Very slowly, almost stealthily, international equity markets are clawing back relative to the United States. On a dollar-adjusted basis Japanese stock returns are now on par with the United States, with both the S&P 500 and the Nikkei 225 up around 4.5% year-to-date. And more recently, international markets are actually leading. Since late July the S&P 500 is down over 1%. During the same time period Europe has advanced 1% in dollar terms, a broad emerging market index is up more than 3% and Japan is up nearly 5%. Returns are based on Bloomberg data.

What accounts for the turnaround and, more importantly, can it continue? Three factors stand out:

1. U.S. growth remains uninspiring, despite expectations for a rebound.

The relationship between economic growth and market performance is unreliable and often non-existent. But for a market that is increasingly dependent on earnings growth, a lack of economic growth is a challenge. Although the U.S. economy continues to grow, it is not obvious that it is accelerating. More interestingly, relative to other parts of the world U.S. economic data is disappointing. The Citigroup Economic Surprise Index is once again negative for the U.S. while it is positive for a broader array of major economies.

2. The Federal Reserve will no longer ride to the rescue.

For most of the post-crisis period investors could, and often did, dismiss soft growth on the assumption it would lead to more monetary easing. That is no longer likely. While the Fed has verbally committed to a shallow and short tightening cycle, interest rates are still likely to rise. This is also putting upward pressure on the dollar, which will in turn pressure U.S. earnings.

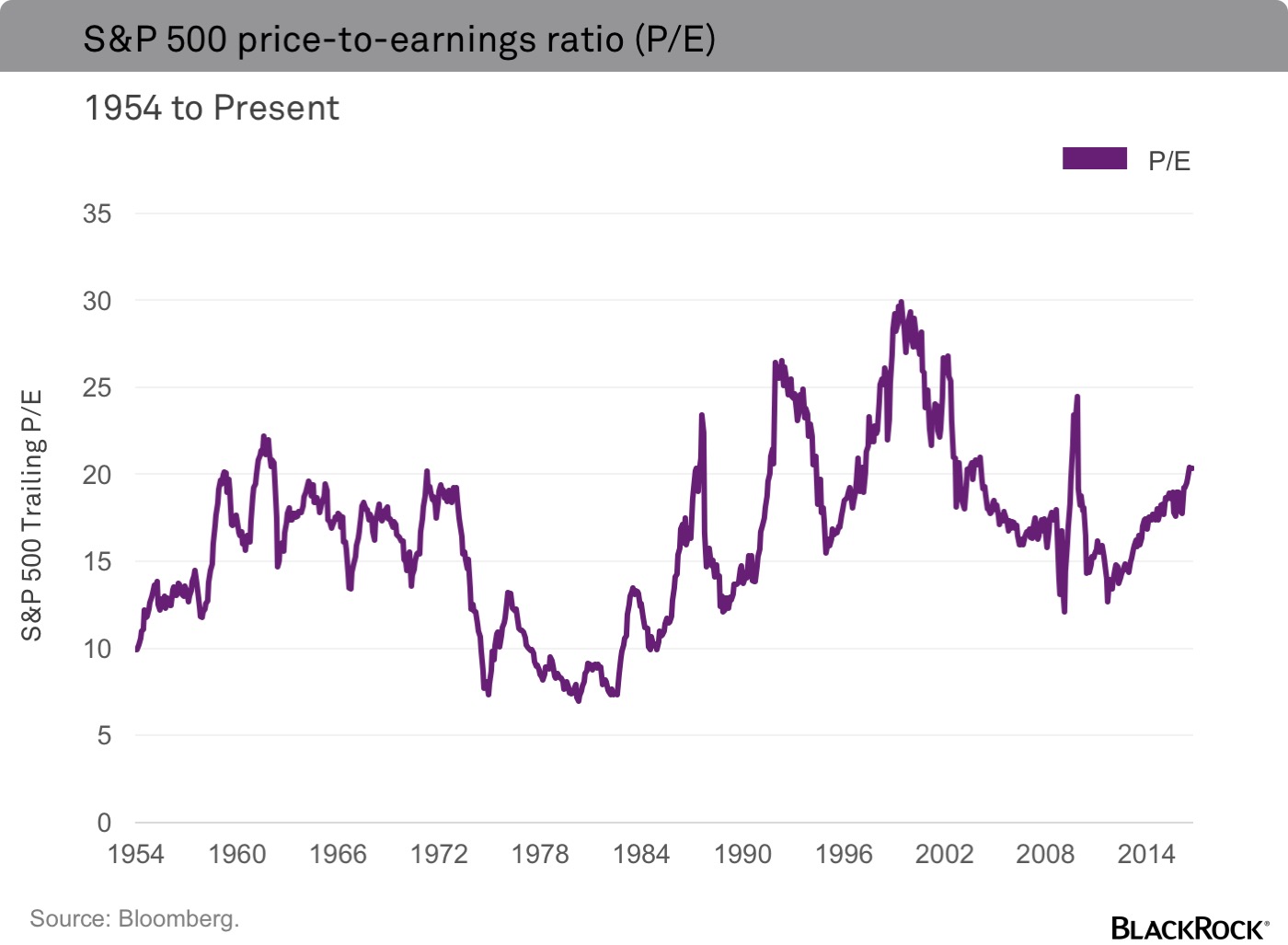

3. U.S. stocks are expensive; other markets aren’t.

As shown in the chart below, U.S. equities are trading at over 20x trailing price-to-earnings (P/E) and over 26x cyclically adjusted earnings (Shiller P/E). Valuations at these levels have historically been associated with lower forward returns. In contrast, equity markets in Europe, Japan and emerging markets appear somewhere between fairly valued and relatively inexpensive.

For long-term investors, the final point is particularly important. Value is often irrelevant in the short term, but over the long term valuations tend to mean-revert. For example, during the past 60 years, annual changes in the P/E of the S&P 500 had a -0.20 correlation with the change the following year.

This is one of the reasons many investors are lowering their long-term return assumptions for U.S. equities. Indeed, the BlackRock Investment Institute forecasts a 4% annual return for large cap U.S. equities over the next five years. This below-average forecast assumes a steady 2% annual compression in multiples. In other words, if correct, investors will be less willing to pay more for each dollar of earnings and stocks will climb at a much slower pace.