Manufacturing Activity in China Just Shifted into Overdrive

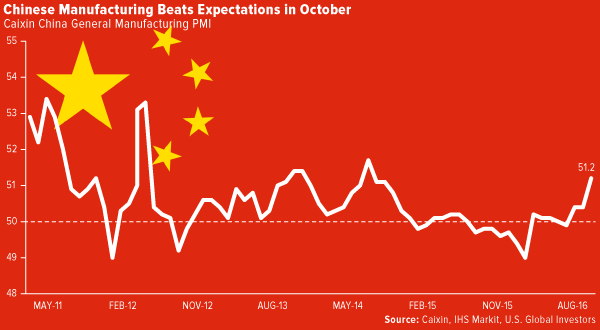

A wave of positive economic data suggests the Chinese economy is stabilizing and that business confidence is improving. The country’s purchasing managers’ index (PMI), which measures the health of its manufacturing industry, rose to 51.2 in October, handily beating economists’ estimates of 50.3.

Expanding at its fastest pace since July 2014, the industry was stimulated by a strong rebound in new orders and higher commodity prices. Output rose to an incredible five-and-a-half-year high. And with backlogs of work beginning to pile up, manufacturers trimmed employees at the slowest pace in 17 months.

Also encouraging is the country’s third-quarter gross domestic product growth, which came in at 6.7 percent for the third straight quarter, all but assuring investors that the economy can achieve the government’s earlier guidance of between 6.5 percent and 7 percent. Higher business confidence helped maintain steady growth, “as proved by the rebound of medium to long-term corporate loans and reacceleration of private investment growth,” according to Singapore-based OCBC Bank.

Consumer spending appears to be robust. In the first nine months of the year, consumption contributed nearly 60 percent to GDP growth, with significant demand gains made in health care, education, financial products and entertainment.

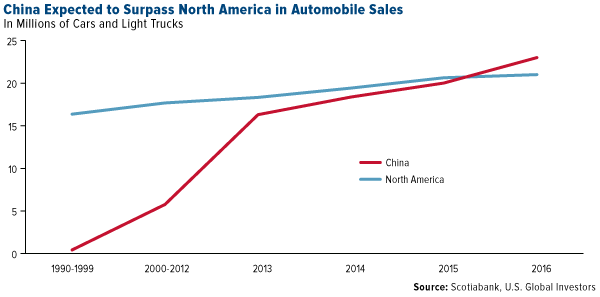

Automobile sales jumped a phenomenal 32 percent year-over-year in September, the fourth straight month of growth exceeding 20 percent. Sales have been so robust—reflecting a rush to purchase new cars before the government’s reduction in sales tax on small vehicles expires at year-end—that new vehicle purchases in China are expected to surpass sales in North America for the first time ever this year.

Such a great number of cars on the road has resulted in famously massive traffic jams that turned miles of highways into parking lots. Some as many as 50 lanes wide, the very worst incidents in Beijing found hundreds of drivers stuck in lines for days. Beijing officials have recently proposed stopgap measures, but the nightmare congestion underscores the need for greater capacity, which will require even more investment from the Chinese government, not to mention untold amounts of cement, asphalt, steel and other materials.

But really, these are traffic jams you have to see to believe.

China Attracting Assets

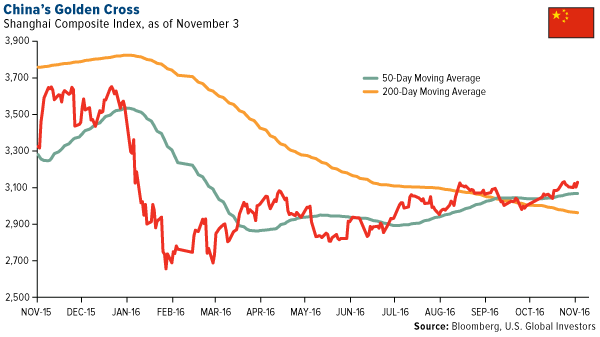

The market seems to like what it sees. The Shanghai Composite Index is back up to levels last seen in January, fueled by not only encouraging manufacturing data but also hopes the government will make good on its promises to support infrastructure spending and restructure state-run enterprises. Stocks recently signaled a bullish “golden cross,” when the shorter-term moving average crosses above the longer-term average.

In a note this week, Goldman Sachs analysts reported they expect reforms to accelerate in the next few years as China transitions from a middle-income country to an advanced economy. Reforms include efforts to restructure or eliminate “zombie” state-owned enterprises and remove marginal capacity. New policies on how to address public corruption have also been floated.

Among ETFs focused on a single emerging market, China funds attracted the largest inflows in the month of October, with new money totaling $275 million, according to Citi Research data.

Inflows into Mexico-focused ETFs were a distant second, at $133 million, indicating a surplus of bets on a Hillary Clinton presidential win next week. (It should be noted, though, that since the FBI announced last week that it would be reviewing just-discovered Clinton emails, Mexico ETFs have turned volatile as the chances of a Donald Trump victory improve.)

Who Will Lead the SEC in a Clinton Administration?

|

While I’m on the topic of the election, I find it worth sharing that a shake-up at the very top of the Securities and Exchange Commission (SEC) could be unfolding in front of our eyes—with some potentially serious ramifications.

Massachusetts Sen. Elizabeth Warren, one of the most outspoken critics of Wall Street serving in Congress today, recently urged President Barack Obama to remove Mary Jo White as head of the SEC for, among other things, failure to fully implement the Dodd-Frank financial reforms.

The White House flatly rejected Warren’s request, but it raises a few questions: Is she positioning herself to run the SEC herself? Could Sen. Warren, a strong supporter of Clinton, be appointed as the new SEC chair if Clinton were to win? What effect would that have on capital markets?

Although pure speculation, the scenario is worth pondering.

Another Infrastructure Boom Ahead?

Much has been made of the Chinese economy’s transition from one driven by industrial production to one supported by consumption and services. While this shift is indeed taking place, China still remains the world’s largest engine for energy and materials demand, with support from a growing population and rising household income.

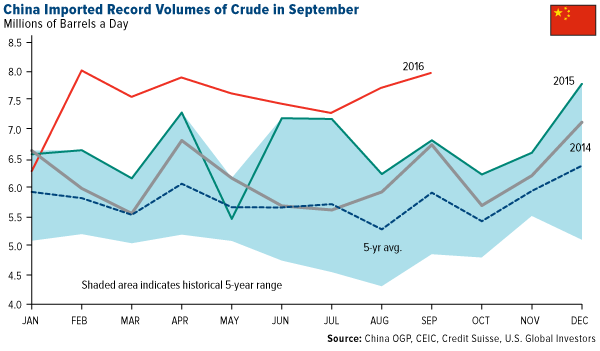

The country imported a record amount of crude oil in September, up 18 percent year-over-year, surpassing the U.S. for the second time in 2016. Averaging 8 million barrels a day, imports came close to the 8.6 million daily barrels the U.S. produces on average.

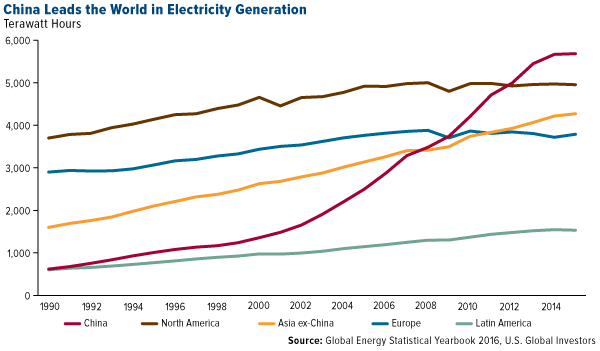

I also would like to point out that China remains the world’s number one generator of electricity. The chart below shows just how dramatic capacity growth was in the first decade of the century. In 1990, the country’s electricity needs were equivalent to Latin America’s, but as its government pushed ahead with fiscal spending for huge infrastructure projects, demand blew past the continents of Europe and North America.

Although infrastructure investment has declined overall from this period, there’s still plenty to get excited about. In the first eight months of 2016, infrastructure spending rose an impressive 19.7 percent over the same period last year, and in May, the government announced it would be pumping more than $721 billion into as many as 303 transportation projects over the next three years.

Two projects in particular are worth noting here. Construction on what will eventually be the world’s largest airport by surface area is currently underway in Beijing. Upon completion in 2019, the $12 billion airport, to be called Beijing Daxing International Airport, will serve as many as 100 million passengers a year, roughly in line with the world’s busiest airport, Hartsfield-Jackson Atlanta International Airport.

Then there’s the ongoing Belt and Road Initiative (BRI), one of the most ambitious undertakings in human history. With total infrastructure costs estimated at $5 trillion, the biblical-size trading endeavor—a sort of 21st century Silk Road—will cost 12 times as much as what the U.S. spent on the Marshall Plan to rebuild Europe following World War II. The initiative has the participation of 65 countries from Asia, Africa and Europe, and is poised to raise the living standards for more than half of the world’s population.

“Though China’s pace of expansion has slowed from the double-digit rates seen in the first decade of the century,” writes HSBC’s Noel Quinn, Chief Executive of Global Commercial Banking, “its global influence—as the world’s second-largest economy and a trading powerhouse—is far greater than 10 or even five years ago. The country’s overseas investments are only likely to increase, further underlining its pivotal role.”

HSBC: Your Candidate’s Win Could Reward Gold Investors

With the U.S. presidential election just four days away, London-based HSBC says gold investors should see a significant bump in price no matter who wins.

The bank sees a Trump victory more supportive of gold as a potential “protection against protectionism”—the New York businessman has been very critical of trade deals, including the North American Free Trade Agreement (NAFTA) and the proposed Trans-Pacific Partnership (TPP)—but a Clinton win could also help boost prices to as high as $1,400 by year end, HSBC says.

The yellow metal jumped above $1,300 an ounce this week after the Federal Reserve stayed pat on interest rates. It’s stayed in that range even with the mostly positive jobs report today, which tells me investors are feeling some anxiety as we draw closer to the election.

As always, I recommend a 10 percent weighting in gold—5 percent in bullion and coins, 5 percent in gold stocks. Rebalance every year.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.50 percent. The S&P 500 Stock Index fell 1.94 percent, while the Nasdaq Composite fell 2.77 percent. The Russell 2000 small capitalization index lost 2.04 percent this week.

- The Hang Seng Composite lost 1.44 percent this week; while Taiwan was down 2.57 percent and the KOSPI fell 1.85 percent.

- The 10-year Treasury bond yield fell 7 basis points to 1.77 percent.

Domestic Equity Market

Strengths

- Materials was the best performing sector for the week, declining 0.59 percent versus an overall decrease of -1.94 percent for the S&P 500.

- FMC Corp, a diversified research company in the chemical industry, was the best performing stock for the week, increasing 11.26 percent.

- Facebook crushed earnings this week. Earnings per share came in at $1.09 a share against expectations of $0.97 per share and revenue beat slightly at $7.01 billion against expectations of $6.92 billion for the quarter. Both daily and monthly active users also beat.

Weaknesses

- Technology was the worst performing sector for the week, falling by 2.87 percent versus an overall decrease of 1.94 percent for the S&P 500.

- First Solar, a provider of specialty solar energy solutions, was the worst performing stock of the week declining 20.07 percent on pricing pressures.

- Tronc crashed nearly 19 percent after Gannett terminated buyout talks. Gannett Media, owner of newspapers such as USA Today, has ended its pursuit of Tronc, the publisher of newspapers such as the LA Times and the Chicago Tribune, according to a statement from Gannett.

Opportunities

- Want a raise? Leave your job. Average hourly earnings appreciated 2.8 percent from a year earlier, the quickest pace in seven years. Ironically, rising wages are encouraging people to look for new employment triggering the number of people leaving jobs voluntarily to rise 12.1 percent. We haven’t seen numbers like these since 2006.

- HSBC thinks gold will go up no matter who wins the election. In a note to clients, James Steel, the chief precious-metals analyst at HSBC, wrote that a Clinton win means gold will go as high as $1,440 by the end of 2017 while a Trump win could propel the metal to $1,575 by the end of next year.

- U.S. jobs continued to improve in October and wage gains kept the current pace of growth, signs that the labor market and economy continue pushing forward.

Threats

- Hourly wage growth points to inflation above the Federal Reserve’s 2-percent target, Capital Economics economist Paul Ashworth writes in a note. “The solid gain in employment and the acceleration in average hourly earnings growth in October will increase expectations that the Fed will hike interest rates in December (assuming that the election doesn’t throw a spanner in the works.)” NOTE: Futures imply a 78-percent probability that the Fed will tighten in December.

- Earnings disappointments amid U.S. dollar strength represent a potential trigger for a near-term correction in U.S. equities.

- A number of drug wholesalers have reported earnings misses and provided disappointing guidance, specifically citing worse-than-expected generic drug pricing pressure. In light of this new information, which implies that company disclosed pricing pressure is worse than current government data show, the outlook for pharma drug-related shares has weakened.

The Economy and Bond Market

Strengths

- U.S. manufacturing saw a stronger-than-expected October. The Institute of Supply Management's purchasing managers’ index (PMI) came in at 51.9 for the month, above expectations of 51.7 and up from the prior month's 51.5. "After rebounding out of contractionary territory in September, the sustained advance in the ISM manufacturing PMI helps to confirm that the August deterioration was a short-lived blip," wrote Brittany Baumann, macro strategist at TD Securities.

- Automobile sales trounced expectations. According to Autodata, sales rose at a seasonally adjusted annual rate of 18.29 million. Analysts had estimated that total vehicle sales rose at a rate of 17.6 million, according to Bloomberg.

- October was a record-breaking month for deals. Merger-and-acquisition (M&A) volume totaled $489 billion in October, the highest monthly amount in at least 12 years, reported Bloomberg.

Weaknesses

- Outlays for U.S. construction projects fell 0.4 percent in September, the Commerce Department reported Tuesday. Economists polled by MarketWatch expected growth of 0.4 percent compared with an originally reported 0.7 percent fall in August. September spending of $1.15 trillion was 0.2 percent below a year ago. This is the first year-on-year decline in construction spending since July 2011.

- Chicago PMI fell more than expected. The index on Midwest business activity fell to 50.6, much lower than the 54.0 projected by economists.

- U.S. gasoline futures spiked over 11 percent after Colonial Pipeline shut down its main gasoline and distillates pipelines following an explosion and fire that killed a worker in Shelby, Alabama. The incident was the second time in two months the company had to close the crucial supply line to the U.S. East Coast.

Opportunities

- Accelerating wage growth and falling profit margins could actually result in higher U.S. investment spending. Business capex tends to increase during periods when the labor share of income is rising. This reflects the fact that business investment represents what economists call "derived demand” where firms typically expand capacity only when they feel that final demand for their goods or services will increase. The end result could be the emergence of a virtuous circle in which rising wages push up consumer spending, causing firms to hire more workers and invest in new capacity leading, in turn, to even faster wage growth.

- The Federal Reserve said this week that the case for a rate hike "continued to strengthen." Based on the language from the Fed, it appears that a December rate hike is highly likely.

- Global Manufacturing PMI rose to 52 in October versus 50 in September. The report showed broad-based expansion with 22 out of the 31 nations showing improved operating conditions. The solid gains in most of the PMIs in October suggest global growth will continue to improve in the fourth quarter.

Threats

- Municipal bonds posted the biggest monthly loss since the Taper Tantrum of 2013. State and local government bond prices have slid amid growing expectations that the Federal Reserve Board will resume raising interest rates as soon as December, halting a rally that had pushed yields to record lows. The Bloomberg Barclays Municipal Bond Index returned a loss of 1.13 percent in October which is the worst showing since August 2013 (when Ben Bernanke jarred investors with plans to scale back the central bank’s bond purchases). Bonds could suffer further if either the odds of a rate hike or the expectations of higher long-term interest rates increase.

- According to BCA, although the outlook for U.S. corporate bond default losses has improved, current spreads do not offer adequate compensation. The BCA model forecasts that the corporate default rate will moderate to 4.1 percent from 5.4 percent during the next 12 months, which is also consistent with Moody's baseline forecast. The default-adjusted spread explains the bulk of the variation in junk returns. In the best case scenario where the default rate improves, excess junk returns are predicted to be close to zero. In the pessimistic scenario, excess returns during the next 12 months are forecast to be deeply negative. Thus, while the default outlook is improving alongside a better outlook for economic growth, wider spreads are still required to make the risk/reward trade-off in junk bonds attractive.

- The U.S. presidential election next week will be biggest event of the week. The polls have narrowed to less than 2 percent, which is within the margin of error. A Trump victory (or an unclear result) will lead to greater volatility in global markets.

Gold Market

This week spot gold closed at $1,304.40, up $28.90 per ounce, or 2.27 percent. Gold stocks, however, as measured by the NYSE Arca Gold Miners Index, ended the week up by 4.92 percent. The U.S. Trade-Weighted Dollar Index finished the week down -1.41 percent.

| Date | Event | Survey | Actual | Prior |

|

Oct-31 |

Eurozone CPI Core YoY |

0.8% |

0.8% |

0.8% |

|

Oct-31 |

Caixin China PMI Mfg |

50.1 |

51.2 |

50.1 |

|

Nov-1 |

U.S. ISM Manufacturing |

51.7 |

51.9 |

51.5 |

|

Nov-2 |

ADP Employment Change |

165k |

147k |

202k |

|

Nov-2 |

FOMC Rate Decision |

0.50% |

0.50% |

0.50% |

|

Nov-3 |

U.S. Initial Jobless Claims |

256k |

265k |

258k |

|

Nov-4 |

U.S. Durable Goods Order |

-0.1% |

-0.3% |

-0.1% |

|

Nov-4 |

Change in Nonfarm Payrolls |

173k |

161k |

191k |

|

Nov-10 |

U.S. Initial Jobless Claims |

261k |

-- |

265k |

|

Nov-11 |

Germany CPI YoY |

0.8% |

-- |

0.8% |

Strengths

- The best performing precious metal for the week was silver, up 3.69 percent. Weakness in the U.S. dollar began to materialize this week, benefiting the precious metals sector.

- With polls increasingly tight ahead of the U.S. elections on November 8, gold upside will persist, according to a note from UBS this week. In fact, as seen in the chart below, the U.S. Mint has already seen gold-coin sales in the U.S. climb to the highest since January. Additional positive news for the yellow metal comes from HSBC who reports that physical gold demand from China remains steady with the SGE premium trading between $4 and $6 per ounce.

- Gold is heading for its longest run of weekly gains this week since the U.K.’s Brexit vote shook financial markets, reports Bloomberg, primarily on rising concern that presidential candidate Donald Trump may prevail over Hillary Clinton in next week’s election. The precious metal held near a one-month high as investors weighed the need for a haven against expectations of higher U.S. interest rates, Bloomberg continues.

Weaknesses

- The worst performing precious metal for the week was palladium, rising just 0.93 percent. A story from Equities.com this week on asteroid mining, noted that if humans were ever able to get their hands on just one asteroid, it would be a game-changer. Even if a small metalliferous asteroid could be harvested, it would contain more platinum group metals than what has been mined here on earth.

- Non-farm payrolls came in on Friday up 161,000, slightly missing expectations of 170,000. Earlier in the week the Institute for Supply Management said its Purchasing Managers’ Index pushed further into expansion territory in October, reports Kitco News, rising to a reading of 51.9. For now, gold is holding near its one-month gains.

- The trade gap in Turkey widened in September by the most this year, reports Bloomberg. The balance of gold shipments went from a surplus to a deficit. To be specific, the precious metals’ trade went from $520 million to $160 million. Russia is in a similar situation according to its Finance Ministry. The eight-month output for silver in the country fell 11 percent year-over-year and the output for gold fell 1.3 percent year-over-year, reports Bloomberg.

Opportunities

- HSBC says that the policy proposals from the two U.S. presidential candidates have “significantly different implications for gold and other assets.” If Clinton wins, the research group sees gold at $1,400 an ounce by year-end and around $1,440 an ounce in 2017. A Trump win, however, would be “decidedly gold-bullish,” the group writes. HSBC believes Trump could send gold prices to $1,500 relatively quick. Echoing these thoughts is a forecast from Citigroup which states that gold may rally to $1,400 an ounce if Trump wins the election.

- Hillary Clinton’s odds of winning the U.S. presidential election dropped from 82 percent to 71 percent on October 27 (the day prior to the FBI reigniting the email controversy), according to poll aggregator FiveThirtyEight. A Trump win or a sweep by the Democrats could send investors running, reports Bloomberg, much like the aftermath of the Brexit vote in June. So what does the election mean for commodities? According to Bloomberg, a Clinton win will put pressure on coal and oil because of her environmental policies, particularly in regards to combating climate change. If Trump wins, natural gas prices could suffer because coal is a beneficiary under Trump.

- Newmont Mining completed a $1.3 billion sale of its Indonesian copper and gold assets to a local consortium, reports Bloomberg. This deal reduces Newmont’s dependence on copper and narrows its geographic focus to the Americas, Africa and Australia, the article continues. The company has lowered its debt by 56 percent since 2013 and has generated $2.8 billion in asset sales.

Threats

- Bullion’s run in 2016 has slowed a bit in the second half of the year as the market gears up for higher U.S. borrowing costs. Although the FOMC made no moves during its meeting this week, the probability that it will hike rates in December has climbed to 71 percent from 59 percent, reports Bloomberg. “If policy makers signal stronger support for future rate hikes during the meeting, bullion prices could adjust very quickly,” Xu Wenyu, analyst at Huatai Futures Co. said.

- The CME Group will start London gold and silver spot contracts in January, reports Bloomberg. Scrutiny from regulators has shaken up the city’s over-the-counter trading, sending exchanges fighting for a share of London’s gold market, the article continues. “There is a risk that liquidity is split too thin,” David Govett, head of precious metals trading at Marex Spectron Group said. “With three exchanges, that will just be multiplied."

- The London Metal Exchange (LME) has laid out plans to expand in China, according to its top executives. Charles Li, who oversees Hong Kong Exchanges & Clearing Ltd., LME’s parent company, says that China is the bigger prize for the world’s top metals exchange, reports Bloomberg. “We want a lot of the small- and medium-sized players, who can trust that system we are building in China, to trickle into the international system,” Li said at a seminar in London this week. With the recent scrutiny of gold price fixing in London, hopefully new regulations will improve price transparency but not reduce liquidity.

Energy and Natural Resources Market

Strengths

- In last week’s Investor Alert, we made note of the tremendous outflows that took place in gold. This week, the tide has changed as gold gained 2.12 percent on the back of stabilized positioning in gold futures and in the SPDR Gold Shares ETF.

- The best performing sector for the week was the NYSE Arca Gold Miners Index. The index rose 5.1 percent, largely benefiting from gold’s best week since early June.

- Evolution Mining, an Australian gold company, was the best performing stock in the broader natural resources sector this week. The stock rose 14.2 percent on the back of favorable moves in the gold price.

Weaknesses

- OPEC’s October oil output set new records. OPEC’s oil output added pressure to the imbalanced global crude market as October’s production figures set fresh record highs. The organization is currently above its target range by 820,000 barrels per day on the back of volume recoveries in Nigeria and Libya.

- The worst performing sector this week was the S&P/TSX Composite Oil & Gas Exploration & Production Index. The index fell 4.9 percent as crude prices fell the most since early January.

- The worst performing stock for the week was Occidental Petroleum. The Houston-based company fell 9.6 percent in succession with the fall in oil prices this week.

Opportunities

- China’s Manufacturing PMI for the month of October sharply increased to a 27-month high as a result of the government’s initiatives in increased infrastructure and PPP project spending. These initiatives are based on China’s 13th five-year plan, which was initiated earlier in March.

- At Macquarie’s annual base metals summit in London this Monday, 400 attendees were cautiously optimistic about base metal prices in 2017. Delegates took part in a poll that gauged where they expect overall world and Chinese growth to be, and the sentiment has strengthened considerably compared to the past three summits.

- Earlier this week, the Colonial Gas Pipeline in Georgia unfortunately exploded. The pipeline is expected to reopen this weekend; however, this is a sign of how outdated the infrastructure in the U.S. is at present. A positive read-through for industrial and construction materials in the years to come.

Threats

- After a steady downtrend in inventory during the summer months, U.S. crude oil inventories took everyone by surprise this week, posting a 14.4 million build versus an estimate of 1.01 million. This is the highest weekly inventory build in 34 years.

- The ISM Manufacturing Index in New York has contracted for the 3rd month in a row. This is the worst streak of prints in seven years, a negative read-through for industrial materials demand.

- Many miners have come to depend on the uplift in resource prices as a “get out of jail card.” Miners have had a great year; however, the prosperity of some might be thrown into question if industrial metal prices are to pull back in the future.

China Region

Strengths

- Both the October China official Manufacturing PMI and the Caixin China Manufacturing PMI data came in solid this week at 51.2 (for both), beating respective expectations for prints of 50.3 and 50.1.

- Official China Non-manufacturing PMI came in at 54.0, ahead of last month’s 53.7, while the Caixin China Services PMI number (52.4) also rose from September’s 52.0 print.

- In October, Singapore PMI data came in at 50.2, slightly ahead of expectations for a 50.0 print but down from September’s 52.9.

Weaknesses

- South Korea has suffered of late from several high-profile troubles. These include Hanjin Shipping’s implosion and Samsung’s Galaxy Note 7 explosions, but the country now also must deal with fallout from a political scandal as President Park Guen-hye struggles with claims that her longtime friend Choi Soon-sil has also long interfered in the affairs of the state. Park’s approval rating has collapsed to a record-low 5 percent even as some opposition members are calling for her resignation.

- The Nikkei Philippines Manufacturing PMI dropped to 56.5 from the recent multi-month high of its 57.5 September print.

- Both imports and exports missed expectations in South Korea for the October period. Imports came in down 5.4 percent, worse than an anticipated decline of only 4.4 percent, while exports fell 3.2 percent, slightly below expectations for a decline of only 3.1 percent.

Opportunities

- Vietnam is reportedly closer to moving ahead in privatizing state-owned assets by selling stakes in companies like Saigon Beer Alcohol Beverage Co., Hanoi Beer Alcohol Beverage Corp. and Vietnam Dairy Products, according to Bloomberg News.

- This weekend we get third quarter Indonesia GDP data, and expectations are for a 5.08 percent growth rate. Indonesia’s ongoing Tax Amnesty Scheme (TAS) is designed, in the main, to bring in more tax revenue for the country to offset its continuing infrastructure build-out, and investors will be watching progress and growth in the country carefully.

- Myanmar could possibly become a net exporter of cement by 2018, reports Bloomberg News.

Threats

- China halted UnionPay card payments for most Hong Kong insurance policies this week as the country seeks further restrictions against potential outflows.

- U.S. monetary policy and interest rate speculation—as well as election outcomes—may play an outsized role in forthcoming months.

- In a step determined to curb the pace of rising property prices, the Hong Kong government raised the stamp duty on residential purchases to 15 percent for all buyers, regardless of resident or non-resident status.

Emerging Europe

Strengths

- Hungary was the best-performing country this week, gaining 72 basis points. Final October manufacturing PMI was reported at 57, slightly below the flash reading of 57.2. Bloomberg’s survey was expecting a much lower reading for October of only 53.8.

- The Hungarian forint was the best-performing currency this week, gaining 2.5 percent against the dollar. Moody’s credit rating agency will announce Hungary’s sovereign debt rating late on Friday, and most economists expect an upgrade to investment grade. Moody’s is the only credit rating agency which still has Hungary at Ba1 – the highest junk rating with positive outlook.

- The health care sector was the best-performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst-performing country this week, losing 5.2 percent. The president of Turkey, Recep Erdogan, is further cracking down on his party opposition. Eleven pro-Kurdish (HDP) party members were detained on charges of being linked to terrorist group PKK. The lira hit a new record low against the dollar.

- The Russian ruble was the worst-performing currency this week, losing 2.3 percent against the dollar. The Russian currency is highly correlated with the price of Brent crude oil, which lost 8.5 percent in the past five days.

- The consumer staples sector was the worst-performing sector among eastern European markets this week.

Opportunities

- The final eurozone manufacturing PMI for October was reported a little above the flash reading, at 53.5 versus 53.3, the best reading since January 2014. The improvement was due to France and Spain. Germany’s reading came a bit softer at 55.0 versus 55.1, but still way above the 50 mark that separates growth from contraction.

- Russian inflation surprised positively, declining to 6.1 percent in October from 6.4 percent on year-over-year basis. Easing inflation will allow the central bank of Russia to continue cutting its main rate. Oleg Kouzmin, Renaissance Capital economist, sees Russia gradually cutting 200 basis points toward 8 percent by the end of 2017, with the first rate cut happening in first quarter of next year.

- Klaus Regling, head of the European Stability Mechanism (ESM), said that Greece should get a short-term relief in interest payments by the end of the year. The ESM chief further mentioned that medium-term steps on debt would be taken when the current bailout program ends and could be followed by a longer term relief if Greece adheres to reforms.

Threats

- Many investors were badly surprised in June with Brexit, and some worry that the election outcome in the U.S. could end up as a big surprise too. If Hillary Clinton wins she most likely will continue policies of the current President Barack Obama, but Donald Trump is the change candidate. His plans to break up existing trade deals and to impose punitive tariffs on Chinese imports that could hurt smaller European countries, which depend on global trade. Also, Trump supports reducing commitments to NATO, giving encouragement to Moscow’s expansionistic instincts.

- According to Bloomberg’s survey, Poland has a 45 percent chance of expanding slower than 3 percent in 2016. Poland has kept up economic gains on no less than 3 percent every quarter into the third year, expanding 3.3 percent in 2014 and 3.9 percent in 2015.The outlook for the country has deteriorated in the year since the Law & Justice party came to power.

- Turkey is facing escalating political risk at home, increasing geopolitical tension in Syria and Iraq, currency depreciation, and an economic slowdown. In February, Fitch may decide to cut Turkey’s credit rating below the investment grade, which will put more pressure on the market.

© US Global Investors