Judging by recent headlines, cash is once again king. The Wall Street Journal recently reported that investor cash levels currently represent 5.8% of portfolios, the highest in 15 years.

Many investors interpret high cash levels as a contrarian indicator, suggesting an excessive level of caution. The logic goes that if cash levels are high, there is more “dry powder” for fund managers to invest. Today, however, there is potentially a different interpretation regarding high cash levels.

With U.S. stocks trading for more than 20x trailing earnings, credit spreads tight and volatility roughly 35% below its long-term average, it is difficult to argue that investors are overly pessimistic (source: Bloomberg). Instead, high cash levels are a rational response to the changing structure of cross-asset correlations.

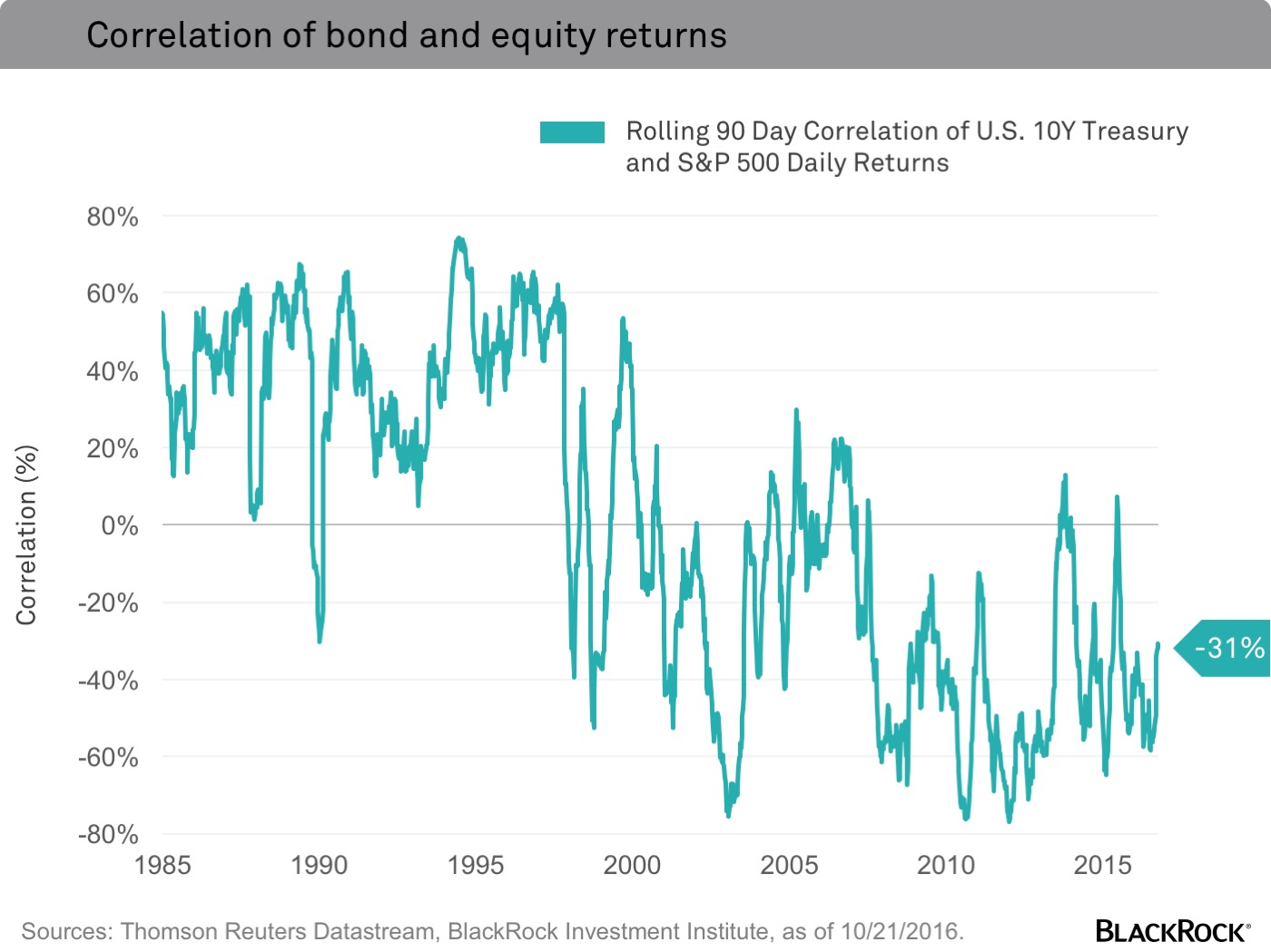

Typically, bonds provide three attributes in a portfolio: income, volatility control and diversification. Slow nominal gross domestic product (GDP) and central bank policy have already conspired to rob bond investors of income. Yet investors have still been aggressive buyers of bonds this year. Why? A large part of the reason has been that bonds have provided an effective hedge against equity risk. Until recently, that is. It is starting to change.

For most of the post-crisis environment bonds have tended to move inversely with stocks. This pattern is consistent with the historic norms: When economic growth and the central bank policy rate are both low, the correlation between stocks and bonds tends to be negative. While growth, both nominal and real, remains muted, central bank policy is evolving. By either choice or necessity, monetary stimulus may be reaching its limits, the Federal Reserve (Fed) is likely to hike rates in December and continue hiking next year.