Nippon Steel have agreed to the 116 percent rise in prices as Asian demand outpaced supply. Prices were last above $200 a tonne in 2012 after major flooding compromised a third of global supply out of Australia.

- Crude prices may rally to $78 a barrel if they crack above $50, says Bloomberg. The report shows crude forming an inverse head and shoulders pattern, which technical analysts indicate may be the force that clears the commodity’s path to $78 a barrel.

Threats

- Disappointing China trade numbers reignite fears global recovery may be faltering. As Reuters reports, China's September exports fell 10 percent from a year earlier, far worse than expected, while imports unexpectedly shrank after picking up in August.

- Aurubis, Europe’s biggest copper smelter is slashing 2017 premiums on its copper cathodes as market outlook weakens. Copper, the worst performing metal this year, is expected to remain oversupplied in 2017 as mine output continues to rise ahead of demand growth.

- Alcoa kicked off the third quarter reporting season with a miss and earnings’ downgrade, casting a shadow over the broader market. Alcoa reported weaker revenues on its upstream division, and lowered earnings’ forecasts for its downstream division, leading investors to question whether the U.S. economy may be on weaker footing.

China Region

Strengths

- Chinese equities were the best outperformers in the region. The Shanghai Stock Exchange Composite Index closed up 1.02 percent this week.

- China’s Producer Price Index (PPI) rose 0.5 percent month-over-month in September, and also rose 0.1 percent year-over-year in September, the first positive reading since January 2012. This indicates that the severe industrial deflation that started two years ago has likely come to an end.

- Fitch upgraded Taiwan by a notch to AA- with stable outlook. Fitch noted that the fiscal outlook was good, driven by strong revenues and prudent expenditures.

Weaknesses

- The Chinese renminbi weakened noticeably following Golden Week holidays and SDR basket inclusion. In a volatile week for FX markets globally, the yuan climbed well above 6.70, which had until lately seemed to mark something of an unofficial ceiling.

- Chinese trade data came in weaker than expected for the September period. Imports fell 1.9 percent versus expectations for a year-over-year gain of 0.6 period, while exports fell 10 percent for the same timeframe (well below an expected decline of 3.3 percent).

- South Korea’s unemployment rate ticked up slightly to 4 percent this week, missing expectations for a steady September print of only 3.8 percent.

Opportunities

- Bloomberg reports that India’s biggest SUV producer, Mahindra and Mahindra, is looking for a joint venture partner in China to manufacture and sell electric vehicles. China has previously announced a target of some 5 million electric vehicles on its road by 2020.

- Despite recent—and perhaps justified—international hullabaloo over some of Philippine President Rodrigo Duterte’s questionable comments and more opaque policies, the populist former Davao City mayor is running an 86 percent approval rating after his first three months in office.

- While problematic in its own way, Indonesia does appear likely to retain its ban on raw nickel ore exports and bauxite, which will hypothetically prevent a flood of supply to the market, which could weigh heavily on pricing.

Threats

- Thailand mourns the death of beloved King Bhumibol Adulyadej (Rama IX), who until his death on Thursday afternoon in Bangkok was the world’s longest-reigning living monarch. The king was 88. Reports of the king’s failing health had in recent days weighed upon the baht and SET Index. One major constant throughout King Bhumibol’s 70-year reign was a fairly regular change of government: Some 10 coups occurred over the last seven decades. Now Thailand, bereft of her own constant in the form of an extraordinarily popular monarch, must continue to demonstrate that the investment climate remains attractive.

- Chinese property and construction names took a few licks this week after government officials in several cities announced additional steps to curb the pace of property price appreciation.

- Samsung risks losing market share as its Galaxy Note 7 battery fiasco drags on.

Emerging Europe

Strengths

- Greece was the best performing country this week, gaining 2.1 percent. Greece is pushing forward with its reforms and it is pleasing the market. Trading volumes are low, however, suggesting low interest in the market. Investors could be waiting for the debt relief talks and Greece’s participation in the European Central Bank’s (ECB’s) quantitative easing program.

- The Ukrainian hryvnia was the best performing currency this week, gaining 16 basis points against the dollar. Leaders of Russia, France, Germany and Ukraine may meet soon to revive peace efforts for Ukraine. However, prospects of a quick solution to Ukraine’s conflict between the government and Russia-backed separatist rebels seem remote.

- The energy sector was the best performing sector among Eastern European markets this week.

Weaknesses

- Poland was the worst performing country this week, losing 1 percent. Losses on the Warsaw Stock Exchange were led by weakness in banks, which sold off to a two-month low after the Polish Security Commission said FX loan bills will cost lenders 9.3 billion zloty, versus government’s numbers of 4 billion zloty.

- The Polish zloty was the worst performing currency this week, losing 2.7 percent against the dollar. The currency remains under pressure from a variety of domestic risk

- Consumer staples was the worst performing sector among Eastern European markets this week.

Opportunities

- The first review of Greek reforms was officially completed on October 10, and the Eurogroup approved partial disbarment of 1.1 billion euros out of the remaining 2.8 billion-euro tranche. The second review is expected to start next week, targeting labor reforms and the legal framework of the trade union. Greek officials are maintaining that the review will be finished by November 7. If Greece can push forward with its reforms, the market should be pleased.

- During the Istanbul Energy Summit, Russia and Turkey once again agreed to build Turkish Stream, a natural gas pipeline under the Black Sea that could be up and running by the end of 2019. This deal will allow Moscow to strengthen it gas market position in Europe and cut its reliance on gas shipments through Ukraine. Currently, between 40 and 50 percent of Russian gas exports to Europe passes through Ukraine. Russia has agreed to provide a 10 percent discount to Turkey.

- According to Berenberg’s research, for a second consecutive week, investors withdrew $13 billion from developed markets equity funds and put $3.5 billion into emerging market equity funds. Overall significant inflows into EM continue on the hunt for yield.

Threats

- Turkey’s Prime Minister Binali Yildirim pledged to bring a draft law that will enable changes to be made in the constitution, bringing in Executive Presidency into Turkey. The current ruling AKP party does not have enough seats in the parliament to change the constitution, but it can take the issue to a referendum. Some analysts say that the referendum is just around the corner, which could bring more social unrest and will present a threat to Turkish democracy.

- According to BCA’s Emerging Markets strategy team, the U.S. dollar’s corrective phase is over, and it is about to rally. This is bad news for emerging markets. Further, the last released FOMC minutes had a hawkish tone, and the futures market is pricing in a 68 percent probability of a rate increase this year, pushing the dollar higher and emerging currencies lower.

- Hungary’s leading leftist newspaper, Nepszabadsag, has been shut and its employees suspended after the publication piled up significant losses despite cost cuts, according to the owner. The radical nationalist Jobbik opposition party blamed right-wing Prime Minister Viktor Orban for the closure, saying his Fidisz party wanted to control the entire Hungarian media.

© US Global Investors