The Two Faces of the U.S. Labor Market

- The Two Faces of the U.S. Labor Market

- Do ‘Strong Men’ Scare Away Investment?

- This Year’s Nobel Prize Goes to Contractors

Editor’s note: You can now follow our musings on ![]() Twitter @NT_CTannenbaum.

Twitter @NT_CTannenbaum.

When I arrived home one night a couple of weeks ago, I heard shouting coming from our kitchen. This isn’t altogether unusual; parents and teenagers periodically raise their voices when resolving differences. Yet I found that my wife and daughter weren’t shouting at each other, but rather at the telecast of one of the Presidential debates. Not wanting to enter the fray, I took my dinner out of the microwave and retreated to the basement.

Both Ms. Clinton and Mr. Trump claimed the upper hand in the three debates, but neither emerged as a clear winner. Knockout blows are rare in these sorts of encounters; one exception occurred in 1980, when Ronald Reagan looked into the camera and asked “Are you better off than you were four years ago?” Jimmy Carter, already teetering, fell figuratively to the electoral canvas.

Ever since then, the question Reagan posed has been a standard point of analysis during election season. More often than not, the employment picture is a key consideration. Overall, the news on this front is considerably better than it was four years ago. But underneath the surface, one can find lingering frustrations that are driving the electorate.

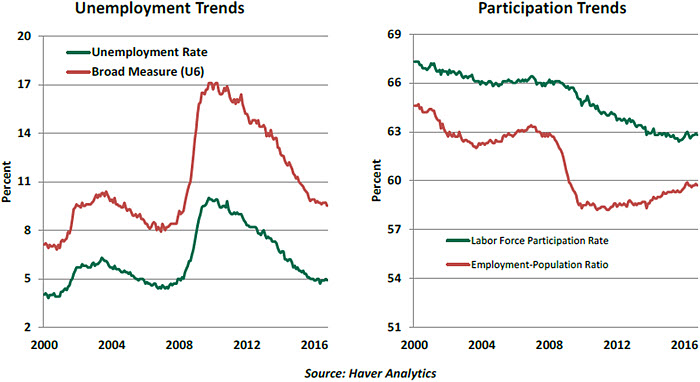

The October employment report was another in a long line of positive readings. A net of 161,000 new positions were created in October, putting the year-to-date average at 181,000. Hourly earnings recorded the best reading for the current expansion (+2.8% over the past year). Since 2009, 13.9 million jobs have been created and the official unemployment rate has fallen about 5 percentage points. The broadest measure of joblessness has reached another post-crisis low.

Employment is arguably the most important economic metric we follow. It is considered both a lagging indicator that reflects rising business confidence and a leading indicator of consumption. It has an elemental quality: one cannot suggest that an economy is performing well if it is not creating opportunities for its workforce.  Many observers, including the Federal Reserve, have been pleased with recent developments. Monthly job gains have not matched past cycles, but a critical difference this time around is the persistent decline in the labor force participation rate. Academic work has estimated that more than half of this drop is due to workers transitioning into retirement, a natural demographic progression. The ranks of those working part time because full-time work is not available has fallen, as has the number of “discouraged” workers who have stopped looking for jobs because prospects are poor.

Many observers, including the Federal Reserve, have been pleased with recent developments. Monthly job gains have not matched past cycles, but a critical difference this time around is the persistent decline in the labor force participation rate. Academic work has estimated that more than half of this drop is due to workers transitioning into retirement, a natural demographic progression. The ranks of those working part time because full-time work is not available has fallen, as has the number of “discouraged” workers who have stopped looking for jobs because prospects are poor.

Nonetheless, there are signs that the American labor market has not returned to full health:

- The ratio of those employed to the country’s total population is the lowest since 1984. There are those who view the retirement narrative with some skepticism; there are certainly those past 65 who might want or need work that aren’t finding it. Over the past 10 years, the labor force participation rate for those above retirement age has increased from 12% to nearly 20%; some think this should be even higher, but that opportunities are not available.

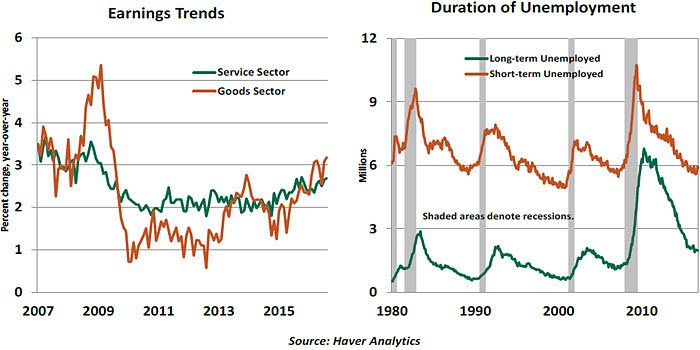

- Wages have grown very modestly during this expansion. Even after the increases of the last couple of years, the annualized advance in hourly earnings is still well below the peak seen during the last expansion. This has occurred in spite of measures that have raised minimum wages in some professions and regions. This suggests one of two things: either there is hidden scarcity in the labor supply that we are not measuring, or the jobs we are creating carry lower-than average wages.

- There remains a hardened core of long-term unemployed. While the ranks of those out of work fewer than 26 weeks has dropped substantially during the expansion, the number of workers unemployed for more than half a year is still higher than the peaks seen during past recessions. Further, labor force participation among 45-54 year olds without college education has fallen steadily over the past decade. It is safe to say few of these workers are retiring early and wealthy.

- Employment anxieties remain high in the United States. The Conference Board’s survey finds that 22% of those polled still feel that “jobs are hard to find.” When asked to identify the major problems facing the country, respondents rate employment in the top three. While trade has been fingered as a villain by some, the advance of technology is (as it has in the past) threatening to disrupt industries and their employees.

- What can be done to initiate broader-based improvements in the job market? Remedies will require a blend of good policy and personal responsibility.

- There are two steps that should probably not be taken toward this goal. The first is more monetary easing; Fed policy is a blunt instrument that may not be ideal to address the secular roots of lingering joblessness. Recognizing this, the Federal Open Market Committee is likely to raise interest rates next month. The second, as we discussed two weeks ago, is to close the borders to trade; this step has the potential to destroy jobs, not create them.

- More promising avenues might be additional support for retraining, fostering an environment conducive to new business formation and improving educational opportunities at the primary and secondary levels. These steps would all require coordination between the White House and Congress, which has been elusive over the past two decades. And to make these actions maximally effective, individual initiative will certainly be needed.

- The shouting that has dominated this campaign will soon be over, and not a moment too soon. One can only hope that raised voices will be replaced by reasoned reflection aimed at extending our great run of job creation. The country’s economy, and its social fabric, may depend on the success of this process.

A New Force in the Philippines

- A fair, reliable and predictable regime is essential for businesses—local or foreign—to invest in a country. It is particularly important for foreign direct investment (FDI), since it is neither easy nor inexpensive to pack up your operations and leave when the local situation turns adverse. The threat of instability can hamper the flow of capital.

- The rising temperature between the new Philippine president, Rodrigo Duterte, and the United States’ government underscores this risk. Though both countries have historically enjoyed deep political, defense and economic relations, President Duterte has been vocal about his plans to sever that relationship.

- While the government recently assured its full support of the American-dominated business process outsourcing (BPO) sector that employs 1.2 million people, there is disquiet among American businesses, and as a result, some American businesses are reevaluating their plans. It is highly likely that FDI inflows into the country will suffer despite the reassurances, and for good reason.

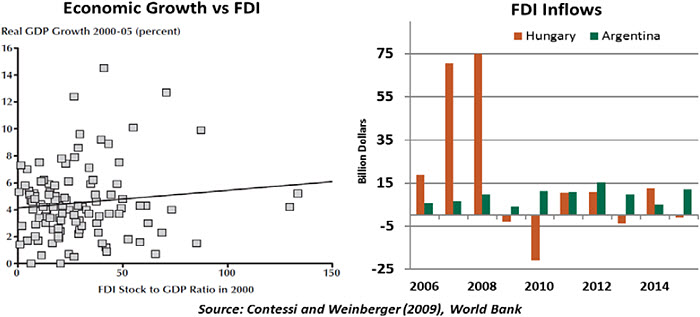

- History is littered with examples of governments appropriating or expelling foreign businesses, and even though global governance is better than it has ever been, there are rude reminders from time to time. In 2012, Argentina’s then-president, Cristina Fernández de Kirchner, nationalized YPF, a major Spanish oil company. Since 2010, Hungarian strong man Viktor Orbán has been imposing random levies and taxes on foreign investors to help balance the government’s books.

- In both cases, investors voted with their feet. FDI inflows to Argentina fell to a third within two years of the YPF episode, while Hungary has seen net FDI outflows in four of the last seven years.

- Foreign businesses often present politically expedient targets, falling victim to an intersection of nationalist mobilization, populist-socialism and weak public finances. Ironically, those very countries are most in need of foreign capital and expertise. In that, the new chapter opened by Argentina’s new president, Maurico Macri, and the recent change in signals coming out of Budapest are most welcome. All eyes are now on Manila.

Reading the Fine Print

- Contracts are a ubiquitous part of modern life. They cover a wide range of services that we use (communications, shelter, insurance) and relationships we have with others (business partners, employers, spouses). They are absolutely essential to the operation of economic systems.

- Contracts work well in some contexts, but not in others. Improperly specified, they can lead to bad outcomes. Studying the proper design and application of contracts earned professors Oliver Hart of Harvard University and Bengt Holmström of the Massachusetts Institute of Technology the 2016 Nobel Memorial Prize in Economic Sciences. While academic economic work is sometimes accused of being overly ethereal, Holmström and Hart have generated insights that apply to some very current topics.

- Professor Holmström’s research has focused significantly on the use of contracts in the workplace. Aligning the interests of shareholders, managers and workers is a key objective of any compensation system. Some employees receive a standard wage or salary, while others are covered by incentive arrangements. Holmström suggested that the form of remuneration should be geared as closely as possible to things the employee can control.

- Linking employee compensation directly to profits or the share price of the company tends to reduce the “agency problem” between shareholders and those who work for the firm. Devices that enforced this alignment, like incentive stock options, grew significantly in popularity in the 1980s and 1990s. But the design of these systems had important flaws: many workers had only limited ability to affect the bottom line, and gained or lost for reasons beyond their control. Professor Holmström’s work concludes that if it is difficult to tie an individual’s actions to a particular result, then compensation should be a fixed salary.

- Holmström also argued that improperly structured employment contracts can lead to poor outcomes. Holders of stock options who were more influential to corporate results occasionally engaged in behavior that maximized the share price at key junctures but were not always accretive to long-term value. Wells Fargo incented the creation of new accounts without placing sufficient stress on the need to conduct business according to laws and regulations, and this proved damaging. Paying traders big bonuses on short-term gains without recognizing the risk of reversal can also be dangerous. Deferred compensation and potential “claw back” of past earnings attempt to cure the misalignment.

- Professor Hart’s work illustrates the flaws in incomplete contracts. It is not possible to foresee all eventualities to specify in a contract, leaving them susceptible to failure. Most of us have homeowners or renters insurance, which (at least in theory) can lead us to be more careless about reducing risk where we live. If our contract with the provider mandates smoke detectors or offers a rebate for home security systems, it more completely aligns the incentives of the parties to the agreement.

- A similar situation exists in medical insurance, where co-payments and deductibles discourage overuse of care. If these features are too onerous, however, patients may choose not to get basic care that could head off more expensive therapies later on. Rebates on premiums for those who enter wellness programs have also become more common. The optimal structure of health insurance systems remains a very critical topic.

- Hart’s work also tackled the question of when functions should be performed in-house, and when they can be contracted out. Governments are increasingly turning to outsourcing to provide public services; policing, education, administration and prisons are examples. But it may be difficult to construct a contract that results in desired levels of quality while still producing economies. In these cases, public sector management is a better choice.

- The Nobel Economic Sciences Prize Committee has recently turned its attention to work on micro-level subjects instead of broader policy research. This is a welcome shift; in many cases, getting down to details can produce better outcomes.

© Northern Trust